Circle's listing has sparked market attention towards stablecoins, making Circle the first compliant stablecoin stock; however, behind the glamour, there are hidden crises.

After reviewing Circle's prospectus, it can be found that Circle faces three fatal problems:

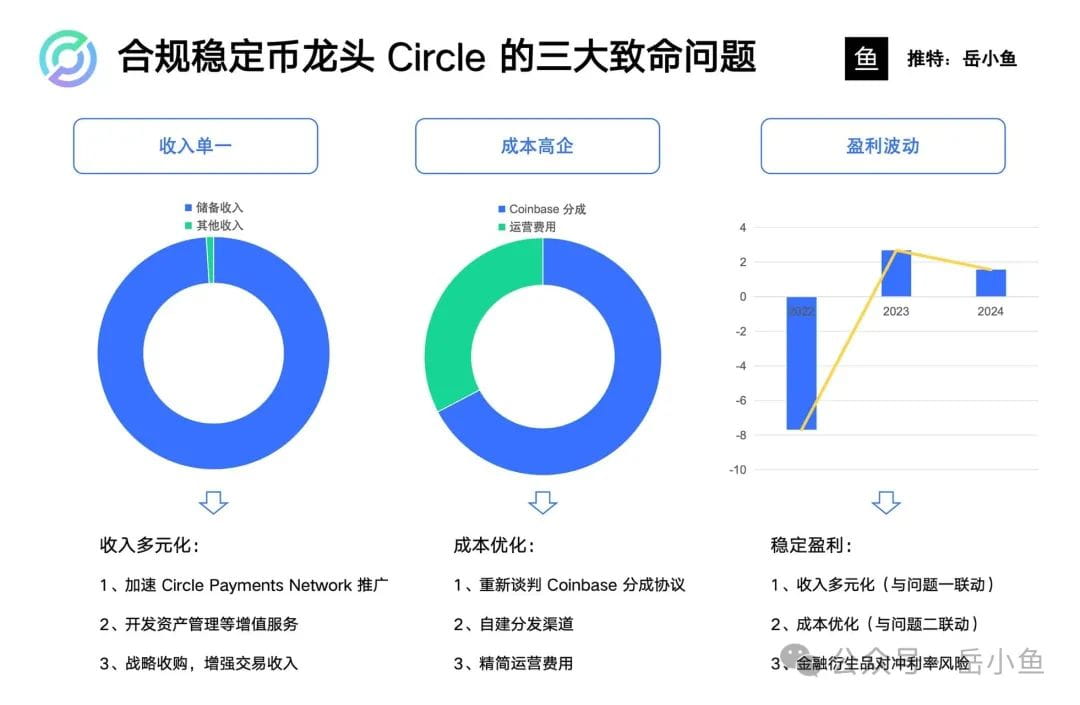

First, revenue is singular, with 99% coming from reserve income and only 1% from other revenues;

Second, high costs, with 60% of revenue going to Coinbase and a net profit margin of only 9%;

Third, profit fluctuations; profits are unstable, with a net loss of $770 million in 2022, a profit of $270 million in 2023, and a decline to $160 million in 2024.

Let's take a look at the underlying causes of these three major issues and what efforts Circle is making to address them.

1. Singular income

With 99% of income coming from reserve funds, this means Circle has no other profit points, which is a very obvious 'valuation ceiling' for a company.

Let's first look at this core business model:

The USDC issued by Circle is a stablecoin pegged to the U.S. dollar at a 1:1 ratio, supported by low-risk assets such as U.S. dollars and short-term government bonds.

When users hold USDC, Circle invests these funds in assets such as U.S. Treasury bonds to earn interest income, while USDC holders do not receive interest.

This model is essentially a form of 'interest-free financing'; Circle invests user funds without needing to pay costs, similar to how banks absorb deposits and then lend, but with lower risk (due to investments in government bonds rather than loans).

Circle's business model can be seen as digital dollar bond arbitrage.

Thus, Circle's profitability depends on two variables:

First, the circulation of USDC; the larger the circulation, the larger the scale of reserve assets, leading to higher interest income;

Second is the interest rate environment; U.S. Treasury yields directly determine reserve income, and a high interest rate environment is very favorable for Circle.

Although Circle has occupied the ecological niche of being the 'leader in compliant stablecoins' and can eat more cake as the track expands, now that the Federal Reserve has entered a rate-cutting cycle, U.S. Treasury bond yields may drop to 2% or lower, Circle's profits have been directly halved.

Furthermore, with more traditional finance entering the market and competitors (some emerging stablecoins) starting to pay interest to holders, Circle's 'interest-free financing' model will face challenges and may further lose market share in compliant stablecoins.

At this point, Circle only has reserve income as its profit point, so it cannot support a higher market value.

Circle's proposed solution is:

Accelerating the promotion of Circle Payments Network: Circle launched the Circle Payments Network in May 2025, aiming to provide instant, low-cost cross-border payment services using USDC, connecting banks, digital wallets, and payment service providers.

Developing value-added services: Developing USDC custody and asset management tools for institutional clients (such as crypto funds and banks) and charging management fees.

Exploring non-U.S. dollar stablecoins and emerging markets: Circle has issued EURC (Euro-pegged stablecoin) and plans to promote USDC and EURC in Asia and Latin America, where the growth in these new markets has been quite effective.

2. High costs

60% of Circle's revenue is given to Coinbase, primarily as distribution and promotional fees.

Among them, this revenue sharing ratio is a heavy burden for Circle.

Why does Circle give 60% of its revenue to Coinbase?

This relates to the development history of USDC, as Circle and Coinbase are the co-founders of USDC.

Circle is responsible for the issuance of USDC and the management of reserve assets, while Coinbase provides distribution channels, technical support, and marketing, with both parties sharing USDC reserve income (mainly from U.S. Treasury interest) based on agreements.

When USDC was first launched in 2018, Circle's brand and distribution capabilities were weak, relying on Coinbase's exchange status and user network to rapidly expand USDC's market share, thus giving Coinbase a dominant position in the cooperation.

Coinbase is the leader among U.S. compliant exchanges, possessing strong bargaining power.

Moreover, for a long time, USDC's circulation and trading volume have highly relied on Coinbase's infrastructure, making it difficult for Circle to break away in the short term.

For example, in 2024, based on a total circulation of $32 billion, Coinbase contributed about 50%-60% of USDC's circulation, approximately $16-19.2 billion.

In the cooperation agreement between Circle and Coinbase, there is actually a quite interesting clause:

If Circle cannot distribute this dividend to Coinbase in certain situations, or if there are regulatory issues, Coinbase has the right to become the issuer of USDC itself, meaning it can take USDC and become the issuer.

Although USDC is now fully issued and operated by Circle, Coinbase still plays a relatively important role.

Circle has also recognized the long-term risks of high commission rates, so it has taken measures such as renegotiating commission agreements and building its own distribution channels.

For the former, renegotiating the commission agreement is still difficult due to legal constraints, making it hard for Circle to break free from these limitations;

The latter, building its own distribution channels, can still effectively alleviate the profit pressure from high commissions.

3. Profit fluctuations

It must be acknowledged that the market value scale of stablecoins is still strongly correlated with the cyclical fluctuations of the cryptocurrency industry.

The bull and bear cycles of the cryptocurrency market directly affect the overall size of the stablecoin market.

Circle reported a net loss of $768.8 million in 2022, primarily due to the crypto bear market;

In 2023, a profit of $267.6 million was achieved, attributed to cost control and rising interest rates;

In 2024, it is expected to fall to $155.7 million due to soaring distribution costs.

We can review the changes in USDC issuance, which have several key milestones:

The first milestone is the DeFi summer of 2020, when USDC's issuance reached $55 billion;

The second milestone is the collapse of UST in 2022, which saw a massive influx of funds into USDC, allowing its market value to maintain for a long time, even in the crypto bear market;

The third milestone is the strong rise of Solana in early 2023, which led to good growth for USDC compared to USDT;

The fourth milestone is the March 2023 collapse of Silicon Valley Bank, coupled with unfavorable regulatory policies from the U.S. SEC, which caused USDC's issuance volume to drop by about 30%, and by the end of 2023, it fell by about 50%.

The fifth milestone is when Trump won the election, leading to a surge in stablecoins, with USDC growing to over $60 billion, an overall increase of 80%.

Thus, we can see that the bull and bear cycles of the cryptocurrency market are extremely important for the growth of stablecoins, and the impact of policies on stablecoins with compliance as the main selling point is also extremely significant, especially for compliant stablecoins like USDC.

To mitigate profit fluctuations, Circle needs to address issues related to both the first and second problems; on one hand, diversifying income to reduce dependence on interest rates, and on the other hand, optimizing costs to stabilize profit margins.

More critically, Circle can leverage its compliance advantages to solidify its market position in response to fluctuations in the crypto market.

To summarize

Stablecoins can be seen as a revolution in the traditional financial system.

Stablecoins are a very critical infrastructure that can replace SWIFT, bank settlement, and the foreign exchange system.

Circle's vision goes far beyond issuing stablecoins; Circle aims to build a new financial system, with USDC being the core of this new financial system.

However, Circle also has many issues, especially the three fatal problems mentioned above, which need to be resolved by Circle.

Regardless of the outcome, Circle's listing has set a benchmark for the crypto industry and is motivating more people to pay attention to stablecoins; we can continue to monitor this transformation of the financial system.