Written by: Shenchao TechFlow

On August 4, Lido co-founder Vasiliy Shapovalov announced a 15% layoff.

In the current context where almost everyone believes that an institution-driven ETH bull market is imminent, and the SEC has shown signs of approving ETH spot ETF staking applications, this news clearly contradicts everyone's expectations.

As one of the leading projects in the ETH staking track, Lido may be seen as the biggest beneficiary of the SEC's approval of ETH staking ETF news, but is that really the case?

Lido's layoffs are not just a simple organizational adjustment, but a microcosm of the entire decentralized staking track facing a turning point.

The official explanation is 'for long-term sustainability and cost control,' but behind it reflects a deeper industry change:

As ETH continues to flow from retail investors to institutions, the survival space for decentralized staking platforms is being increasingly compressed.

Let’s rewind to 2020, when Lido just launched, and ETH 2.0 staking had just begun. The 32 ETH staking threshold deterred most retail investors, but Lido's innovation of liquid staking tokens (stETH) allowed anyone to participate in staking while maintaining fund liquidity. This simple and elegant solution enabled Lido to grow into a staking giant with over $32 billion in TVL in just a few years.

However, in the past two years, changes in the crypto market have shattered Lido's growth myth. As traditional financial giants like BlackRock start to lay out ETH staking, institutional investors are reshaping this market using a familiar set of methods. Key players in this institution-driven ETH bull market have offered their own solutions: BMNR chose Anchorage, SBET chose Coinbase Custody, and BlackRock's ETFs all adopted offline staking.

Without exception, compared to decentralized staking platforms, they prefer centralized staking solutions. Behind this choice are compliance considerations and risk preferences, but the ultimate result points to one thing: the growth engine of decentralized staking platforms is 'stalled.'

Institutions move left, decentralized staking moves right

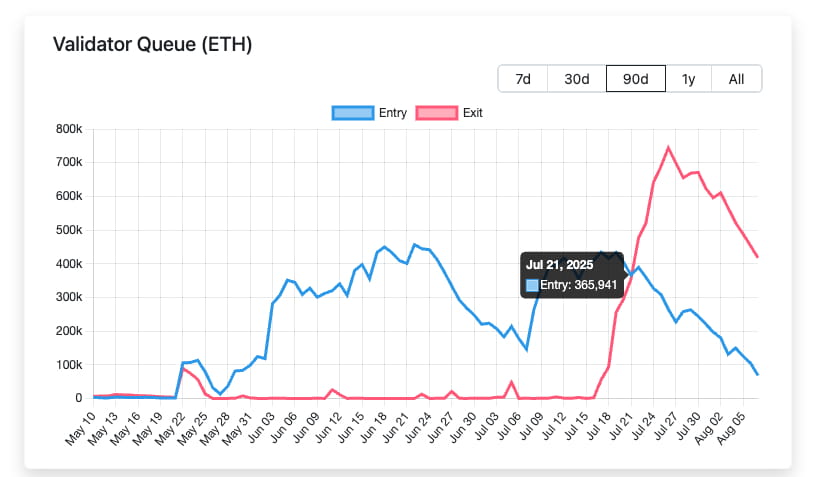

To understand the logic behind institutions' choices, we need to look at a set of data: starting from July 21, 2025, the number of ETH queued for unstaking began to significantly exceed the number entering staking, with the largest difference reaching 500,000 ETH.

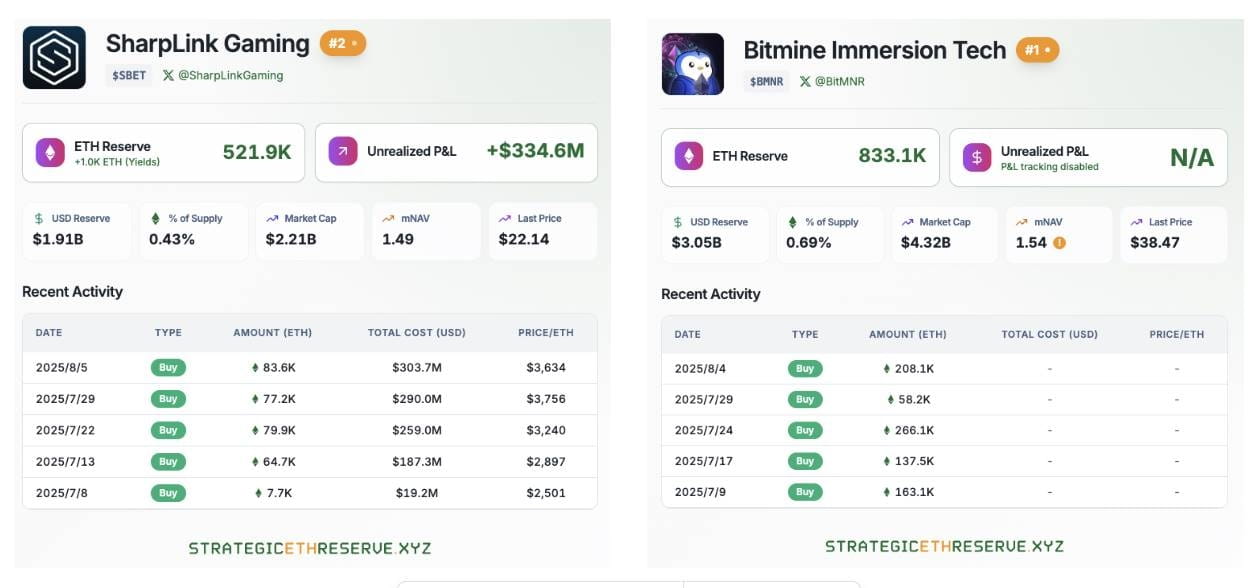

At the same time, ETH strategic reserve companies led by BitMine and SharpLink are continuously purchasing ETH in large quantities, with the current total number of ETH held by just these two companies exceeding 1.35 million ETH.

Institutions like BlackRock on Wall Street have also been continuously purchasing after the SEC's approval of the ETH spot ETF.

Based on the above data, it is undoubtedly concluded that ETH is continuously flowing from retail investors to institutions. This drastic change in holding structure is redefining the rules of the entire staking market.

For institutions managing billions of dollars in assets, compliance is always the top priority. When reviewing BlackRock's ETH staking ETF application, the SEC also clearly required that applicants must be able to demonstrate the compliance, transparency, and auditability of their staking service providers.

This precisely strikes at the Achilles' heel of decentralized staking platforms, as node operators of decentralized platforms like Lido are distributed globally. While this decentralized structure enhances the network's censorship resistance, it also complicates compliance review significantly. Imagine when regulators require KYC information for each validating node, how will decentralized protocols respond?

In contrast, centralized solutions like Coinbase Custody are much simpler. They have clear legal entities, comprehensive compliance processes, traceable fund flows, and even insurance coverage. For institutional investors who need to report to LPs, the choice is obvious.

When evaluating staking programs, institutional risk control departments focus on one core question: Who is responsible if something goes wrong?

In Lido's model, losses caused by node operator errors will be shared among all stETH holders, and it may be difficult to hold specific responsible parties accountable. However, in centralized staking, service providers bear clear compensation responsibilities and even offer additional insurance protection.

More importantly, institutions need not only technical security but also operational stability. When Lido changes node operators through DAO voting, this 'people's vote' becomes a source of uncertainty in the eyes of institutions. They prefer to choose a predictable and controllable partner.

Regulatory easing, but not entirely favorable

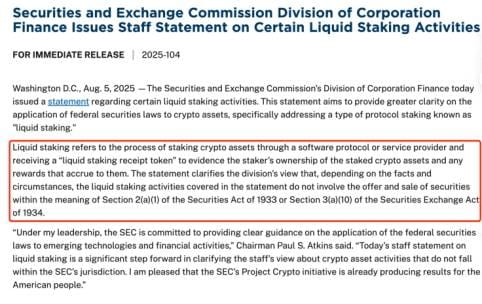

On July 30, the SEC announced it had received BlackRock's ETH staking ETF application. Just on August 5, the SEC released new guidance: specific liquid staking does not fall under the jurisdiction of securities law.

It seems that everything is developing positively; on the surface, this is the long-awaited good news for decentralized staking platforms, but a deeper analysis reveals that it may also be the sword of Damocles hanging over all decentralized staking platforms.

The short-term benefits brought by regulatory relaxation are obvious. Mainstream decentralized staking platform tokens like Lido and ETHFI surged over 3% immediately after the announcement. As of August 7, the PRL liquid staking asset increased by 19.2% within 24 hours, while SWELL rose by 18.5%. The price increase reflects the market's optimistic expectations for the LSD track, and more importantly, the SEC's statement has cleared compliance obstacles for institutional investors.

For a long time, traditional financial institutions have been primarily concerned about the potential risks of securities law when participating in staking activities. Now, this cloud has been largely dissipated, and it seems that SEC approval for ETH staking ETFs is just a matter of time.

However, behind this thriving scene lies a deeper crisis in the track.

The SEC's regulatory easing not only opens doors for decentralized platforms but also paves the way for traditional financial giants. When asset management titans like BlackRock start launching their own staking ETF products, decentralized platforms will face unprecedented competitive pressure.

The asymmetry of this competition lies in the gap of resources and channels. Traditional financial institutions have mature sales networks, brand trust, and compliance experience, which decentralized platforms find difficult to compete with in the short term.

More critically, the standardization and convenience of ETF products have a natural appeal to ordinary investors. When investors can purchase staking ETFs with one click through familiar brokerage accounts, why would they go through the trouble of learning how to use decentralized protocols?

The core value proposition of decentralized staking platforms—decentralization and censorship resistance—seems weak in the face of institutional waves. For institutional investors pursuing yield maximization, decentralization is more of a cost than an advantage. They care more about yield, liquidity, and operational convenience, which are precisely the strengths of centralized solutions.

In the long run, regulatory easing may accelerate the 'Matthew Effect' in the staking market. Funds will increasingly concentrate on a few large platforms, while smaller decentralized projects will face survival crises.

A deeper threat lies in the disruption of business models. Traditional financial institutions can lower fees through cross-selling, economies of scale, and even offer zero-fee staking services. In contrast, decentralized platforms rely on protocol fees to maintain operations and are at a natural disadvantage in price wars. How will a decentralized platform with a single business model respond when competitors can subsidize staking services through other business lines?

Therefore, while the SEC's regulatory easing brings opportunities for market expansion to decentralized staking platforms in the short term, in the long run, it is more like opening Pandora's box.

The entry of traditional financial forces will completely change the rules of the game, and decentralized platforms must find a new way to survive before being marginalized. This may mean more radical innovations, deeper DeFi integrations, or—ironically—a certain degree of centralized compromise.

At this moment of regulatory spring, decentralized staking platforms may not be facing a time for celebration, but rather a turning point for survival.

The risks and opportunities of Ethereum's staking ecosystem

Standing at the critical juncture of 2025, the Ethereum staking ecosystem is undergoing unprecedented transformations. Vitalik's concerns, shifts in regulation, and the entry of institutions—these seemingly contradictory forces are reshaping the entire industry landscape.

Indeed, challenges are real. The shadow of centralization, intensified competition, and impacts on business models could each become the last straw that breaks the decentralized ideal. But history tells us that true innovation often emerges from crises.

For decentralized staking platforms, the institutional wave is both a threat and a driving force for innovation. When traditional financial giants bring standardized products, decentralized platforms can focus on deep integration within the DeFi ecosystem; when price wars become inevitable, differentiated services and community governance will become new moats; when regulation opens the door for everyone, the importance of technological innovation and user experience will be further highlighted.

More importantly, the expansion of the market means the pie is getting bigger. When staking becomes a mainstream investment choice, even niche markets can support the prosperous development of multiple platforms. Decentralization and centralization do not have to be a zero-sum game; they can serve different user groups and meet different needs.

The future of Ethereum will not be determined by a single force, but shaped collectively by all participants.

As tides rise and fall, only the fittest survive. In the crypto industry, the definition of 'fittest' is far more diverse than in traditional markets, which may be the reason we should remain optimistic.