Author: Gate Research Institute

Abstract

•Stablecoins are classified into three types according to the price anchoring methods: fiat-collateralized stablecoins, crypto-collateralized stablecoins, and algorithmic stablecoins.

•Currently, the global market value of stablecoins has reached 260.728 billion USD, accounting for about 1% of the nominal GDP of the United States in 2024. The number of users holding stablecoins has exceeded 170 million, representing about 2% of the global population, widely distributed across more than 80 countries and regions.

•Countries' governments are increasingly emphasizing stablecoin regulation, with core legislative motivations encompassing financial stability, currency sovereignty, and cross-border capital regulation. The U.S., Hong Kong, and other economies have successively introduced systemic regulatory regulations, and global stablecoins have entered an era of strong regulation, reshaping international financial order and monetary power structures.

•The rise of stablecoins reflects a covert competition for currency sovereignty and financial hegemony. As a strategic core resource intersecting financial sovereignty, financial infrastructure, and capital market pricing power, stablecoins have become a focal point of financial governance.

•While stablecoins enhance financial efficiency, they still face challenges such as anchoring mechanism risks, decentralization conflicts, and cross-border regulatory coordination.

Introduction

On July 18, 2025, the U.S. House of Representatives passed the (GENIUS Act) with a vote of 308 in favor and 122 against, and the (CLARITY Act) regulating the structure of the crypto market has been submitted to the Senate, while another bill opposing CBDC (Central Bank Digital Currency) has passed the House vote.

Outside the United States, countries are increasingly introducing stablecoin policies: Hong Kong will implement the Stablecoin Regulation on August 1, Russia's central bank provides crypto custody, and Thailand has launched a cryptocurrency sandbox. These developments mark the entry of stablecoins into the regulatory era, officially starting the great power game over stablecoins.

Given that stablecoin legislation has become a focal point of financial governance, this article aims to analyze the reasons behind various countries' government stablecoin legislation, compare the similarities and differences in the bills, and analyze the impact of stablecoin compliance on the existing financial order, providing reference opinions for industry builders and investors' decision-making. It is recommended that investors closely monitor regulatory trends, focus on participating in fiat-backed stablecoins, avoid compliance risks associated with algorithmic stablecoins, and traditional financial institutions should adapt to the trend of asset tokenization and explore more opportunities, while crypto institutions should continuously advance compliance progress.

1.1 Definition and classification of stablecoins

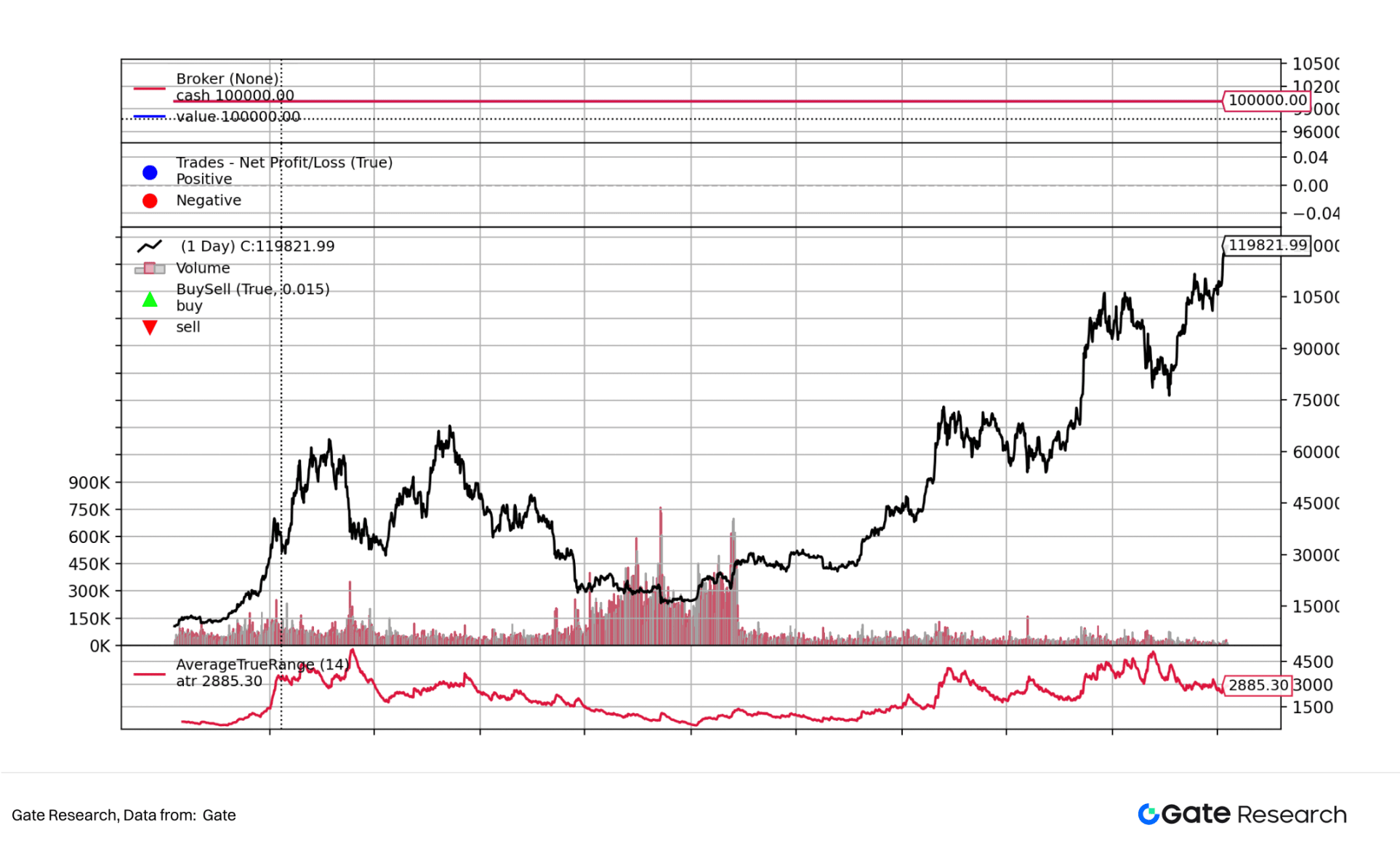

The following chart shows the BTC price curve and the 14-day ATR curve, demonstrating that the volatility of traditional cryptocurrencies, primarily BTC, is excessively high, hindering the promotion and application of cryptocurrencies. Stablecoins emerged in 2014 to address this issue, aiming to maintain price stability.

Stablecoins typically achieve value anchoring by linking to fiat currencies, commodities, or other cryptocurrencies, or by utilizing algorithmic adjustment mechanisms. They are widely used as core mediums in digital asset trading, DeFi applications, and cross-border payments.

Based on price maintenance methods, stablecoins can be divided into three types:

•Fiat-backed stablecoins

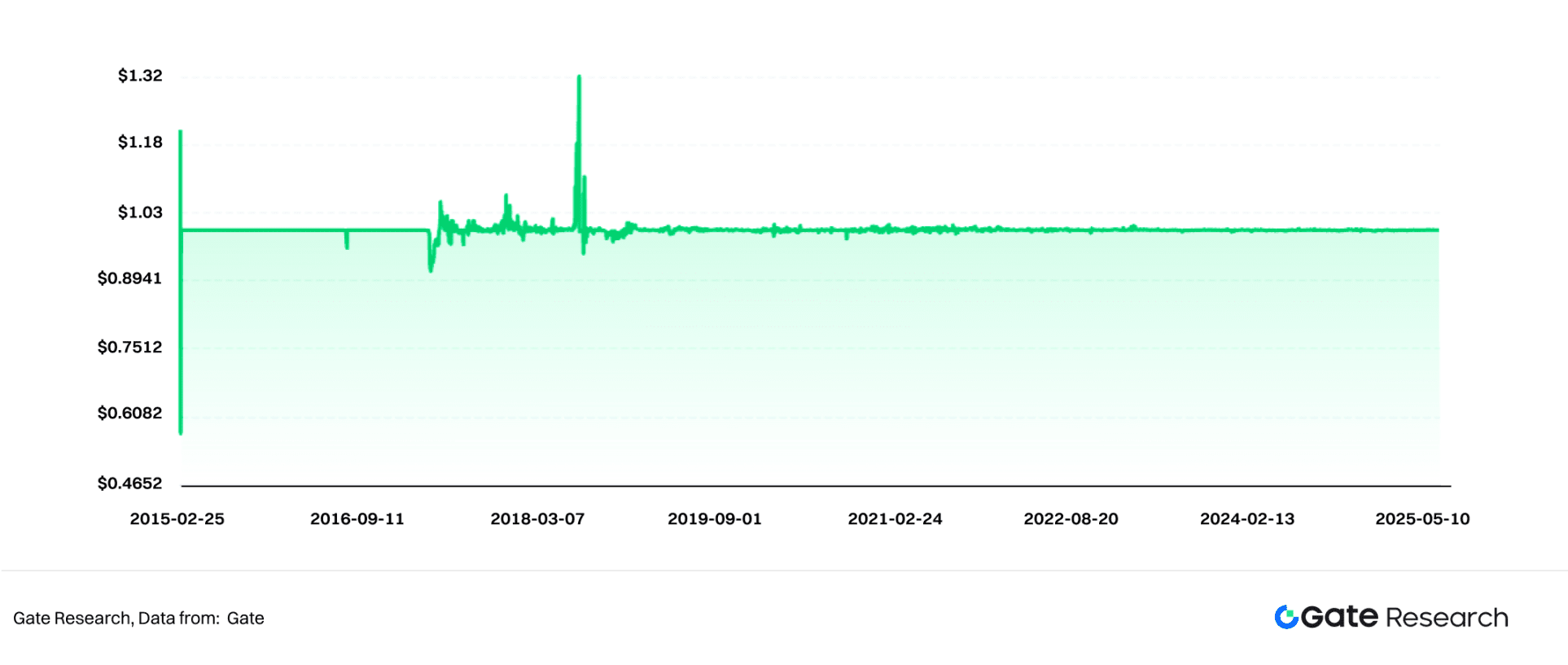

Fiat-backed stablecoins are the most common type of stablecoins, accounting for 92.4% of the market share. They achieve price stability by pegging tokens to fiat currencies like the USD. Issuers deposit fiat money or highly liquid assets (like government bonds) into banks or custody accounts, then mint and issue tokens at a 1:1 ratio. Examples include USDT and USDC; the following chart shows the price curve of USDT.

•Crypto-backed stablecoins

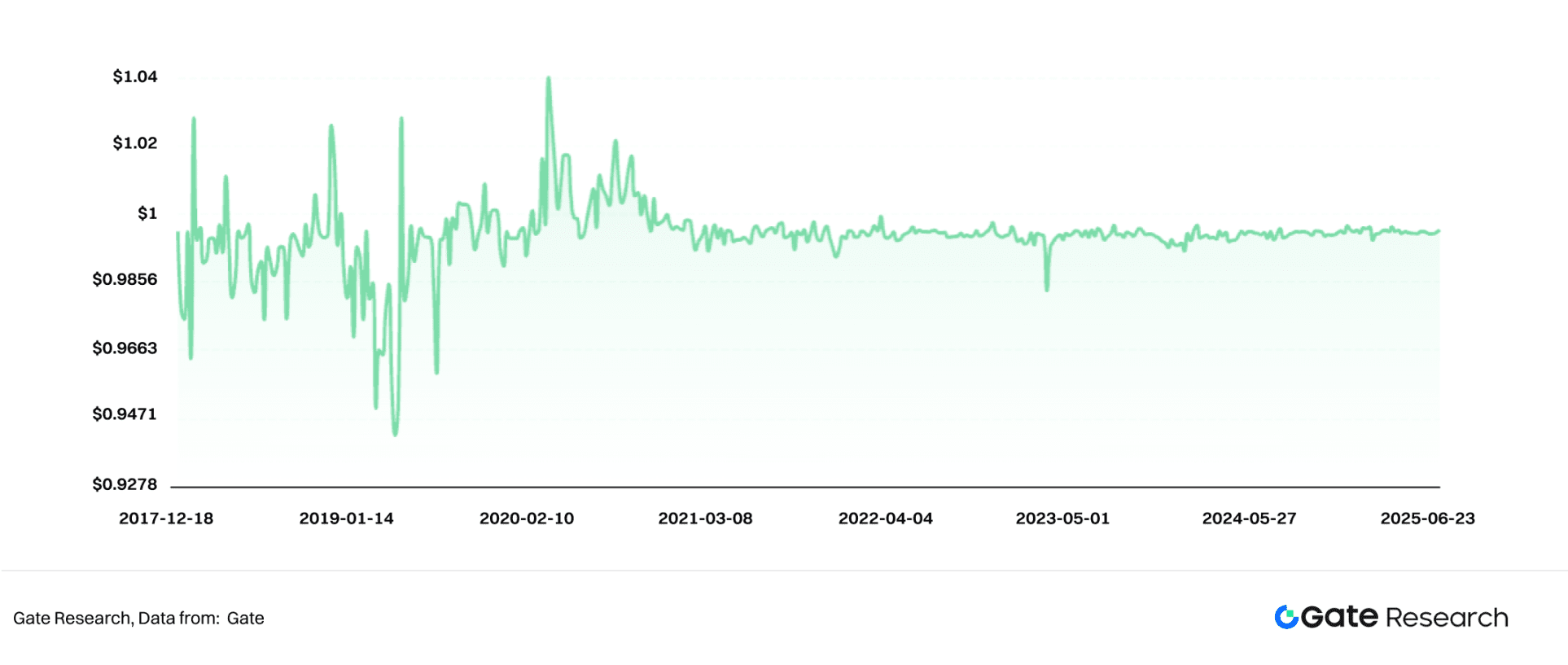

Unlike fiat-backed stablecoins, crypto-backed stablecoins are collateralized by cryptocurrencies, which tend to be highly volatile, often using an over-collateralization method (with a collateralization rate typically around 150%) and introducing on-chain liquidation mechanisms to maintain stablecoin value. For example, DAI issued by MakerDAO (Sky) allows users to mint DAI tokens by over-collateralizing ETH. The following chart shows the price curve of DAI.

•Algorithmic stablecoins

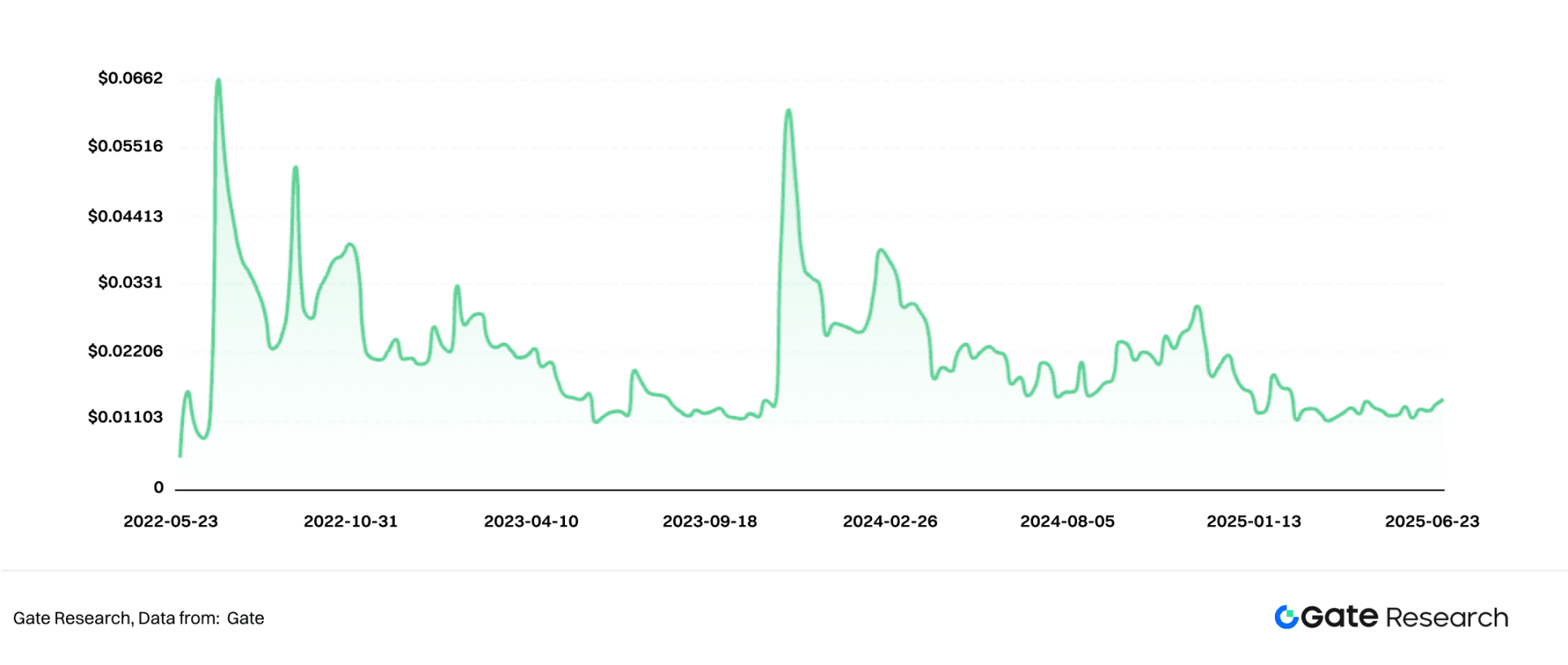

These types of stablecoins do not rely on physical assets for support but instead use algorithms and market supply-demand dynamics to maintain the token price. When the token price exceeds 1 USD, the system will increase the token supply to lower the price; when the price drops below 1 USD, the system will buy back and destroy tokens to raise the price. For example, UST (which has collapsed) has become an independent cryptocurrency that is no longer pegged to the USD as of 2025. The following chart shows the price curve of USTC.

Comparison chart of three types of stablecoins

1.2 Characteristics of stablecoins

The unique value anchoring mechanism of stablecoins distinguishes them from the severe volatility of traditional cryptocurrencies, thus they are widely regarded as 'digital cash' or 'bridge assets' within the crypto asset ecosystem. They have the following characteristics:

•Price stability

By linking to stable assets like the USD or gold, or adopting over-collateralization and algorithmic adjustment mechanisms, stablecoins achieve lower price volatility, possessing stronger store of value and medium of exchange attributes.

•Bridging traditional finance and decentralized finance (DeFi)

Stablecoins are issued on a blockchain with traditional finance as the underlying asset, allowing interaction with on-chain protocols and tools, especially playing important roles in core applications such as DeFi lending, liquidity mining, and derivatives trading.

•Lower payment costs and higher efficiency

Leveraging blockchain technology, stablecoins can achieve near-real-time cross-border transfers, with transaction fees significantly lower than traditional banking systems, and without geographic or time restrictions, markedly improving the efficiency of capital flow.

•Anti-inflation and capital hedging

Most stablecoins are pegged to USD assets, which means they share the same inflation characteristics as the USD. In countries with severe inflation or currency devaluation (such as Argentina and Turkey), stablecoins have become an important means for residents to hedge risks and preserve assets due to their stability. In certain regions of Africa and Latin America, stablecoins have become tools for everyday payments.

1.3 Major application scenarios

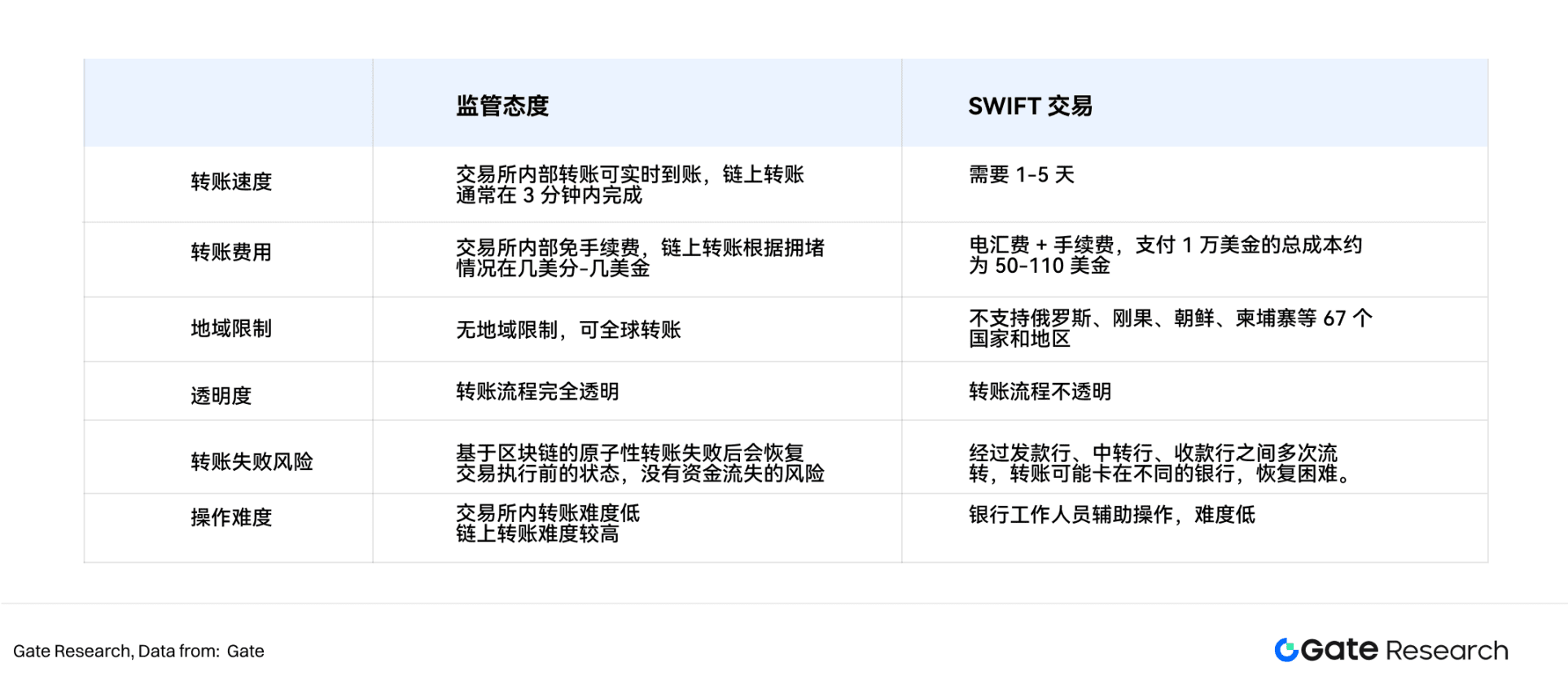

Based on the characteristics of stablecoins mentioned above, they are currently applied in multiple scenarios such as decentralized finance, cryptocurrency trading, cross-border trade, daily payments, and capital hedging. Among these, cross-border trade is a key area of focus in the recent U.S. and Hong Kong legislation. Using stablecoins for transactions can effectively avoid problems of currency inflation in certain countries, and their payment costs and efficiency are far superior to traditional SWIFT systems.

Legislative background

2.1 The rise of stablecoins

Currently, the global market value of stablecoins has reached 260.728 billion USD, surpassing the market value of MasterCard, accounting for about 1% of the nominal GDP of the United States in 2024, making it an important component of the international financial system that cannot be ignored. The penetration rate of stablecoins worldwide continues to rise, with over 170 million users holding stablecoins, representing about 2% of the global population, widely distributed in more than 80 countries and regions.

2.2 Motivations for government intervention in regulation

Governments worldwide are actively intervening in stablecoin regulation, motivated not only by the prevention of financial risks but also by core interests related to currency sovereignty, financial security, and cross-border capital control, as well as mitigating fiat currency credit risks.

•Preventing systemic financial risks: Avoiding the loss of control over stablecoins leading to disruptions in payment systems and capital markets, and preventing the spillover of risks similar to the 2008 shadow banking crisis.

•Maintaining currency sovereignty and financial order: Preventing private stablecoins from replacing fiat currencies in domestic circulation, thereby weakening central banks' control over monetary policy and payment systems.

•Combating illegal cross-border capital flows: Stablecoins can bypass regulatory systems like SWIFT, with governments concerned about their potential misuse in money laundering, tax evasion, and sanctions evasion.

•Hedging against the impact of 'USD stablecoin hegemony': The U.S. promotes USDT/USDC to become 'on-chain dollars,' while other countries explore local currency stablecoins (HKD, Euro, RMB) through legislation to counteract.

•Mitigating fiat credit risks and supporting government bonds: By 2025, the market value of USD stablecoins has exceeded 260 billion USD, with U.S. Treasuries generally accounting for over 60%-80% of reserve assets. The demand for stablecoin reserves has become an important buyer of U.S. Treasuries, providing continuous support for USD credit.

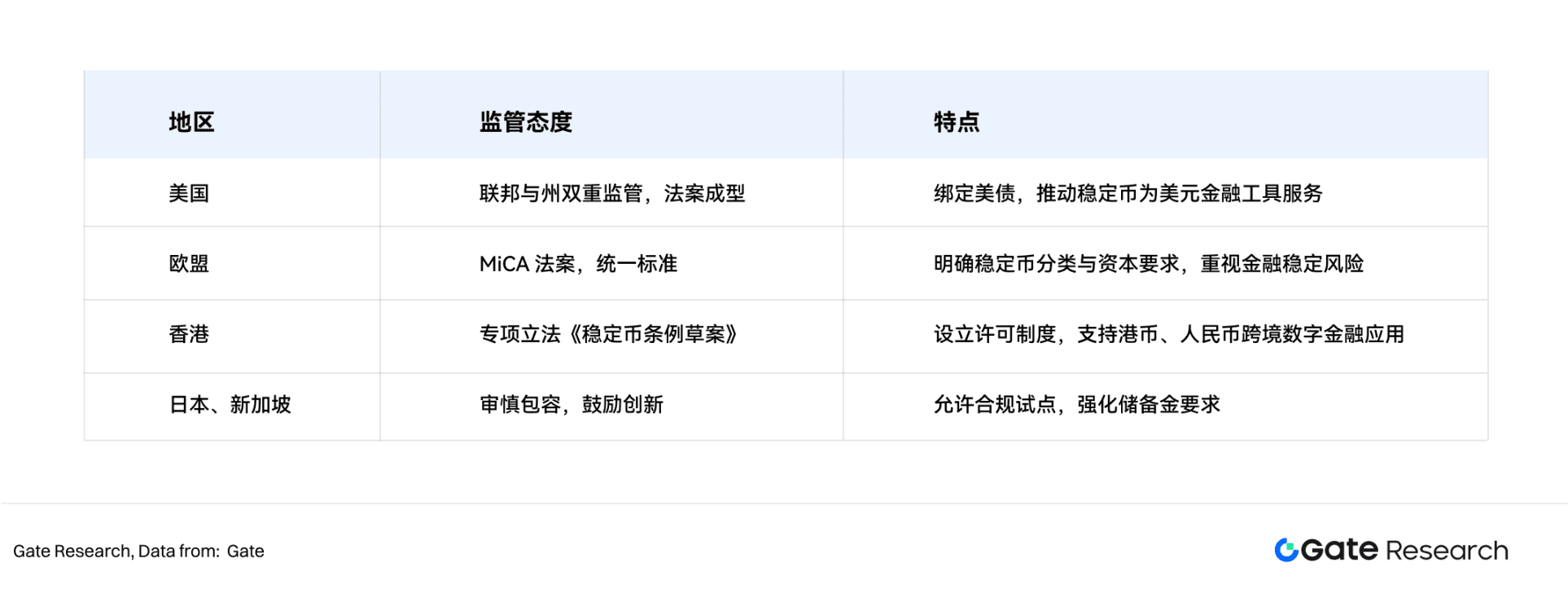

In order to strengthen the international status of their currencies, protect consumer asset safety, seize discourse power in the digital asset field, and address the lack of regulation of stablecoins, the U.S., Hong Kong, Europe, and others have successively introduced systematic regulatory regulations. The stablecoin industry has officially entered an era of strong regulation and compliance.

Progress of stablecoin regulation among major global economies

Since 2022, with the expansion of stablecoins in the global market, countries have successively issued related regulations for oversight. The following chart shows the timeline of stablecoin regulatory progress across countries:

3.1 The U.S. introduces the (Genius Act) and the (Clarity Act)

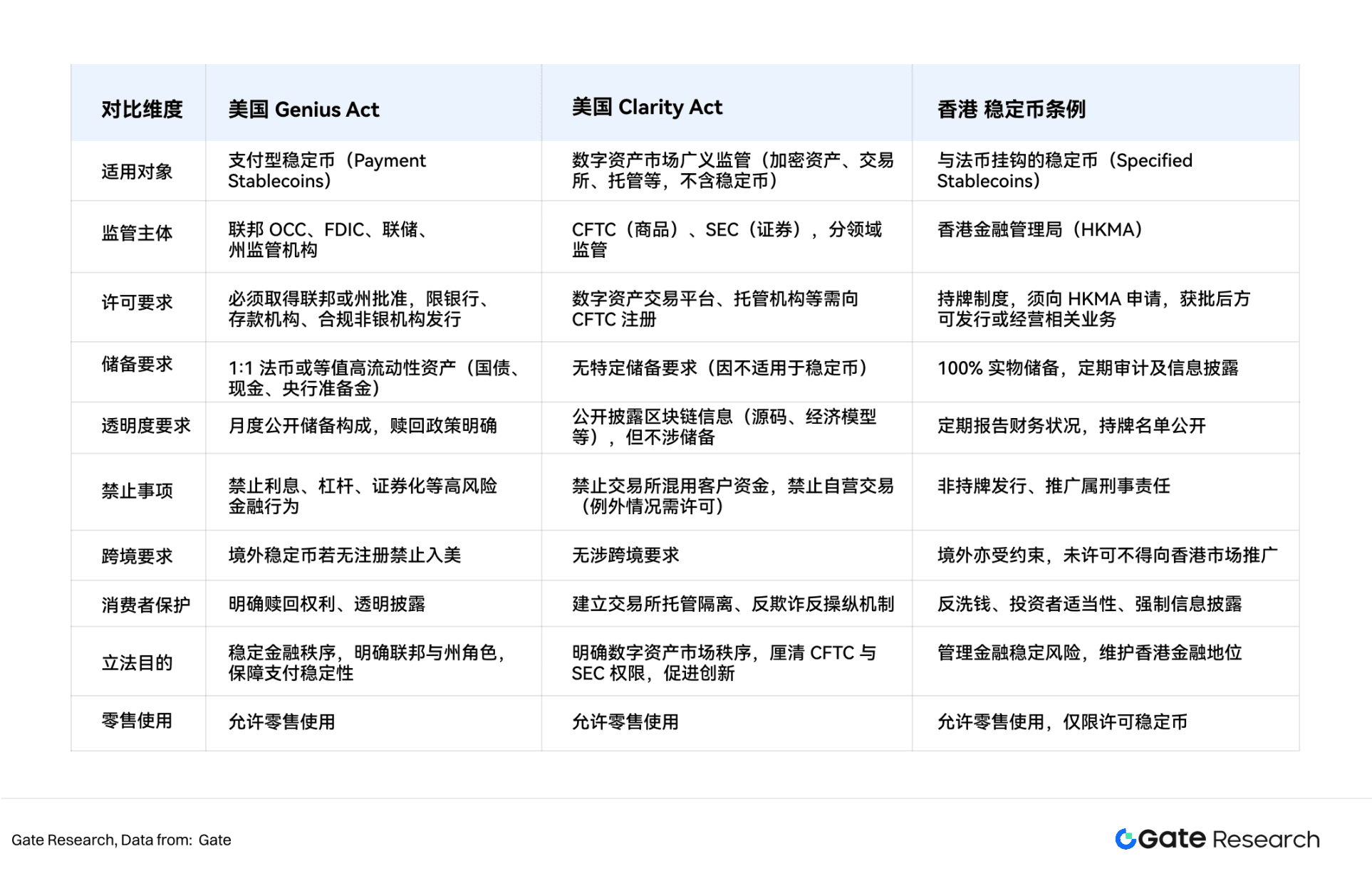

The renowned Genius Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) was passed by the Senate on June 17, 2025, and passed the House of Representatives on July 17, 2025, with a vote of 308–122, and was signed into law by President Trump on July 18, 2025. This marks the first establishment of a unified federal regulatory framework for stablecoin issuance in the U.S. Its core content includes:

•Regulatory model: A dual-track system of federal and state, with unified authorization by the Office of the Comptroller of the Currency (OCC).

•Issuing entities: Limited to banks, deposit institutions, and specific non-bank financial institutions approved.

•Reserve requirements: Require 1:1 fiat reserves, and the reserve assets must be U.S. Treasuries or cash, ensuring the redemption capability of stablecoins.

•Transparency obligations: Issuers must undergo monthly audits, information disclosure, and anti-money laundering scrutiny.

•Business restrictions: Issuers are prohibited from offering interest on stored value or engaging in leveraged, securitized, or other financial activities to curb the accumulation of systemic risks.

•Cross-border restrictions: Prohibit unapproved foreign stablecoins from circulating in the U.S. market, reinforcing a firewall in the capital markets.

On the same day, the Clarity Act (Digital Asset Market Clarity Act) was passed by the House of Representatives and sent to the Senate for review. Its main purpose is to clarify the regulatory responsibilities of the SEC and CFTC in the digital asset market, covering trading platforms, crypto derivatives, DeFi, etc.

3.2 Hong Kong introduces the (Stablecoin Regulation)

The Hong Kong Legislative Council passed the Stablecoin Regulation on May 21, 2025, which will officially take effect on August 1, 2025. The main contents include:

•Licensing system: All activities related to the issuance, sale, and marketing of stablecoins must obtain permission from the Hong Kong Monetary Authority (HKMA).

•Scope of application: Focus on stablecoins pegged to fiat currencies, excluding purely crypto asset-linked products.

•Capital requirements: Minimum capital requirement of 25 million HKD, and must have effective risk management and internal control mechanisms.

•Reserve requirements: 100% physical or equivalent liquid asset reserves, subject to regular audits and disclosures.

•Anti-money laundering and consumer protection: Strictly comply with AML/CFT standards and investor suitability requirements.

•Liability for violations: Engaging in relevant business without permission will constitute criminal liability, with a maximum penalty of imprisonment and fines.

Hong Kong and the U.S. have significant differences in stablecoin compliance requirements:

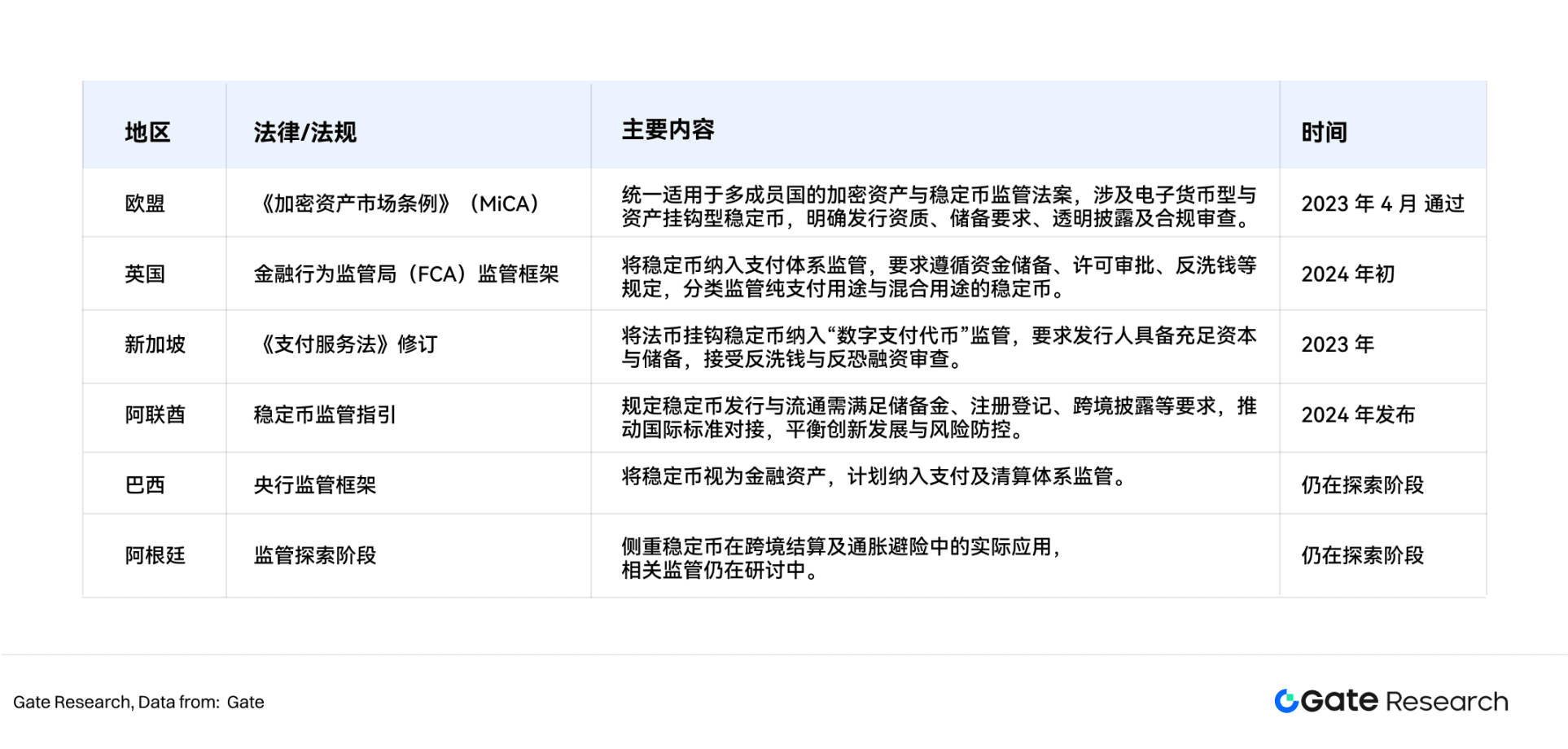

3.3 Dynamics of other economies

Except for the United States and Hong Kong, other major economies are also actively promoting regulatory frameworks related to stablecoins, with an overall trend of prudential tightening and gradual shaping.

Overall, the range of regulations in various countries mainly focuses on collateralized stablecoins, excluding riskier algorithmic stablecoins, which will further limit the development of algorithmic stablecoins. Additionally, Hong Kong only recognizes fiat-backed stablecoins, not allowing the issuance and circulation of crypto-backed stablecoins, thereby further solidifying the dominance of fiat-backed stablecoins.

Although the regulatory attitudes and progress regarding stablecoins vary among countries, they generally build frameworks around core principles such as 'reserve transparency, anti-money laundering scrutiny, consumer protection, and financial stability,' gradually aligning with their national digital asset or financial system regulations.

Restructuring of financial order dominated by stablecoins

4.1 Competition for financial sovereignty behind stablecoins

Currently, stablecoins pegged to the USD account for over 90% of the market value, with products such as USDT and USDC forming de facto standards in global exchanges, DeFi, and cross-border payments. This situation not only maintains the USD's position in traditional finance but also completes the deep penetration of USD influence into the new digital finance ecosystem through stablecoins.

Legislation such as the U.S. (Genius Act) specifies that USD stablecoins must be backed by high-quality assets such as U.S. Treasury bonds and short-term notes, reinforcing the binding relationship between stablecoins and core USD assets (Treasuries). This mechanism creates a 'dual anchoring structure of stablecoins and U.S. Treasuries,' where stablecoin issuers hold large amounts of U.S. Treasuries, indirectly providing ongoing buying pressure for the U.S. Treasury, further solidifying the USD's dominant position in the global financial system. This mechanism establishes a 'latent buying relationship' between stablecoins and USD assets, solidifying the foundation of USD financial hegemony worldwide.

The widespread circulation of USD stablecoins globally has led to a trend of 'on-chain dollarization' in many emerging markets and high-inflation countries, eroding the use case of local currencies and financial sovereignty. For instance, in Argentina, Turkey, and Russia, USDT has become the default tool for residents to preserve assets and conduct cross-border payments. This phenomenon is viewed in literature as the USD completing its digital penetration into financially vulnerable countries through stablecoins, undermining the monetary policy independence of these nations.

At the same time, regulatory progress for fiat stablecoins such as the Euro and HKD reflects countries' attempts to hedge against the spillover effects of USD stablecoins through local currency digitalization and stablecoin legislation. A new round of currency competition in the digital age has begun, shifting the struggle for financial hegemony from traditional systems to on-chain ecosystems.

4.2 Competition for next-generation financial infrastructure

Stablecoins carry not only payment and trading functions but are also gradually becoming core components of the new generation of cross-border payment and clearing infrastructure. Compared with the traditional SWIFT system, stablecoins have advantages such as real-time settlement, low cost, and decentralization. The U.S. hopes to replicate the infrastructure hegemony of SWIFT in the on-chain financial world through USD stablecoins, incorporating global payment, settlement, and custody services into its rule system. Meanwhile, international financial centers like Hong Kong and Singapore are promoting deep integration of local financial infrastructure with fiat stablecoins through policy guidance to seize positions as hubs and nodes of cross-border digital finance.

4.3 Competition for digital asset pricing power

In the current digital asset market, stablecoins are not only mediums of exchange but also deeply involved in the restructuring of pricing power in the digital asset market. USDT and USDC nearly monopolize the major trading pairs in the crypto market, becoming the de facto standard for liquidity anchoring and pricing of on-chain assets. Changes in their supply directly affect overall market risk appetite and volatility levels.

The United States has strengthened its control over the pricing power and liquidity dominance of the digital asset market through stablecoin legislation and regulation, indirectly solidifying the USD's core position in global capital markets. Meanwhile, Hong Kong, the EU, and others aim to push for local currency stablecoins to gain more regional pricing power and discourse rights in future digital financial competition.

Risks and challenges

The risks associated with stablecoins stem from both the systemic risks of their price anchoring mechanisms and compliance risks arising from external regulations.

5.1 Preventing systemic risks

The core of achieving price stability in stablecoins lies in the value stability of the underlying assets. Therefore, the greatest systemic risk for stablecoins comes from price volatility of the corresponding collateral leading to price decoupling.

Looking back at the first stablecoin, BitUSD, which was launched in 2014 and lost its 1:1 peg to the USD in 2018, due to its collateral being an obscure, highly volatile asset with no guarantees—BitShares.

In the same year, MakerDAO's DAI adopted an over-collateralization mechanism and liquidation mechanism to combat the risks posed by high volatility of crypto assets, but it essentially could not improve capital efficiency and exposed stablecoins to the price volatility risks of collateral assets. Similarly, stablecoins backed by fiat assets do not guarantee absolute safety.

In March 2023, due to the collapse of three U.S. banks (Silicon Valley Bank (SVB), Signature Bank, and Silvergate Bank), both USDC and DAI experienced decoupling. According to disclosures from Circle, the issuer of USDC, 3.3 billion USD of cash reserves backing the stablecoin were held at SVB. This led to a single-day drop of over 12% for USDC.

The value of DAI has also experienced volatility, primarily due to its collateral reserves being tied to USDC and related tools during that time. Stability returned only after the Federal Reserve announced support for bank creditors, allowing USDC and DAI to return to their respective pegging levels. Subsequently, both stablecoins adjusted their reserve structures, with USDC primarily holding its cash reserves at Bank of New York Mellon, while DAI diversified its reserves across multiple stablecoins and increased its holdings in real-world assets (RWA).

This chain reaction of decoupling events serves as a reminder for stablecoin issuers to diversify their asset allocation to combat systemic risks.

5.2 Violating the principle of decentralization

Although stablecoins have once driven the widespread use and compliant access of cryptocurrencies, their mainstream models (such as USDT, USDC) depend on centralized entities for operation and fiat assets for backing, which runs counter to the core ideals of blockchain's native decentralization and censorship resistance.

Some scholars believe that fiat-backed stablecoins essentially serve as on-chain mirrors of fiat currencies like the USD, thereby reinforcing dependence on the traditional financial system (USD, banking system), creating a 'centralized core beneath a decentralized appearance', and undermining the original ideals of cryptocurrency decentralization.

This centralized dependency not only restricts stablecoins to the credit risks of issuers and custodians but also potentially leads to freezing or tampering in extreme situations (compliance policies, scrutiny pressure), contradicting the essential purpose of blockchain, which is 'permissionless and immutable'.

5.3 Difficulties in cross-border regulatory coordination

Globally, stablecoins involve multiple jurisdictions, cross-border finance, and data flows, but there are significant discrepancies in countries' regulatory positions, definitions, and compliance requirements regarding stablecoins:

Due to significant differences in regulatory frameworks among countries, stablecoins face strong uncertainties and legal risks in cross-border use, clearing, and compliance processes, easily leading to 'regulatory arbitrage' and compliance blind spots, hindering their global development.

5.4 Potential financial sanction risks

As international situations become turbulent, stablecoins also face the risk of being incorporated into financial sanctions tools. The U.S. may leverage regulation-led USD stablecoins to enhance scrutiny over capital flows and fund uses, and even implement freezing and blocking sanctions against specific entities and countries.

Alexander Baker pointed out that stablecoins have, to some extent, become an on-chain extension of the USD, and may in the future, like SWIFT and other traditional systems, become part of the U.S. financial weaponization toolkit. For some emerging markets, cross-border transactions, and on-chain financial projects, this undoubtedly increases political and compliance risk exposure, further promoting global exploration of de-dollarization and regional local currency stablecoins.

Conclusion

The rise of stablecoins reflects the reconstruction of monetary order in the digital financial era. Since their inception, stablecoins have continued to penetrate various fields such as payments, trading, and asset reserves, and with their efficiency, low cost, and programmability, they have gradually become an important bridge connecting traditional finance and the digital economy. Today, stablecoins are not only the core infrastructure of the crypto market but also profoundly impact the evolution of the global financial landscape, increasingly being incorporated into the financial regulation and monetary strategy of more countries.

The rise of stablecoins reflects a covert competition for currency sovereignty and financial hegemony. The dominant position of USD stablecoins in the global market further consolidates the USD's ruling status in the on-chain world, with its reserve structure deeply tied to U.S. Treasuries, making stablecoins an important extension tool of U.S. financial strategy. Emerging markets and other major economies are attempting to gradually weaken the penetration effects of USD stablecoins through local currency stablecoins, digital currency regulation, and building cross-border payment systems, promoting global monetary diversification and local currency digitalization. Stablecoin legislation has become a key variable in the reshaping of future international financial order, reflecting deeper national interests and the redistribution of financial power.

However, the future development of stablecoins still faces many uncertainties. Firstly, the systemic risks inherent in the pegging mechanism and reserve structure are difficult to eliminate in the short term, leaving potential trust crises and market volatility risks. Secondly, a unified global regulatory framework has not yet formed, and there are many obstacles to cross-border regulatory coordination and legal applicability, which keep stablecoins in a gray area, facing ongoing compliance and policy risks. Thirdly, issues such as centralized issuance and financial weaponization create inherent tensions with the original ideals of decentralized blockchain, and how to balance regulatory compliance and technological autonomy remains a core issue the industry must face.

In the future, stablecoins will play an increasingly important role in financial infrastructure, currency competition, and international settlement systems. Their development path is closely linked to the deep integration of decentralized finance and real-world assets, as well as the construction of a new global financial order and the redistribution of discourse power.

References

•Gate, https://www.gate.com/zh/price

•Sky, https://sky.money/

•Tether, https://assets.ctfassets.net/vyse88cgwfbl/1LdSmP3HBynDxm6wvkDSsL/c4bcbd1f6fc18a0e8b3a12444ac8ae97/ISAE_3000R_-_Opinion_Tether_International_Financial_Figures___Reserves_Report_31.03.2025_RC187322025BD0040.pdf

•Deltec, https://www.deltecbank.com/news-and-insights/the-history-of-stablecoins/

•Tether, https://tether.to/en/

•DeFiLlama, https://defillama.com/stablecoin/dai

•CSPengyuan, https://www.cspengyuan.com/pengyuancmscn/credit-research/macro-research

•rwa.xyz, https://app.rwa.xyz/stablecoins?utm_source=substack&utm_medium=email

•Swift, https://www.swift.com/about-us/legal/document-centre

•Congress, https://www.congress.gov/bill/119th-congress/senate-bill/394/text

•Whitehouse, https://www.whitehouse.gov/fact-sheets/2025/07/fact-sheet-president-donald-j-trump-signs-genius-act-into-law/