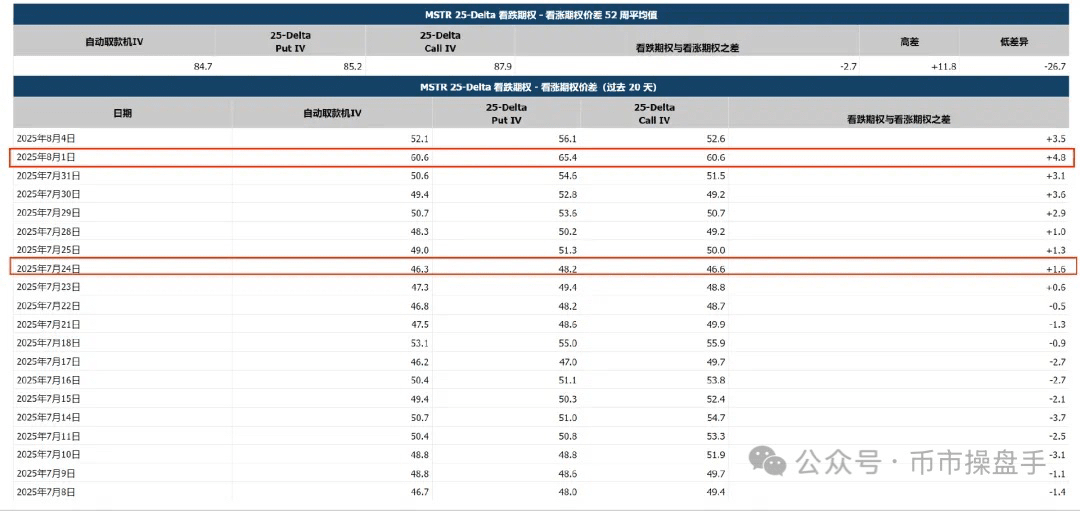

Recently, Bitcoin has oscillated downwards from high levels, compounded by ancient whale sell-offs, leading to a persistent panic sentiment in the market. Meanwhile, MicroStrategy (MSTR), seen as the 'U.S. stock leverage' for Bitcoin, has continued to experience a downward trend since July 15, with a cumulative decline of over 20% over 12 trading days, and its put option trading volume has surged 300% month-over-month, further exacerbating market pessimism. Market Chameleon data shows that the difference in implied volatility between one-year put options and call options for Bitcoin turned positive on July 24 and reached 4.8% on August 1, the highest since April 9. This change indicates that traders are increasing their bets on further declines in MSTR's stock price. So, will MSTR's further decline drag down Bitcoin?

Although MSTR has historically been highly correlated with Bitcoin price trends, this round of decline reflects more the early release of its financial risks: as the low-interest convertible bond financing window closes, the company is shifting to a more aggressive capital structure—financing tools are progressively upgraded from common stock and preferred stock to high-cost floating-rate perpetual preferred stock. This shift not only significantly increases the credit risk premium but also puts substantial pressure on annual dividend expenditures.

According to the terms of the preferred shares issued by MSTR, the total annual dividend expenditure will reach $587.7 million, specifically consisting of: STRK ($45.04 million), STRF ($210 million), STRD ($110 million), and STR-C ($222.66 million). Based on the financing plan disclosed on August 1, if MSTR completes a $4.2 billion issuance of preferred shares (with a coupon rate of 9%), annual dividend expenditures will surge to $965.7 million, a 64% increase from the current level. As MSTR's cash flow is highly dependent on financing, if external fundraising is hindered, the company may face default risks or be forced to sell its Bitcoin reserves—this also explains why its one-year put option implied volatility has recently soared.

However, considering that MSTR's asset premium rate is still nearly 35%, the short-term bubble effect on Bitcoin is negligible (unless the asset premium rate turns negative).

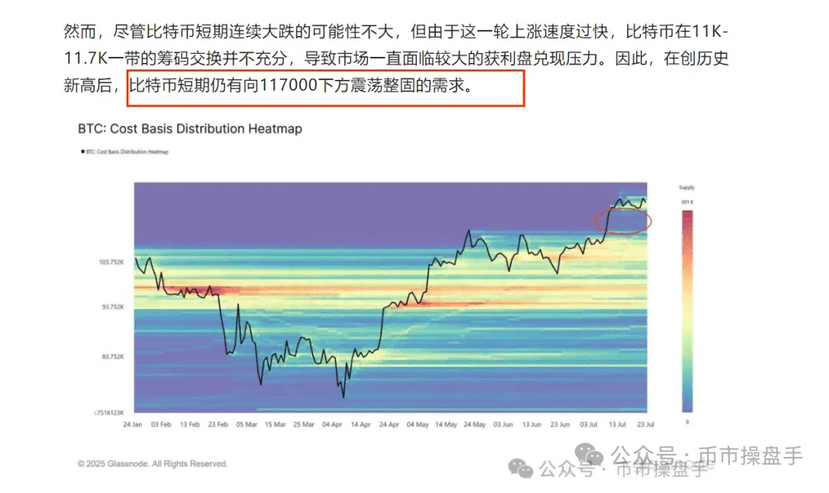

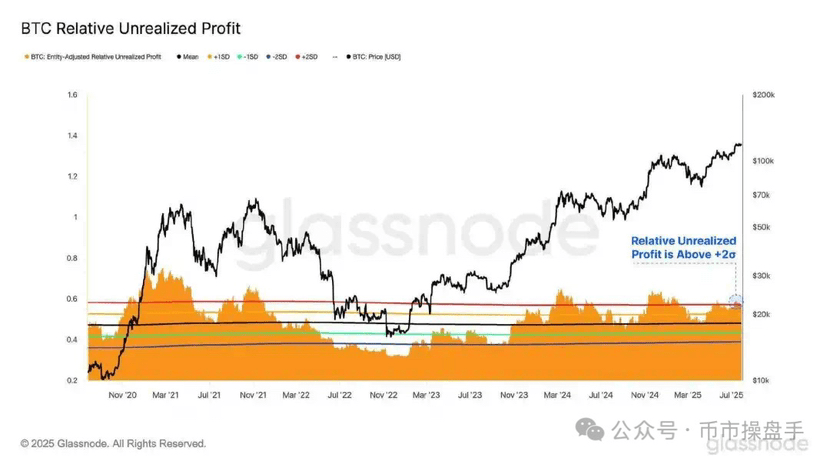

In the previous article, I pointed out that Bitcoin has a short-term adjustment demand, mainly due to its rapid rise during the breakthrough of historical highs, which has led to a dislocation in chip distribution. According to glassnode data, after breaking through $120,000, the proportion of Bitcoin holders not realizing profits has exceeded two standard deviations (2SD), meaning that over 95% of holders are in profit. Notably, since November 2021, whenever the proportion of Bitcoin investors not realizing profits exceeds two standard deviations, the probability of experiencing a turbulent adjustment in the following two months reaches 100%.

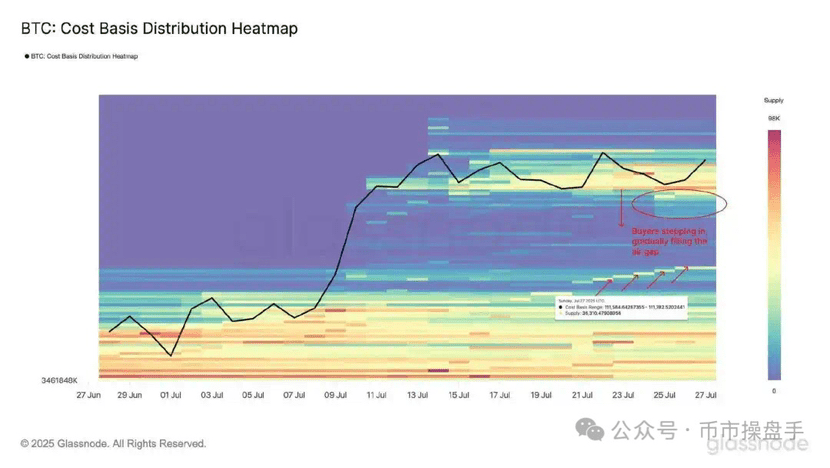

Recently, after a two-week adjustment, Bitcoin has begun to exchange chips in the $117,000-$110,000 range. The market's 30-day average holding cost has gradually risen from $112,000 to $114,500, and the proportion of holders not realizing profits has also fallen from 95.3% to below 90% (currently at 89.7%). Referencing the previous two rounds of adjustments, the proportion of investors not realizing profits returned to near the mean, and even though the downward adjustment space for Bitcoin is likely small (the last round of adjustment was 11.2%, and this round is likely to be less than 11.2%, but 8% has already been completed), the current horizontal oscillation time is still clearly insufficient.

On August 2, the Chairman of the U.S. Securities and Exchange Commission (SEC) officially launched the 'Project Crypto' regulatory innovation initiative, which introduces three core measures for the first time—relaxing asset issuance access standards, establishing a technological innovation exemption mechanism, and fostering super applications with scale effects, aiming to systematically enhance the U.S.'s leadership in the global crypto asset field. Since this plan mainly focuses on asset tokenization (especially RWA) and application innovation (especially in the DeFi direction), Ethereum has once again received strong policy support following the (GENIUS Act).

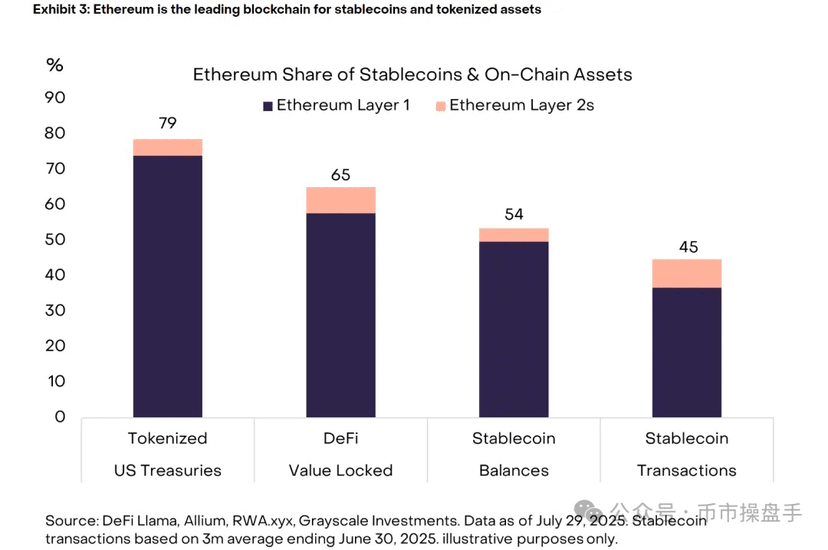

Ethereum's ability to gain an advantage stems from its systemic advantages within the crypto economic ecosystem, primarily reflected in three aspects: First, Ethereum carries 53% of the total value of stablecoins in the entire market and processes 45% of the daily trading volume of stablecoins; second, in the decentralized finance space, Ethereum protocols lock up a high proportion of value, accounting for 65%, while supporting nearly 80% of the tokenized U.S. Treasury market; most importantly, institutional participants, including leading trading platforms like Coinbase, Kraken, and Robinhood, as well as tech giants like Sony, have chosen Ethereum as their preferred infrastructure network for blockchain business.

Under the dual policy support of the (GENIUS Act) and 'Project Crypto', Ethereum is transforming from a public chain platform into a core hub linking traditional finance and the crypto economy, with its 'institutional-level' network effects creating insurmountable competitive barriers. These policy dividends not only reinforce Ethereum's market leadership but also herald a new wave of institutional development in the crypto industry.

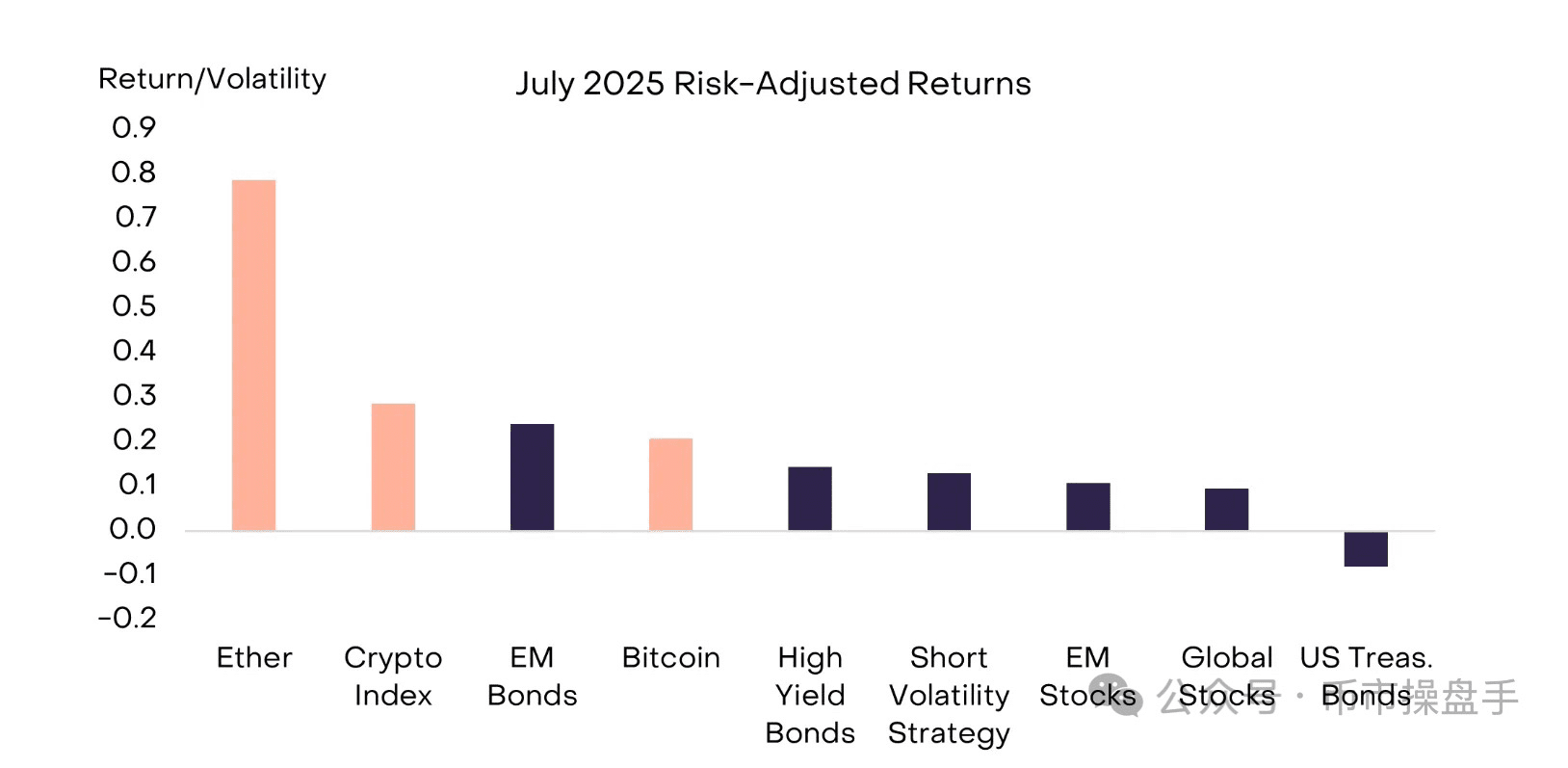

In July, the cryptocurrency market exhibited significant differentiation: the FTSE/Grayscale cryptocurrency industry market index (tracking the market capitalization of investable digital assets) rose a cumulative 15%, with Ethereum performing the best, surging 49% in a single month, significantly outperforming Bitcoin's 8% increase and other categories of digital assets. This indicates a significant shift in market dynamics. In a stock pattern, funds always flow towards the path of least resistance. When the trend is already very clear, ordinary people just need to follow!