Written by: White55, Mars Finance

1. The regulatory "watershed": Why did the SEC bow to liquid staking?

SEC staff statement excerpts regarding certain cryptocurrencies' liquid staking activities. Source: SEC

On August 6, 2025, the U.S. Securities and Exchange Commission (SEC) quietly released a groundbreaking (Liquid Staking Activities Guidance), clearly stating for the first time that liquid staking tokens (LST) do not constitute securities issuance in specific scenarios, and related service providers do not need to register under the (Securities Act). The implication of this guidance is that the staking ecosystem of mainstream public chains like Ethereum and Solana has finally received a "compliance pass."

The core logic of the SEC is the division of economic substance:

Staking receipt tokens (such as stETH, mSOL) serve merely as "proof of ownership," and their issuance and trading do not involve the characteristics of "investment contracts." As long as the act of depositing crypto assets is independent of any commitment to "profit from the efforts of others," it does not trigger the Howey Test.

Regulatory boundary clarification: The SEC has named protocols such as Lido, Marinade Finance, and JitoSOL as meeting exemption criteria, as their functions are limited to "administrative services" (such as token minting and reward distribution) rather than active management or yield guarantees.

This transformation is driven by a dual game of politics and markets:

SEC Chair Paul Atkins has shifted from the previous administration's "enforcement-based regulation" style to promote the "Project Crypto" initiative, viewing staking as a "cybersecurity service" rather than a speculative tool.

(CLARITY Act) compulsion: Congress intends to exclude node operations, staking, and self-custody wallets from the definition of "securities brokers," forcing the SEC to compete for rule-making authority.

2. Dissecting liquid staking: Why is it the "liquidity engine" of DeFi?

1. Mechanism: From asset lock-up to capital bifurcation

Liquid staking allows stakers to use alternative tokens to maintain the liquidity of their staked tokens and earn additional yields through DeFi protocols using these alternative tokens.

Before delving into liquid staking, let us first understand staking and its related issues. Staking refers to locking cryptocurrency within a blockchain network to maintain its operation while enabling stakers to earn rewards. However, staked assets often become illiquid during the staking period, as they cannot be exchanged or transferred.

Liquid staking allows cryptocurrency holders to participate in staking without relinquishing control over their held assets. This fundamentally changes the way users stake. Projects like Lido introduce liquid staking to provide a tokenized representation of staked assets in the form of tokens and derivatives.

It enables users to gain the advantages of staking while retaining the flexibility to trade, allowing these tokens to be traded in decentralized finance (DeFi) applications or transferred to other users.

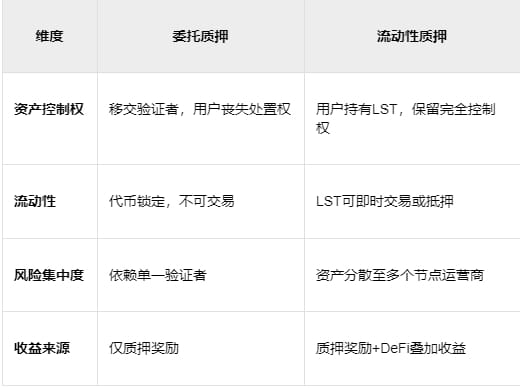

2. The "power struggle" with delegated staking

In a Delegated Proof of Stake (DPoS) network, users vote to select their preferred representatives. However, the purpose of liquid staking is to allow stakers to circumvent the minimum staking threshold and token lock-up mechanisms.

Although the basic concept of DPoS draws on Proof of Stake (PoS), its execution method is different. In DPoS, network users have the right to elect representatives, known as "witnesses" or "block producers," who are responsible for block verification. The number of representatives participating in the consensus process is limited and can be adjusted through voting. Network users in DPoS can pool their tokens into a stake pool and use their combined voting power to vote for their preferred representatives.

On the other hand, liquid staking aims to lower investment thresholds and provide stakers with a way to bypass token lock-up mechanisms. Blockchains typically have minimum requirements for staking. For example, Ethereum requires anyone wishing to establish a validator node to stake at least 32 Ether. It also requires specific computer hardware, software, time, and expertise, all of which necessitate significant investment.

This model has ignited market growth: the total locked value (TVL) of liquid staking protocols has surpassed $67 billion, with Ethereum accounting for 76% ($51 billion), and Lido alone holding 31% market share.

3. How liquid staking works

Liquid staking aims to eliminate the staking threshold, enabling holders to profit using liquidity tokens.

Stake pools allow users to combine multiple small stakes into a larger one using smart contracts, which provide corresponding liquid tokens (representing their share in the pool) to each stake holder.

This mechanism eliminates the threshold to become a staker. Liquid staking goes further, allowing stakers to achieve dual yields. On one hand, they can profit from the staked tokens; on the other hand, they can profit from trading, lending, or any other financial activities using liquidity tokens without affecting their existing staked positions.

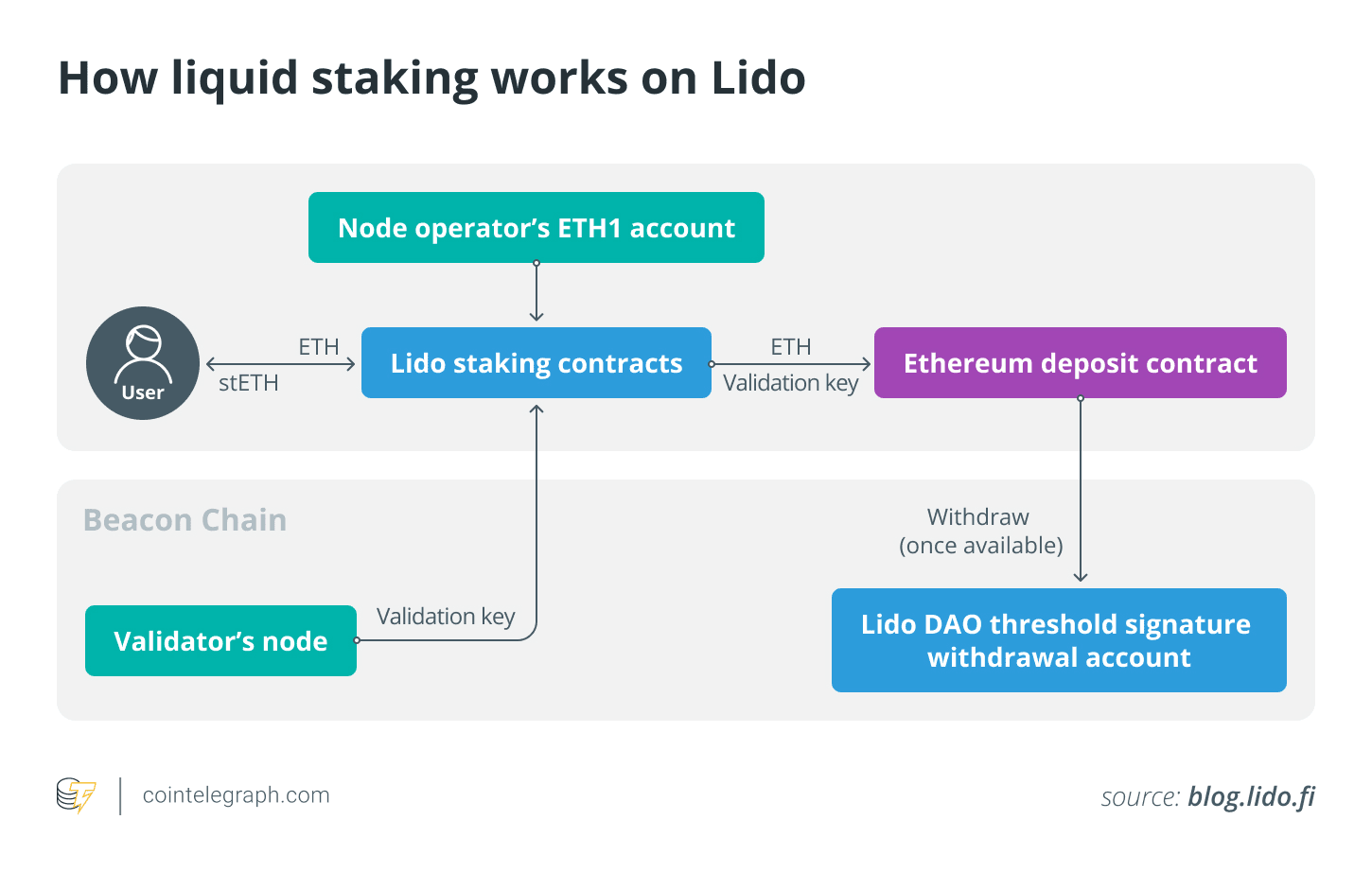

Taking Lido as an example, it helps us better understand how liquid staking operates. Lido is a liquid staking solution for PoS currencies, supporting multiple PoS blockchains including Ethereum, Solana, Kusama, Polkadot, and Polygon. Lido offers an innovative solution to the barriers posed by traditional PoS staking by effectively lowering entry thresholds and the related costs of locking assets into a single protocol.

Lido is a smart contract-based staking pool. Users can deposit assets into the platform to stake on the Lido blockchain through the protocol. Lido allows ETH holders to stake a small portion of the minimum threshold (32 ETH) to receive block rewards. After depositing funds into Lido's staking pool smart contract, users receive Lido Staked ETH (stETH), a token compatible with ERC-20, generated upon deposit and destroyed upon withdrawal.

The protocol allocates the staked ETH to validators (node operators) within the Lido network, which are then deposited into the Ethereum Beacon Chain for verification. These funds are subsequently held in smart contracts, which the validators cannot access. The ETH deposited through the Lido staking protocol is divided into collections of 32 ETH, which are held by active node operators on the network.

These operators use public validation keys to verify transactions involving user-staked assets. This mechanism allows users' staked assets to be distributed across multiple validators, thereby reducing the risk of single points of failure and risks associated with staking on a single validator.

Stakers can deposit tokens such as SOL, MATIC, DOT, KSM, etc., into Lido's smart contracts to receive stSOL, stMATIC, stDOT, and stKSM respectively. StTokens can be used for DeFi yield generation, providing liquidity, trading on decentralized exchanges (DEX), and many other use cases.

4. The "domino effect" of SEC guidelines: Who is celebrating? Who is cautious?

1. Institutions: From bystanders to "staking whales"

The staking revolution of ETF issuers: Rex Shares has launched the first Solana staking ETF in the U.S., holding SOL through a Cayman subsidiary and staking at least 50% of the position; BlackRock, VanEck, and other Ethereum ETF applicants are urgently revising their proposals to include staking terms—analysts predict a probability of approval exceeding 95%.

The trend of public companies "hoarding coins for interest":

Bitcoin mining company Bit Digital liquidated its mining machines and shifted to Ethereum staking;

SharpLink Gaming staked all 198,000 ETH (approximately $500 million), earning 102 ETH in a single week;

BitMine raised $250 million to establish an ETH staking fund, operated by Wall Street veteran Tom Lee.

Wall Street's new calculation: Treasury yields are only 4%, while staking ETH can yield 5% plus asset appreciation potential—this is the crypto version of "fixed income +."

2. The compliance turning point of DeFi

The "secondary market" explosion of LSTs: Institutions can incorporate stETH and other tokens into their balance sheets or use them as collateral for derivatives. Alluvial's CEO predicts: "The exemption of staking tokens from securities will give rise to a trillion-dollar on-chain treasury market."

The retail entry revolution: Robinhood has opened ETH and SOL staking to U.S. users; Kraken has achieved non-custodial Bitcoin staking through the Babylon protocol (users' BTC remains on the mainnet, earning yield through Tapscript locking).

Endgame: When Wall Street takes over the staking empire.

The SEC's green light is actually a prelude to institutional compliance:

Staking as a Service (StaaS) will replace retail mining, becoming standard configuration for asset management giants like BlackRock and Fidelity;

LST derivatives (such as futures and options) are landing on CME and ICE, attracting hedge funds to hedge staking yield fluctuations;

The entry of sovereign funds: Funds from the UAE and other countries are testing staking ETFs, viewing them as "digital sovereign bonds."

The ultimate goal of all this is to transform PoS chains like Ethereum and Solana into a "digital bond market" for global capital—where staking yields are the new treasury yields, LSTs are the new T-Bills, and the SEC's seal is merely the key to Wall Street's vault.

History never repeats but it rhymes: In 1688, underwriters in London’s coffee houses secured ocean-going merchant ships with wealth; in 2025, the SEC guarantees the sailing safety of the sea of code with a guideline.