Imagine: You have to pay rent at the end of the month, but your salary will be in your account in 10 days; the owner of a small business has 500,000 unpaid invoices in his hand, but is in a hurry to purchase raw materials - in traditional finance, you may have to borrow high-interest loans or give up orders, but Huma Finance (HUMA) is saying: "Pledge your 'money that you will definitely have', and we can give you cash now".

What it does is not ordinary lending, but turning "future income" into a tradable "time asset", using blockchain's smart contracts to issue an "advance withdrawal permit" for "money that has not yet arrived". This is the core logic of the world's first PayFi network: to seamlessly integrate payment scenarios (salary, invoice) and financial services (lending) on the chain.

🕰 First break the question: Why is "future money" worthy of trust?

The logic of traditional encrypted lending is "mortgaging existing encrypted assets" (such as borrowing USDC with ETH), but Huma has set its sights on something more universal - "certain cash flow". These cash flows are like "unripe fruits":

For workers: A monthly salary of 30,000 is a "certain future income" signed with the company. As long as you are not unemployed, it will arrive in 10 days;

For enterprises: The 500,000 invoices signed by the customer stipulate payment in 30 days. As long as the customer does not default, the money cannot escape;

For cross-border remittances: Overseas workers remit 2,000 US dollars to their families every month, which is a "regular cash flow" for many years.

What Huma does is use smart contracts to "credit rate" these "future money": Through off-chain data verification (such as access to on-chain evidence of salary flows and invoice contracts), the algorithm will calculate "the probability of default for this future income", and then lend in advance at a ratio of 70%-90%. Simply put: the more certain you are to get the money, the more you can borrow now.

🔗 PayFi's "on-chain bite technique": How does a smart contract act as a "credit judge"?

If Huma is compared to a "future income bank", then its smart contract is a "fully automatic credit officer", completing the operation of "future money for current money" in three steps:

Cash flow on the chain to "do notarization"

You need to "certify and store evidence on the chain" for pay slips, invoices, remittance records and other vouchers through Huma's compliance interface (these data will be encrypted and only exposed to the algorithm without revealing privacy). For example, the 500,000 invoices uploaded by small business owners will generate an "immutable payment voucher due" on the chain, which is equivalent to putting a "notary office seal" 📜 on future money.

Algorithm calculates "discount rate"

The smart contract will automatically analyze: Is the company of this pay slip stable? What is the credit of the customer corresponding to the invoice? What is the historical default rate? Finally, give a "loanable ratio" - for example, civil servants' salaries may be lent 90% (extremely low default risk), and start-up companies' invoices may be lent 70% (the probability of customer default is slightly higher).

Borrow money and pay it back "automatically"

After you borrow money, the smart contract will monitor the "time point when future income arrives": once the salary arrives, the loan and handling fee will be automatically deducted; when the invoice is due, the customer will pay, and the money will be directly transferred to the lenders. The whole process does not require manual collection, just like setting an "automatic repayment alarm clock" ⏰ for your future self.

💎 HUMA token: More than governance, it is a "lubricant for the cash flow ecosystem"

The HUMA token is not a simple "handling fee", but an "ecological glue" that makes this "future income market" smoother:

When nodes help Huma verify the authenticity of cash flow (such as verifying whether the invoice is valid), pledging HUMA can get rewards - which is equivalent to "paying wages to credit judges" and encouraging more people to participate in data verification;

When the community discusses "whether to add 'freelancer project funds' as collateral", HUMA holders vote to decide - allowing the ecosystem to cover more "non-traditional cash flows" (such as advertising revenue of Internet celebrities);

In the long run, high-quality borrowers can accumulate "on-chain credit scores" by repaying on time, and HUMA may become a medium for "credit score exchange rights" (such as lower borrowing rates).

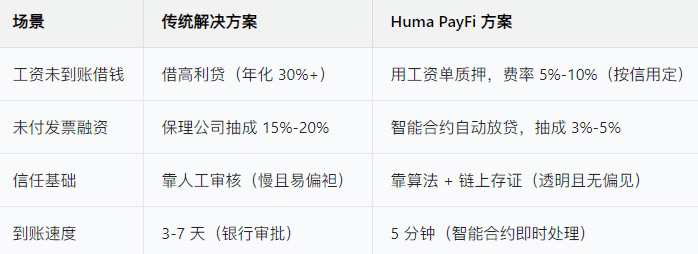

🆚 Comparison table: The "time difference revolution" between Huma and traditional lending

🌱 Future brainstorming: When "all future income" can be traded on the chain

Freelancer's "receivables project": Received a 100,000 design order, the customer pays in 3 installments, Huma allows to borrow 70,000 in advance with the first installment of receivables to buy equipment;

Artist's "royalty stream": A song can earn 20,000 royalties per month. Pledge this "future royalty stream", you can borrow 100,000 now to make a new album;

Even "retirement pension": Advance pledge part of the retirement pension for the next 5 years and exchange it for a sum of money to pay for children's tuition (of course, the algorithm will strictly control the lending ratio to avoid excessive debt).

What Huma is doing is essentially pricing "time" - allowing everyone and every company's "future earning ability" to become cash flow that can be used flexibly at the moment. And PayFi, this new species, may make DeFi from a "game for encrypted asset players" to a tool that truly serves "everyone's daily economic activities".

#humafinance $HUMA @Huma Finance 🟣