The Great Depression of 1929 led to the establishment of the Securities Exchange Act of 1934 and the SEC, but whether this is unfortunate or fortunate depends on whether you are an e/acc accelerationist or see it from a regulatory freedom perspective. After that, the SEC never again prevented financial innovation or crises.

In 1998, LTCM (Long-Term Capital Management) faltered with Russian bonds using quantitative methods, almost causing a repeat of the 1929 Great Crisis, yet this did not prevent the 1999 ATS (Alternative Trading System) regulations from taking effect, fully embracing information technology for quantification, hedging, and arbitrage.

After the 2008 financial crisis, regulation targeting dark pool trading was initiated, but dark pools still exist. In 2025, after Gary Gensler leaves, the SEC is determined to embrace the new trend of the future—everything can be on-chain, and everything can be compliant.

On-chaining: RWA is just the starting point. Future transactions, asset allocation, and earning will revolve around on-chain operations, just like embracing blockchain using computers.

Compliance: Airdrops, staking, IXO, and rewards, creating a U.S.-specific super app (Reg Super-App), with all DeFi re-Americanized.

The SEC's existential crisis

The Great Depression created the SEC, and cryptocurrencies will end the SEC.

Timeline of SEC regulatory shift: Gary Gensler's departure —> Crypto Task Force –> Project Crypto

There is a trail to follow; the SEC's regulatory activity can be divided into the time when Gary was dismissed in January and the new crypto policies after the current chair, Atkins, took office in April, marked by the establishment of the Crypto Task Force, culminating in Project Crypto at the end of July, completing a comprehensive 'surrender' to crypto.

To understand why Project Crypto emerged, one must find answers from the SEC's regulatory dynamics between April and July, during which there were frequent actions. On one hand, cases like Ripple and Kraken need to conclude decently, while on the other hand, companies like Coinbase and Grayscale are becoming increasingly strong, actively demanding the SEC to loosen regulations.

Especially, the Ripple case marks the SEC's shift from 'enforcement-style regulation' to 'regulatory service.' The subsequent restart of Kraken's IPO process proves that the crypto concept has been fully accepted by U.S. regulators, and Robinhood is also starting to advance tokenized stocks.

The approval of BTC/ETH ETF physical staking and redemption is the most significant progress. However, more currencies and more forms are still in a case-by-case review state, such as Trump's own Trump Group ETF also being in line.

Daring to obstruct the United States' journey into cryptocurrency, this is no ordinary SEC; it must strike hard!

Image description: SEC 2025 Cryptocurrency Regulatory Paradigm Shift

Thus, Trump chose to play unorthodox, supporting the CFTC and launching legislative actions like the Genius Act. The CFTC is already on the road to expanding its power, and the White House's cryptocurrency report announced a substantive acceptance of existing DeFi.

The SEC has previously 'transferred' the regulation of stablecoins to banking regulators, with more digital asset regulatory powers being allocated to the CFTC. Where the SEC goes from here is a pressing reality to consider.

The more significant Clarity Act has not yet officially become law. If the SEC does not take proactive measures, it will be completely overtaken by the CFTC, especially since the issuance of stablecoins has already substantially touched the core of securities law. Before the Clarity Act becomes law, the SEC must take administrative practices to preemptively delineate regulatory boundaries and create established facts.

However, within the current framework, there is little the SEC can do, such as approving more staking ETFs (like SOL), issuing any type of currency ETF, tokenized stocks, securities, etc., as well as approving crypto companies for listing and treasury (DATCO) companies. The SEC's attitude has been to wait for change, repeatedly delaying and pausing various topics.

On July 17, there were already rumors about the SEC planning to merge with the CFTC. Just after the launch of the SEC's Project Crypto, the CFTC's Crypto Sprint plan also followed closely, and the details are not important.

The division of responsibilities between the SEC and CFTC will end in the cryptocurrency era. The SEC's choice to maximize departmental interests can only be to embrace the new era and abandon all dogmas of the old world.

The 'on-chaining' of the real world.

DeFi is fully compliant, marking the end of offshore arbitrage.

Previously written, the Genius Act and Clarity Act did not address specific DeFi regulation; the former only covered stablecoins, while the latter was too macro. Now, the SEC's Project Crypto details regulations from an administrative perspective, constraining all aspects of DeFi from the angles of personnel, finance, and regulation.

No need to go overseas; people should return to America.

In summary, everything that offshore exchanges and overseas foundations can do can now be done domestically in the U.S.

Whether stablecoins, IXO, or tokenization (stocks, bonds), although the regulatory affiliations differ, the SEC will not casually prosecute for illegal securities issuance as long as communication is done well.

Secondly, how the Tornado Cash founder's judgment shows that the SEC has no right to interfere, but the SEC can ensure the safety of developers, encouraging builders to choose the U.S. for development and promoting healthy and orderly competition.

DeFi has rules; money should return to America.

In summary, do not engage in any offshore shell games, nor need to overly worry about the degree of decentralization.

All token issuance, on-chain activities (staking, lending, trading, investing), and reward distribution involved in DeFi are compliant, especially as self-custody trading has been elevated to the height of 'American liberal values.' Various types of crypto-staking ETFs will be fully opened.

Finally, do not engage in offshore regulatory arbitrage; everything can return to the U.S. for investment, development, and entrepreneurship, ensuring that crypto happens in America.

RWA has regulations; tokens on the U.S. chain.

In summary, on-chaining has officially become the main theme.

Compared to DeFi, RWA has separate regulations, distinguished into types such as stocks, bonds, equity, and physical assets. The window for tokenized stocks and tokenization in the private market (Pre-IPO) is now open.

This will be a more profound transformation than computerization, from paper certificates to electronic transactions, and then to comprehensive on-chain operations. Any asset that can be financialized will be tokenized, and the information gap between a few and the majority will be completely eliminated, although this may take many years.

Ultimately, DeFi will become a new form of finance, not just a supplement to TradFi, and ETH will become the new vehicle for American financial hegemony.

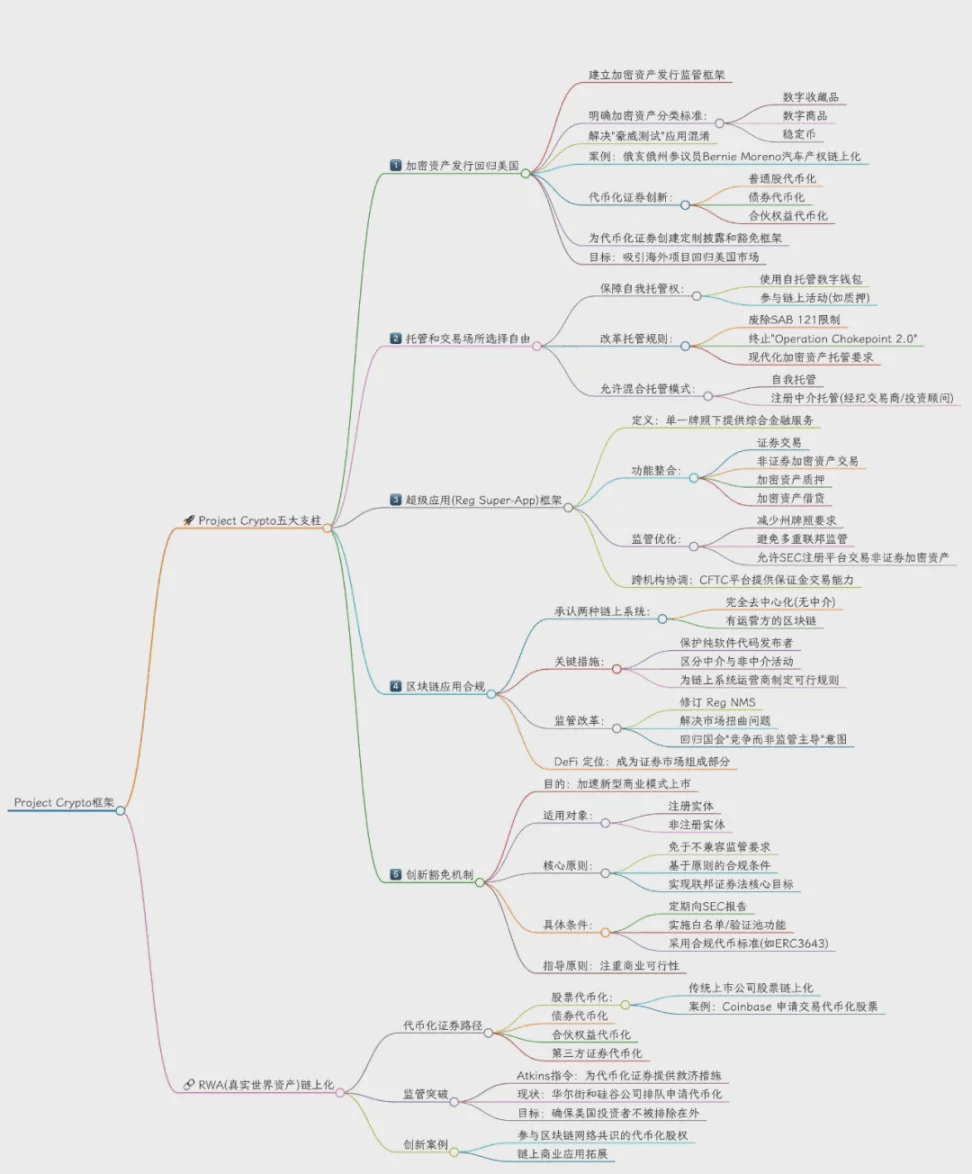

Image description: SEC Project Crypto Framework

The title of this section is borrowed from the slogan of RWA L1 Rialo developed by Subzero Labs. This time, RWA will no longer be synthetic assets or virtualized custodial issuance, but will directly open the possibility of putting any asset on-chain. For example, the newly listed Figma also retains the option to issue tokenized stocks.

Stocks are tokenized stocks, and assets are tokenized assets.

Conclusion

A booster for financial bubbles, or a necessary path for asset innovation.

From today onward, Project Crypto can be said to be the moment of securities law for DeFi. However, how much of the departmental principles can be implemented, and how much can be accepted by Trump and Capitol Hill, remains to be seen.

However, the CFTC and SEC will completely merge, as the future digital commodities and digital securities will be difficult to distinguish.