"Buy land, they’re not making it anymore." This quote, often mistakenly attributed to Mark Twain in the 20th century, has frequently been used in real estate sales. Gravity strongly endorses this statement; if humans cannot achieve interstellar travel, land, like Bitcoin, is "not subject to inflation."

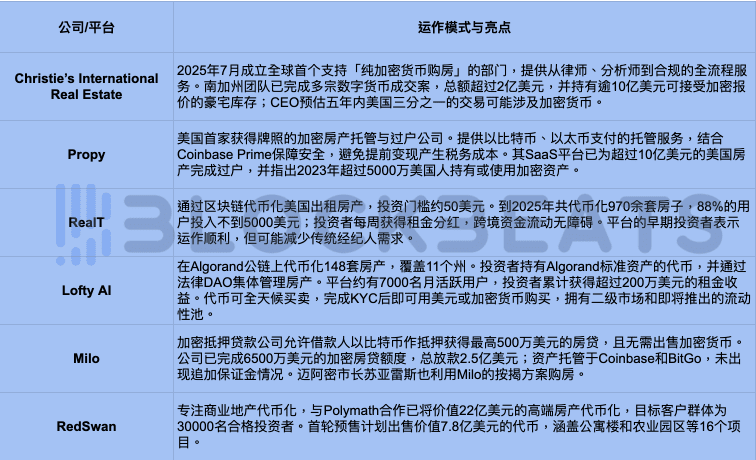

In 2025, the crypto wave spread from Silicon Valley to Wall Street and finally impacted Washington. As compliance gradually progresses, it quietly begins to change the fundamental structure of the real estate industry. In early July, Christie’s International Real Estate officially established a dedicated department for crypto real estate transactions, becoming the first mainstream luxury real estate brokerage brand to fully support 'pure cryptocurrency payments for home purchases' as a corporation.

And this is just the beginning. From Silicon Valley entrepreneurs to Dubai developers, from Beverly Hills mansions in Los Angeles to rental apartments in Spain, a wave of real estate trading platforms centered on blockchain technology and digital assets is emerging, forming a new track of 'Crypto Real Estate.'

How crypto can drive the next wave of American real estate.

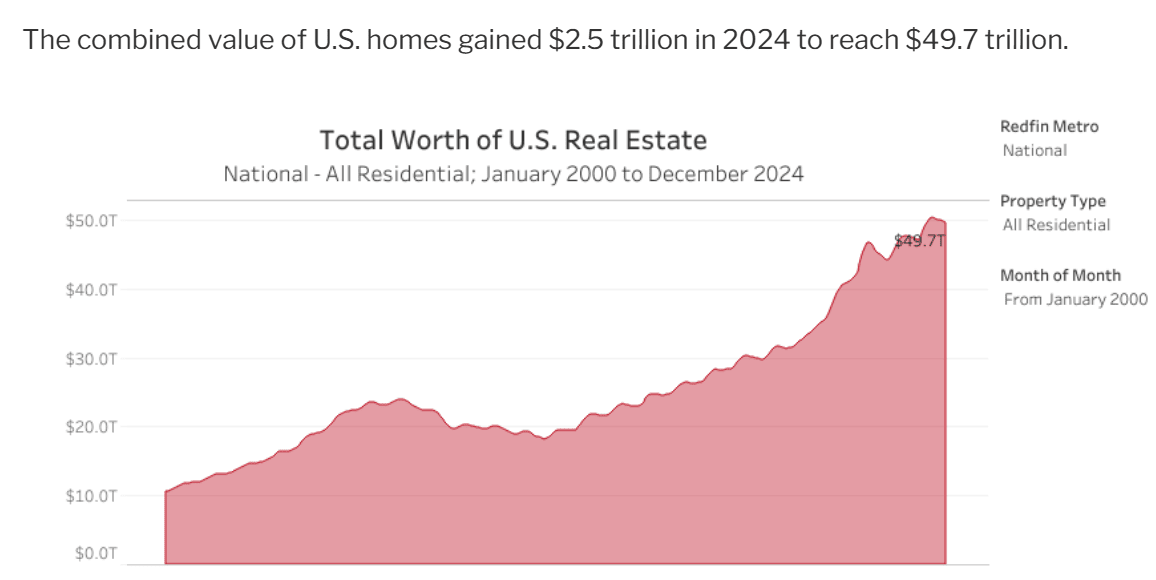

The value of U.S. real estate reached nearly $50 trillion in 2024, making it one of the world's most significant asset markets. This figure was about $23 trillion a decade ago in 2014, indicating that the asset scale in this field has doubled within ten years.

Overall size of the U.S. real estate, Awealthofcommonsense analysis report.

In June 2025, the NAR report showed that the median home price in the U.S. reached $435,300, up 2% from the same period last year. The housing inventory stands at about 1.53 million units, with a supply-demand ratio of 4.7 months. High home prices and long-term supply shortages have raised the thresholds. Coupled with persistently high mortgage rates (the average fixed rate for 30 years was about 6.75% in July 2025, while Bitcoin mortgages are currently around 9%), this has suppressed transaction volumes, and low liquidity has prompted real estate investors to seek new liquidity sources.

High interest rates hinder not only the low liquidity issue for real estate investors. Over the past five years, property owners have seen an average increase in wealth of $140,000. However, many families are reluctant to use their real estate assets for loans to release liquidity because their paths to cashing out are generally limited to two: selling the entire asset or renting it out. Using real estate for loans, given the current interest rates, is not a good choice, and selling seems also not to be a better investment decision amid continuously rising property prices.

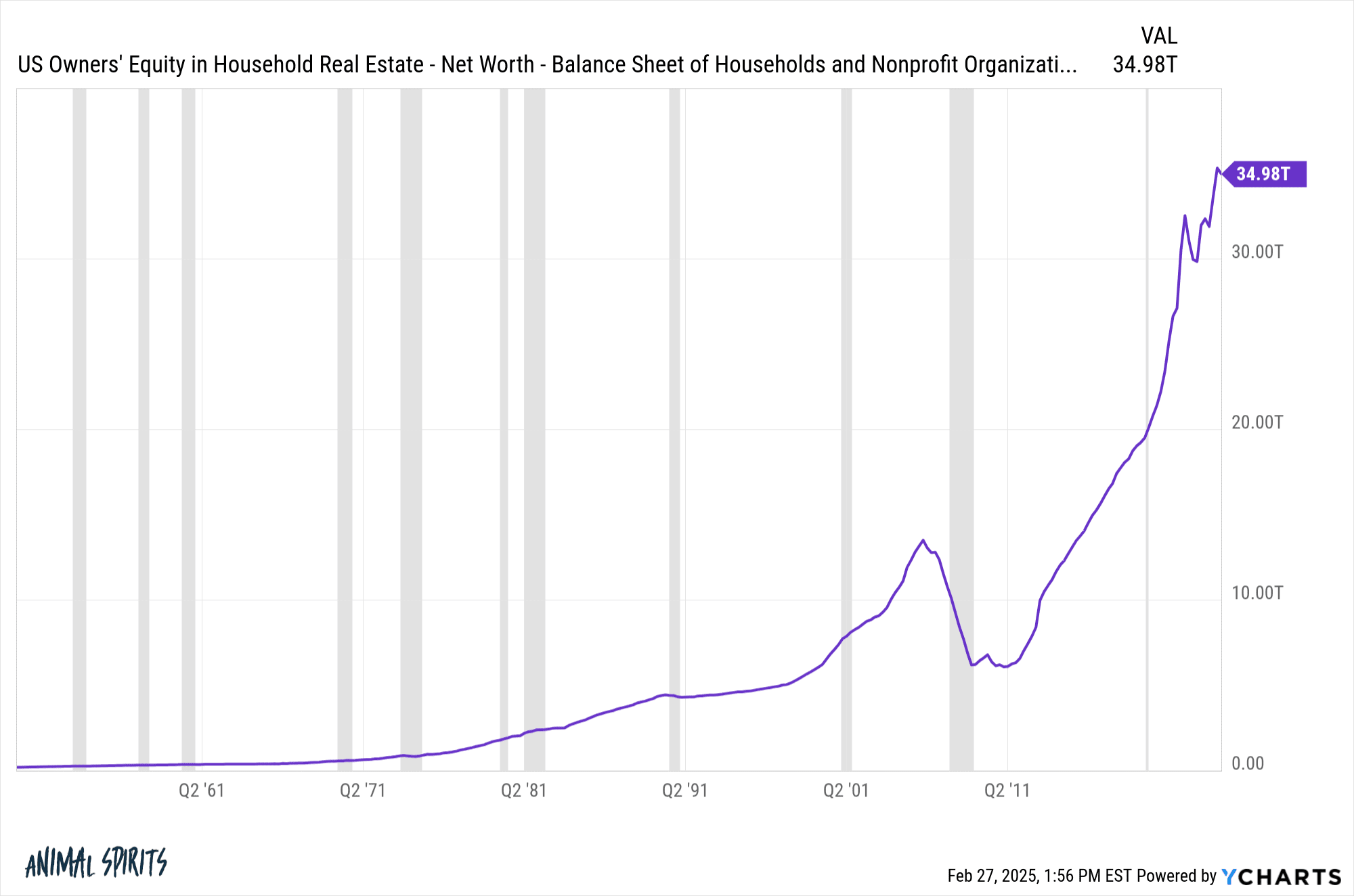

Therefore, in the overall $50 trillion real estate sector, about 70% of the equity (approximately $34.98 trillion) is owned by holders, meaning only 30% is supported by borrowed funds, with the remainder being the buyers' own capital. For instance, if a family owns a property worth $500,000, although nominally they own it, if they wish to sell, they must deduct the borrowed portion to ascertain their actual ownership. Assuming 70% equity, they would hold $350,000 in equity in that property.

U.S. real estate equity holdings, source: Ycharts.

However, just having a supply-demand relationship is far from sufficient; the concept of RWA has been developing for many years but has only truly exploded in the past two years, particularly after Trump's election in 2025, which further increased the upward slope.

The core is compliance, especially for investors in low-liquid assets like real estate. The new FHFA director, William Poole, ordered in March 2025 that mortgage giants Fannie Mae and Freddie Mac formulate plans to allow the inclusion of crypto assets in reserve assets when assessing single-family mortgage risks, without needing to convert them to dollars first. This policy encourages banks to regard cryptocurrencies as countable assets in savings, expanding the borrower base.

In July 2025, Trump signed the GENIUS Act and promoted the CLARITY Act. The GENIUS Act first recognizes stablecoins as legal digital currencies, requiring stablecoins to be fully backed 1:1 by dollars or safe assets like short-term government bonds and mandating third-party audits. The CLARITY Act attempts to clarify whether digital tokens are categorized as securities or commodities, providing regulatory pathways for practitioners.

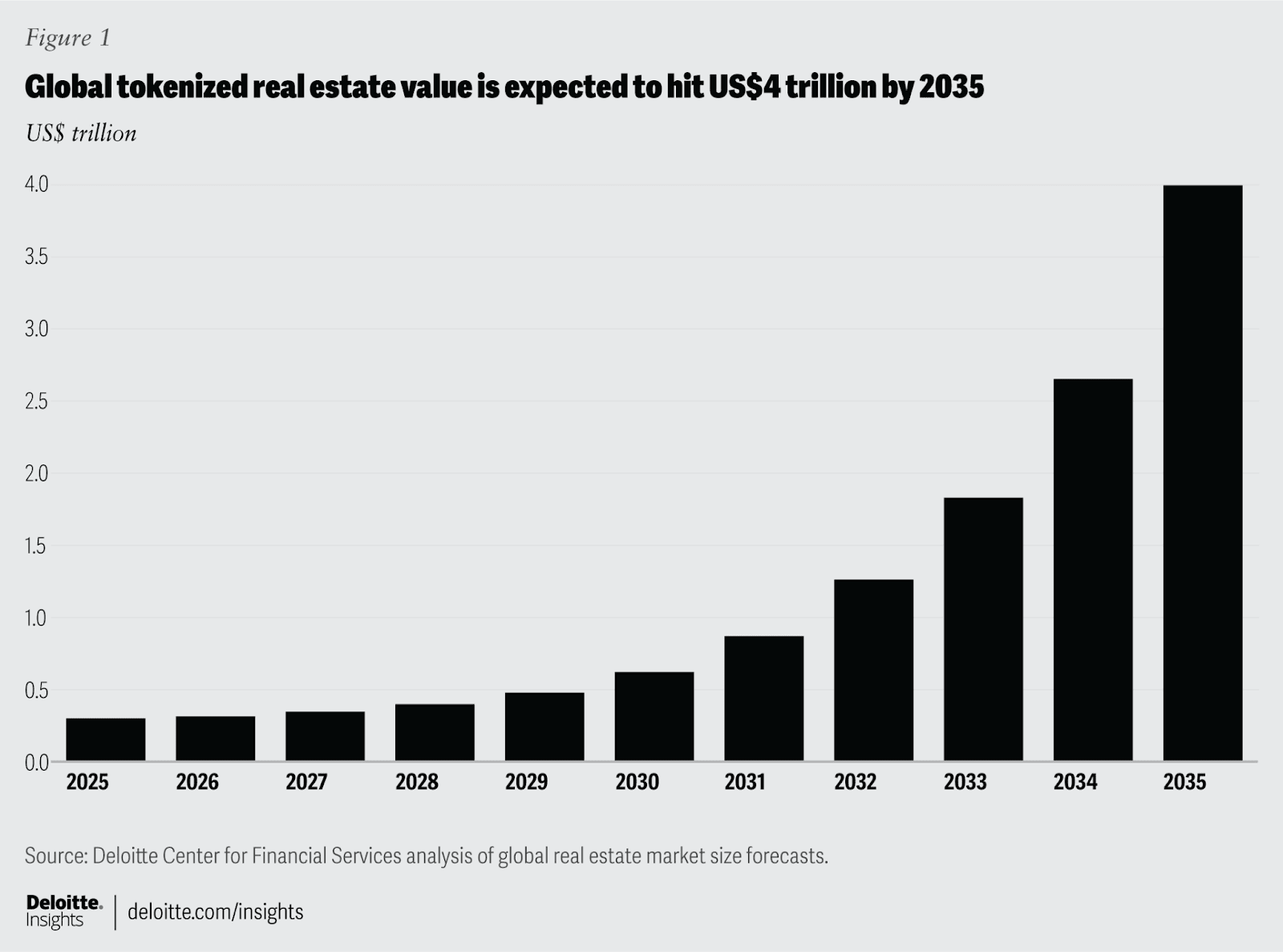

These combinations provide a greater margin of safety in the field, and combined with the scarcity attributes of real estate similar to Bitcoin (land cannot be increased, but properties can be built, akin to mining), it makes the two easier to combine. Digitalization helps break down high barriers. One of the big four accounting firms, Deloitte, predicts that by 2035 approximately $4 trillion in real estate may be tokenized, far exceeding the less than $300 billion in 2024.

Tokenization can break down large real estate into smaller shares, providing global investors with a low-threshold, high-liquidity way to participate, while also creating cash flow for sellers and buyers who originally lacked funds. That said, while $4 trillion is an attractive figure, it is debatable, much like institutional predictions that ETH's market cap will reach $85 trillion in the future, but how far has it actually developed? Perhaps we can find some alpha in the market.

Fragmented? Lending? Renting? Providing liquidity? Play real estate like you play DeFi.

Unlike low-liquid counterparts like gold and art, real estate inherently carries additional financial attributes. Its connection to crypto further diversifies these attributes.

While there have been previous attempts, the collaboration between the Harbor platform and RealT in 2018, which launched blockchain-based real estate tokenization services, is considered one of the earlier and more substantial real estate tokenization projects.

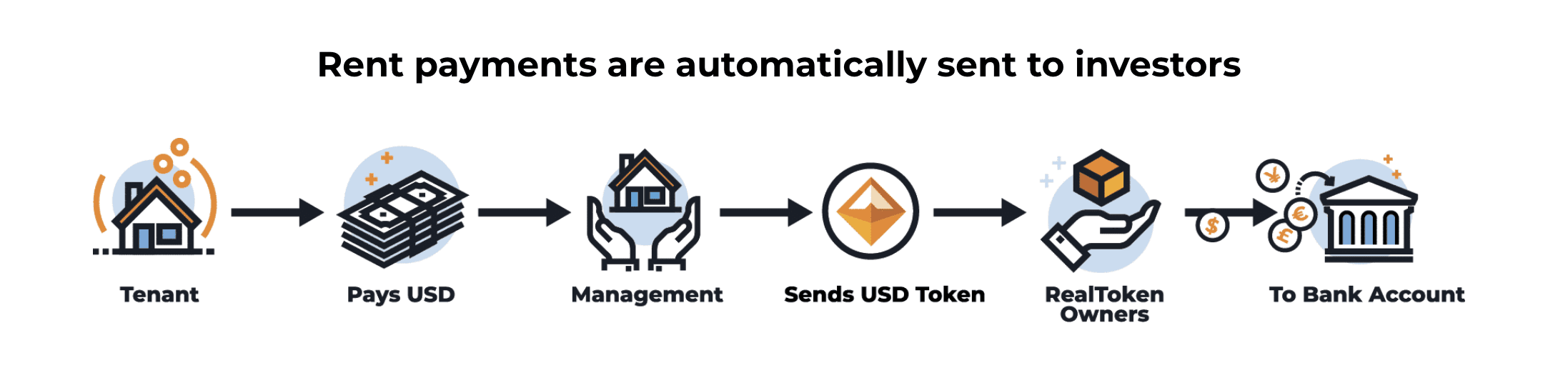

Specifically, the RealT platform uses blockchain to split property rights into tradable RealTokens. Each property is owned by an independent company (Inc/LLC); purchasing RealTokens is equivalent to holding a share of that company and proportionally enjoying rental income. The platform employs Ethereum's authorization issuance mechanism, keeping the investment threshold low (usually around $50), and both transactions and rental income distribution occur on-chain, relieving investors of the daily management work typical of traditional landlords. RealT distributes rental income weekly to holders in stablecoin (USDC or xDAI).

The expected yield comes from the Return on Net Assets (RONA), which is calculated as annual net rental income divided by total property investment. For example, if a property’s expected annual rental income after expenses is $66,096 and the total investment is $880,075, then the RONA is 7.51%. This value does not include leverage or property appreciation gains. Currently, the platform’s average yield fluctuates between 6% and 16%.

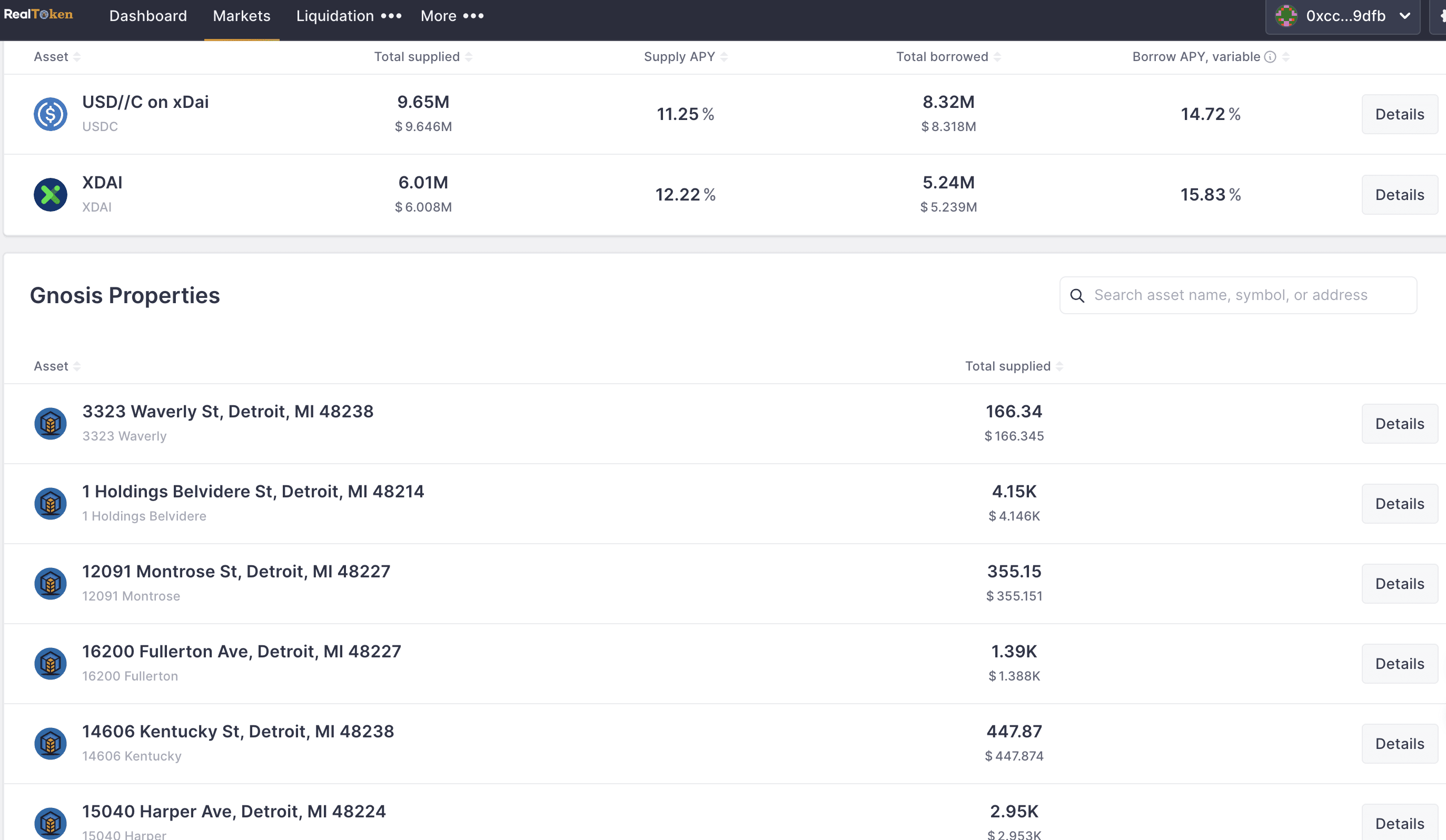

Once tokenized, the next natural step is to apply it. RealT’s properties do not have loans; all funding comes from selling RealTokens. However, to allow holders to flexibly utilize assets, RealT has launched the RMM (Real Estate Money Market) module.

Based on the Aave protocol, RMM allows you to do two things: first, provide liquidity, similar to LP interest in DeFi, where investors can deposit USDC or XDAI into RMM to receive corresponding ArmmTokens, which accumulate interest in real-time. Secondly, by mortgaging RealTokens for loans, you can use your held RealTokens or stablecoins as collateral to borrow assets like XDAI. There are also two loan rate options: fixed rate (similar to short-term fixed rates but will adjust when utilization is too high or rates are too low) and variable rate (which fluctuates based on market supply and demand).

Opening up this lending path means leverage is possible, just like how real estate investment groups borrowed money to buy houses years ago, using mortgage loans to buy more houses. By mortgaging RealTokens to borrow stablecoins and then purchasing RealTokens, this can be repeated several times to increase overall returns. It is important to note that with each layer of leverage added, the health factor decreases and risk increases.

Note: The health factor is the inverse ratio of the mortgage value to the loan value; the higher the health factor, the lower the risk of liquidation. A health factor dropping to 1 means that the collateral value equals the loan value, which could trigger a liquidation. Ways to avoid liquidation include repaying part of the loan or adding more collateral (similar to margin in perpetual contracts).

Beyond using real estate as collateral for loans, recent discussions have increasingly focused on using crypto-native asset collateral to buy homes. Financial technology company Milo allows borrowers to use Bitcoin as collateral to obtain up to 100% loan-to-value mortgages. As of early 2025, it has completed $65 million in crypto mortgage business, with total loans exceeding $250 million. Policy levels are also 'green-lighting' this model, as the FHFA requires mortgage giants Fannie Mae and Freddie Mac to consider compliant crypto assets in their risk assessments. While crypto mortgage rates are generally close to or slightly higher than traditional mortgage rates, their main attraction lies in the ability to finance without selling crypto assets.

Further Reading: (Bitcoin Mortgages, a $6.6 Trillion New Blue Ocean)

A Redfin survey shows that about 12% of first-time homebuyers in the U.S. used cryptocurrency gains to pay down payments (through sales or mortgage loans) after the pandemic. Coupled with the shift in policy direction, this will undoubtedly attract 'big businesses,' and 'Crypto Real Estate' is also welcoming the entry of high-end real estate economic companies for the first time.

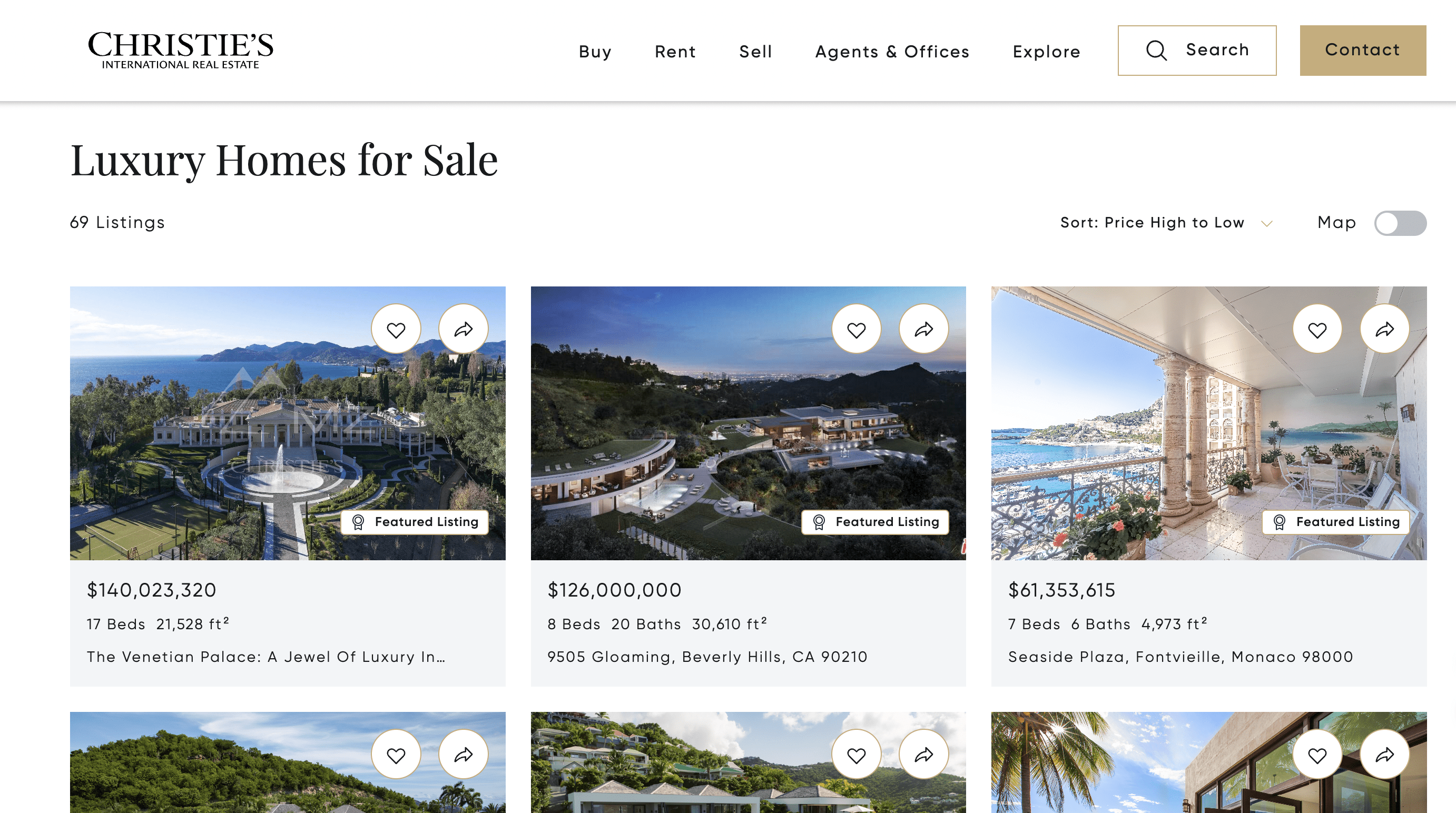

In July 2025, Christie’s International Real Estate took the lead in establishing the world's first luxury real estate department focused on cryptocurrency, marking a symbolic case of integration between traditional high-end real estate brokerage and digital assets. Interestingly, this initiative did not stem from a top-down strategic push but in response to the genuine needs of high-net-worth clients.

Christie’s executives stated, 'An increasing number of affluent buyers wish to complete real estate transactions directly with digital assets, prompting the company to build a service framework that supports full-process crypto payments.' In Southern California, Christie’s has completed multiple luxury transactions fully paid in cryptocurrency, totaling over $200 million, all at the 'eight-digit' level for top-tier residences. Currently, Christie’s holds a crypto-friendly property portfolio valued at over $1 billion, including many luxury homes willing to accept 'pure cryptocurrency offers.'

One mansion accepting pure cryptocurrency payments, valued at $118 million, "La Fin," is located in Bel-Air, Los Angeles, featuring 12 bedrooms, 17 bathrooms, a 6,000-square-foot nightclub, a private wine cellar, a subzero vodka tasting room, a cigar lounge, and a gym with a climbing wall. Previously, the listing price was as high as $139 million, source: realtor.

Christie’s crypto real estate department not only provides payment channels based on mainstream crypto assets like Bitcoin and Ethereum but also collaborates with custodians and legal teams to ensure transactions are completed within a compliant framework. This includes cryptocurrency payment custody, tax and compliance support, and asset matching (exclusive crypto real estate portfolios that meet specific investment needs of high-net-worth clients).

Aaron Kirman, CEO of Christie’s Real Estate, predicts that 'in the next five years, over one-third of residential real estate transactions in the U.S. may involve cryptocurrency.' Christie’s transition indirectly confirms the penetration of crypto assets among high-net-worth individuals and foreshadows a structural change in traditional real estate transaction models.

Infrastructure is becoming more complete, but it seems that 'user' education still has a long way to go.

As of now, the tokenization of real estate projects has begun to take shape, but it seems to still fall short of expectations. RealT has tokenized over 970 rental properties to date, generating nearly 30 million in pure rental income for users; meanwhile, Lofty has tokenized 148 properties across 11 states, attracting about 7,000 monthly active users, who share approximately 2 million in rental income annually through token ownership. The scale of several projects hovers around tens of millions to hundreds of millions, and their inability to break through may have multiple reasons.

On one hand, blockchain does indeed free transactions from geographic restrictions, allowing for cross-border instant settlement, and transaction fees are lower compared to traditional real estate transfer costs. However, investors need to understand that this is not a "zero cost" ecosystem: token minting fees, asset management fees, transaction commissions, network fees, and potential capital gains taxes constitute a new cost structure. Compared to the "one-stop service" of traditional real estate agents and lawyers, crypto real estate requires investors to actively learn and understand smart contracts, on-chain custody, and crypto tax regulations.

On the other hand, while liquidity is a selling point, it is accompanied by higher volatility. Tokenized properties can be traded on the secondary market around the clock, allowing investors to receive rental income and exit positions at any time. However, when liquidity is insufficient, token prices may be significantly higher or lower than the true valuation of the property itself, with market fluctuations potentially outpacing the cycles of physical real estate, increasing the speculative nature of short-term trading.

Additionally, many platforms have introduced DAO (Decentralized Autonomous Organization) governance, allowing investors to vote on matters such as rent and maintenance. This sense of participation is akin to playing Monopoly, lowering the threshold and enhancing interactivity, but it also imposes new demands on users: they need to understand property management and have awareness of on-chain governance and compliance. In the absence of sufficient education, investors may misjudge risks and view digital real estate as a short-term arbitrage tool rather than a long-term asset allocation.

In other words, the real threshold for crypto real estate is not in technology, but in cognition. Users need to understand mortgage rates, liquidation mechanisms, on-chain governance, tax reporting, etc., which is a disruptive change for groups accustomed to traditional home buying models.

As regulation becomes clearer, platform experiences are optimized, and mainstream financial institutions get involved, the future of crypto real estate is expected to shorten this educational curve. However, in the foreseeable years, the industry still needs to invest more resources in user training, risk control education, and compliance guidance to truly transition 'crypto real estate' from a niche experience to widespread adoption.