The (2025 Global Stablecoin Industry Development Report) jointly released by PANews and the Mobile Payment Network tracks and analyzes the overall situation of the stablecoin industry, combining on-chain transaction data, policy developments, and industry evolution paths, systematically sorting through six dimensions.

Source: PANews

Original Author: Frank

The year 2025 is a key milestone in the development of stablecoins. In this year, stablecoins not only set records in market size and trading activity but also saw an acceleration in regulatory policies and capital interest. A product originally from the internal 'safe haven' tools of the crypto market is gradually moving toward the forefront of global payments, cross-border trade, DeFi infrastructure, and even sovereign credit.

The (2025 Global Stablecoin Industry Development Report) jointly released by PANews and the Mobile Payment Network points out that stablecoins have become one of the most critical infrastructures connecting traditional finance and the crypto world, and are changing the global financial operating landscape. The report tracks and analyzes the overall situation of the stablecoin industry, combining on-chain transaction data, policy developments, and industry evolution paths, systematically sorting and analyzing six dimensions: development history, market structure, application scenarios, global regulation, development potential, and potential risks.

(The full report can be downloaded at the end of this document)

U.S. dollar stablecoins hold an absolute advantage.

The report finds that in the global stablecoin market, the market share of U.S. dollar stablecoins holds absolute dominance, with an issuance volume of 256.4 billion USD, while fiat stablecoins from other countries are still in their infancy, with the second-ranked euro stablecoin only reaching a scale of 490 million USD. The scales of yen, pound, won, and lira stablecoins range from hundreds of thousands to millions of USD. Thus, non-U.S. fiat stablecoins still hold considerable potential.

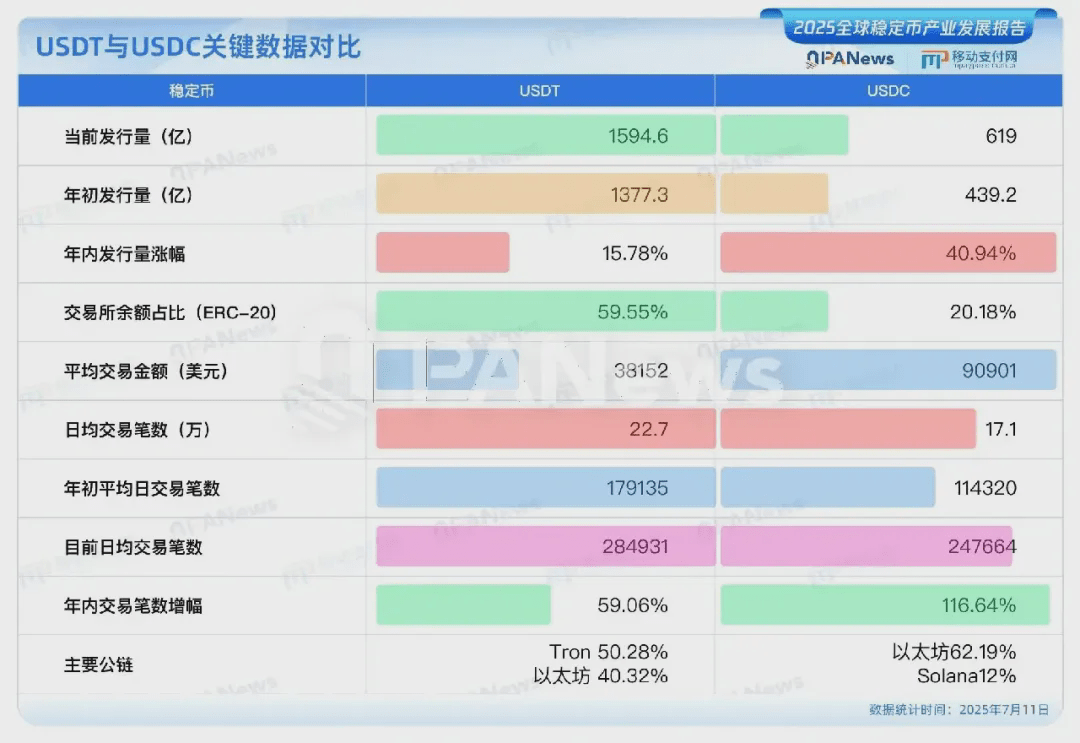

As of July 2025, the total market value of global stablecoins has exceeded 250 billion USD, showing significant growth since the beginning of the year. Among them, Tether (USDT) and Circle's USDC together occupy 86.5% of the market, forming a dual oligopoly in the stablecoin field. Meanwhile, the annual on-chain transfer amount reaches 36.3 trillion USD, surpassing the total annual transaction volume of Visa and Mastercard, becoming a new cornerstone of the global payment network. In addition, USDC has shown significant growth in 2025, with an annual growth rate of 40.9%. Based on this growth rate, USDC is expected to surpass USDT around 2030.

This outbreak is not a fleeting phenomenon, but the result of multiple forces working together.

Major economies such as the U.S., Europe, and Hong Kong are gradually advancing stablecoin legislation, with regulatory paths becoming increasingly clear.

Traditional financial and tech giants such as JPMorgan, BlackRock, PayPal, JD.com, and Ant Group are all getting involved.

USDC's parent company Circle successfully went public in the U.S., igniting the imagination of the capital market regarding stablecoins.

Users in several high-inflation countries (such as Argentina, Turkey, and Nigeria) regard stablecoins as a 'digital dollar' hedging tool.

Emerging scenarios such as DeFi, RWA, and payment settlements continue to inject actual demand into stablecoins.

In terms of on-chain activity, the number of monthly active stablecoin addresses globally has exceeded 30 million, while the total number of on-chain holding addresses has surpassed 168 million. According to Visa data, after excluding robots and exchange wallets, the proportion of transactions led by real users has increased from less than 15% in 2023 to around 22% currently, with the user structure gradually transitioning from arbitrage robots to enterprises and retail investors.

From Circle to JD.com, stablecoins are entering the 'mainstream battlefield'.

The role of stablecoins is evolving from 'trading hedging anchor' to 'mainstream digital financial asset'. Since the beginning of this year, many global tech giants and financial institutions have been increasing their involvement in stablecoins.

Circle's IPO: Stablecoin issuer Circle successfully listed on the U.S. stock market, with its market value once approaching 100 billion RMB, becoming the first 'quasi-systemically important financial company' in the stablecoin industry.

PayPal and Visa integrate stablecoin settlements: PayPal launches the PYUSD stablecoin and goes live on high-performance public chains like Solana; Visa introduces USDC in B2B settlements with Worldpay.

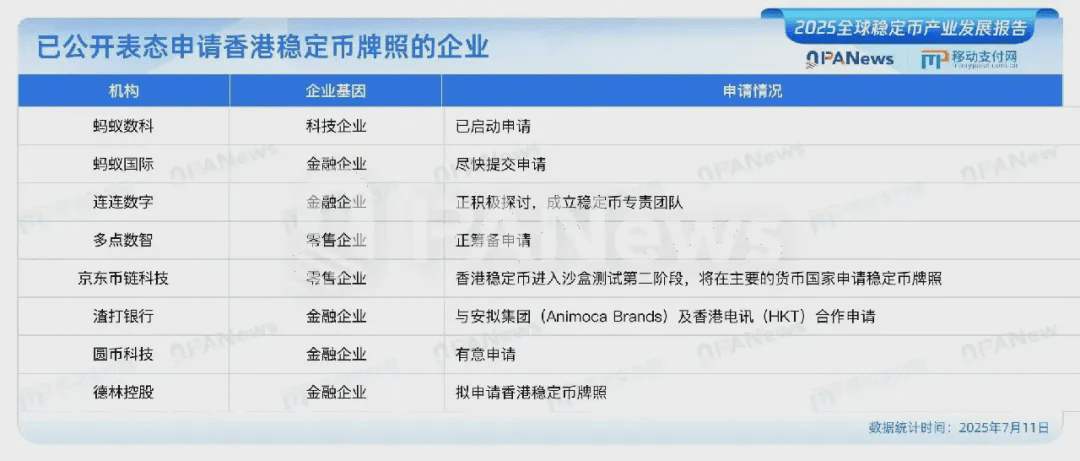

JD.com and Ant Group enter the Hong Kong stablecoin market: JD.com's stablecoin has entered the regulatory sandbox testing phase in Hong Kong, with application scenarios including cross-border payments, investment transactions, and consumer settlements.

Shopify and Walmart support stablecoin payments: Retail giants promote the direct use of stablecoins for online retail payments through partnerships with Stripe, Coinbase, and others.

Emerging public chains see high growth: New public chains like Base and Solana are attracting a large number of stablecoin deployments due to low fees and high scalability, with Solana's stablecoin market value increasing by over 600% this year.

The joint promotion by traditional finance, internet platforms, and crypto-native forces has enabled stablecoins to upgrade from 'crypto-specific settlement tools' to widely usable digital payment intermediaries, also raising higher demands for regulatory compliance.

Behind the scale boom, there remain structural uncertainties.

However, behind the hot market performance, stablecoins also face many structural challenges and controversies.

First is the issue of 'real usage scale'. The report indicates that although the total transfer amount of stablecoins reaches 36 trillion USD, as much as 70-80% is composed of 'virtual traffic' such as transfers between robots and exchanges, and the actual C-end or enterprise usage scale still needs further exploration and definition.

Secondly, there is the issue of 'anchoring mechanisms and transparency'. Although USDT sits at the top of the industry, it has yet to release a complete audit report issued by one of the 'Big Four accounting firms', and its reserve asset structure and risk exposure have long been a point of contention in the market; while USDC is more transparent and compliant, it still lags behind USDT in terms of application popularization and ecosystem integration.

In addition, there are still differences and games among regulatory policies in various countries; some regions have yet to open the use of stablecoins, while some markets (such as Hong Kong and Singapore) are actively taking on the role of experimental fields for institutional innovation.

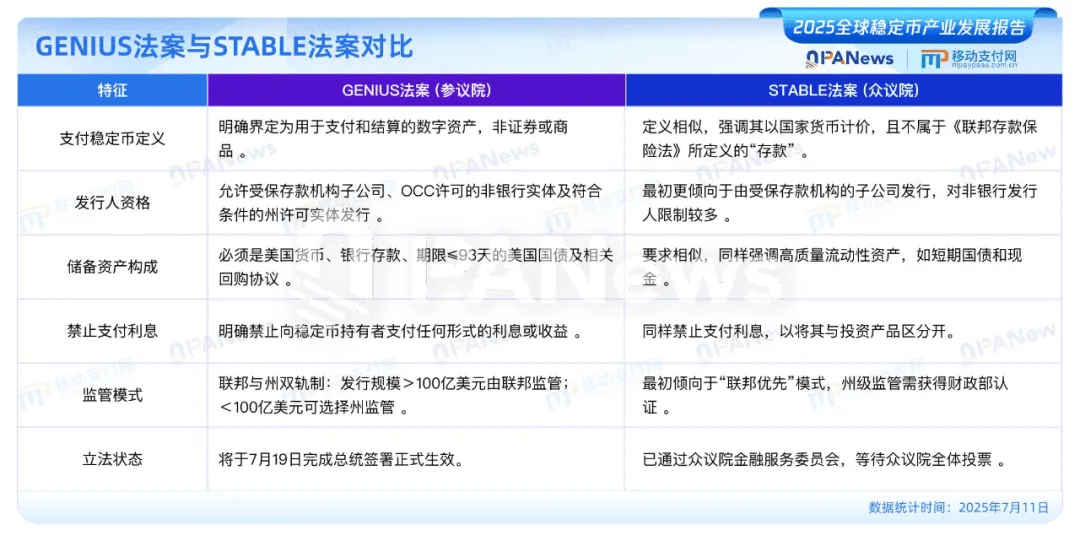

It is noteworthy that the United States (GENIUS Act) has explicitly stated that stablecoins are not classified as securities, prohibits algorithmic stablecoins, and requires 100% reserves to be in highly liquid assets (such as cash and short-term U.S. Treasury bonds). If this legislation comes into effect, it will profoundly impact the operational logic and global compliance structure of existing mainstream stablecoins.

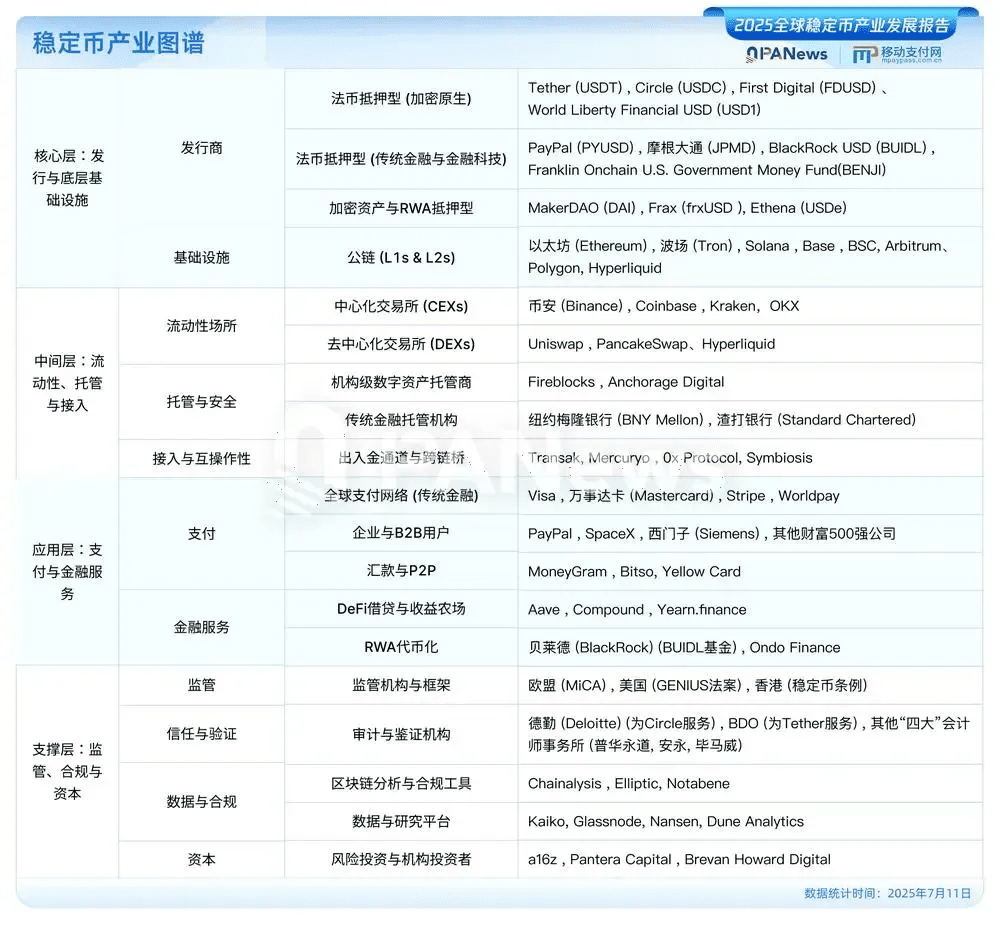

Report Highlights: A panoramic view of the evolution route of stablecoins across six dimensions.

The report jointly released by PANews and the Mobile Payment Network adopts a method of on-chain statistics + categorized tracking + public information cross-validation, providing a comprehensive overview of the development of stablecoins, covering the following six dimensions:

1. Development History: Reviewing the ten-year evolution route of stablecoins from BitUSD to USDT, DAI, and USDC.

2. Market Structure: Detailed analysis of the 'USDT + USDC' dual oligopoly structure, distribution of public chain issuance shares, monthly active user trends, and other core data.

3. Application Scenarios: Focusing on the key roles of stablecoins in cross-border payments, DeFi, retail payments, and RWA fields.

4. Global Regulation: A systematic overview of regulatory dynamics and legislative paths in major economies such as the U.S., Europe, Hong Kong, Japan, and South Korea.

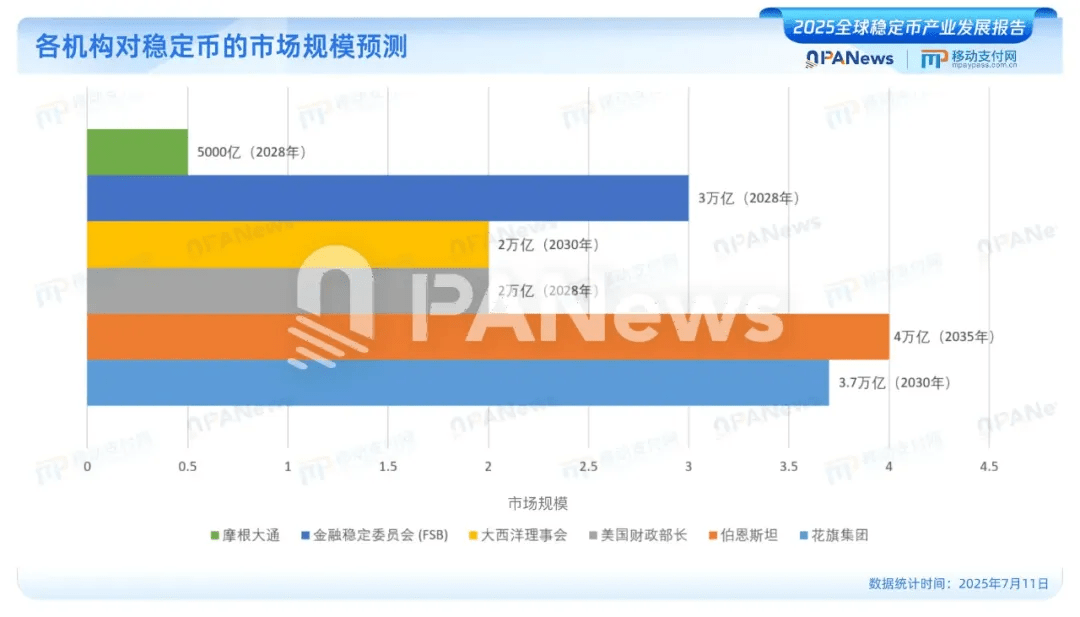

5. Future Potential: Analyzing how stablecoins can become a global payment network, a force for purchasing U.S. Treasury bonds, and the competitive relationship with CBDCs.

6. Risk Warnings: Covering potential challenges such as decoupling, audit transparency, systemic attacks, and money laundering regulatory issues.

The report also specifically points out that non-U.S. dollar stablecoins are still in the early stages of development: the market value of euro stablecoins is less than 500 million USD, while stablecoins for currencies like the yen, pound, and won are mostly in the tens of millions of USD, indicating significant expansion potential in the future.

🔗 Download report link:

https://www.panewslab.com/qre/gsidr/2025