As more US-listed companies announce their transformation into 'cryptocurrency reserve strategy' companies, claiming to buy and hold tokens as core financial allocations, this trend successfully attracts investors' attention. However, behind the seemingly harmonious combination of the crypto space and traditional finance lie layers of risks, from founders swapping hands to the exit actions of venture capitalists, ultimately still a capital game for retail investors.

Exchanging tokens for stocks: from founders to investors, everyone is 'swapping hands'.

Yesterday, The Ether Machine, Inc. (NASDAQ: ETHM), operated by Ethereum veteran Andrew Keys and members of Consensys, with investment from VCs like Pantera and Kraken, publicly debuted, claiming to become the world's largest public investment vehicle for Ethereum.

(The Ether Machine announces its listing: led by Pantera Capital, supported by over $1.5 billion in funding)

However, upon examining the process of ETHM's new stock subscription financing of over $800 million, it mainly involves founder Andrew Keys 'investing' the early accumulated 169,000 ETH (approximately $645 million) into the company he founded and issuing new shares in exchange, completing the investment, fundraising, and purchase of ETH.

In other words: 'ETH is mine, the extra stocks are also mine, and in the end, it’s declared that fundraising has been completed.'

This is similar to yesterday's $200 million equity credit agreement between Mercurity and Solana Ventures, where the Solana official fund can purchase shares at a favorable price, while Mercurity can obtain funds or directly allocate SOL.

(US stock Mercurity Fintech claims to create a SOL treasury with Solana Ventures, which Solana Ventures denies)

This type of operation seems unnecessary to hide and has even become a tacit gameplay in the recent trend of 'US stock shell transformations into MicroStrategy'.

Token-stock binding, double the risk: The correlation between stock prices and token prices becomes an unexploited bomb in the market.

These crypto reserve companies tightly bind stock codes with cryptocurrencies, seemingly creating a myth where stock prices rise along with token prices, but in reality, it's a double leverage on market volatility, and perhaps the two are not clearly connected. The recent performance of MicroStrategy, the largest in market capitalization, is the best proof.

(Why does MicroStrategy MSTR not rise even as Bitcoin hits new highs?)

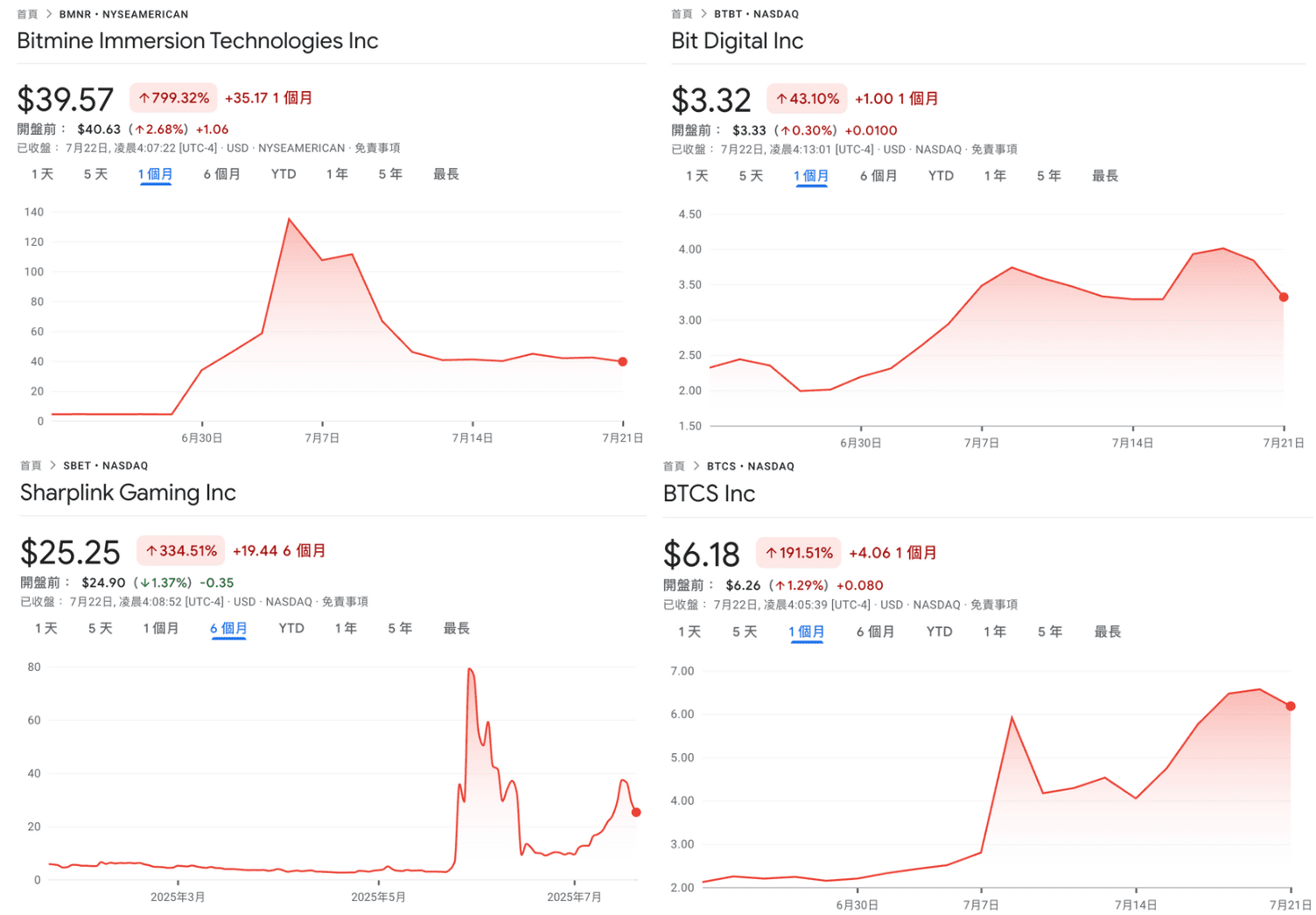

In fact, multiple Ethereum reserve companies have become heavy casualties of the downturn. Even though most doubled within a month, companies like BMNR, SBET, BTBT, and BTCS have all dropped 75%, 35%, 25%, and 27% from their peaks.

These declines are not due to the deterioration of corporate operations and are unrelated to ETH's recent strong performance. One reason may be a decrease in speculative fervor, while another may relate to unknown hidden relationships with crypto VCs.

(Not every company can be MicroStrategy: The 70% drop of Sharplink reveals the risks of crypto reserve companies)

The US stock market is a good place for VCs to exit: a complete cycle of speculation and cashing out without hesitation.

Market observer @_FORAB has found that behind these cases often lurks the presence of large venture capital institutions or market makers. For example, Pantera Capital not only appears in multiple cases like BMNR, SBET, and ETHM, but also participated in the latest Ethena ENA reserve company acquisition of StablecoinX (formerly TLGY).

This wave is a self-rescue market for many VCs and market makers.

Invested too much in garbage projects and tokens, and it's hard to revive them even with more money, but I happen to have a batch of ETH, SOL, or leftover USD funds.

A few companies together invest in a US-listed shell company, I invest money, you invest tokens, issue a bunch of stocks to ourselves, officially announce the transformation into a MicroStrategy, and sell to the lucky ones who come over from the US stock market. Subsequently, we can print more shares and distribute dividends to shareholders.

— AB Kuai.Dong (@_FORAB) July 21, 2025

The entire model seems to have already established a cash-out template:

VCs hold many tokens (such as BTC, ETH, or SOL)

Acquire a US-listed company and 'invest and take shares' using proprietary tokens.

The company issues new shares at a discount to VCs, and releases a press release announcing its transformation into a crypto reserve company.

After a wave of market speculation, cash out from US stocks at a peak stock price.

Looking back at the recent sluggish performance of many crypto project tokens, this complete cash-out strategy has become the profit outlet for current VCs, while the true payers are US stock investors who FOMO and fail to see the truth.

The craze for crypto reserve companies is merely a transfer of wealth; how long can the US stock market sustain this?

On the surface, these crypto reserve companies attempt to inject crypto assets to keep up with capital narratives, but in reality, this is an asset transfer action conducted by VCs in collaboration with US companies. They acquire shares at nearly zero cost, package the transformation as potential and value, and then exit with profits as the market heats up.

However, the end of this financial game may still lead to a cliché ending. Capital players choose to exit from US stocks, and once the market's absorption capacity weakens or regulatory concerns arise, the signs of bubble bursting can be seen.

This article 'I provide tokens, you provide money; US stock investors take the reins: Revealing the underlying risks of crypto reserve company speculation' first appeared on Chain News ABMedia.