Key metrics: (14Jul 4pm HK -> 21Jul 4pm HK)

BTC/USD -2.8% ($122,800 -> $119,400) , ETH/USD +25.0% ($3,040-> $3,800)

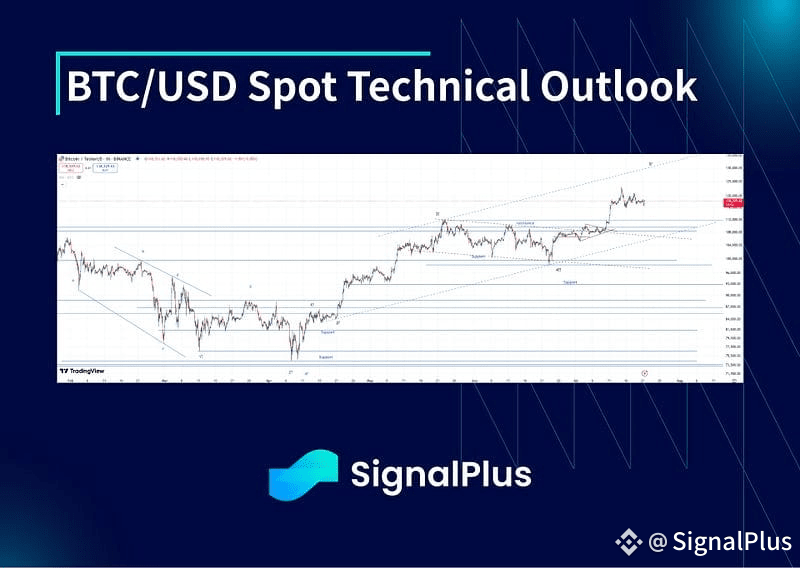

Having finally taken the lid off above $112k, BTCUSD has found a short-term consolidation level around $117–120k . We expect the most probable path from here is to continue onwards and complete the progression with terminal target in the $125–135k range, but there is a high risk of elongation/further correction given the price action to get here

Support below here is initially at $116k and then below that at the previous highs of $112k. A clean move below $112k would leave us revisiting the question ‘is the upward move already complete?’. Topside target continues to be $125–135k after which we expect the market to enter into a more volatile and choppy corrective period that could span 2–6 months

Market Themes

Risk on sentiment continues to dominate as the market remains unperturbed by external noise around geopolitics, tariffs or even rumours of Trump firing Powell as Fed chair. Ultimately it feels as though equity markets are in ‘short cover’ mode as retail exuberance picks up and ‘everything up’ seems to be the nature of the current rally. While fundamentals struggle to justify these local highs in valuations, the market seems to be looking ahead to the upcoming Fed cuts (with some dovish notes from likes of Waller in recent weeks), but also importantly this last leg of the rally feels under-subscribed and that is perhaps driving some forced participation at these levels

Crypto as a complex has seen participated in this ‘everything up’ rally, most notably in Alt coins as Bitcoin remains well-subscribed and faced some strong initial resistance after breaching through $123k briefly at the start of last week. Likely we are seeing a bit of a short-term rotation particularly among the crypto native community, with the likes of ETH/BTC healthily off the lows and triggering some stops. ETF inflows into Bitcoin from TradFi remained positive every day for the 2nd week running, indicating that AUM continues to get allocated to the complex in a healthy manner, while ETH ETF inflows picked up dramatically as ETH treasury companies (SBET, GAME, BTBT etc) posted huge rallies on the week and proceeded with share offerings to take advantage of the rally… and use the proceeds to buy more ETH!Given the impact the buying from MSTR had initially for BTC, the market is justifiably cautious to fade this move too early

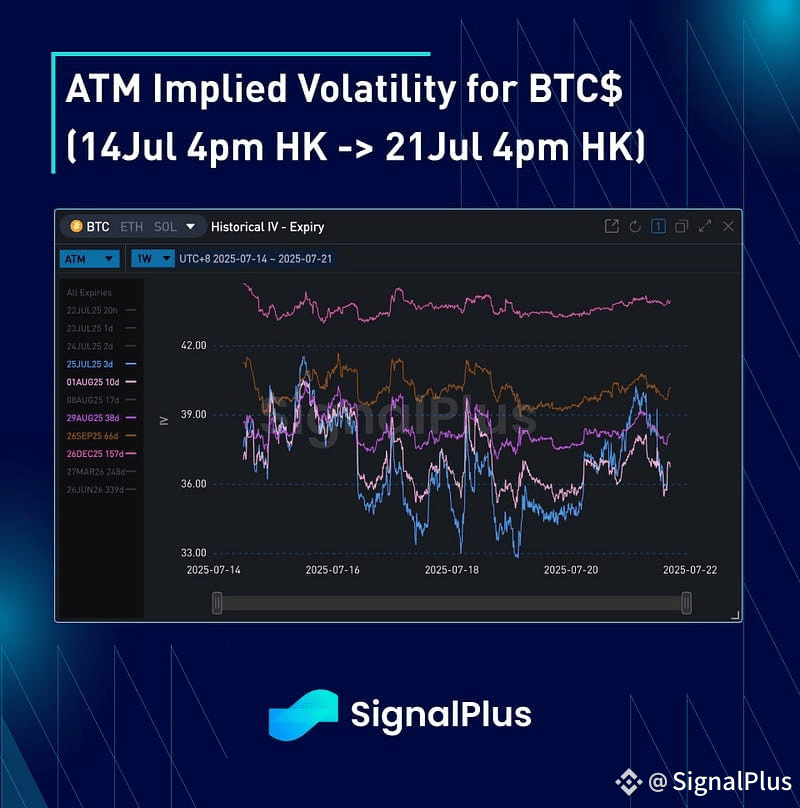

BTC$ ATM implied vols

Realised volatility has picked up in the past two weeks, climbing from a very low base of 23–27v up to 35–37v on a high frequency basis. While the absolute level of realised remains fairly low on a historic basis, the magnitude of the pick up from the lows, in combination with the spot break to a fresh range, is indicative of the market moving away from the heart of its gamma length and history has suggested this tends to eventuate in a higher vol regime further down the line. For now the market clearly has some overhang vol longs particularly in the front-end of the curve, and this combined with a lack of participation from clients due to the heart of summer, is keeping a lid on implied levels, though implied levels are showing signs of basing overall

The term structure has slowly begun to steepen out, though versus historic levels of steepness the curve is not that steep, with the market struggling to price in term premium for a materially higher vol regime further down the line. However we have begun to see buyers of year-end call-spreads as the market begins to subscribe to another wave higher for spot in Q4, and with funding/basis starting to widen out and realised picking up from a low base, we believe a reprice higher in volatility levels further out the curve is justified

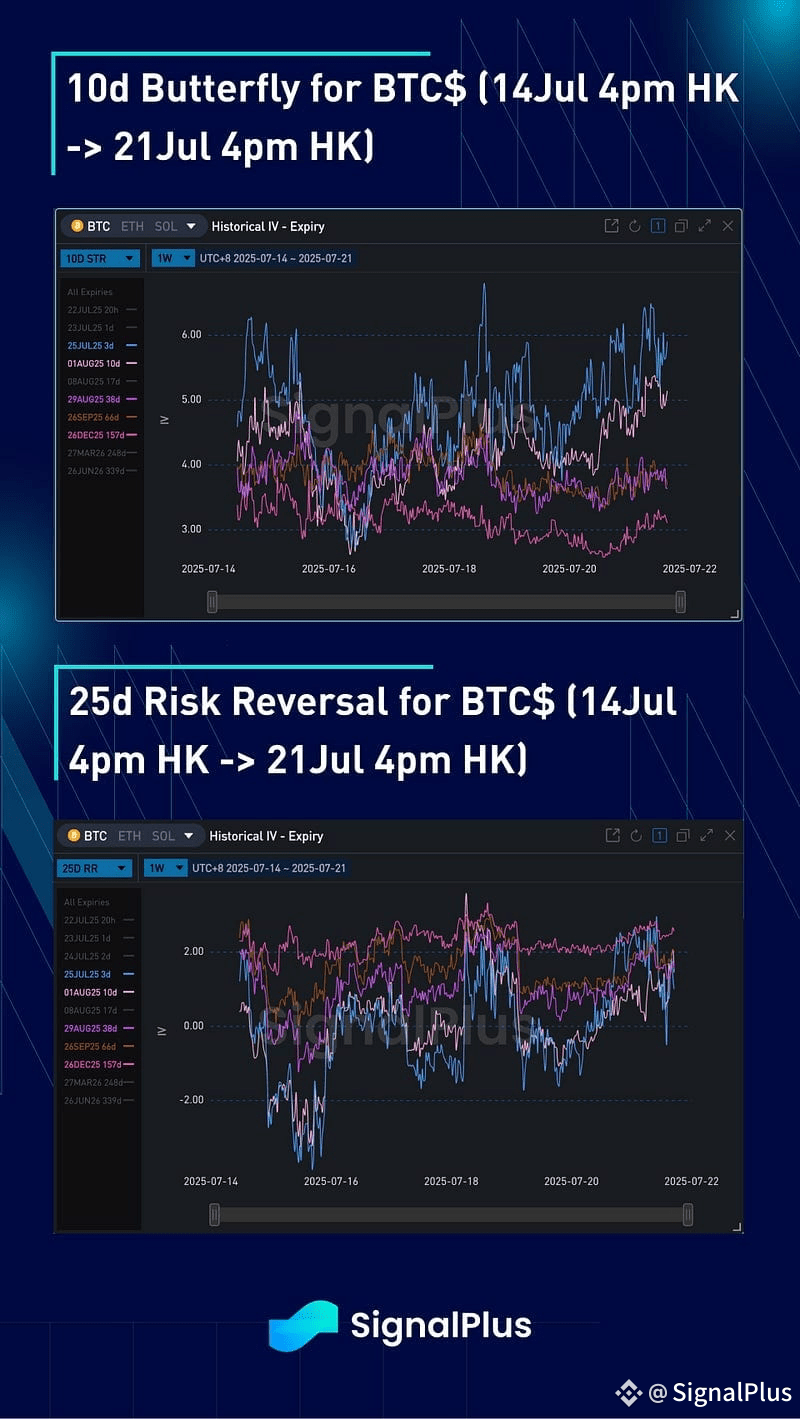

BTC$ Skew/Convexity

Skew prices were pretty static last week, with choppy 2-way price action in spot around the $117–120k range not attractive particularly strong directional interest one way or another. In longer dated tenors, the directional bias remains for topside, and this is keeping skew prices supported for calls in end-August expiries and out

Convexity prices edged higher in the front-end of the curve last week, as the market remains reluctant to hold too much local gamma in this environment given the choppy but mean-reverting nature of the spot price action. Further out the curve, demand for call-spreads has supplied the market for some convexity, which is keeping fly levels fairly suppressed in these expiries

Good luck for the week ahead!