Overnight, the Financial Times reported a significant development: President Trump is preparing to sign an executive order allowing 401(k) and other pension plans to invest in cryptocurrencies, gold, and private equity as 'alternative assets'.

According to three informed sources, the order will require regulatory agencies to reassess current pension investment restrictions, clearing obstacles for digital assets to enter the $8.7 trillion U.S. pension market.

This trend is not without warning signs. On May 28, the U.S. Department of Labor revoked guidance from the Biden era that treated cryptocurrencies with 'extreme caution', stating it involved 'regulatory overreach'. Earlier, in 2022, Republican Congressman Peter Meyer proposed the Retirement Savings Modernization Act, attempting to incorporate digital assets into the 1974 Employee Retirement Income Security Act (ERISA) framework. Although it did not pass, it planted the seeds for today's policy shift.

Trump's ambition for 'digital assets'

The core intention of this executive order is to break the long-standing focus of 401(k) plans on traditional stocks and bonds and to provide broader asset allocation flexibility.

The order will explicitly instruct Washington's regulatory agencies to thoroughly study and begin removing the existing barriers that hinder alternative assets, particularly digital assets, precious metals, and funds focused on corporate mergers, private loans, and infrastructure transactions, from being included in 401(k) professionally managed funds.

In a cautious statement to the Financial Times, the White House remarked: 'President Trump is committed to restoring prosperity for ordinary Americans and securing their economic future. However, any decision should only be considered official policy once announced by the president himself.' Nonetheless, this statement does not obscure the strong signal from the Trump administration to promote the mainstreaming of cryptocurrency.

In fact, this move is a continuation of Trump's series of pro-crypto policies. From promising during his campaign to liberate digital currencies from 'overly harsh regulation' to his family business—Trump Media & Technology Group investing over $2 billion to purchase Bitcoin and other digital currencies, and even launching its own stablecoin and other digital tokens, Trump has become a heavyweight player in the digital assets field, with his personally disclosed crypto asset holdings exceeding $51 million.

The government has also taken action; the Department of Labor revoked a policy in May that discouraged 401(k) plan managers from offering cryptocurrency investment options, paving the way for this executive order.

Interpretation: The deeper significance of opening the U.S. pension market

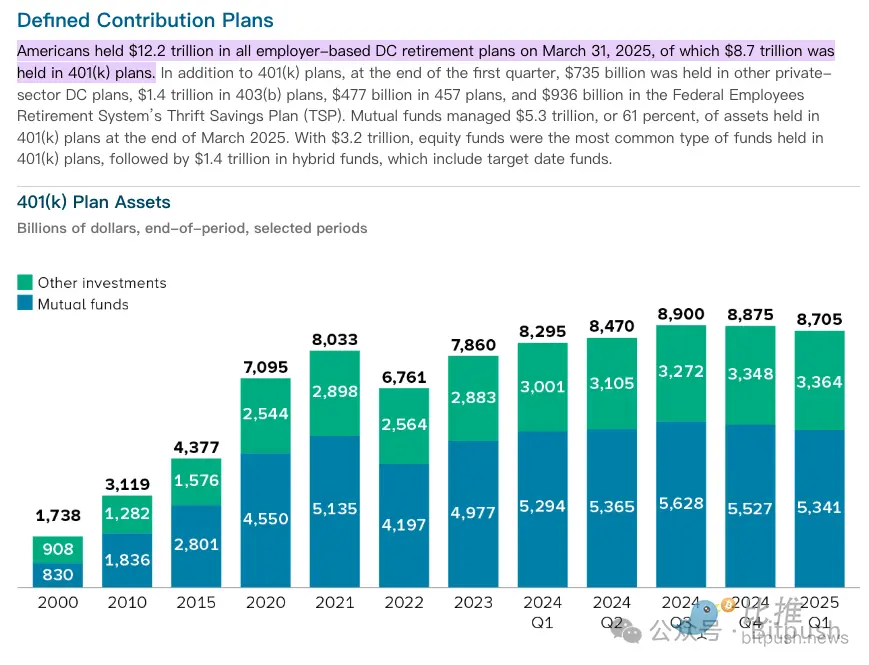

To grasp the potential impact of this policy, one must understand the structure and scale of the U.S. pension market. As one of the largest pension systems in the world, the total scale of the U.S. pension market reaches $9 trillion.

Specifically, according to public data, as of March 31, 2025, the total assets of all employer-sponsored defined contribution (DC) retirement plans reached $12.2 trillion. Notably, the 401(k) plan holds $8.7 trillion.

These massive funds mainly come from tens of millions of American wage earners. The 401(k) plan, as an employer-sponsored occupational pension, is the core of long-term savings for most wage-earning families due to its appeal of payroll deductions, tax benefits, and employer matching contributions.

Traditionally, these massive pension funds primarily flow into publicly traded securities. As of the end of March 2025, there were $5.3 trillion (61%) managed by mutual funds within 401(k) plans alone. Among these, equity funds, with a size of $3.2 trillion, have become the most common type, followed by balanced funds (including target-date funds), which manage $1.4 trillion. This asset allocation status, predominantly in stocks and bond mutual funds, provides ample space for the alternative investments promoted by Trump.

The IRA (Individual Retirement Account) provides individuals with more autonomous retirement savings options. The wealth accumulated by ordinary Americans forms a significant source of 'long money' that drives U.S. economic growth and financial market stability.

In comparison to China's pension system, both aim to construct a multi-tiered safety net. China's 'enterprise/professional annuities' are similar to the employer-sponsored nature of the U.S. 401(k), while 'individual pensions' are closer to the IRA's individual investment model. Therefore, the U.S. move to open pension investments has global implications for the wealth allocation concepts of the general public.

Private equity giants and new opportunities: the redistribution of a trillion-dollar cake

Beyond cryptocurrencies, this executive order represents a potential feast for the world's largest private equity firms, such as Blackstone, Apollo, and BlackRock. These giants have largely pinned their hopes for future growth on managing funds from ordinary retirement savers.

Private equity firms predict that once they successfully enter the 401(k) retirement plan market, they could attract hundreds of billions of dollars in new industry assets.

To this end, they have taken proactive measures to establish partnerships with large asset management companies: Blackstone has teamed up with Vanguard, and companies like Apollo and Partners Group are providing investment services to large 401(k) plan sponsors like Empower. BlackRock has also begun collaborating with third-party management firm Great Gray Trust for retirement savings plans.

As policy is brewing at the federal level, some state governments have already started pilot programs. According to previous reports, legislators in North Carolina proposed a bill allowing certain pension funds to allocate up to 5% of their balances to cryptocurrencies. The retirement systems in Michigan and Wisconsin have also actually invested in spot Bitcoin and Ethereum ETFs, providing a reference for federal-level policies.

Headwinds remain

In terms of legislation, the U.S. House of Representatives passed three important cryptocurrency-related bills on Thursday local time: the CLARITY Act, the GENIUS Act, and the Anti-CBDC Surveillance National Act. Among them, the CLARITY Act and the Anti-CBDC Surveillance National Act will be sent to the Senate for review. The GENIUS Act is expected to be signed into law by President Trump on Friday local time, marking substantial progress in Congress's efforts to promote cryptocurrency legislation and providing a clearer legal framework for the industry.

However, even with favorable legislation, the market still faces challenges. Investing retirement savings in less liquid private assets is not without risks; inherent issues such as high fees, elevated overall leverage, and lower transparency in fund asset valuations are factors that regulators and investors need to consider carefully.

When Trump's executive order meets the $9 trillion pension market, this experiment may redefine the meaning of 'retirement savings'—is it about allowing ordinary people to share in the technological dividends of the digital age? Or is it exposing pensions to new risks? The answer may depend on how regulators find a balance between innovation and protection.