External buyers are driving a paradigm shift for $ETH assets, challenging our inherent perception that it 'can only go down.'

The trading code is $ETH.

Wall Street is experiencing a highlight moment for cryptocurrency.

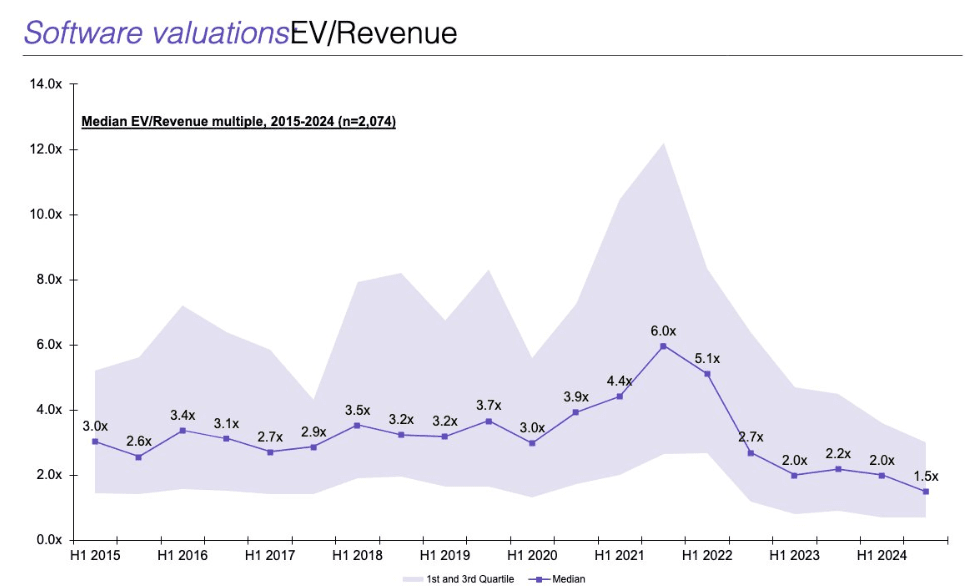

Traditional finance (TradFi) is exhausting the resources of growth narratives. AI has become the hot topic in the market, but attention to it has become excessive, and software companies are far less attractive today compared to the 2000s and 2010s.

At a deeper level, those growth investors raising capital for innovative stories and large addressable markets (TAM) know well that most AI-related companies are valued at ridiculous premium levels, and that other so-called 'growth narratives' are no longer easily found. Once highly regarded FAANG stocks are also gradually transforming into 'high quality, profit-maximizing, medium growth rate' composite assets.

For example, the median enterprise value to revenue (EV/Rev) multiple of software companies has fallen below 2.0 times.

At this time, cryptocurrency has made its appearance.

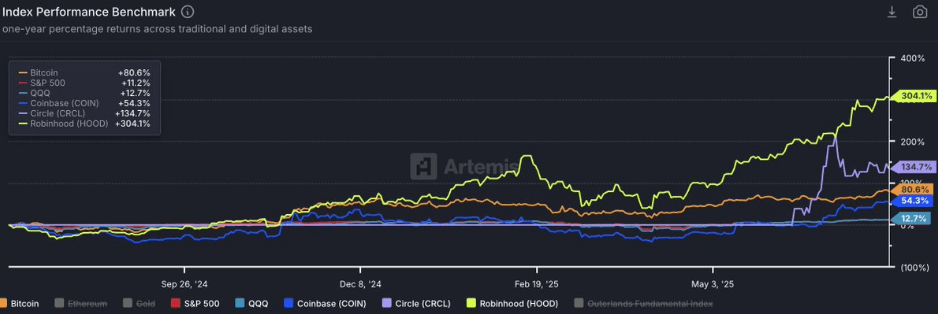

Bitcoin ($BTC) breaks its historical high, and the U.S. president heavily promotes our assets at a press conference, accompanied by a wave of favorable regulatory trends that bring the cryptocurrency asset class back into the spotlight for the first time since 2021.

This time, the protagonists are no longer NFTs and Dogecoin. This time, it’s the era of digital gold, stablecoins, 'tokenization,' and payment reform. Stripe and Robinhood are claiming that cryptocurrency will be the core focus of their next growth phase; $COIN (Coinbase) has successfully joined the S&P 500 index; Circle demonstrates to the world that cryptocurrency is attractive enough for growth stocks to overlook earnings multiples again.

But how does all of this relate to $ETH?

For us crypto natives, the realm of smart contract platforms seems very decentralized. There’s Solana, Hyperliquid, and a dozen other emerging high-performance blockchains and Rollups (on-chain scaling solutions).

We know that Ethereum's leading position has truly been challenged, and it faces existential threats. We also know it has yet to resolve the value capture issue.

But I highly doubt Wall Street understands these things. In fact, I can boldly say that most Wall Street investors know almost nothing about Solana. To be honest, XRP, Litecoin, Chainlink, Cardano, and Dogecoin might be more recognized in external markets than $SOL. After all, these individuals have been indifferent to the entire cryptocurrency asset class for several years.

What Wall Street knows is that $ETH represents the 'Lindy Effect' (the idea that things that have existed a long time are more likely to continue existing), having been tested in practice, and has been the main 'beta investment choice' alongside $BTC for years. Wall Street sees that $ETH is the only other crypto asset with a liquidity ETF. Wall Street is enthusiastic about the upcoming catalysts and classic relative value investments.

Those suited investors may not know much about cryptocurrency, but they are aware that Coinbase, Kraken, and now Robinhood have all decided to 'build on Ethereum.' With minimal due diligence, they can discover that Ethereum has the largest stablecoin pool on-chain. They will start calculating 'moon math' and soon realize that while $BTC has reached a historical high, $ETH is still over 30% lower than its peak in 2021.

You might think that relatively poor performance looks pessimistic, but these individuals have different investment approaches. They prefer to buy assets that are priced lower but have clear targets, rather than chasing those that make them question whether they have 'missed the opportunity.'

I believe they have arrived. Investment authorization is not an issue; any fund can drive cryptocurrency exposure through appropriate incentives. Although crypto Twitter (CT) has claimed for over a year that they will no longer touch $ETH, the trading code has performed consistently well over the past month.

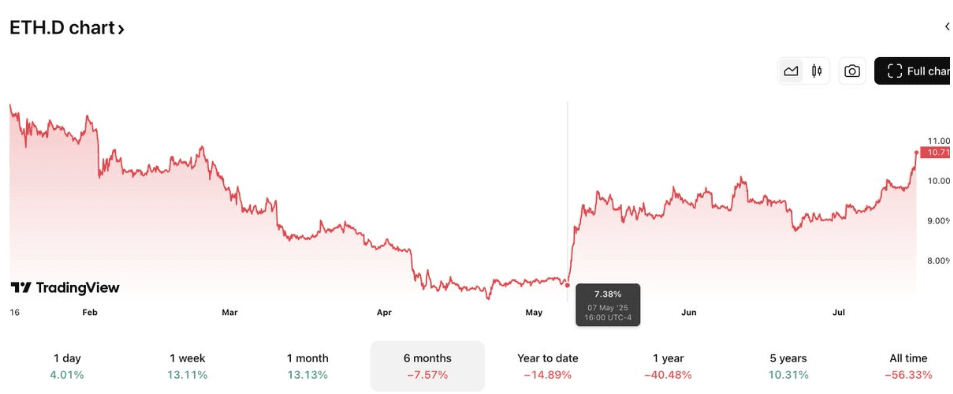

As of this year, $SOLETH has fallen nearly 9%. Ethereum's market dominance hit a low in May and has since established the longest upward trend since mid-2023.

If the entire crypto Twitter (CT) has labeled $ETH as the 'cursed currency,' why does it still perform excellently?

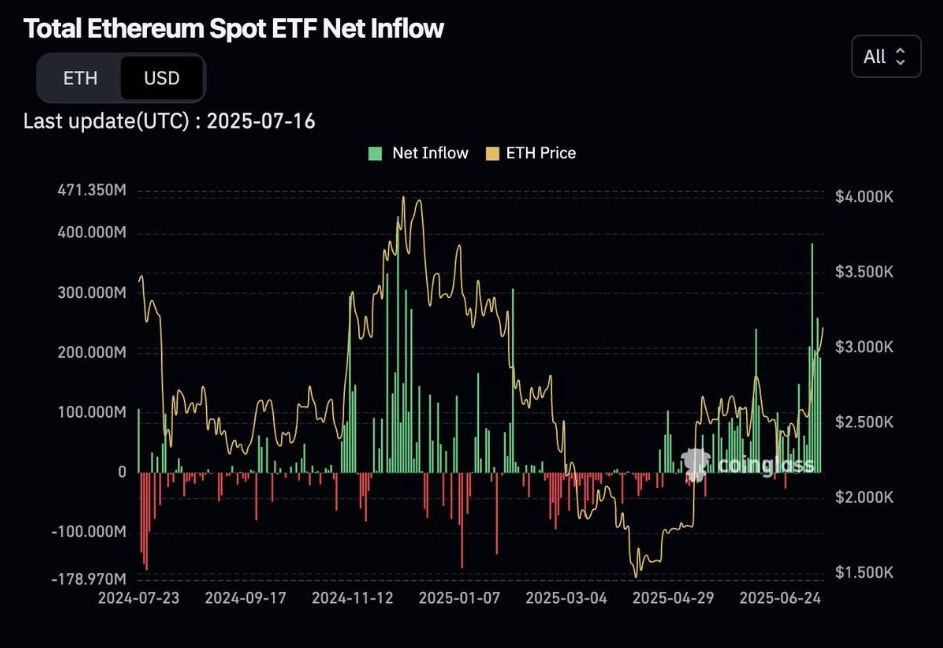

The answer is: it is attracting new buyers.

Since March of this year, spot ETF inflows have shown a one-way growth trend.

Microstrategy Clone funds similar to $ETH are aggressively increasing their positions, adding early structural leverage to the market.

Perhaps some crypto natives realize they have insufficient exposure to $ETH and start to reposition, possibly exiting their positions in $BTC and $SOL, which have performed well over the past two years, and instead allocating to Ethereum.

I’m not saying that Ethereum has solved its existing problems. I think what might happen at this stage is that $ETH as an asset begins to decouple from the Ethereum network itself.

External buyers are driving a paradigm shift for $ETH assets, challenging our inherent perception that it 'can only go down.' Shorts will eventually be forced to cover. Then, crypto native capital will start chasing the upward trend until a certain broad speculative frenzy for $ETH occurs and ends with a spectacular top.

If all of this really happens, then a new historical high (ATH) won’t be far off.

#特朗普施压鲍威尔 #比特币巨鲸动向 #以太坊连续两日领涨

$BTC