Original text: Mason Nystrom, Investor at Pantera Capital

Translation: Zen, PANews

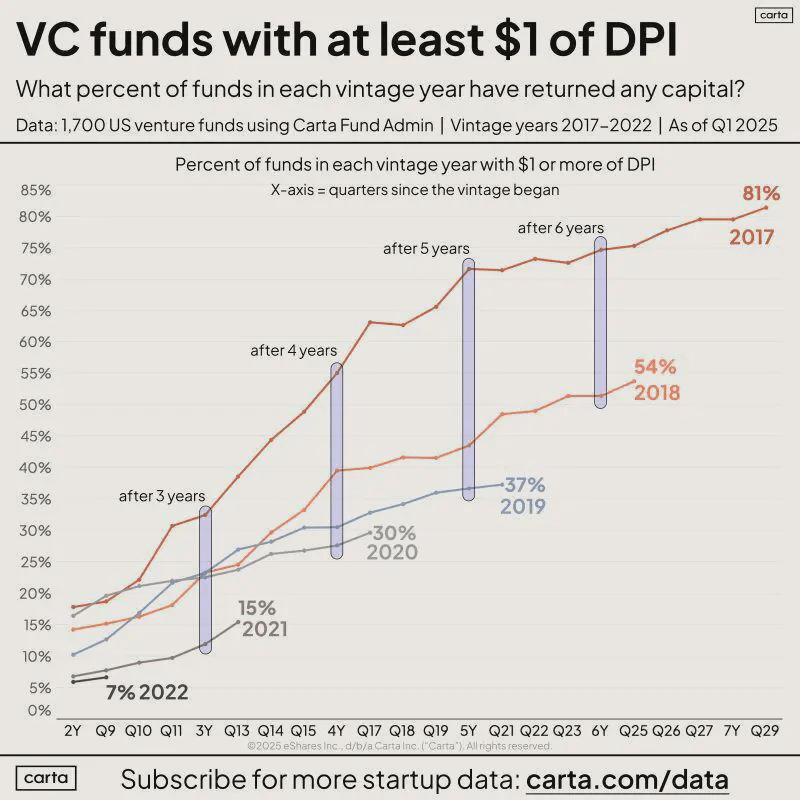

Today, financing has become difficult due to challenges faced by upstream DPI (Distributed Portfolio Index) and LP (Limited Partners) funding.

In the broader venture capital field, funds from different periods have returned less capital to LPs than in the past. This, in turn, has led to a shrinkage of available 'dry powder' for existing and newly established VCs to invest, thus exacerbating the financing difficulties for founders.

What does this mean for crypto venture capital?

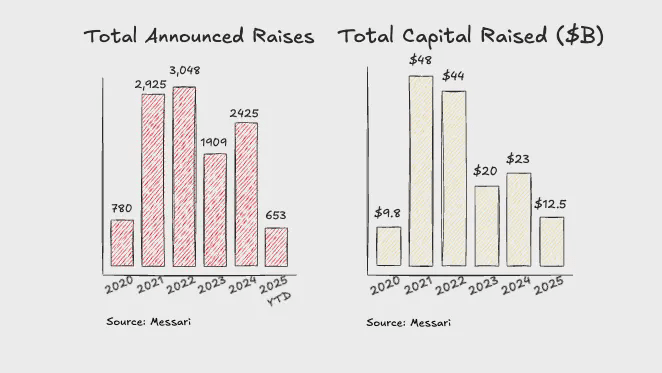

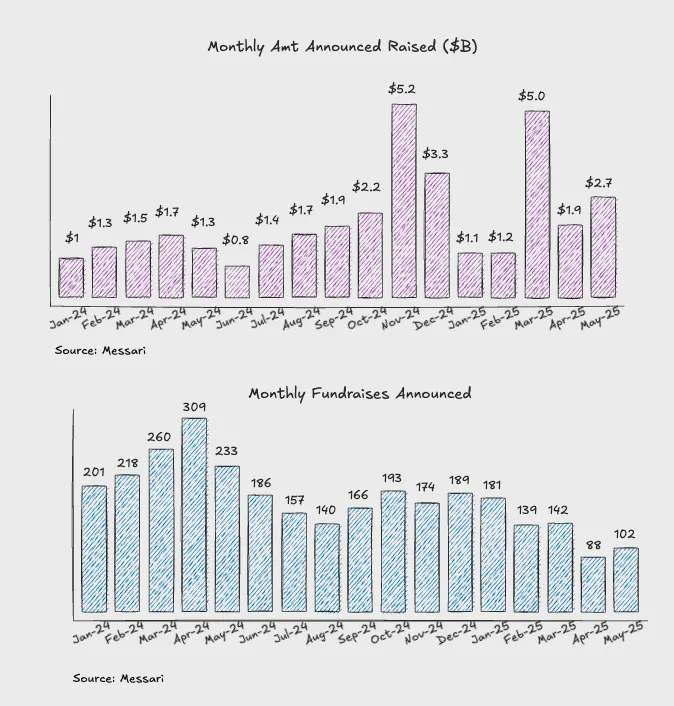

The number of transactions is expected to slow down in 2025, but the pace of capital deployment will remain the same as in 2024. The decrease in the number of transactions may be related to many VC funds nearing the end of their lifecycle and the reduction of available 'dry powder'. However, some large funds are still completing significant transactions, so the pace of capital deployment remains consistent with the past two years.

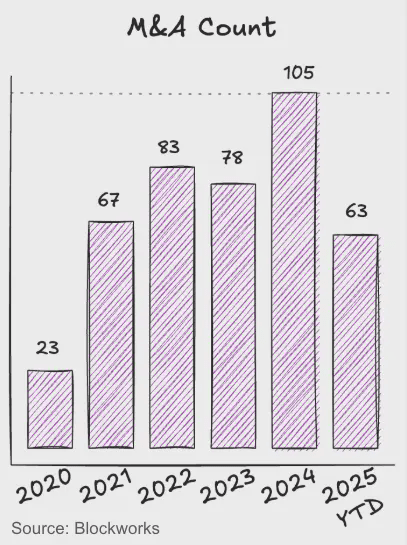

In the past two years, M&A activities in the crypto space have continued to improve, benefiting liquidity and exit opportunities. Recent large M&A cases, including NinjaTrader, Privy, Bridge, Deribit, and HiddenRoad, provide more assurance for industry consolidation and crypto equity VC exits.

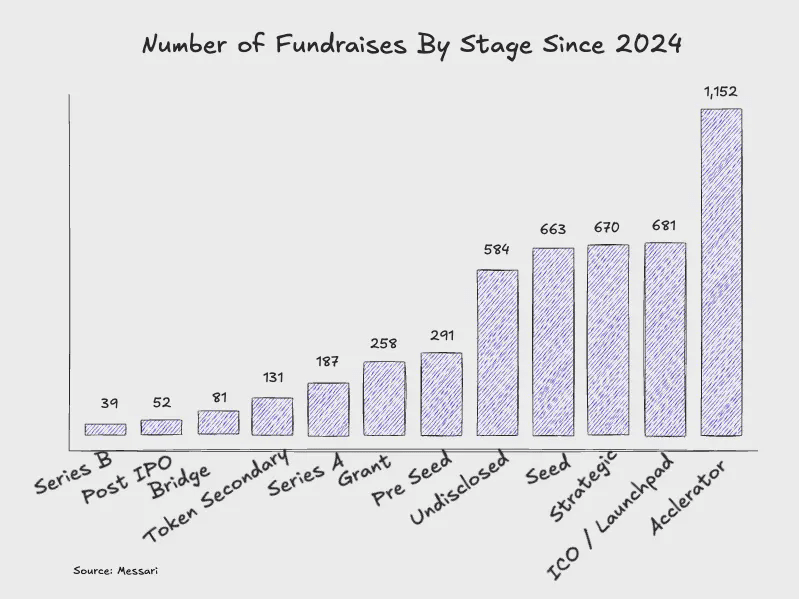

In the past year, the overall number of transactions has remained stable, with some larger late-stage transactions announced for completion in Q4 2024 and Q1 2025. This is mainly due to more transactions being concentrated in the pre-seed, seed, and accelerator stages, where capital has remained relatively abundant.

By financing stage, accelerators and startup platforms lead in the number of transactions. Since 2024, a large number of accelerators and startup platforms have emerged, which may reflect a tightening financing environment, where founders prefer to issue tokens early to launch projects.

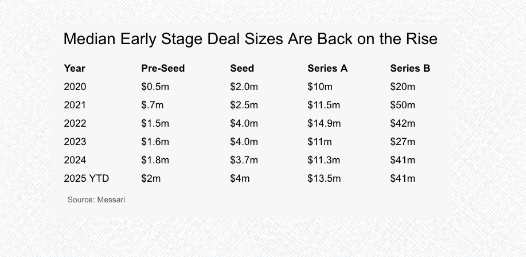

The median size of early financing rounds has rebounded. The scale of pre-seed financing has continued to grow year-on-year, indicating that funding in the earliest stages remains ample. The median financing for seed rounds, Series A, and Series B has approached or rebounded to 2022 levels.

Crypto VC Prediction One: Tokens will become the primary investment mechanism.

The market will shift from a 'token + equity' dual structure to a 'single asset carrying value' model. One asset, one set of value accumulation logic.

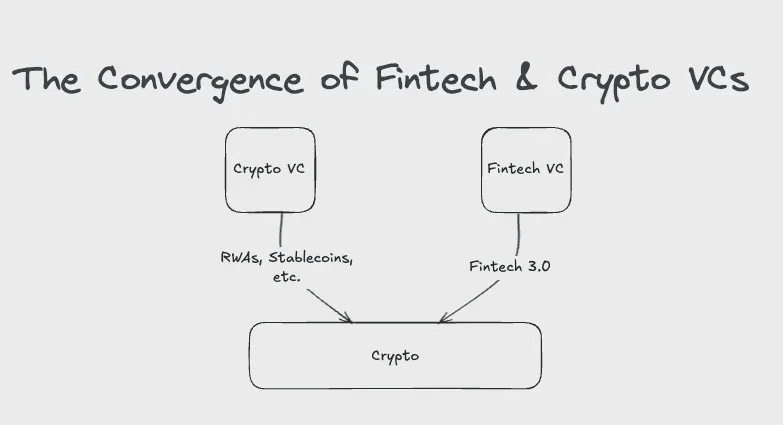

Crypto VC Prediction Two: The Accelerating Integration of Fintech VC and Crypto VC.

Every fintech investor is becoming a crypto investor, focusing on the next generation of payment networks, new digital banks, and blockchain-based asset tokenization platforms. Crypto VCs face competitive pressure, and those that haven't positioned themselves in the stablecoin/payment sector will struggle to compete with fintech VCs that have rich payment experience.

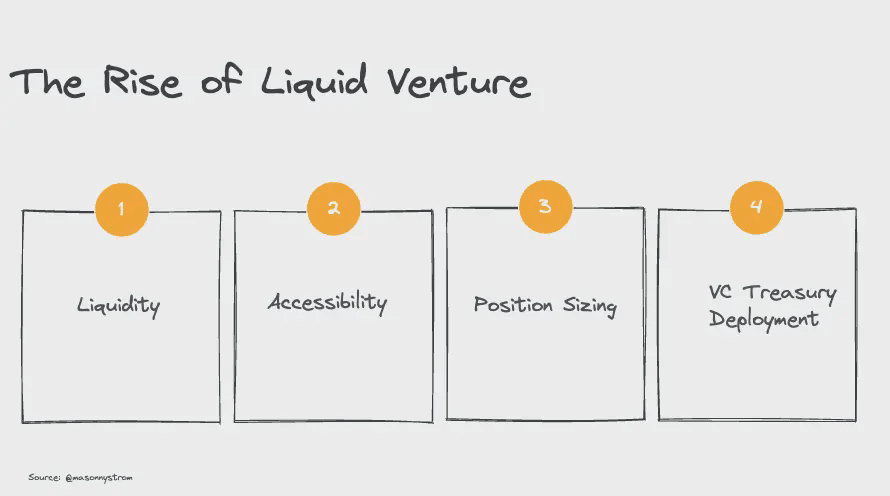

Crypto VC Prediction Three: The Rise of 'Liquidity Venture'.

"Liquidity Venture" seeks venture-like opportunities in the circulating token market:

Liquidity - publicly traded assets/tokens have higher liquidity, meaning faster exit paths.

Accessibility - private VC investments have high thresholds, while liquidity ventures allow investors to purchase tokens directly without needing to 'snatch projects', and can also trade over-the-counter (OTC).

Position management - companies issuing tokens early allow small funds to establish meaningful positions, while large funds can invest in high market cap circulating tokens.

Capital operation - the best-performing crypto VC funds typically allocate reserve assets in mainstream tokens like BTC and ETH, achieving excess returns. I personally expect that during bear market cycles, VC funds will more often draw on funds in advance and invest in quality tokens.

The crypto space will continue to be at the forefront of venture capital. The integration of public and private capital markets is a development trend in venture capital, with more traditional VC funds choosing to place bets in liquid markets (such as post-IPO holding tools) or secondary equity markets, while the crypto space has long been on this path. Crypto continues to lead in innovation in capital markets. As more assets are on-chain, more companies will choose 'on-chain first' financing methods.

Finally, the results in the crypto market often exhibit a more 'power-law distribution' than traditional venture capital - top crypto assets are not only competing to become digital sovereign currencies but also to serve as the foundational layer of the new financial economy. Although the return distribution is more extreme, this is precisely why crypto VC will continue to attract a significant inflow of capital in pursuit of asymmetric returns.