Author: Zuo Ye, Crooked Neck Mountain

Secret to getting rich = Innovative asset type + Enhanced capital efficiency

$PUMP's issuance stirred up the atmosphere, and amidst the noise turning to silence, the biggest beneficiary has emerged: MemeCore. Its token $M not only topped the CT hot list but also successfully secured Binance Alpha, followed closely by Bonk targeting Chinese region users.

The English project parties speaking Chinese reminds me of the era of SBF, when the world was still unified.

Image description: Bonkfun speaks Chinese

Image source: @SolportTom

But don’t be nervous; today is not about analyzing the price trends of PUMP, but about discussing why Meme platforms issue tokens, and why even after the end of the large Meme cycle, issuing tokens can still create waves.

Earn the last penny

PumpFun's issuance maximizes its value as a Meme platform.

A normal Meme platform should have died when CZ announced the end upon entering with FourMeme. Please note, I am referring to the end of Meme platforms as a consensus across the entire industry, as mainstream asset issuance platforms. If we talk about Meme itself, we should trace back to the emergence of $TRUMP in January.

Previous review: Meme comes from the sea and goes back to the sea.

The subsequent breakup between PumpFun and Raydium shows clear evidence of consensus split: you build the AMM pool, I build the Meme launchpad.

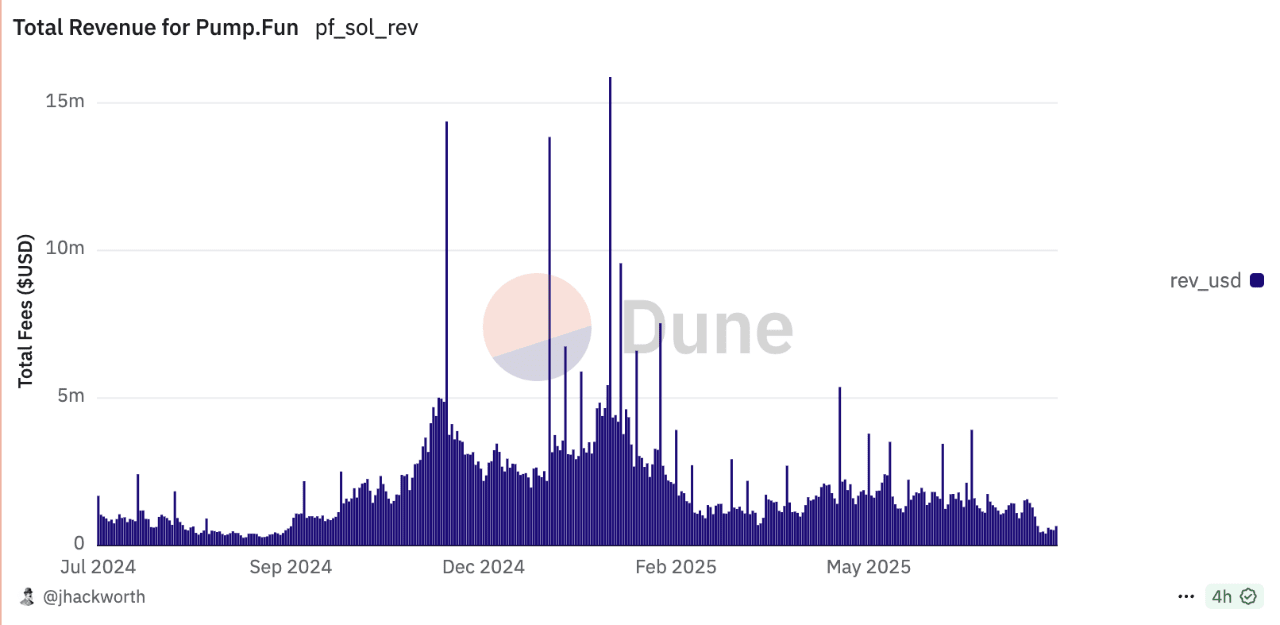

Image description: PumpFun profit trend

Image source: @jphackworth42

It is increasingly strange how, not only has the Pump Fun platform token become the focus in the past six months, but it can also attract many similar ones like Bonk and $M to share liquidity. Referring to DePIN, NFT, BTCFi, and the L2 track, basically, none can maintain the explosive traffic they had during the initial narrative's end.

A more normal rhythm is to directly issue tokens to drain market liquidity at the peak of industry consensus.

• For example, the 'positive case' of NFT is Blur, while the negative case is OpenSea.

• DePIN's Filecoin, Helium (Mobile), and the negative is Starpower.

• BTCFi's Babylon and a bunch of BTC L2s are the negatives.

However, the normal liquidity of Meme has been absorbed by $TRUMP. Theoretically, the emergence of FourMeme should have been the death knell for PumpFun, but the PUMP token can still stir the winds.

PumpFun has provided the perfect exit strategy for a dying track, earning the last penny accumulated from the market.

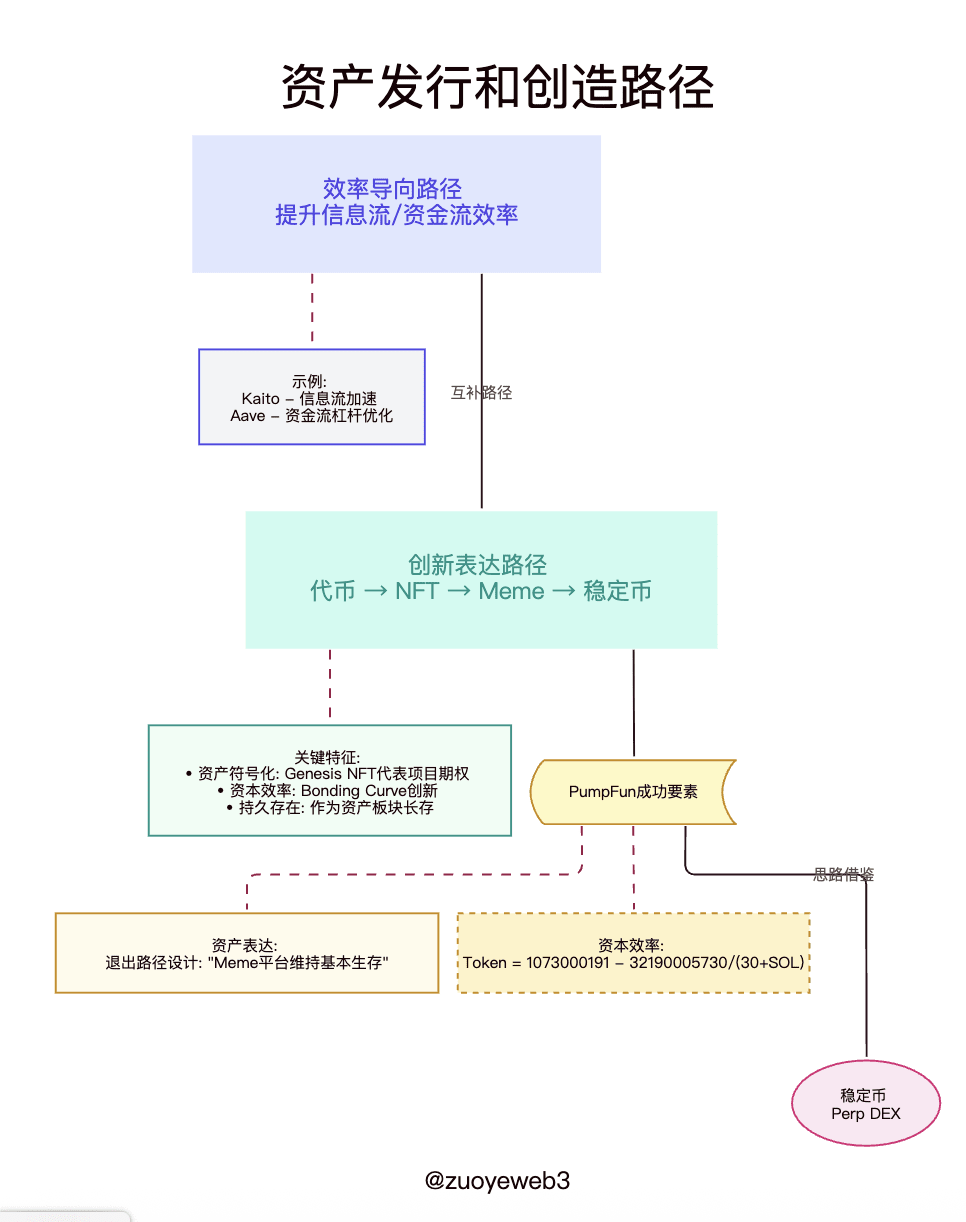

The creation and expression of crypto assets can be efficiency-oriented, allowing information flow (Kaito) or capital flow (Aave) to move faster and with higher leverage, or it can be innovative expressions, evolving along the lines of token—NFT—Meme—stablecoin.

If we are to answer how PumpFun achieved this, we should first review the successes and failures of NFTs. Unlike the paths of inscriptions and BTCFi, which were ultimately debunked, NFTs have found their place in the realm of project parties.

Genesis NFTs represent options for projects, or even a kind of Coinlist equivalent, depending on how the project party designs them. As fashionable symbols and tickets, NFTs have failed, while asset symbols have succeeded.

The trend of NFTs will certainly not return. My understanding is that Meme, as an asset sector, will endure.

Just like the season of clones will not return, it does not prevent everyone from continuing to produce clones and earn Alpha points.

Meme is the same. People's valuation systems will change. PumpFun will not be Binance, nor will it be Hyperliquid, but isn't Uniswap still alive?

Between complete failure and moving towards success, there is also the choice of safely landing. Right or wrong, let the world judge.

The next feasible scenario

Previously, the crypto industry believed that landing meant moving towards mass adoption.

Now, the crypto industry believes that landing means completing the final issuance action.

Image description: Asset issuance and creation path

Image source: @zuoyeweb3

Not everyone will be enchanted by Meme, but as long as someone is willing to participate, then as an asset type and launch platform, it can maintain basic survival. There must always be a place for people to buy on-chain Maotai and virtual $LABUBU.

From blue-chip NFTs to Genesis NFTs, from $TRUMP to $PUMP, an era has come to an end. In the small cycle of crypto, Meme lasted for 6 months, which is longer than many 2-3 month technical narratives.

The only mystery left is the unsolved riddle of the Bonding Curve. We know that the x*y=k of AMM DEX exists, but we still do not know how the specific parameters of the Bonding Curve are derived.

A fun fact: FriendTech also uses Bonding Curve. Earlier, in the 2020 DeFi Summer, it was actually a three-way kill between AMM, order book, and Bonding Curve. Only Uniswap took AMM, dYdX took the order book, and Bonding Curve only shone when it met PumpFun.

Another secret left by PumpFun is that the Bonding Curve enhances capital efficiency. Meme has never been a simple new type of asset; PumpFun's capital efficiency orientation as a platform is also the key to product design success.

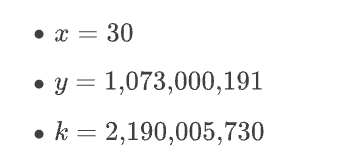

Referring to @CuntouErjiu's algorithm, Pump Fun's algorithm is a super modification of x*y=k, Bonding Curve equation:

Quantity quantity

The parameter values are:

Other Meme launch platforms can reverse-engineer and reference PumpFun's specific parameters, but how this formula itself is derived has almost become an unsolved mystery in the crypto circle. It's like AI large models; open-source code has no meaning; only open-source training methods and datasets are truly open-source.

Unfortunately, no one has truly reverse-engineered PumpFun's original formula to this day. Based on this, the moat of PumpFun in enhancing capital (Meme) efficiency remains solid. Even if Meme is no longer popular, the residual traffic can still serve as the value foundation for $PUMP.

In this regard, PumpFun is much more reliable than many ghost chains. The exit of USDT from Algorand/EOS indicates that what is forgotten is not Meme.

However, it must be acknowledged that the era of Meme as a representative is completely over. It was once glorious, but now it is difficult to maintain. Only BTC and ETH have been able to remain strong, and SOL still needs to go through numerous tests to enter the market.

At least SOL is not recognized by PumpFun, and all earned SOL is exchanged into U-based capital. EOS, however, has held onto the raised BTC until now. Which category does the Ethereum Foundation selling ETH belong to?

Conclusion

Currently, the hot topics are RWA and stablecoins. It is meaningless to keep an eye on PumpFun, but PumpFun will perform better than FriendTech and Blur, and Meme will outperform NFT and BTCFi. PumpFun's approach is worth learning from.

Start with the end in mind. The founder must design an exit path from the very beginning, not merely issue tokens, but also answer whether, on the grand stage of crypto, after the explosive breakout, there can still be a suitable position found backstage.

I can predict that Perp DEX will also be like this, as we find it hard to discover the off-chain matching algorithm of the order book.

Similarly, there are

1. Routing algorithm of DEX aggregator

2. Trading matching algorithm of dark pool DEX

3. On-chain options product liquidity 'detonation' algorithm

Especially on-chain options, which are currently facing the same dilemma as Meme trading in the previous PumpFun era, with liquidity being too low. The common LP Token subsidy model used by DEX does not seem to be effective.

To add a word, the on-chain options product model also needs to be reinvented, either as an original crypto product like Meme or as a reconstruction of perpetual contracts in the crypto circle. Perhaps VIX is a good idea?