———————————————————

"Native" innovation refers to things that did not exist before and could only emerge under new technological paradigms. In the Web3 world, we have been asking: what is truly 'native' to blockchain and crypto technology?

Fred Wilson provided a classic framework in a 2009 article:

"Native" refers to opportunities that could not exist before and only arise when new platforms emerge. For instance, pushing news to a mobile phone is not called "native" because startups find it hard to do better than CNN in creating a "CNN on mobile."

This idea is sharp: true 'native' innovation will only emerge when a new interface fundamentally changes the way we interact with the system. Applied to Web3, I believe stablecoins (especially in payments and banking) are one of the most 'native' innovations in the crypto world. Interface transformation brings aggregation opportunities; every transformation in finance begins with a new user interface.

These interfaces will experience friction in the early stages, but they will also bring 'aggregation' opportunities by redefining the initiation, verification, and settlement of value.

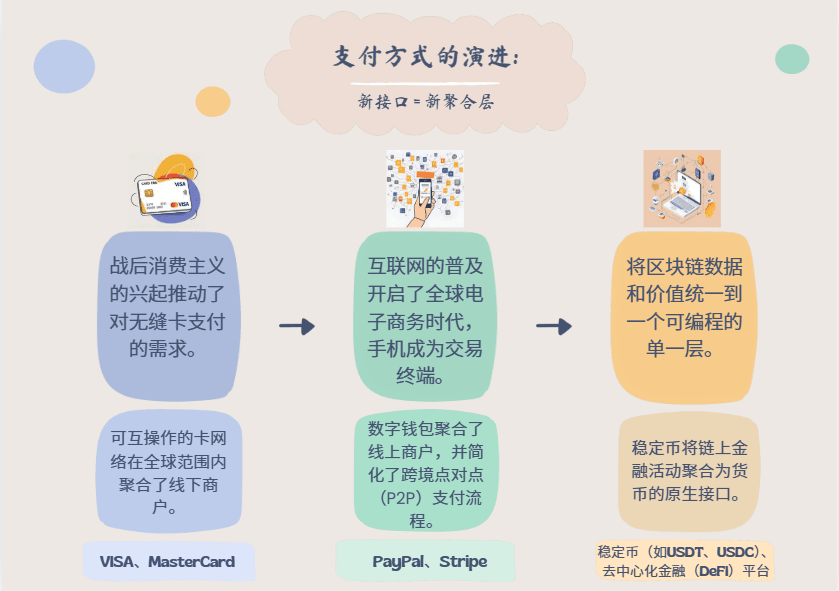

🔹 Card Era: Credit cards replace cash, becoming the new payment interface.

🔹 Digital Age: Digital wallets (like PayPal) have become the payment interface for e-commerce.

🔹 Web3 Era: Stablecoins are becoming the new interface for 'banking.'

1) Card Era 🔻

The birth of Visa and the global network. After World War II, the US economy took off, and consumer demand skyrocketed. Consumers wanted smoother payment methods, leading to the emergence of credit cards. In 1950, Diners Club pioneered this, followed by Amex and MasterCard.

However, early credit card systems were fragmented. A card from one bank might not work on another merchant's network, lacking true interoperability.

In 1958, Bank of America launched BankAmericard, connecting banks and merchants through an authorization mechanism, creating a scalable system. By 1976, it transformed into Visa, a global network that aggregated fragmented payments.

2) Digital Age 🔻

PayPal and the interface of online commerce. In the late 1990s, the rise of eBay drove cross-border and P2P trade. However, payment systems lagged: buyers didn't want to share credit card information directly and faced the hassle of foreign exchange and remittances.

PayPal seized the opportunity, reducing payment friction through email-based transfers and quick account openings, embedding itself in the internet-native economic system, becoming the dominant player in online payments.

3) Web3 Era 🔻

Stablecoins serve as the interface for value flow. So, what is 'native' in Web3? In this world, data is money, and money is data.

Traditional financial systems separate information and value: SWIFT is only responsible for sending payment instructions, while actual settlements go through complex banking networks, which are time-consuming, costly, and opaque.

Blockchain integrates information and value, allowing value to flow like information. This opens a programmable, composable financial design space:

🔹 Trustless: Each transaction can be verified on-chain.

🔹 Permissionless: Anyone can develop and use financial services.

🔹 Interoperability: Assets can flow freely between different protocols and chains.

Stablecoins are the core of this system. They have become the native interface for depositing, earning, borrowing, and spending in the crypto economy, effectively acting as a new type of 'bank interface.'

📍 From Interface to Network: Stablecoins are becoming the new liquidity layer.

Just as credit cards were fragmented before Visa appeared, today's stablecoins are also operated by different issuers with different strategies and backgrounds, resulting in fragmentation. But they are all competing to become the default liquidity layer in the crypto financial system.

Major players have already started taking action:

1️⃣ Ripple spends $1.25 billion to acquire Hidden Road, pushing RLUSD into the institutional market.

2️⃣ Circle launches the B2B-focused Circle Payments Network, concentrating on settlements.

3️⃣ MasterCard collaborates with OKX to create an end-to-end stablecoin payment channel.

4️⃣ Visa collaborates with Bridge to support stablecoin digital cards.

5️⃣ Stripe launches stablecoin-native accounts, serving global developers.

No one wants to miss the next 'Visa'-like aggregation opportunity.

📍 Narrow Banking and Deposit Flight

The US Senate passed the (Genius Act), paving the way for traditional financial institutions to issue stablecoins. This will attract more banks into the stablecoin space in the short term, but in the long run, it may lead to deposit flight from traditional banks.

If users can deposit, earn, borrow, and spend money directly on-chain, with assets settling instantly and generating yield, why would they still store money in traditional banks?

In the future, traditional banks may become 'narrow banks'—only serving as a 'on- and off-ramp' between fiat and cryptocurrencies. For example, @fraxfinance is developing frxUSD, attempting to become a universal, cross-chain stablecoin base layer.

Just as PayPal once seized transaction volume from payment processors, stablecoins may begin to siphon deposits from banks. Future banks may adopt a 'narrow bank' model: only responsible for custody and channel operations, while credit creation shifts elsewhere.

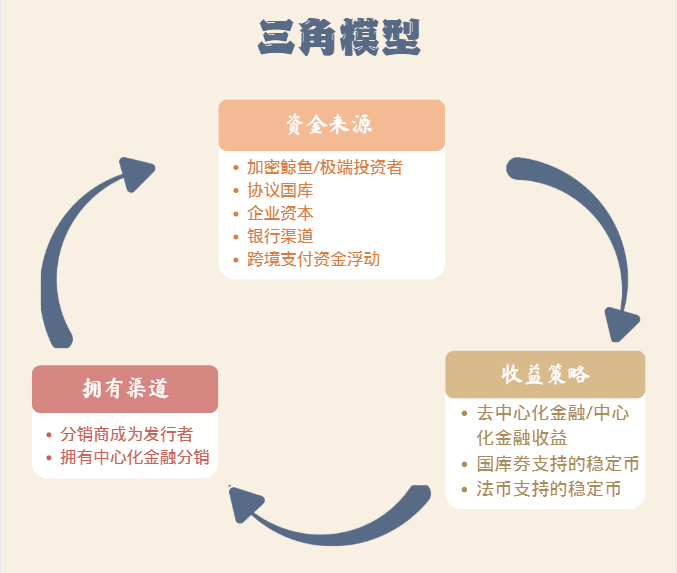

📍 The Golden Triangle of Stablecoins

Stablecoins are evolving from trading tools to the native interface for depositing, earning, borrowing, and spending in the crypto economy, gradually becoming a new type of digital liquidity layer—programmable, composable, and globally usable currency.

But to become the default 'money' layer, it's not just a matter of trust or speed. Stablecoins need to solve three key challenges, which traditional banks have addressed through infrastructure, regulation, and scale. In the crypto world, this is known as the golden triangle of stablecoin strategy:

🔹 Acquire Supply: Where does the liquidity for stablecoins come from? Can it quickly and reliably tap into large amounts of idle capital?

🔹 Control Channels: How will stablecoins be utilized? Can you control key distribution points, such as exchanges, brokers, or Web2 scenarios?

🔹 Design Yield: Can you create scalable, compliant yield strategies that meet the needs of users, partners, and regulators?

Most stablecoin projects can only excel at one, a few can manage two. The real winners are those projects that can effectively handle all three.

————————————————————

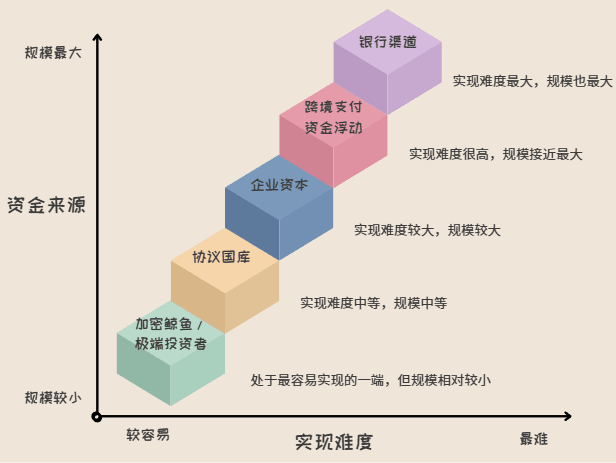

1. Acquire Supply: The race to seize idle capital 🔻

The winners in the stablecoin space are those who unlock the 'trapped dollars' first. Liquidity is not infinite; this is a race of speed—whoever can quickly siphon funds from the largest, most underutilized capital pools will win. Here are several directions in the race, from simple to complex, from small to large:

1️⃣ Crypto whales/players: This is the fastest-moving source of funds. For example, @ethena. Starting with crypto whales, players, and leveraged traders on exchanges and DeFi.

2️⃣ Protocol Vault: Large scale, strong stickiness. For example, @buidlfi's $280 million TVL comes from only 69 wallets, with the top two major contributors being @ethena_labs and @SkyEcosystem. Stablecoins are becoming reserve assets for crypto-native institutions.

3️⃣ Corporate Funds: From RWA projects to regional fintech companies, everyone is chasing corporate treasuries and cross-border remittance networks. For example, @USDX has made early progress in this area.

4️⃣ Cross-border payment floating funds: Stablecoins have become the second-largest payment channel globally. The 'trapped' liquidity in the crypto interoperable settlement layer is a natural source of funds. Watch @codex.

5️⃣ Banking Channel: After the (Genius Act), banks can directly participate in stablecoin infrastructure. @fraxfinance

Is among the first players to enter this space.

————————————————————

2. Control Channels: Distribution determines fate 🔻

Distribution is the moat. Whoever can control the last mile of user experience—wallets, exchanges, brokers, or merchant networks—can lock in usage and defense. Currently, there are two major strategies:

——Distribution parties become issuers:

🔹 @PayPal launches $PYUSD, directly monetizing its own payment ecosystem.

🔹 @stripe launches stablecoin accounts supporting USDB issued by Bridge.

🔹 @CumberlandSays's @Hashnote_Labs launches USYC, a yield-bearing stablecoin backed by US Treasuries.

🔹 JPMorgan, Bank of America, Citibank, and Wells Fargo are also exploring joint issuance of stablecoins.

——Control centralized finance distribution:

🔹 @coinbase is a key distribution engine for @circle's USDC.

🔹 @Binance replaces $BUSD with $FDUSD as the internal settlement token.

🔹 @ethena_labs promotes USDe quickly by integrating with @Bybit_Official.

🔹 @Ripple acquires Hidden Road, deepening its institutional brokerage network.

————————————————————

3. Yield Strategy: Designing the yield curve for stablecoins 🔻

In addition to trust and liquidity, stablecoins also need to compete on yield. However, yield design has a classic trade-off: high returns limit scalability.

Current yield strategies fall into three major categories: DeFi/CeFi yield-bearing stablecoins:

1️⃣ Attract funds through high yields, but risk management and regulation are complex. For example:

——Ethena: Starting from a delta-neutral strategy and expanding into asset management and payment solutions.

——Perena: A 'stable bank' on Solana, collaborating with external vaults to diversify yield sources.

——CAP: Creating yield for stablecoin holders through restaking and Franklin Templeton's asset management.

——Resolv: Expanding from delta-neutral to multiple crypto yields, isolating risks with RLP tokens.

——Falcon: A synthetic dollar protocol supported by DWF Labs, using a reverse delta-neutral strategy.

——StableLabs: USDX maintains delta-neutral dollar positions through multi-currency arbitrage.

2️⃣ Treasury-type stablecoins: Moderate yield, institutional-level structure. Ondo and Hashnote tokenize US Treasury bonds through money market funds (MMF), balancing compliance and composability.

3️⃣ Fiat-backed stablecoins: No yield, maximum scale. USDC, USDT, FDUSD, PYUSD occupy distribution advantages through exchanges and payment channels, earning from off-chain floating funds with minimal incentives for users.

📍 Summary:

Stablecoins are reshaping the monetary system just as Visa abstracted the relationship between merchants and banks into a universal settlement layer. Stablecoins now abstract the bank's deposit layer into an open API. This fundamentally changes the interface of the banking industry. Within this interface transformation lies opportunity: to use stablecoins as a core operating system to rebuild the monetary system from scratch.

Winners will be those players who can simultaneously manage supply, channels, and yield. They will define what 'money' is in Web3.

🔹 Original article translation link: https://x.com/YettaSing/status/1942238646754738676?t=_jKbJyi0R1IoTynVLQzD8A&s=19