Geopolitics has once again become a market focus. Israel attacked Iranian facilities, which was followed by Iran's retaliation, leading to a spike in oil prices and weakening market risk sentiment last Friday. The market is worried about the risks of escalating conflict, particularly regarding Iran potentially blocking the Strait of Hormuz and possible U.S. intervention, which will affect oil prices during the peak driving season in the U.S.

Meanwhile, the rise in oil prices has reached a two-year downward trend line. If a more convincing upward breakout occurs, it may not be favorable for overall risk sentiment in the short term. However, the market generally believes that the impact of energy supply disruptions should be limited, such as the increase in production from Saudi Arabia and other supplementary sources, but the most sustainable path still relies on resolving issues through diplomatic means.

Notably, in this round of conflict, there has not been a significant 'flight-to-quality' buying in dollars and U.S. Treasuries, indicating that global investors' concerns about U.S. capital flows are still greater than their concern over the Middle East situation, which should not be overlooked.

Interest rate volatility has also fallen close to multi-year lows, indicating that the macro market is more inclined to shift its focus back to tariffs and economic fundamentals.

In fact, this round of conflict has had little impact on market expectations for interest rate cuts in 2025. Currently, the market still expects only two rate cuts by the end of the year, even though inflation data has repeatedly come in below market expectations.

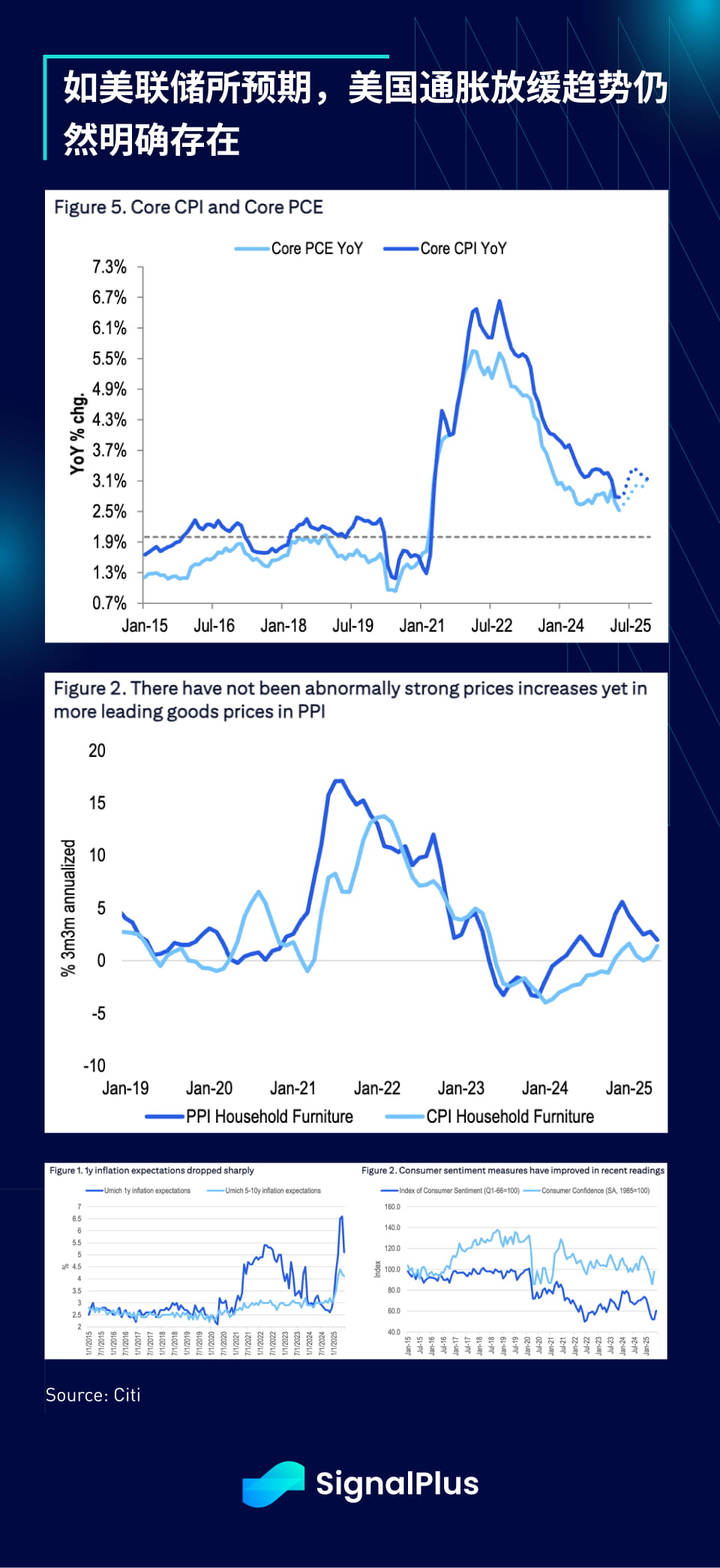

Before last Friday's fluctuations, the market was celebrating lower-than-expected inflation data across multiple developed markets (excluding Japan), where U.S. CPI, PPI, New York Fed inflation expectations, and Michigan inflation expectations were all below expectations.

In fact, the recent core CPI being significantly lower than expected has helped boost risk sentiment and provides the Federal Reserve with more room to maintain an accommodative financial environment.

Equity long-short hedge funds have resumed increasing their long positions in stocks, with net exposure rising to a one-year high. In the short term, the path of least resistance for the market remains upward.

Cryptocurrencies have once again validated their positioning as 'high-risk assets', with prices of various tokens falling sharply last week. On Friday, cryptocurrency prices fell with the stock market, resulting in the liquidation of over $1.2 billion in futures positions. The drop on Friday was mainly driven by altcoins, while BTC returned to around $105k, supported by stable ETF capital flows and holdings from listed companies.

Net inflows into BTC ETFs have reached $1.4 billion, while ETH ETFs have just broken the record for more than two consecutive weeks of net buying, indicating that participation from TradFi remains strong. We expect prices to continue to follow stock market sentiment and gradually rise as we enter the summer.

This week will see multiple central bank meetings (including the Federal Reserve, the Bank of Japan, the Bank of England, the Norges Bank, and the Swiss National Bank), but we believe the substantive impact will be limited. From the Federal Reserve's perspective, there may be some slight dovish signals, and the market will focus on whether it will use the recent series of lower-than-expected inflation data and weak unemployment claims data as a basis for further dovish shifts. We do not expect any significant policy actions; the recent market focus will remain on the developments between Israel and Iran, especially any substantial military escalation or dangerous political moves. Meanwhile, the U.S. remains mired in a deadlock over tariffs and budget negotiations. Wishing everyone successful trading this week!