Source: IgniteRatings, X

Moody’s Ratings (Moody’s) has downgraded the Government of United States of America’s (US) long-term issuer and senior unsecured ratings to Aa1 from Aaa and changed the outlook to stable from negative.

This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns.

— — Moody’s, May 16, 2025

Moody’s downgrade of the US long-term credit rating marks the last major credit agency hold-out to have removed US debt from a vaunted ‘AAA’ status. The announcement came hours after Friday’s market close, and might have played a hand in pushing the House Budget Committee to advance their “One, Big, Beautiful Bill” in unusual hours on Sunday night to minimize market fallout.

Ignoring all the political charade around spending measures, does a credit rating still matter? Readers might recall that the collapsed Silicon Valley Bank was given a solid ‘A’ rating into its final hours, and more seasoned readers might remember the comical ratings assigned to CDOs, CMOs, subprime mortgages, and China property bonds to draw their own conclusions.

But let’s cover some of the relevant points this week in a FAQ format.

When were there previous ratings downgrades?

S&P in Jul 2011, Fitch in August 2023.

Are there immediate, technical consequences?

For ‘ratings based’ holders who cannot hold non AAA debt

They’ll change the rules (as they have), given the scale and irreplaceability of US debt as an asset class.

Impact on centralized asset clearing

DTCC and CME treat treasury collateral using maturity and security based haircuts, with less dependency on ratings.

Impact on money market funds

Short-term maturity profiles dilute the impact of credit ratings; treasury bills demand has barely blinked despite the prior rating downgrades and even debt ceiling shenanigans.

Long-term treasury reserve status

Realistically, President Trump’s tariff policies and the global trade reset have had exponentially more impact on global treasury demand than any rating agencies could do.

What happened to markets previously?

2011 was a bit of more of a shock as it was the first downgrade and came in the first iterations of the debt ceiling ‘crisis’, which we have now normalized as political theatre.

Equities fell ~20% in Jul-Aug and treasury yields… fell 120bp (prices went UP) after the downgrade, due to risk-off hedging and the ongoing QE at the time. So much for that.

In 2023, the downgrade happened in August after the debt ceiling crisis in the early summer, and at a time when the treasury was withdrawing liquidity though the TGA rebuild (reserves) along higher treasury issuance. SPX fell ~10% and treasury yields went up about 50bp as a continued YTD trend move at the time. The downgrade might have accelerated their relative moves but didn’t appear to have been a game changer in and of itself.

Will the downgrade impact fiscal decision making?

The House Committee did advance their budget in an usual Sunday night vote, so there’s some effort made to mitigate the market fall out.

In terms of cutting USD spending and reigning in deficits? It might give more voice to the fiscal hawks but unlikely to change the longer-term trajectory of out-of-control spending and the ongoing concern on unsustainable treasury supply.

It will add to uncertainty over the timing / delay in the final passage of the bill, and dampening potential positive impacts of tax cuts given their negative budget impacts.

Market reaction this time around?

Equity reaction is likely negative as a knee-jerk, in light of the prior experience as well as the rapid run-up in prices over the past few weeks on very limited leadership (growth stocks, Mag-7 etc).

Less certain on bonds, depends on the extent of the equity risk-off, the subsequent political action from budget hawks vs Trump’s deal making, the ability to pass the Senate bill before debt ceiling deadline, and any contagion impact it might have on Trump’s 90-day tariff truce.

Net net, probably a risk negative on the whole on US equities, USTs, as well as the dollar.

How are markets positioned in macro?

Macro managers, systematic funds, and quant funds have all covered their shorts / underweight or have gone long.

Last week saw a mini ‘melt-up’ in buying activity as traders scrambled to cover shorts with NYSE stocks making a recent new highs in their Advance-Decline Line.

How was last week’s data?

Pretty bad for bonds.

Michigan sentiment showed a massive drop in outlook despite the recent tariff trade relief.

Headline was the lowest level since Jun 2022, and closest to the lowest levels since the 1980s.

Long-term inflation expectations came in at the highest levels since 1991 (4.6%).

One-year inflation reading came in at an astonishingly high reading of 7.3%, the highest since 1981.

Should markets worry about foreign selling?

Let’s take a look at what happened over the past few months.

In equities, non-US investors have already stopped buying US equity funds and have been net sellers of bond funds since March. This trend is likely to continue for the near future.

However, in terms of impact, bank data suggests that foreign investors hold a total of ~$57 trillion of USD assets in 2024, vs $2.2 trillion in 1990. ~$17 trillion of which are in equities, and $15 trillion in bonds.

Said in another way, foreigners hold ~20% of total US equity supply and 30% of US bond supply.

These are not small notionals that can be sold and de-risked in meaningful amounts without impacting the total capital markets structure.

Plus, ownership is scattered across various foreign holders, so any rash decisions from one will have complex game-theory implications on other holders.

For equities, key will remain earnings performance, which have been positive so far. JPM data suggests that SPX Q1 earnings have surprised by ~8% to the upside, with 70% of companies having reported, and 54% of companies beating revenues and 70% beating earnings estimates. Mag-7 earnings were also well ahead of the index at a blistering +28% EPS growth.

In terms of ownership, ignoring ambiguities out of ‘Carribean’ (ie. Cayman) entities for now, UK, Canada, and Japan are the top-3 holders of US assets globally, all of which should be expected to be close US allies. Chinese holdings is at a mere distant 4th at 4% vs ~8–9% for the upper group.

And judging from the past month, Japanese investors have been selling USTs but against big inflows into equities, mitigating fears of any significant ‘de-dollarisation’, and turned out to be more of an asset allocation move.

So in short, probably shouldn’t expect any huge de-coupling flows in the meantime… For now!

How about Crypto?

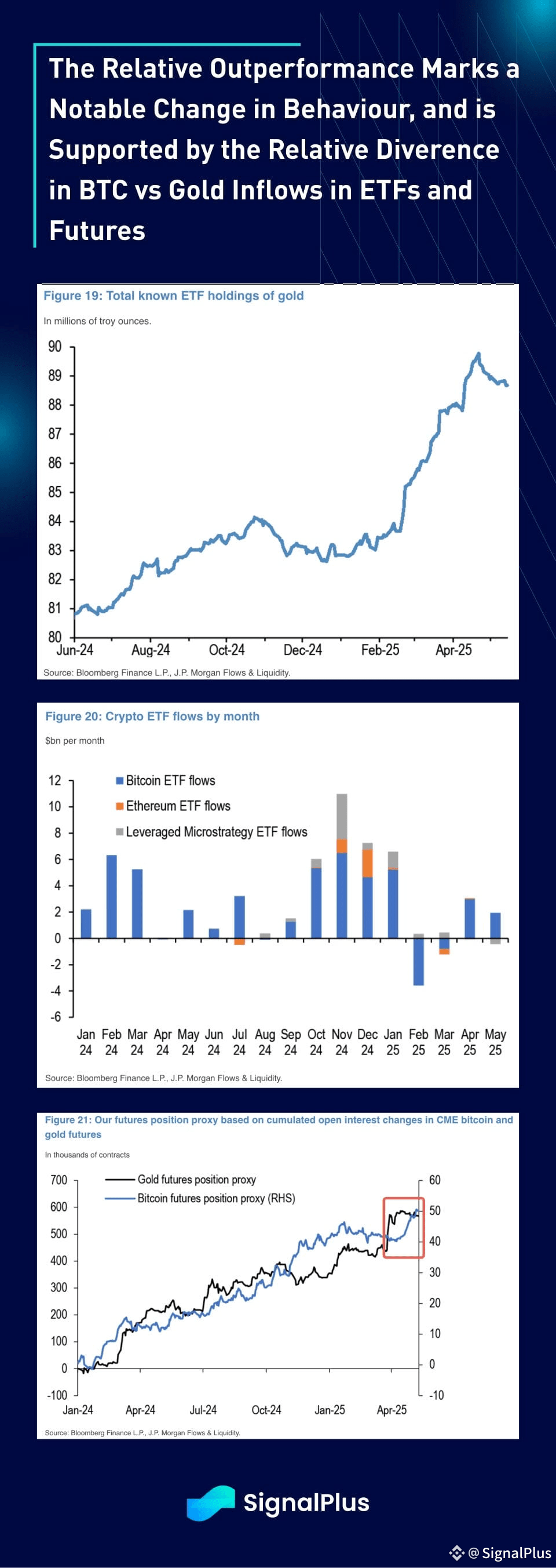

Interestingly, crypto prices have hung in throughout this move despite an ~7% sell off in gold prices from the peak.

Unlike in previous months where both BTC and gold went up in unison, Bitcoin has been rising against a drop in spot gold which is also reflected in ETF flows.

Gold ETFs saw a notable drop in flows against a small rise in BTC ETFs, with a similar pattern in gold vs BTC futures on CME.

In short, with macro markets stabilizing and the USD-debasement trade reflected across most asset classes, we should assume more of these micro-correlation breaks and relative value opportunities to take hold while we await the next major geo-political developments to materialize.

Good luck & good trading!