Over the past week, concerns about trade tensions further eased. Despite a mixed bag of economic data, the unexpectedly strong non-farm report has also cooled worries about economic slowdown. The unemployment rate remained at 4.2%, in line with market expectations.

U.S. stocks collectively rose, astonishingly recovering all losses since the announcement of reciprocal tariffs on Trump's 'Liberation Day' in early April within just two weeks.

Trump's administration has completed 100 days, triggering significant market volatility, with gold briefly becoming the biggest winner, while U.S. stocks, the dollar, and U.S. Treasuries performed at historic lows.

The U.S. added 177,000 jobs in April, exceeding the expected 130,000. Overall, this is a strong report, giving the Federal Reserve room to remain patient.

After the data release, market expectations for the Federal Reserve's rate cuts this year have cooled, with expectations now nearing four cuts. U.S. President Trump reiterated that tariffs will bring in billions of dollars in revenue, stating that we are just in a transition phase, and the Federal Reserve should lower interest rates.

Overall, signs of weakness in multiple areas such as consumption, employment, and manufacturing indicate that the U.S. economy will face greater challenges.

'Oracle of Omaha' Buffett announces he will step down as CEO by the end of the year, stating that 'tariffs are acts of war' and warns that the massive deficit will eventually backfire on the economy. Despite the market's violent fluctuations, he calmly stated that a halved stock price is a true opportunity.

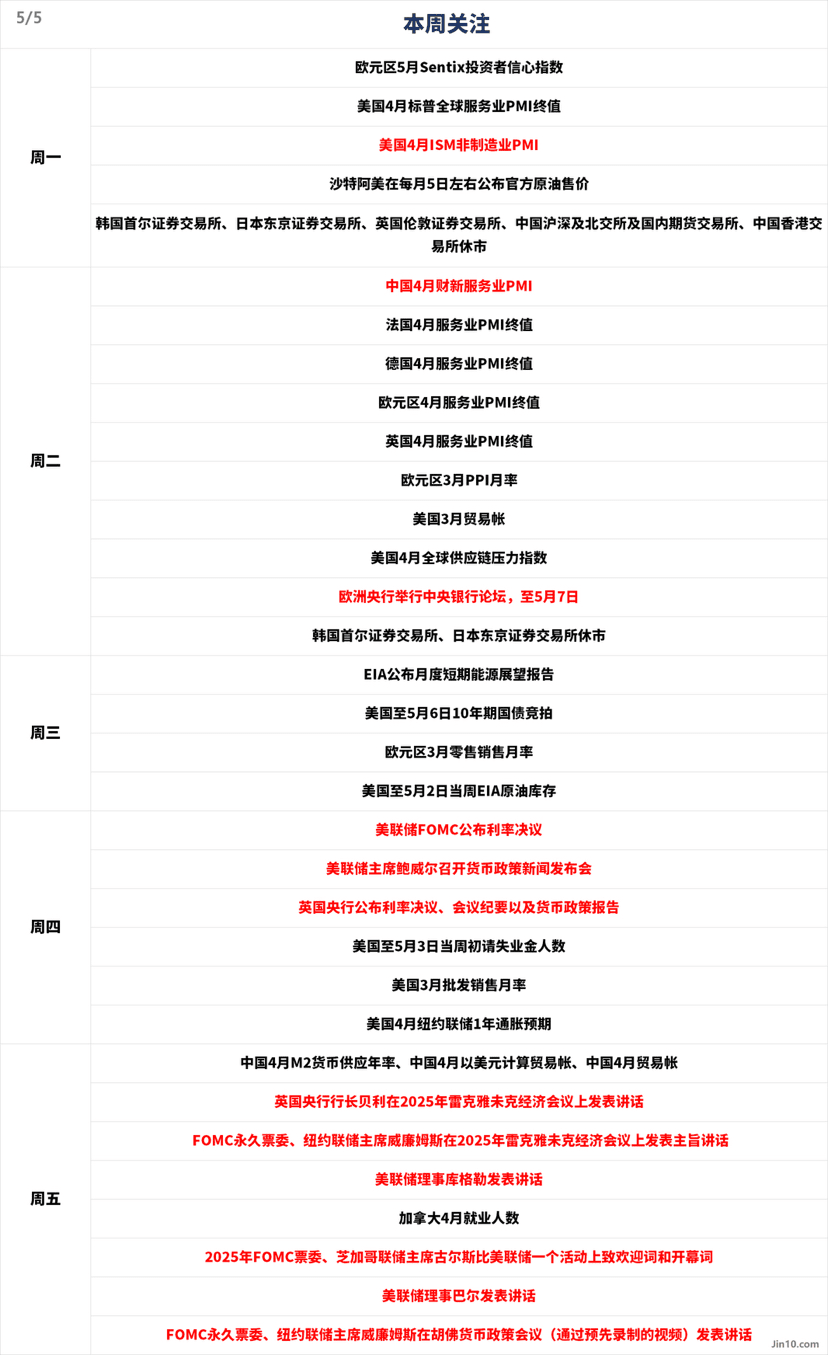

In the coming week, the market's attention will shift to central bank interest rate decisions, including the Federal Reserve and the Bank of England. In terms of economic data, service PMI reports from multiple countries will be released, and the U.S. earnings season will continue.

Here are the key points that the market will focus on in the new week:

Monday 21:45, U.S. April S&P Global Services PMI final value;

Tuesday 9:45, China's April Caixin Services PMI;

Wednesday 1:00, U.S. 10-year Treasury bond auction for the week ending May 6;

Thursday 2:00, the Federal Reserve FOMC announces interest rate decision;

Thursday 2:30, Federal Reserve Chairman Powell holds a monetary policy press conference;

Thursday 20:30, Initial jobless claims for the week ending May 3 in the United States;

Thursday 23:00, U.S. April New York Fed 1-year inflation expectations;

Friday 18:15, FOMC permanent voter, New York Fed President Williams delivers the keynote address at the 2025 Reykjavik Economic Conference;

Friday 20:00, Federal Reserve Governor Cook speaks;

Friday 22:00, 2025 FOMC voter, Chicago Fed President Goolsbee delivers a welcome and opening remarks at a Federal Reserve event;

Friday 22:40, Federal Reserve Governor Barr speaks;

Friday 23:30, FOMC permanent voter, New York Fed President Williams speaks at the Hoover Monetary Policy Conference (via pre-recorded video).

The Federal Reserve will announce its latest interest rate decision next week. There is widespread expectation that interest rates will remain unchanged, despite Trump frequently pressuring the Fed recently. Market focus will be on the Fed's policy statement and Powell's press conference for any signals regarding potential rate cuts later this year to boost the economy.

Looking ahead to June, 'Fed mouthpiece' Nick Timiraos stated after the non-farm data release: 'Currently, this (referring to non-farm) means the Federal Reserve does not need to express any views on June policy at next week's meeting.' He also added, 'The April employment report has lowered the possibility of a rate cut in June, as only one employment report has been released before that.' Goldman Sachs and Barclays have both pushed back their expectations for the next rate cut from June to July.

Market closure arrangements:

Monday (May 5), the Seoul Stock Exchange, the Tokyo Stock Exchange, the London Stock Exchange, China's Shanghai and Shenzhen Stock Exchanges, the Beijing Stock Exchange, domestic futures exchanges, and the Hong Kong Stock Exchange are closed;

Tuesday (May 6), the Seoul Stock Exchange and the Tokyo Stock Exchange are closed.

Due to market closures from Monday to Tuesday, attention may be reduced. Important events next week will concentrate on Thursday and Friday. If the news is positive, there may be a chance to touch 990/2000. If market control signals appear, it may continue to consolidate sideways.

Currently, the key level is at 950-1750. As long as it does not break below, it is positive news. Next, we will see how to strategize. In summary, the continuous upward movement from a low position indicates that the market is in a long-term upward trend. Yumi has hope for next week.