Preface

It took me a while to read The Block Research’s (2025 Digital Assets Outlook Report). It should be a report of relatively good quality in the wave of "review and outlook" at the end of the year. Moreover, the content of each chapter is also very complete. This article has organized some of this report and combined it with my views to provide it for your reference.

Next, let us take a look at the huge potential and application scenarios of blockchain technology from the impact of the overall economy to the vigorous development of various tracks!

1. Overall economy

First, the report starts with the overall overview of the blockchain industry in 2024. In terms of the overall economy, despite the challenging global environment, the U.S. economy has shown resilience, and the Federal Reserve's monetary policy has guided the economy toward stable growth. Cryptocurrency markets are also booming, with Bitcoin surging nearly 140% to a new high of $101,000, while Ethereum is also up 70%. The global cryptocurrency market capitalization reached an all-time high of $3.73 trillion, nearly double its level at the start of the year.

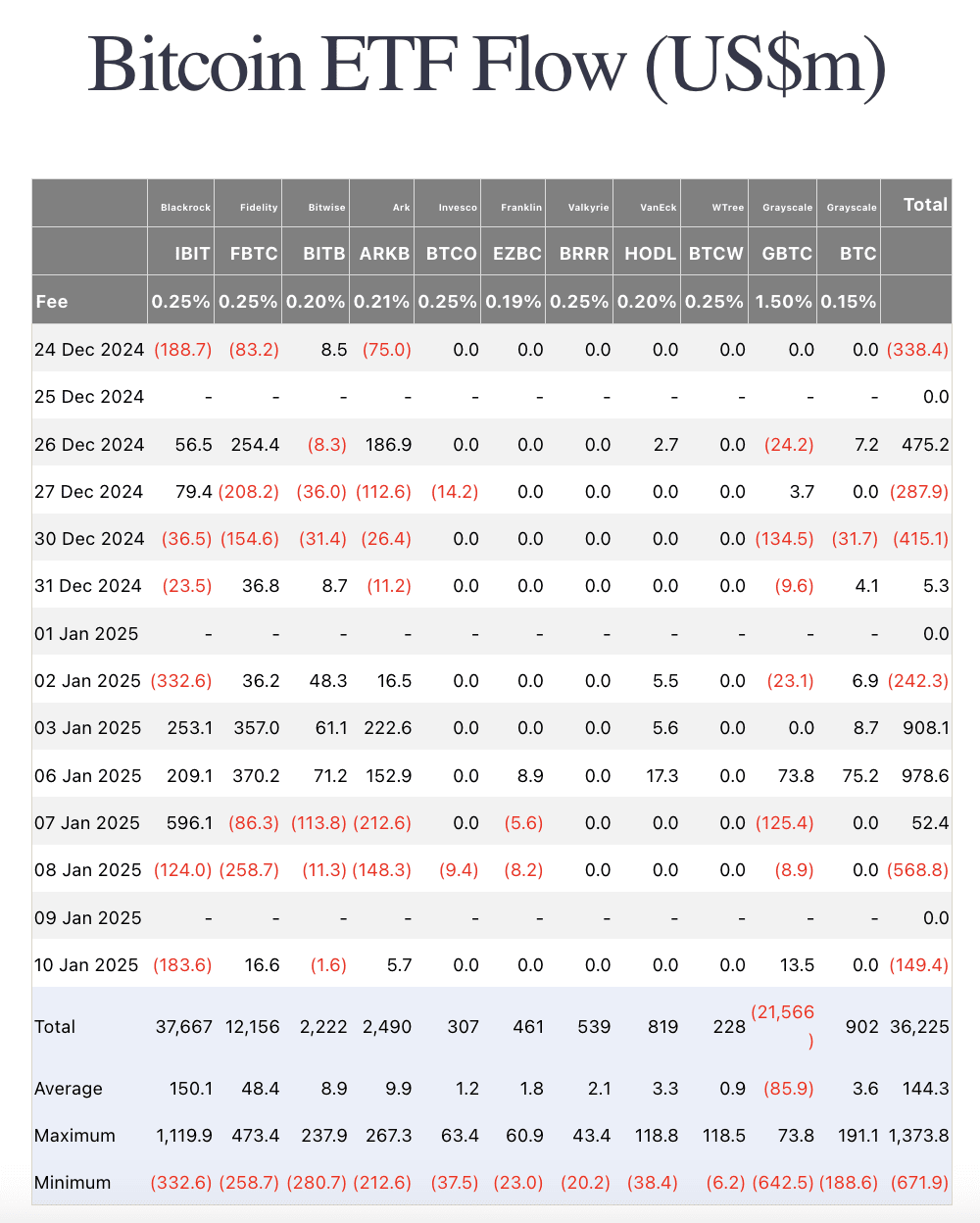

The approval of the Bitcoin spot ETF is another important milestone this year, attracting more than 11 million bitcoins in asset management. Among them, BlackRock's IBIT fund performed the most with more than 445,000 bitcoins under management, followed by They are Grayscale’s GBTC (216,000 Bitcoins) and Fidelity’s FBTC (188,000 Bitcoins). The success of these ETFs further cements Bitcoin’s place in mainstream finance.

In addition, airdrops have also become a hot topic in 2024, with more than 20 projects conducting airdrops and issuing billions of tokens in total. Among them, Layer 2 governance token airdrops dominate, and the Solana ecosystem has also seen several noteworthy airdrops.

Although a lot of money was made through airdrops last year, I think the development of "airdrops" was not good last year. A large number of points and task systems led to the entry of the Lumao Party, and the studio met many witch accounts to create false prosperity on the chain. , so the emergence of various projects with millions or tens of millions of users is actually quite strange.

2. Mining Industry

2024 is the year of Bitcoin’s fourth halving, with the Bitcoin block reward reduced from 6.25 to 3.125. Although the halving reduced miners' income, the rise in Bitcoin prices and increased on-chain activity, such as transactions for Bitcoin Ordinals, BRC-20 tokens, and Runes tokens, more than made up for this loss, making miners Revenue reached $13.3 billion, up from $10.5 billion in 2023.

It is worth noting that the composition of miners’ income has changed, and the proportion of fees for on-chain asset transactions once exceeded 1/5 in December 2023, indicating that the nature of activities on the Bitcoin chain is changing. However, the centralization issue among mining pools remains, with two major mining pools, Foundry USA and Antpool, controlling more than 50% of the computing power, raising concerns about transaction censorship.

Layer 1

In 2024, the Layer 1 blockchain ecosystem has undergone major changes, with the rise of scalable functionality, parallel execution, and consumer-centric applications becoming major trends. High-performance Layer1 networks such as Solana and Sui have gained huge demand among decentralized exchanges (DEX), stablecoins, and DeFi protocols due to their technical capabilities.

Solana’s high throughput and parallel execution capabilities have made it the platform of choice for meme coin trading, with monthly DEX trading volume surpassing Ethereum for the first time and cumulative fees reaching new highs, behind only Ethereum and TRON.

Sui’s parallel execution capabilities have also been recognized by the market, with $SUI becoming the best-performing Layer1 token, with an annual increase of approximately 316%.

The flow of stablecoins is also an important indicator of the growth of the Layer1 ecosystem. Sui, NEAR, Aptos, and Solana have all achieved significant growth in the market value of stablecoins, indicating that users are increasingly interested in these ecosystems.

However, although Ethereum has been suffering from FUD recently, Ethereum still dominates the stablecoin industry, with a total market value of more than $104 billion, reflecting its still certain role and positioning as a global settlement layer. If you judge the quality of a project purely based on currency price, then maybe you are not suitable for paying attention to this market for a long time.

4. Layer 2

In 2024, the Layer 2 industry has also made great progress, with many mainnet launches and token airdrops attracting new attention. The total value locked (TVL) grew from US$22.4 billion to US$42.8 billion, while the total monthly transaction volume also increased from 169 million to 562 million, demonstrating continued growth in user activity.

However, the decline in ecosystem activity after the airdrop indicates a lack of user retention on many newer Layer 2s, highlighting the prevalence of “mercenary capital.” The Ethereum Layer2 ecosystem is rapidly expanding, with more than 100 Layer2 deployed, but economic and user activities are concentrated on the largest and most liquid Layer2 such as Base, Optimism, and Arbitrum.

In order to reduce data costs, more and more Layer2 choose to use off-chain data availability solutions, and the implementation of the Dencun upgrade has also significantly reduced on-chain data expenditures. However, the risk of centralization in the Layer 2 industry is still high, and many Layer 2s lack effective status verification systems and exit windows, which poses a major threat to user security.

5. DeFi

As the DeFi industry continues to grow and consolidate, key trends such as prediction markets, meme currency trading, and the Restking protocol will surface in 2024, reshaping the industry landscape.

Prediction markets experienced explosive growth during the U.S. presidential election, with Polymarket trading volume exceeding $6.9 billion, proving its effectiveness as a reliable source of market intelligence.

Meme currency trading has promoted Solana’s activity. The Pump.fun platform has attracted a large number of users with its “fair launch” model and has become the leading platform for meme currency trading.

Leading DeFi projects continue to innovate. Uniswap launched Unichain and V4 upgrades, Aave’s V4 upgrade and $GHO stablecoin, and Maker changed its name to Sky and launched the Spark lending protocol, all demonstrating the vitality and development potential of the DeFi industry.

Restaking has also become a breakthrough track in the DeFi industry, and EigenLayer has led this trend. Its TVL was US$1.3 billion at the beginning of the year, reaching a record high of US$20 billion in June, and is currently stable at around US$16 billion. As the leading Liquid Restaking protocol, Ether.fi’s TVL reaches $7.3 billion, ranking fourth among DeFi applications, indicating strong market demand for yield and leverage.

6. NFT and games

In 2024, the NFT and gaming industries continue to face challenges, continuing the market downturn of previous years. Total project sales, number of transactions and average reserve prices continue to decline, especially in the gaming industry.

Most of the successful game projects have abandoned the speculative "play and earn" model that dominated the past, and the Ronin Network also showed impressive network indicators in the first half of this year. Highlights in the NFT industry include Milady Maker, Pudgy Penguins, and Bitcoin Ordinals, but the overall market remains sluggish.

Traditional NFT trading volume has dropped significantly. The average weekly trading volume of the Ethereum NFT market has dropped from approximately US$82 million at the beginning of the year to approximately US$33 million in June. The Bitcoin NFT market has also dropped from an average weekly sales volume of nearly US$200 million in April. Sales dropped to a weekly average of approximately $16 million in October.

Magic Eden has successfully responded to market challenges by expanding its functionality to multiple ecosystems such as Ethereum, Polygon, and Bitcoin, and has been particularly successful in Bitcoin Ordinals transactions. The outstanding performance of the Ronin network is due to its complete infrastructure and the migration of game guilds.

Although the chain game market is as cold as the recent weather, there are still battle royale games such as Off the Grid developed by Gunzilla Games, which managed to carve out a niche in the market this year and even attracted 150,000 people to watch the live broadcast at the same time as soon as it was launched. , and topped the EPIC Games Store free game rankings.

Additionally, one of the most anticipated trends in 2025 is the integration of artificial intelligence in NFT and GameFi projects. The ability of AI to create personalization, as well as (MapleStory N) and small games in cooperation with Kaia Network and LINE will be launched this year, which is still worth looking forward to.

In addition to the above, dynamic experiences also provide a compelling new dimension to gaming, allowing for adaptable in-game environments, AIGC content, and responsive non-player characters (NPCs) that can learn and evolve alongside players. We believe that more AI-driven analytics will enable more sophisticated personalization and player feedback, thereby increasing user engagement and retention.

7. Applications on the chain

In addition to the financial industry, blockchain applications have also shown strong development momentum in industries such as memes and gambling, on-chain consumption, real-world assets and DePIN.

Meme and gambling platforms combine financial incentives with social and gaming elements, with Pump.fun’s social trading platform, Fantasy Top’s competitive portfolio game, Rollbit’s crypto-native casino and Polymarket’s prediction markets all seeing significant growth.

On-chain consumer products are also changing traditional online interactions and transactions. Farcaster’s decentralized social network, Blackbird’s restaurant loyalty program and Galxe’s on-chain voucher system have all attracted a large number of users and investments.

Real-world asset (RWA) tokenization has also made significant progress, with total market capitalization growing from close to 0 in early 2020 to over $4 billion by the end of 2024, demonstrating the industry’s emerging product-market fit.

Since there is a very obvious gap in the statistics of RWA data from various platforms, I directly quoted the data from rwa.xyz in the figure below. As of January 13, the total market value of RWA has reached US$15.09 billion. (There is a significant gap with the aforementioned data from The Block)

The Decentralized Physical Infrastructure Network (DePIN) leverages token incentives and a decentralized network to enable individuals to monetize their idle resources while providing enterprises and developers with low-cost, elastic and scalable infrastructure. Solutions such as Hivemapper’s decentralized map platform and Filecoin’s decentralized storage network.

8. TradFi and Cryptocurrency

In 2024, the interest and participation of traditional financial (TradFi) institutions in cryptocurrencies has increased significantly, and the Bitcoin spot ETF launched by BlackRock, Fidelity and other institutions has achieved great success, driving institutional adoption and mainstream recognition.

BlackRock's BUIDL program is a good example of TradFi's entry into the blockchain industry, launching a tokenized money market fund that invests in U.S. Treasury bills, repurchase agreements, and cash, and on multiple blockchains The deployment demonstrates TradFi’s recognition of blockchain infrastructure.

In addition to ETFs, institutions are also exploring other cryptocurrency products and services, such as stablecoins, staking services, and tokenized RWAs. Different blockchain platforms have their own advantages in attracting TradFi, with Ethereum remaining the platform of choice for institutional-grade financial products, Avalanche suitable for enterprise and government applications, and Solana attracting high-performance trading and investment products.

The scope of institutional participation has also expanded its functions to industries such as payments, stablecoins, and Web3. Events such as Stripe's acquisition of Bridge, PayPal's launch of the PYUSD stablecoin, and Sony's establishment of a Web3 department all indicate that TradFi is actively integrating into the cryptocurrency ecosystem.

9. Supervision

The cryptocurrency industry emerged as a significant force in the 2024 U.S. presidential election, investing $135 million in support of crypto-friendly candidates through Super PACs, with notable success. After Trump is elected president, he is expected to bring major changes to the U.S. cryptocurrency regulatory policy, thereby promoting industry innovation and growth.

The Trump administration’s cryptocurrency policy priorities include turning the United States into a “Bitcoin superpower,” establishing a national strategic Bitcoin reserve, developing a comprehensive stablecoin architecture, opposing central bank digital currencies (CBDC), and reforming the Securities and Exchange Commission (SEC) Supervision methods.

In addition, current SEC Chairman Gary Gensler will leave his post after Trump takes office. The change in leadership also symbolizes a key turning point in U.S. cryptocurrency regulation. This change in leadership paves the way for major regulatory reforms. During Gensler’s tenure, more than half of the SEC’s crypto enforcement actions since 2015 occurred during his leadership.

The Trump administration is expected to adopt a friendlier regulatory approach, leading to the growth of market activities such as ETF products, multi-token products, venture capital, M&A, and IPOs. In addition, the government will support the development of tokenization and decentralized autonomous organizations (DAOs) to bring more innovation to the DeFi industry.

Congress is also actively pushing for crypto-friendly legislation, such as the Financial Innovation and Technology for the 21st Century Act (FIT21) and a new bill introduced by Senator J.D. Vance that aims to provide a clearer regulatory framework for the cryptocurrency market.

The response from the industry has been overwhelmingly positive, not only in terms of market performance but also in terms of institutional support. The successful election of pro-crypto congressional candidates and a coalition of 18 states challenging the SEC’s past regulatory approach show that cryptocurrency innovation is gaining increasing mainstream acceptance.

in conclusion

Overall, 2024 is an important year for the development of the blockchain industry, with significant progress made in various tracks. Although most people are still paying attention to memes and the prospects of AI, I personally think that it is already in an unhealthy industry development trend. As a result, the whole of 2024 will be a bit lackluster in terms of "innovation". It cannot be said that there is no innovation at all, but in terms of stunningness and long-term development, there is a clear gap compared with the past few years.

However, I believe that as technology continues to innovate this year, more institutions adopt it, and the regulatory environment improves, the blockchain industry is expected to usher in greater development opportunities. As for the "huge bull market" that many retail investors are looking forward to, I personally believe that when governments and institutions enter the market, it is unlikely that the crypto industry will have a performance beyond its past dividends. Not to mention that many governments are now discussing how to impose taxes.