First of all, it must be acknowledged that both Ethereum and Bitcoin are financial assets in a full transition phase. They are not yet completely defined by the market.

On this basis, I recommend following very closely all the pro-crypto regulation and legislation currently being developed in the United States, since this could accelerate the transition phase. For example, under the proposed CLARITY Act, BTC and ETH would be explicitly classified as Digital Commodities under U.S. federal law.

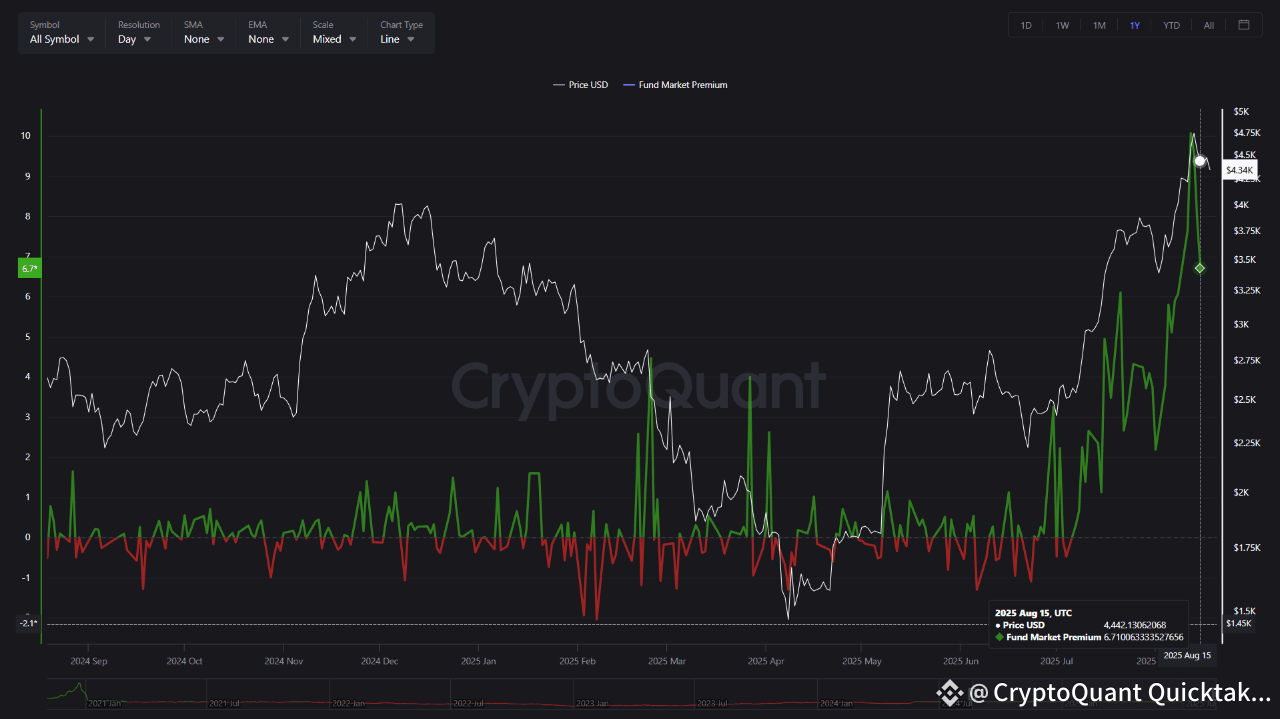

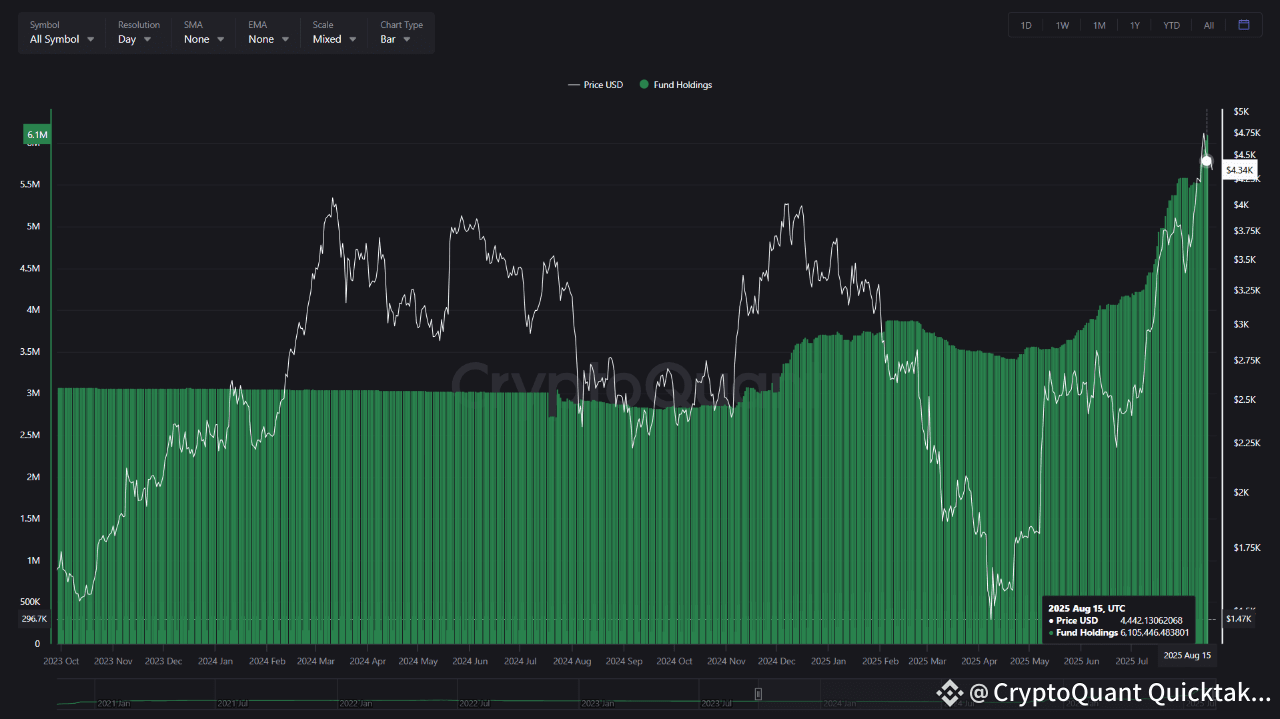

Regarding Ethereum, its institutional era began this year. To validate this statement, let us observe two institutional indicators: 1) Fund Holdings (net position) and 2) Fund Market Premium (premium paid).

1) Fund Holdings.

Based on the latest available data, there are currently 6.1M ETH in the hands of investment funds.

• Compared to the last ATH of December 2024 (3.62M ETH), this represents an increase of +68.40%.

• Compared to the last ATL of April 2025 (3.49M ETH), this represents an increase of +74.99%.

2) Fund Market Premium.

For this figure, I calculated its two-week average, which currently stands at 6.44%.

• Compared to the two-week average at the ATH of December 2024 (0.30%), the increase is +2,047%.

• Compared to the two-week average at the ATL of April 2025 (0.28%), the increase is +2,200%.

Conclusion:

Institutional demand for Ethereum is solid and consistent.

Moreover, beyond its technical impact, this flow of capital also generates a positive psychological effect on the market when observing how tier-1 investment vehicles, such as the Ethereum ETF managed by BlackRock, increase their ETH holdings. That is why I always recommend never underestimating the double effect that Wall Street produces.

This demand could increase further once staking is enabled in Ethereum ETFs, likely this year (it is not yet enabled).

Written by _OnChain