Ethereum’s recent breakout has triggered excitement across the market, but a closer look at the underlying flows suggests caution is warranted.

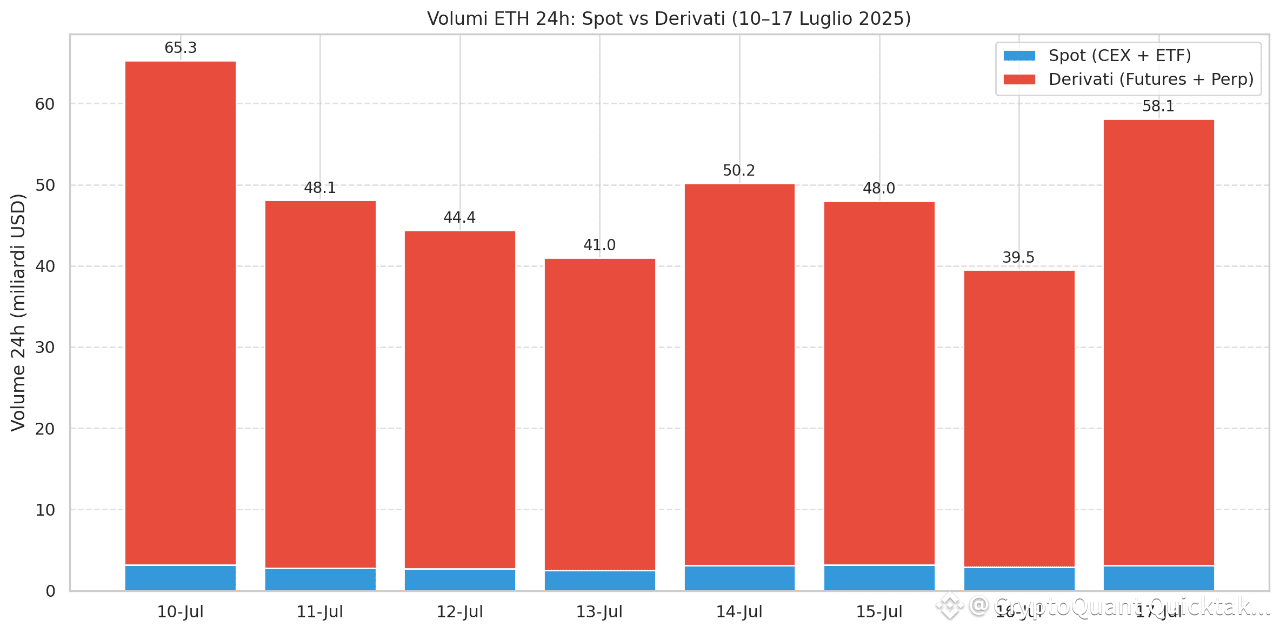

Over the past week (July 10–17), ETH’s 24h trading volume has consistently been dominated by derivatives. Daily notional volumes in futures and perpetuals ranged between $39B and $65B, while spot volume (CEX + ETF) remained relatively flat and modest in comparison. Even on days when ETF flows picked up, the structure remains mostly derivative-driven.

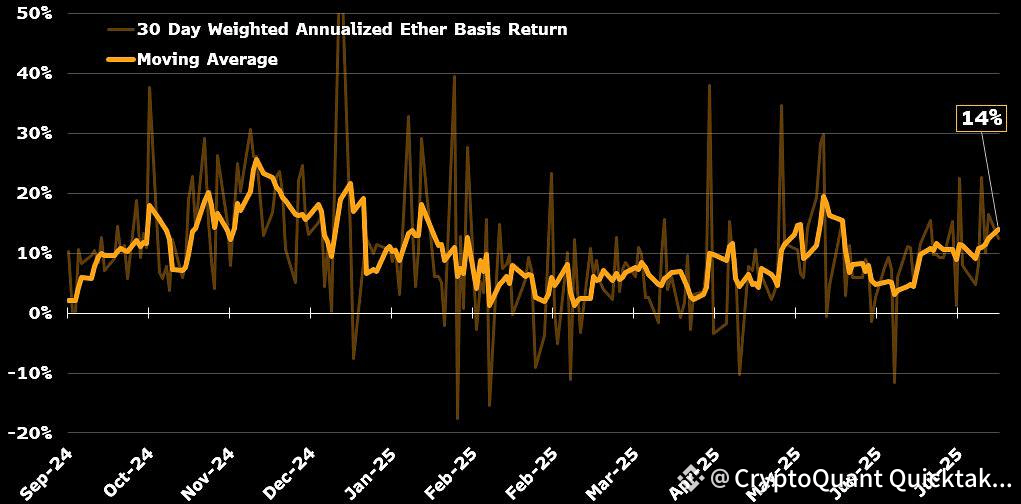

Moreover, there’s an important nuance: a significant portion of recent ETF inflows are likely tied to basis trades. This arbitrage strategy, which involves going long spot (or ETF) while shorting futures, has become increasingly attractive as ETH’s basis widened again, now offering up to 15% APR on a delta-neutral position.

This means that ETF inflows alone shouldn't be interpreted as directional bullish flows. In many cases, they’re simply one leg of a market-neutral arbitrage setup, with the other leg (a short futures position) applying structural pressure to derivative markets.

Until we see a meaningful increase in spot participation from real buyers, not just arbitrage desks, ETH’s rally remains fragile, and heavily dependent on the behavior of leveraged players.

It’s not that spot flows have been weak. It’s that they haven’t confirmed or supported the magnitude of the current move, which appears mostly engineered by futures positioning and funding dynamics.

In short: strong price action, but weak confirmation. ETH is dancing to the beat of derivatives; again.

Written by Cristian Palusci