@Falcon Finance When you begin to look closely at decentralized finance today, one of the questions that keeps coming up is: How can we unlock liquidity without forcing people to sell the assets they believe in? That tension is real for anyone who has held Bitcoin or Ethereum long enough to see prices rise and fall, or for someone who holds a tokenized real-world asset that has value but isn’t producing cash flow. Falcon Finance is one protocol trying to speak directly to that question, and the more I’ve looked into it, the more interesting the approach feels. It doesn’t promise magic, but it does offer a framework that feels grounded in real financial mechanics and that is worth understanding.

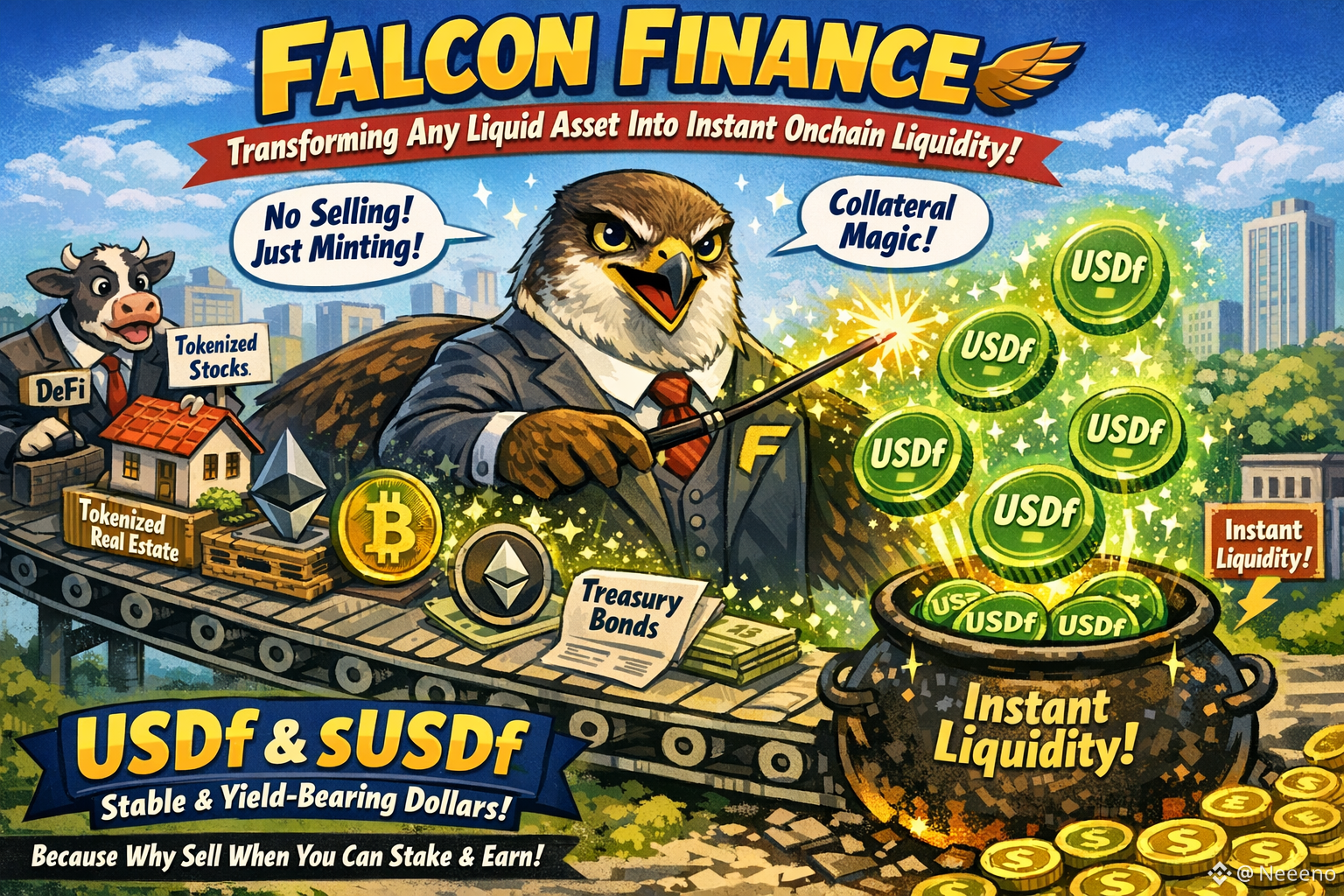

At its core, @Falcon Finance is a universal collateralization infrastructure. That phrase might sound like jargon, but the idea is straightforward: instead of restricting you to a handful of collateral types or forcing you to sell what you own just to get liquid dollars, the protocol lets you use a wide range of liquid assets as collateral and mint a synthetic dollar called USDf.

The “universal” part matters. Traditional stablecoins the kind that are simply redeemable for fiat sitting in a bank aren’t designed to accept, say, Bitcoin or tokenized equities as backing. Falcon’s architecture is different: it accepts stablecoins like USDT and USDC, *but it also accepts more volatile tokens such as BTC and ETH, and even tokenized real-world assets like sovereign bills or tokenized stock.When you deposit these assets into the protocol, you can mint USDf against them. The protocol enforces overcollateralization, meaning the value of the assets you deposit always stays higher than the value of the USDf you mint. This cushion is not a gimmick — it’s meant to maintain stability even if markets move quickly, and it’s the basis for USDf remaining near a one-to-one value with the U.S. dollar.

You might wonder why this matters now, and that’s a fair question. A few years ago, most DeFi projects focused on narrow segments of crypto: lending with a fixed set of accepted tokens, or yield farms that offered high returns for short periods. But the ecosystem has matured. People want systems that can handle diverse collateral classes, that can integrate with broader financial infrastructure, and that can bridge on-chain liquidity with real-world economic activity. That’s partly what Falcon is responding to.

A good way to see this is in the recent expansion of USDf onto Base, the Layer 2 network associated with Coinbase. According to multiple reports, Falcon Finance deployed over $2.1 billion worth of USDf to Base, making it a significant multi-asset collateral stablecoin within a rapidly scaling ecosystem. Integrations like this don’t happen just because of speculation — they happen because developers and users want stable, composable, and widely usable currencies on the chains where real apps are being built.

Once USDf is minted, you can simply hold it as a stable unit of account. But Falcon also offers a second layer of functionality through sUSDf. This isn’t just another token — it’s the yield-bearing version of USDf. When you stake USDf, you receive sUSDf. That token represents a claim on yields generated by the protocol’s diversified strategies, which might include arbitrage mechanisms, market-neutral trading, and other activities designed to produce returns over time.

That dual structure feels intentional. USDf itself remains focused on stability and liquidity, while sUSDf is built for yield over time. It’s a separation that people familiar with traditional finance might recognize: you hold a stable core asset, and separately you choose how much yield risk you want to take on. This separation probably explains why many users view USDf and sUSDf not just as tokens, but as financial primitives — building blocks for lending, borrowing, trading, and more.

The broader narrative here is not one of hype or quick gains. It’s a reflection of where DeFi is heading in late 2025: toward greater integration with real-world finance, more diverse collateral acceptance, and more composability across chains and protocols. Falcon’s use of tokenized assets, including equities and sovereign instruments, places it at that intersection. It doesn’t erase risk — markets can still move, and no system is perfectly immune to stress — but it frames risk in terms familiar to long-time financial engineers, not just crypto speculators

There’s also an important cultural shift underpinning this. The early DeFi era was driven by a kind of experimental rush. Projects promised huge yields, rapid forks of code, and incentive farms that burned through token emissions. What people talk about now is capital efficiency and real utility: how can assets stay productive without being sold; how can staked positions still earn yield while preserving core exposure; how can stable nets of liquidity serve both retail and institutional actors. Falcon Finance’s design choices reflect those conversations.

That doesn’t mean everything is settled. Maintaining a stable peg for synthetic dollars, managing risk across volatile collateral, and navigating emerging regulatory frameworks are all ongoing challenges. But in the context of current DeFi trends, projects like Falcon show how the space is evolving — not away from risk, but toward structured risk that can be measured, diversified, and (hopefully) better understood.

At the end of the day, what Falcon Finance offers isn’t just another stablecoin or yield product. It’s an idea about how liquidity should work in a future where assets aren’t boxed into narrow categories, where collateral can be as diverse as the portfolios people actually hold, and where on-chain value can connect more directly with traditional markets. That’s why USDf and its ecosystem matter now, and why the conversations around universal collateralization feel like more than just another trend.

@Falcon Finance #FalconFinance $FF