Andrew Kang challenges Ethereum’s “digital oil” story, arguing stablecoins, RWAs, and institutions fail to boost network revenue or long-term valuation.

He warns ETH’s high P/S ratio, weak fees, and bearish technicals show structural problems, predicting sharp downside if narratives collapse.

Kang contrasts Wall Street optimism with crypto-native caution, saying ETH risks commodity-like stagnation unless it evolves into digital infrastructure.

On September 25, 2025, the crypto market saw another dramatic day. Tom Lee, co-founder of Fundstrat, said in public that Ethereum’s (ETH) “fair value” is $60,000. He called ETH “digital oil” and said it will benefit from the rise of stablecoins and real-world asset (RWA) tokenization.

His bullish view sparked debate. Andrew Kang (@Rewkang), founder of Mechanism Capital, pushed back hard. On X, he said Lee’s claim “is one of the dumbest, financially illiterate arguments,” and he restated his bearish view on ETH. The current ETH price has fallen below $4,000, down 13% from last week. This supports part of Kang’s concern and adds uncertainty to the market.

Kang is known for sharp insights. During the market correction in April 2025, he predicted ETH would drop below $1,000. It was seen as extreme then, but looks prescient in today’s weak market. This article breaks down Kang’s five bearish points and looks at ETH’s outlook after the ETF era. Is it a Wall Street bubble story, or a structural problem inside crypto?

POINT ONE: THE “GROWTH ILLUSION” OF STABLECOINS AND RWA — WHY ARE FEES FLAT?

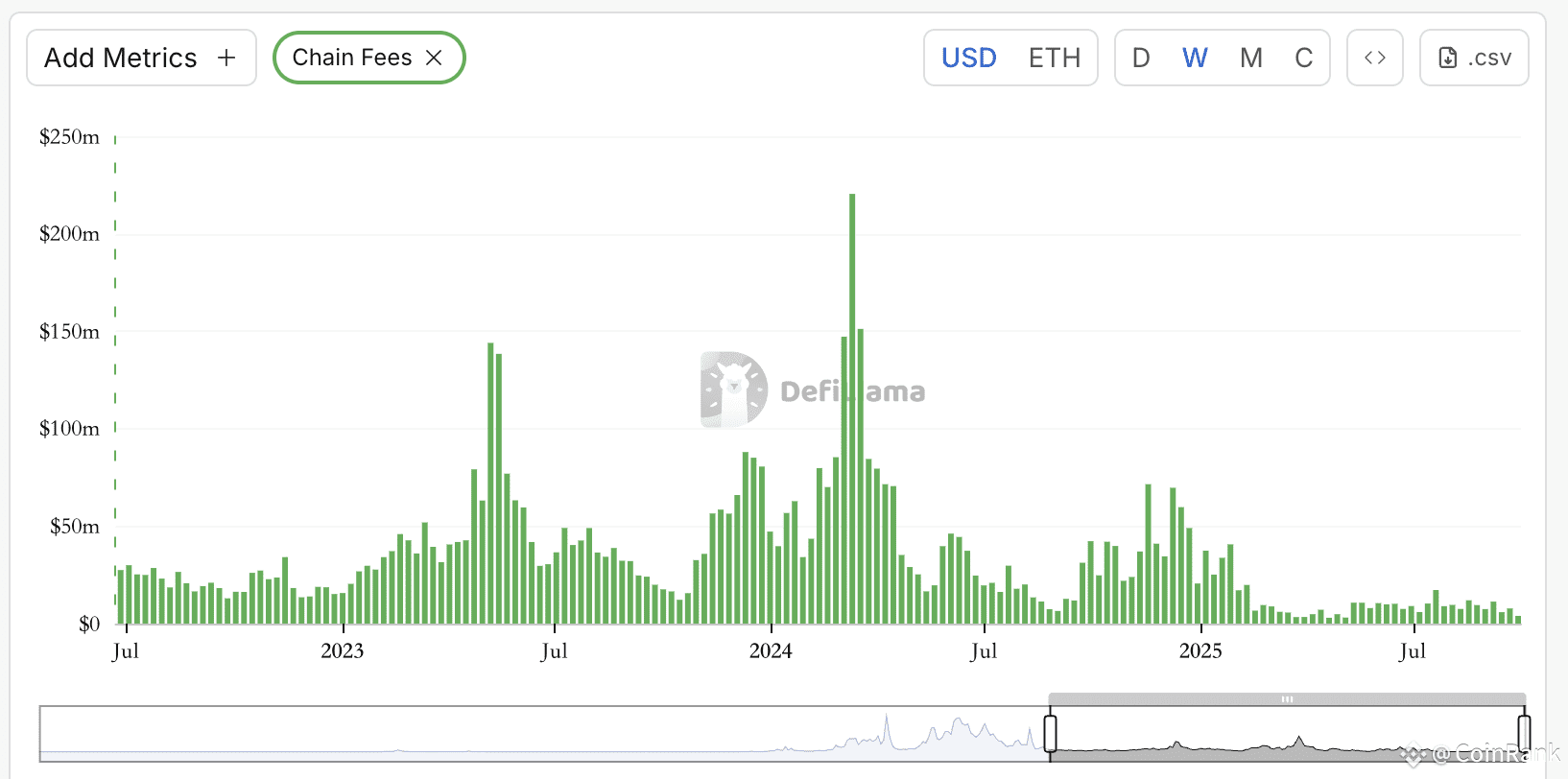

One core question from Kang: the huge growth of stablecoins and RWA has not turned into real revenue for the ETH network. Since 2020, stablecoin volumes grew by 100–1000x. The value of tokenized RWA jumped to the trillion-dollar range. But ETH gas fees are almost the same as in 2020 and only show a small part of on-chain activity. He said: “You can tokenize trillions in assets, but if these assets are not active, they might add only $100,000 of value to ETH.”

This view is not baseless. In September 2025, ETH daily fees moved around but mostly stayed in the $5–10 million range, far below the 2021 peak near $100 million. Even worse, Layer 2s (like Arbitrum and Optimism) are moving many transactions to cheaper chains. Solana, with stronger BD teams, has won over 20% of stablecoin activity. Kang thinks this shows a fragmented ETH ecosystem: the RWA story looks shiny, but it does not create sustainable fee growth. It may be a short-term bubble, like the post-2024 meme-coin boom that later faded.

From a macro view, this comes from an “open-access tragedy of the commons.” Openness brings innovation but weakens value capture. The Dencun upgrade lowered L2 costs, but mainnet fees fell further. Kang warns: if RWA adoption stays “surface-level,” ETH’s revenue model will face long-term pressure.

POINT TWO: THE “DIGITAL OIL” NARRATIVE — THE DOUBLE-EDGED SWORD OF COMMODITIZATION

Tom Lee compares ETH to “digital oil” to show its value as a store and medium of exchange. Kang flips it: “I agree ETH can be seen as a commodity, but that is not bullish. I have no idea what Tom is thinking!” Oil, as a classic commodity, has an inflation-adjusted real price that barely changed over the last century. It swings in cycles and often reverts to the mean.

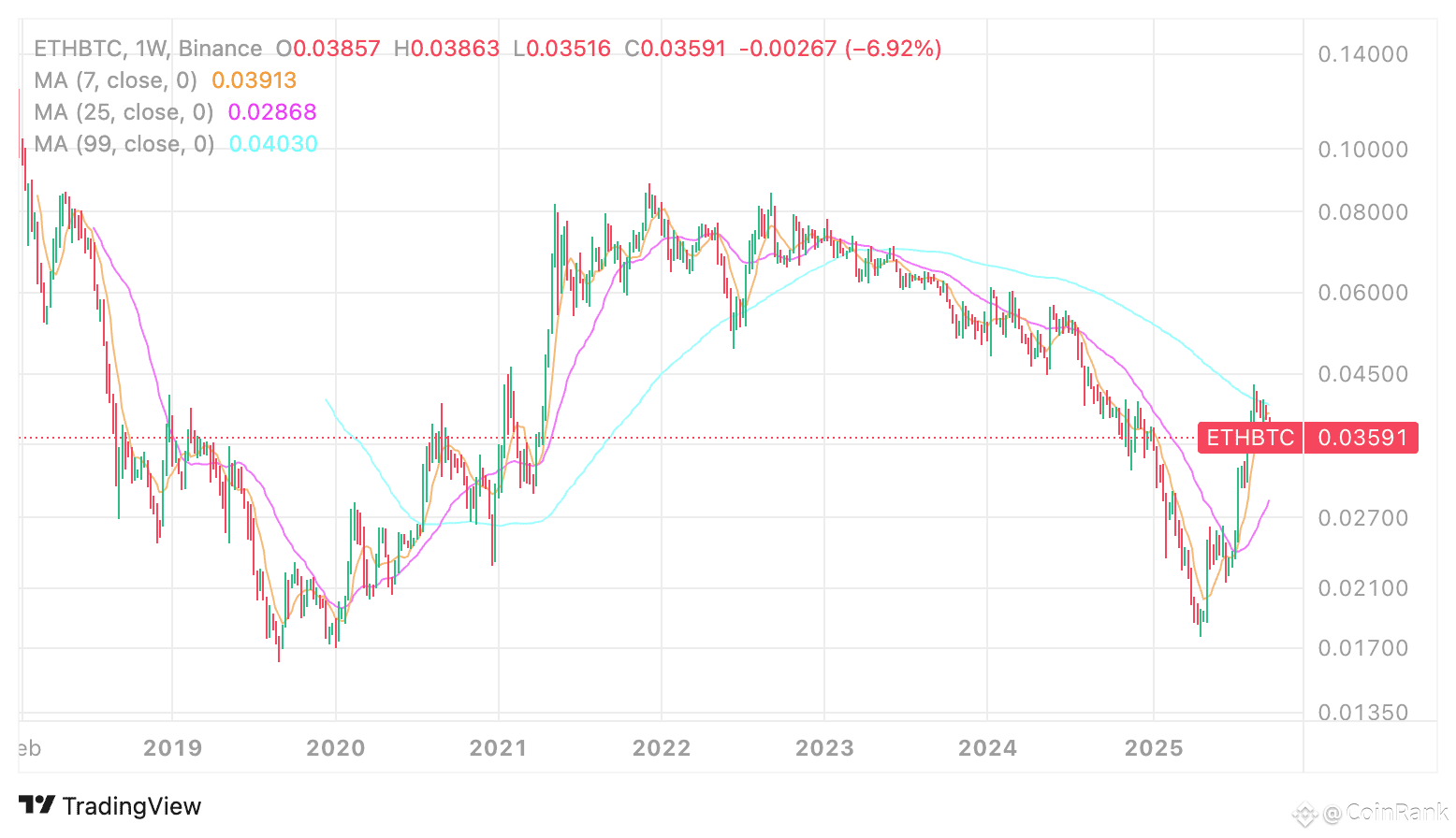

This is the irony. Commodity traits mean volatility and outside dependence. If ETH is truly “digital oil,” its price will depend more on macro forces (like the Fed’s rate cycle) than on tech progress. In September 2025, the ETH/BTC ratio fell to 0.045, half of its 2021 high. Bitcoin’s “digital gold” story looks stronger. Geopolitical shocks can push oil up, but similar shocks for ETH (like tougher rules) are more likely to cause selling.

Kang says Lee ignores mean reversion in commodity markets. Oil often falls 50% or more in bear turns. If ETH follows that path, a move from $4,000 to $2,000 is very possible. This is not only a metaphor but a warning on market psychology: romantic stories near the top often burst.

POINT THREE: INSTITUTIONAL ADOPTION ON PAPER — WHY WOULDN’T BANKS HOARD ETH?

Lee thinks institutions will stake ETH, lock supply, and drive price up. Kang answers with realism: “Do banks hoard gasoline because they must pay energy costs all the time? No. They pay as needed.” As of September 2025, big banks like JPMorgan and Citi have not put ETH on their balance sheets, and they have no public staking plans.

This hits the weak spot of the ETH ETF. After approval in 2024, net inflows once reached $5 billion. But in Q3 2025, net outflows topped $1 billion. The reason is clear: staking yield (about 4% APY) is below bonds and has unlock risk. Giants like BlackRock may hold ETH, but often for trading, not long holding. Kang says real institutional use needs clear rules and strong liquidity. Today, “institution-friendly ETH” looks more like marketing.

Since August, several top traders turned bearish on ETH and warned of multi-billion-dollar liquidations. This supports Kang’s view: shallow institutional money can amplify downside.

POINT FOUR: ROOTS OF AN EXPENSIVE VALUATION — THE CEILING OF FINANCIAL ILLITERACY

Kang says ETH’s market cap (about $480 billion) is near bubble territory, driven by “financially ignorant” thinking. Speculation can lift price in the short run, but without fundamentals it will return to reality. Unless the Ethereum Foundation makes big changes (for example, improving fee burn), ETH will likely underperform for a long time.

By numbers, ETH’s price-to-sales (P/S) is above 100x, far higher than tech stocks on average. Bitcoin’s P/S is only about 30x. This shows ETH’s premium comes from narrative, not cash flow. Kang predicts this “ignorance dividend” has a clear cap. When retail wakes up, selling will come.

POINT FIVE: BEARISH TECHNICALS — A MULTI-YEAR RANGE AS AN IRON CURTAIN

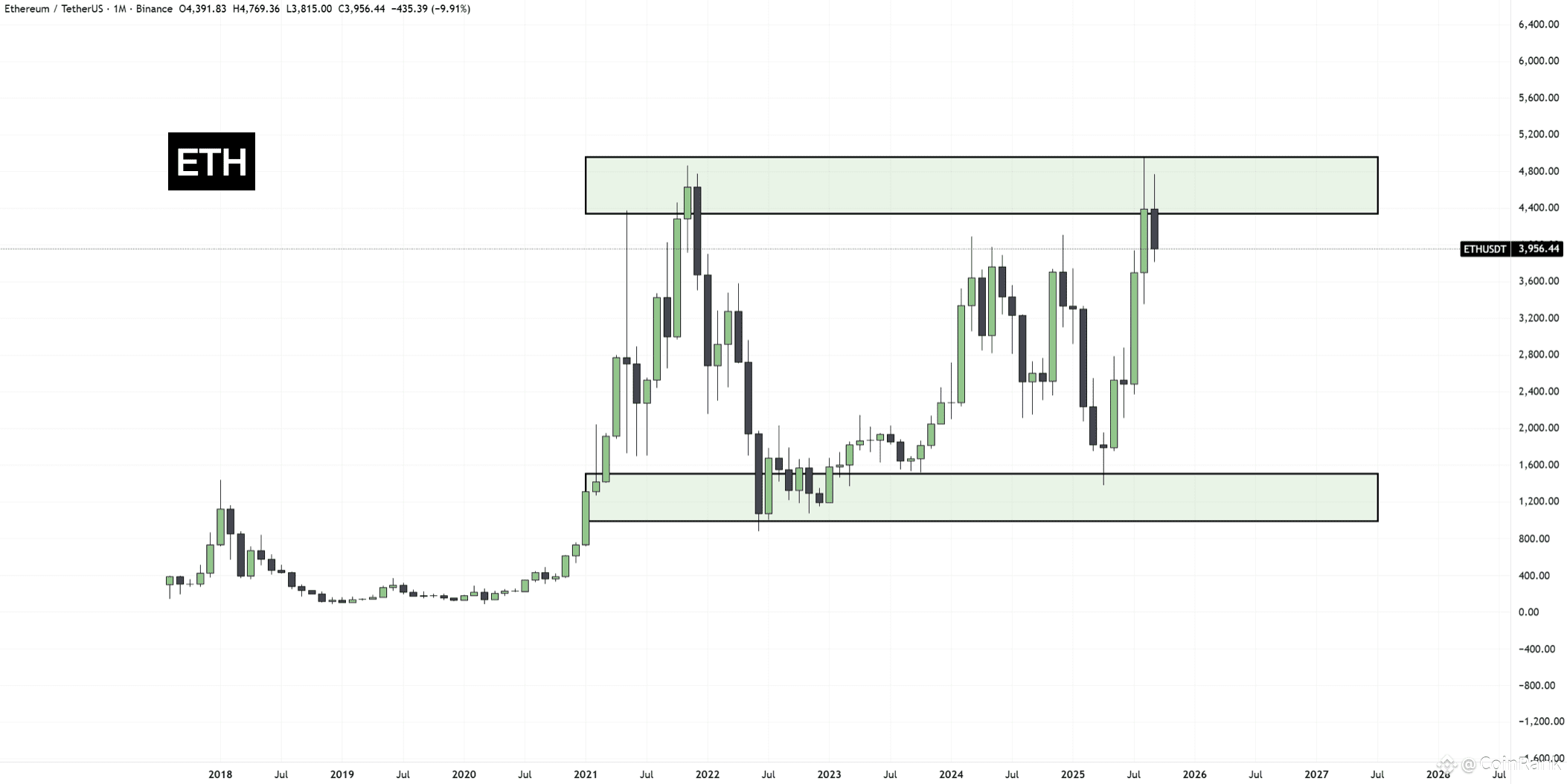

From charts, ETH trades in a multi-year range between $1,000 and $4,800. It hit $4,800 in September but failed to break out. RSI is now in oversold territory. ETH/BTC is in a down channel. Story fatigue plus weak fundamentals support further downside. Key support sits at $3,800–3,500. A break could open an extreme move to $2,800.

Some analysts still see $5,000 by year-end. But retail activity is low in September, and whale liquidations are frequent (one whale lost $36 million). This adds to a bearish mood. Kang’s long-term view: ETH will range until the ecosystem restructures.

CONCLUSION: COMMUNITY DIVIDE AND ETH AT A CROSSROADS

Kang’s bearish stance is not random noise. It is a systematic diagnosis of ETH’s pain points. It offers “exit liquidity” for crypto natives, but also triggers backlash. Some praise his accuracy. Others say he ignores Layer 2 potential. Looking to late 2025, if ETH breaks above $4,950, the $5K hope may return. If not, the “$1,000 ghost” will come back.

Between narrative and reality, ETH’s future depends on shifting from “digital oil” to “digital infrastructure.” Investors should watch short-term volatility and track fee data and institutional moves.

〈Andrew Kang Turns Bearish on ETH: A Deep Challenge to the “Digital Oil” Narrative〉這篇文章最早發佈於《CoinRank》。