11/06 -11/12 64 issues

This weekly report was co-authored by SnapFingers DAO builders Discord: Ya#3727Gu#4974Twitter: @linyao1900 @Guaaronnnn

01 The impact of FTX collapse on crypto regulation

Technological progress has promoted the development of the crypto industry, but it has also brought many problems. At the national level, the anonymity and decentralization of crypto assets provide fertile ground for criminal problems. Traditional regulatory methods are highly dependent on centralized financial institutions such as banks, and the anti-censorship characteristics also increase the difficulty of law enforcement. In addition, virtual currencies in crypto assets, as payment tools, theoretically pose a certain threat to the stability of existing national currencies and affect the central bank's macro-control capabilities.

In terms of regulatory practice, China took the lead in issuing a complete ban during the crazy ICO in 2017, and other countries and regions also began to take specific measures on the legal attributes and regulatory systems of cryptocurrencies around 2018. According to the "Global Cryptocurrency Rules" and "Cryptocurrency Rules for Specific Jurisdictions" issued by the United States in 2018, the current regulatory models are generally divided into three categories:

1. Complete ban

For example, in mainland China, crypto assets and trading platforms are illegal, and strict regulatory policies have been introduced. With the crackdown on cryptocurrencies in 2021, many local Chinese service providers have chosen to move to other countries.

2. Apply existing framework

Such as Singapore and Japan. Cryptocurrency trading and exchanges are legal in Singapore. The Monetary Authority of Singapore (MSA) applies the existing legal framework as much as possible and takes an accommodative approach to cryptocurrency trading. At the same time, based on past policies, the MSA may follow up with other regulations to adjust its position. Japan is the first country to provide legislative protection for virtual assets. It has the most advanced cryptocurrency regulatory environment and recognizes Bitcoin and other digital currencies as legal property.

3. Modify and establish a new framework

For example, Hong Kong, China. Previously, crypto assets were not subject to the regulatory scope of the Securities and Futures Ordinance. Hong Kong adopted a sandbox regulatory approach to conduct regulatory experiments and announced the "Policy Declaration on the Development of Virtual Assets in Hong Kong" at the recent Fintech Week, which regulates the licensing rules for virtual assets.

Summarize

Combined with the recent SEC review of YugaLabs and whether PoS coins are considered securities, we can see that this is a problem of regulatory logic. With the development of encryption technology, DeFi, blockchain games, social networking, creation and other ecosystems need a good growth environment, so it is very important to clarify regulatory guidelines. For the above-mentioned Web3 applications that have emerged due to encryption technology, the focus of supervision should be on the application itself, not the underlying protocol. Similarly, the supervision of encrypted asset transactions should be on the trading platform, not encryption technology.

Traditional exchanges such as Nasdaq and NYSE have already entered the crypto asset trading business, which provides a certain reference for the supervision of trading platforms. The current operation mode of centralized exchanges is very similar to traditional finance, so the possible platform supervision in the future may be familiar, such as the three aspects of entry threshold, information disclosure and technical maintenance. On this basis, law enforcement may be emphasized to maximize the protection of investors' interests.

The essence of FTX's collapse is that it has its own fraudulent behavior. Centralized exchanges can only be built on trust without supervision. We did not see any supervision in the FTX incident, nor did we see the disclosure of the supporting funds for related operations. The introduction of Proof of Reserve can only be said to be helpful in internal fund management, and it may be more of a gimmick for centralized exchanges. We still need decentralization.

02 CEX and DeFi data performance during the FTX crash

The first plunge of FTT began on November 8, and then a large amount of assets flowed out of FTX. At the same time, FTX's transfer of assets deepened users' distrust of CEX. Assets flowed out of major exchange platforms. Further, the trading volume of DEX relative to CEX increased significantly, and some leading DeFi coins grew against the trend. More and more voices believe that DeFi is the future of Crypto trading. The following summarizes the data performance of CEX and DeFi during the collapse of FTX.

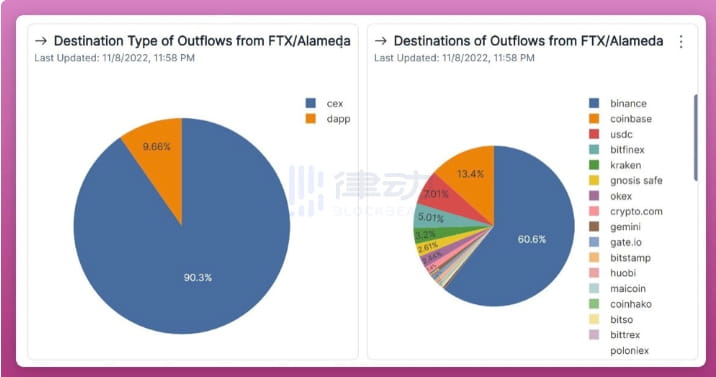

According to flipsidecrypto data, most of the cryptocurrencies withdrawn from FTX flowed to Binance, accounting for 60.6% of the withdrawal flow, followed by Coinbase (13.4%). In general, 90.3% of cryptocurrencies still flowed to CEX.

Nansen data on November 14 showed that in the past week, Nansen-tagged addresses alone withdrew $3.7 billion worth of stablecoins (based on Ethereum) from major platforms (including Binance, OKX, Kucoin, Huobi, Kraken, Coinbase, Bitfinex, etc.).

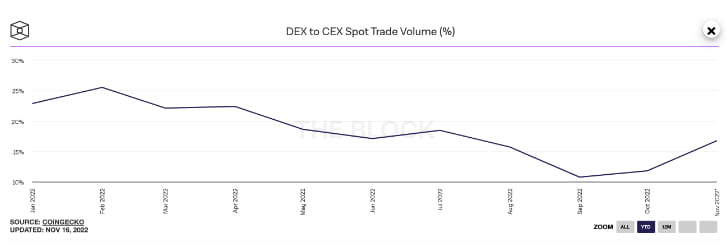

According to data from Theblock as of the 16th, the ratio of DEX and CEX trading volumes, in terms of spot and futures contract trading, has shown a significant increase of 50% compared to October.

According to ultrasound.money data, Uniswap V3 and V2 burned more than 2,300 ETH in 7 days from November 8 to 14, and were one of the main contracts that caused ETH to fall into deflation during this period.

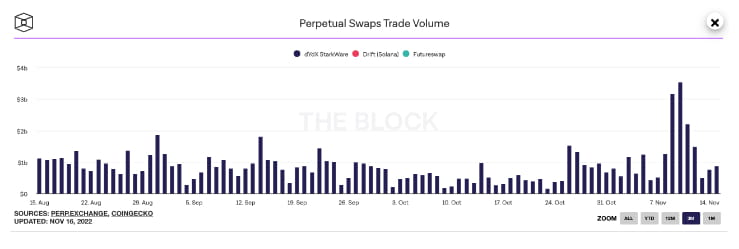

Under extreme market conditions, derivatives trading is significantly active. Coupled with the CEX trust crisis, decentralized derivatives have seen a double increase in trading volume and token prices. DYDX rose 39% in 7 days.

The short-term DeFi data growth brought about by the FTX collapse is clearly event-driven, but the CEX trust crisis will be deeply imprinted in the minds of current crypto market participants. Just as those who experienced the Mentougou incident will trust the wallets they control more, user anxiety and distrust will become the driving force for the long-term development of DeFi.

03 Crypto OG’s views and opinions on the FTX incident

The sudden collapse of financial markets and market shocks have had a huge impact on people’s values. At times like this, we need long-termists’ incisive summaries and a firm attitude towards the future. Some important figures have expressed their views at critical moments.

Arthur Hayes|CEO and Co-Founder of BitMEX

Initially laughed off the idea that FTX would be the Lehman Brothers of this crypto credit cycle.

Believe that the last candle of this crypto bear market is coming soon.

Centralized exchanges will always face these trust issues on behalf of their customers.

FTX is not the first high-profile exchange to fail, and it won’t be the last.

Haseeb |Partner at Dragonfly

Regulation will certainly become stricter around the world.

This is far more serious than what happened with 3AC or Terra at the time because fraudulent lenders are different from gamblers.

The worse situation has not yet arrived, and its indirect impact has not yet been seen.

Don't trust, verify; don't trust humans, trust code.

The core error of all religions is to treat people as objects of worship, which is vividly reflected in the SBF incident.

Crypto will absolutely change the world, it will change the way people and machines interact with money and value.

Yat Siu|Animoca Brands CoFounder 兼 CEO

Animoca’s exposure to FTX is limited to insubstantial trading balances.

Uneasy about the irresponsible behavior of a very small minority.

The losses suffered by the industry over the past week have certainly been devastating, but not as severe financially as what occurred about five months ago.

The work we do now is contributing to our digital future.

The FTX crisis, and other larger crises including Lehman Brothers, occurred because many powerful elite players, often through fraud, pursued zero-sum outcomes that undermined the industries they touched.

The dot-com bubble of 2000, the financial crisis of 2008, and the crypto bear market of 2018 did not stop the growth of the internet, smartphones, and cryptocurrencies. Likewise, current market conditions will not kill Web3.

We firmly believe that Web3 represents the natural evolution of the Internet, the future of digital property rights and the resulting economic freedom that will empower billions of online users in a series of interconnected open worlds and platforms.

🫰I heard that friends who click more likes have good luck, and friends who pay attention to the snapping fingers have a keen eye! 🫰