In the past week, if you ignored the movements in the DeFi sector, you might have missed an important action from @pendle_fi—on July 30, Pendle officially integrated HyperEVM, launching four yield pools all at once.

Within 72 hours of launch, the TVL reached over $65 million, directly pushing HyperEVM into Pendle's 'third-largest TVL chain', second only to Ethereum and BNB Chain.

The signals released behind this are more significant than they appear:

Pendle's expansion logic is not just about multi-chain deployment, but rather about efficiently capturing arbitrage generation spots, starting reverse selection—wherever the real and clearly structured yields are, it will go there.

And HyperEVM, due to its integration this time, is beginning to showcase its real potential as a 'yield layer'.

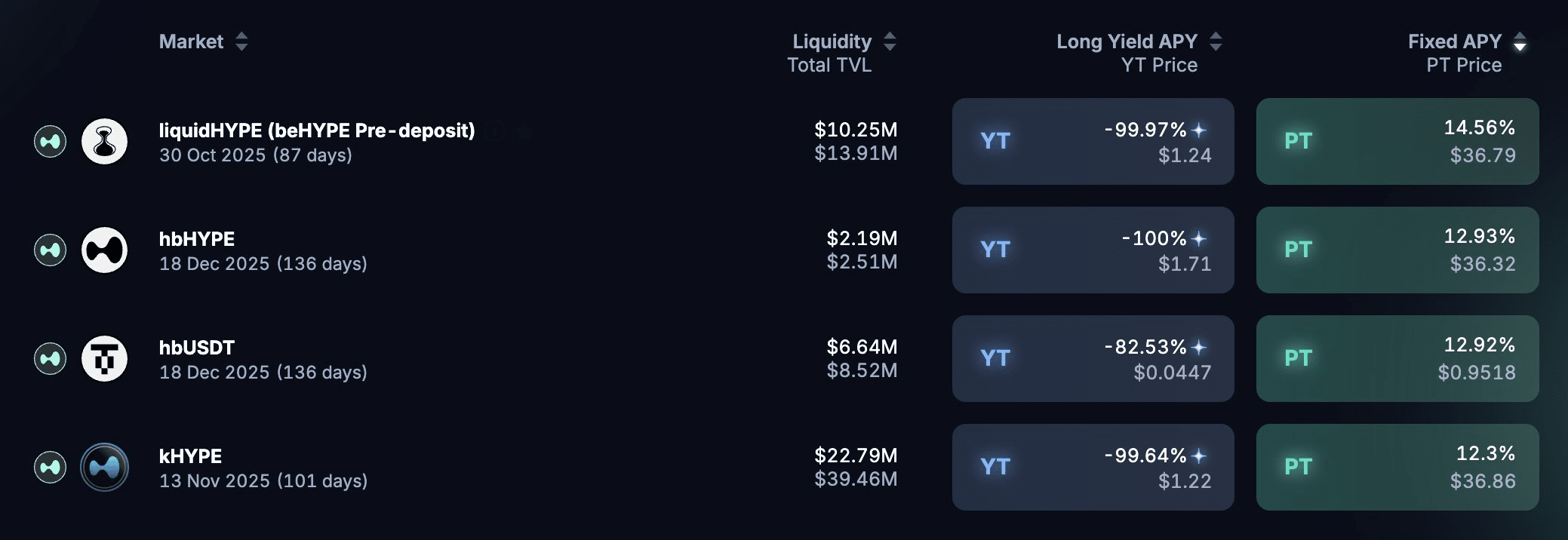

1. Four types of assets correspond to the complete yield structure of current DeFi.

The four pools launched by Pendle this time: hbUSDT, kHYPE, beHYPE, Ultra Hype. These four asset types cover almost all mainstream participation strategies of DeFi users.

📍hbUSDT, anchored to dollar investments, with a safety margin:

hbUSDT is @0xHyperBeat USDT and is the main product of Hyperbeat Earn, with yield primarily coming from Hyperliquid's trading fees (over 60%), theoretically close to risk-free, with the remainder from LP market-making profits.

Both YT and LP can receive points rewards from 7 projects (Hyperbeat / Hyperswap / Ethena / Resolv, etc.), essentially a collection of airdrop expectations.

📍beHYPE, time-limited high yield + points mapping:

Launched in collaboration with Hyperbeat and http://Ether.fi, it is a liquid staking asset, backed by a 6-week points release event (HEART + PENDLE). Its YT is essentially an on-chain version of 'points options', and the timing for exit needs to be assessed before the points event ends.

📍kHYPE, high leverage growth strategy:

PT-kHYPE can be used as collateral to borrow HYPE in HyperLend, then repurchase PT to build a circular position, allowing for up to 5 times leverage, suitable for strategy players skilled at controlling positions.

📍Ultra Hype, lightweight incentive pool:

Although small in scale, it has outstanding yields, low participation thresholds, and a rich combination of points incentives, making it suitable for small-scale, high-quality operations.

Each of the four pools has its own points plan. I personally lean towards stablecoin investments, so I chose PT-hbUSDT. If you have better yield strategies, feel free to share in the comments!

2. Why did Pendle choose to support HyperEVM?

This time Pendle's integration with HyperEVM is actually a continuation of its structured expansion logic:

HyperEVM is one of the few chains with 'real yield sources + high trading volume + on-chain structural incentives', perfectly meeting Pendle's three ideal core conditions:

1) There are stable yield assets (hbUSDT, with real income from Hyperliquid trading fees)

2) There are structured assets (kHYPE, beHYPE can earn points, are collateralizable, and can be leveraged)

3) There is an internal interlinked flywheel design (achieved through LayerZero for ETH↔️Hyper asset cross-chain)

And for HyperEVM, it is also beneficial—

With Pendle, it’s not just about attracting traffic, but HyperEVM also gains an 'interest rate operating system', integrating what was once fragmented points, yields, collateral, and lending into a complete DeFi structure.

3. A change that is happening: structural protocols are starting to dominate chains, which are being reverse integrated by financial structures.

Pendle × HyperEVM is not just a protocol deploying a new chain, but more like a rehearsal of a new type of power structure.

In the traditional model, the chain is the stage, defining ecological boundaries, and the protocols are the actors, making a living on the chain;

But Pendle is beginning to guide 'yield construction' towards a healthier and more sustainable direction—yield logic of the chain itself and related assets are starting to recombine around it, using structural decomposition to generate market-based arbitrage.

From the perspective of participant roles, this change is reshaping power relationships:

1) Project parties are no longer the incentive leaders, but rather expected debt issuers;

2) Users are not just participants, but speculative arbitrageurs of yield structures;

3) Protocols are not just strategy platforms, but structural clearing centers for interest rates and expectations.

Pendle is more like a structural general contractor on the chain, using its interest rate mechanism to package the scattered yields, liquidity, incentives, and expectations across various projects into a valuable market.

This is the core significance of this wave—

Pendle is transitioning from a construction tool to an architectural power, becoming a 'financial intermediary structure of the chain', providing a complete set of financial language to describe and trade all of this!