Bomb #1: Inflation Easing — but not Fast Enough

.

.

What this means: Inflation is cooling—but not quickly enough to stop policymakers from staying cautious. The Fed’s job of anchoring prices isn’t done, and markets expect further vigilance. Recent commentary suggests rate cuts may come later in the year, possibly around September .

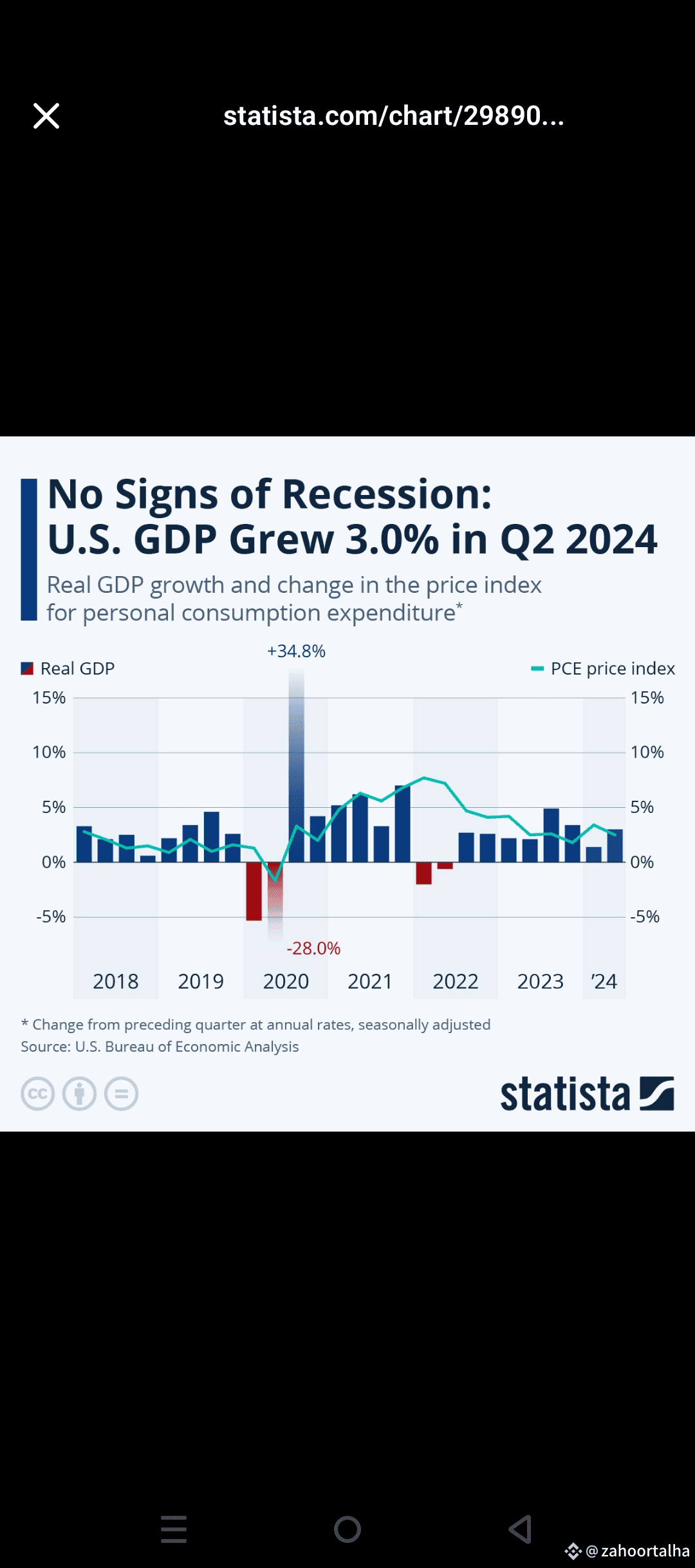

Bomb #2: GDP Surges 3% — But It’s Deceiving

.

.

.

In essence: The growth narrative is skewed. Tariff-induced trade swings and inventory corrections drove the headline number, while real domestic spending and investment remain sluggish and cautious.

Sector Deep Dive

ComponentQ2 Performance & ImplicationsConsumer Spending .Business Investment & ResidentialInvestment in equipment slowed sharply; residential construction continued contracting for a second quarter .InventoriesDeclined, shaving roughly 3.2 percentage points off GDP as businesses worked down earlier stockpiles .

Market and Policy Reaction

.

.

.

The Underlying Story: Masking a Slowing Economy

.

.

Outlook: What Comes Next?

.

Consumer trends may weaken: car-buying surges tied to tariff fear are unlikely to repeat.

Corporate investment remains subdued amid policy uncertainty. Until clearer trade paths emerge, private sector spending may stall.

External headwinds like elevated tariffs and possible geopolitical shocks—especially in global trade—could continue dragging on growth.

Conclusion

Yes, Q2 delivered a 3% GDP rebound and lower inflation, but the shine is narrow. Beneath the surface, the U.S. economy remains fragile—growth is under pressure, driven more by short-term trade mechanics than genuine domestic momentum. The next few months will be critical: sustained consumer demand and clearer investment signals will determine if this “bounce” turns into broad-based expansion—or fades into the backdrop of a cautious, slowing economy.