In the context of virtual currency black and grey market money laundering, we often hear a term: fourth-party payment.

What is fourth-party payment? In practice, how does the black and grey market launder money through fourth-party payment platforms? Today, let's explore this together.

What is fourth-party payment?

Before understanding fourth-party payment, let's first look at how first-party payment to third-party payment works.

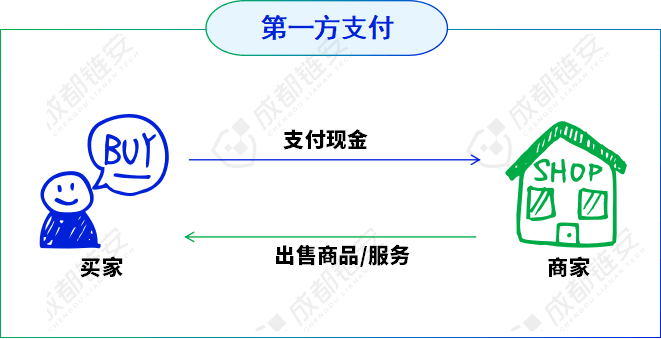

01 First-party payment:

First-party payment refers to cash payment. The buyer and seller directly settle in cash, exchanging cash for goods, without any intermediary involved in the transaction.

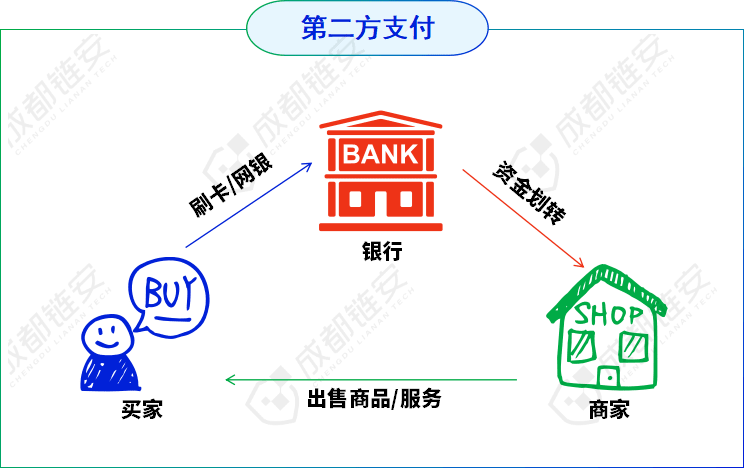

02 Second-party payment:

Second-party payment refers to payment methods relying on bank accounts (e.g., UnionPay POS card swiping, online banking transfers, remittances, etc.). The buyer and seller conduct transaction fund transfers through banks, with the security of funds guaranteed by the banking system. Essentially, the bank acts as a fund intermediary, completing the fund transfer between the buyer and seller through its own clearing system or the central bank's clearing system.

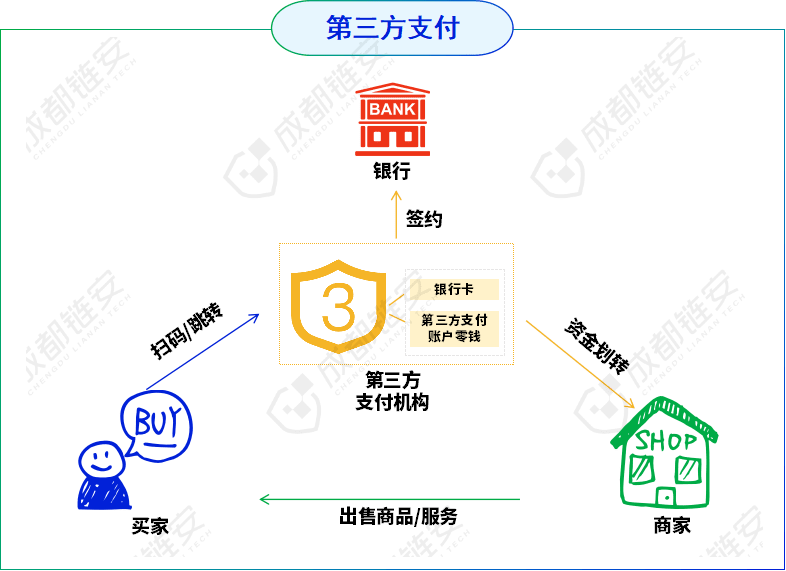

03 Third-party payment:

Third-party payment refers to a network payment model conducted through non-bank third-party payment institutions, which has become increasingly popular with the development of online shopping and mobile payments, such as Alipay, WeChat Pay, and Cloud Flash Pay. Third-party payment institutions must legally obtain a (payment business license) (i.e., 'payment license').

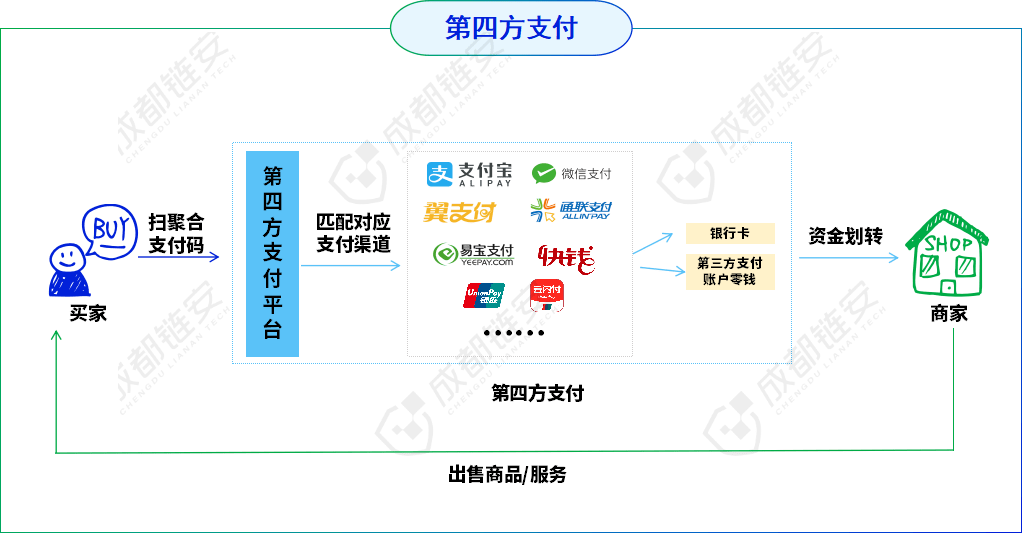

04 Fourth-party payment:

Fourth-party payment is an integrated payment service developed based on third-party payment, which combines various payment services from banks, third-party payments, etc., through technological means. Common integrated payment products include aggregated QR code payments, smart POS, QR code scanners, and QR code boxes.

In our country, legal fourth-party payment (registered as an acquiring outsourcing service institution by the China Payment and Clearing Association, and the 'business type' is integrated payment technology service, the provided payment service can be considered legal fourth-party payment) can only act as an 'acquiring outsourcing institution' for third-party payment institutions and must not engage in core businesses such as qualification review, contract signing, fund settlement, etc.; it must not handle settlement funds for designated merchants in any form or engage in or indirectly engage in fund settlement.

While improving payment efficiency, fourth-party payments are also exploited by criminals, who build illegal fourth-party payment platforms to launder money for upstream crimes such as online gambling and telecommunications fraud.

How does illegal fourth-party payment launder money?

Fourth-party payment platforms typically rely on third-party payment platforms (such as Alipay, WeChat Pay, etc.) for fund settlement, but they do not need to obtain a payment license to operate. This low threshold allows illegal actors to quickly establish illegal payment channels for money laundering activities. The fourth-party payment platform acts as an 'intermediary' in the money laundering chain, providing fund settlement services for upstream crimes (such as online gambling, telecommunications fraud, and the spread of obscene videos). Illegal actors use the fourth-party payment platform to 'launder' illegal funds, making the money appear as legitimate transactions to evade regulation and crackdown.

Typical modes of money laundering through illegal fourth-party payment platforms include:

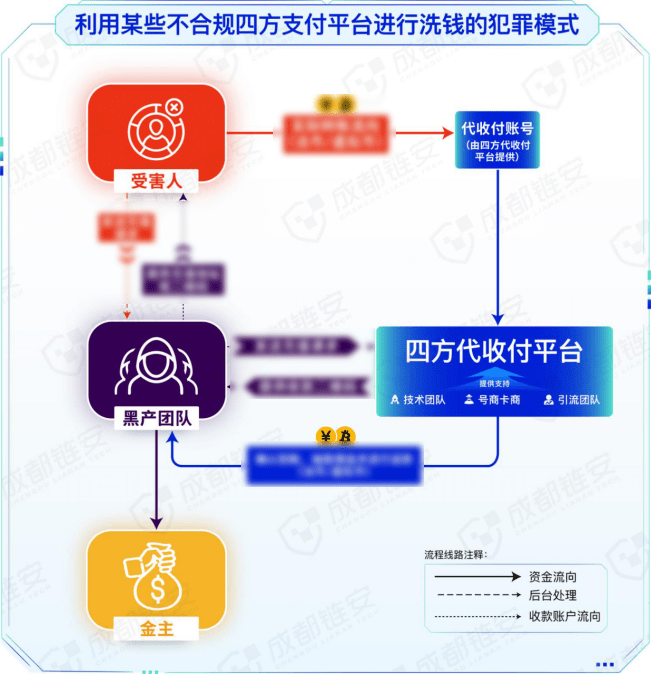

1. Fourth-party payment + fake merchant model:

Criminals establish illegal fourth-party payment platforms and then acquire a large amount of personal information from citizens through leasing, acquiring, and selling information in the black and grey markets, registering e-commerce, physical stores, and other merchant accounts, and opening third-party payment channels aggregated to their own fourth-party platform. When upstream crimes (online gambling, telecommunications fraud, pornography, etc.) need to launder money, they accept illicit funds through the controlled merchants' third-party payment channels and then transfer the funds to the accounts of the upstream criminals through refunds, settlements, and multiple layers of nested transfers between accounts of different industries.

2. Fourth-party payment + virtual goods model:

This model is essentially the fourth-party payment platform leveraging e-commerce platforms + empty package logistics for money laundering. Taking gambling as an example, criminals create fake e-commerce platforms or register online stores on legitimate e-commerce platforms. After completing the store registration, they will list fake goods at prices corresponding to the recharge amounts needed by online gamblers (without actually shipping anything), while also recruiting individuals to place fake orders through part-time jobs. The order fillers purchase goods in the store without having to pay, choosing to have someone else pay instead. The fourth-party payment platform has already been connected with the upstream gambling gang, so when gamblers recharge, they are actually paying for an order generated by the order fillers. Once the recharge is successful, the fourth-party payment platform informs the store that the payment is complete, and the store completes the entire money laundering process by falsely shipping the goods.

In addition to fake goods, there are also various low-price recharge services for online stores. These recharge services have a characteristic: they are more favorable than normal recharge prices, but the recharge amount does not arrive immediately and has a certain time delay (because real user recharge orders take time to match suitable upstream money laundering needs).

3. Fourth-party payment + score-running platform model:

This is currently one of the most typical models of money laundering through illegal fourth-party payments. Criminals establish illegal fourth-party payment platforms that connect with gambling, telecommunications fraud, pornography, and other criminal gangs, providing aggregated recharge channels; they connect with score-running platforms below, issuing recharge demands to achieve the laundering of illicit funds.

Taking gambling recharges as an example: criminals link the fourth-party aggregation payment interface to the recharge channel of the online gambling platform. When gamblers recharge, the fourth-party platform issues score-running tasks to the score-running platform, where score runners use their own bank cards, WeChat/Alipay collection codes to receive funds from gamblers. Finally, they transfer the received funds into legal currency or convert them into virtual currency to the corresponding channels to complete the laundering of gambling funds. Sometimes, the score-running platform may also directly transfer the deposit paid by the score runner to the corresponding channel.

In the fourth-party payment + score-running platform money laundering model, it is worth noting that:

1. Currently, in addition to using bank cards, WeChat/Alipay QR codes for score running, the use of virtual currency for score running is becoming increasingly common. Score runners submit bank cards and collection codes to the score-running platform for receiving payments, while also submitting their virtual currency platform account address and purchasing virtual currency to transfer to the score-running platform as a deposit. After receiving the score-running 'task', the score runner receives illicit funds and exchanges them for virtual currency to transfer to the designated on-chain address.

2. Some illegal fourth-party payments recruit score-running platforms directly to avoid risks, rather than building them themselves. The fourth-party payment platform only provides an interaction interface, connecting the score-running platform, gambling platform, telecommunications fraud, and other project parties, acting as a 'middleman' to profit from the price difference.

3. Score-running platforms have shifted to TG's guaranteed public group score running, using various vehicle teams to achieve the transfer and laundering of illicit funds;

4. In addition, some places equate score-running platforms with fourth-party payments, but in reality, there are still certain differences between the two.

Virtual currency fourth-party payment platform money laundering model:

With the rapid development of virtual currency, the use of virtual currency for money laundering in black and grey markets is becoming increasingly widespread. The virtual currency fourth-party payment platforms mentioned here are not strictly fourth-party payment platforms but rather various virtual currency wallet-like receiving platforms commonly seen in the black and grey markets. These platforms are widely used in current black and grey market money laundering.

These platforms are often named '✲✲ Wallet' or '✲✲ Pay', and they are not true virtual currency wallets nor genuinely decentralized. These platforms were initially created to facilitate fund transfers for gambling platforms, but they have now become funding settlement platforms providing virtual currency and legal currency exchange services for online gambling, telecommunications fraud, and pornography in the black and grey markets. Common platforms of this type include EBpay, OKpay, K豆 Wallet, GOpay, 波币 Wallet, TOpay, NO Wallet, kolpay, ULinx, 808 Wallet, 988PAY, etc.

Generally, these platforms will launch their own platform coins. For example, EBpay has issued a platform coin EB Coin pegged to the renminbi at a 1:1 ratio, where 1EB = 1 renminbi. The platform coin circulates and exchanges only within the platform, but some online gambling platforms can also directly use these platform coins for fund transfers.

Is it safe to buy coins on these platforms? What do you think? How do you know that the USDT you bought didn't come from underground banks or other shady channels?

Selling coins requires even greater vigilance; whether it is platform coins or USDT, the funds that the trading orders match for you may come from telecommunications fraud, online gambling, underground banks, etc. Once the transaction occurs, you may face the risk of card freezing.

Additionally, these platforms may attract users to buy USDT and other mainstream virtual currencies from legitimate channels at high prices, luring them to 'move bricks' to the platform. When users sell their USDT on the platform, they are essentially converting their clean funds into dirty money, helping criminals launder illicit funds. And because these platforms lack a real-name authentication mechanism, you have no way of knowing who you are actually trading with.

In reality, there are many cases of users being card-frozen and asked for refunds after selling coins on these platforms. Initially intending to earn a bit of profit, they ultimately became accomplices in black and grey market money laundering.

It is worth mentioning that after users recharge to these black and grey market platforms from wallets, the operations within the platform cannot be tracked on the chain for fund flow and information, similar to the black box of exchanges, and the virtual currency that users recharge ultimately goes to the platform's official wallet address.

In recent years, to evade crackdowns and tracking, the methods of money laundering in black and grey markets have continuously evolved, with new money laundering techniques emerging: from offline to online, and then to a combination of online and offline (such as various cash withdrawal laundering); from bank card money laundering to virtual currency, score-running platforms, fourth-party payments, underground banks, and various combined methods.

In this article, we briefly introduce some typical money laundering models of fourth-party payment, hoping to help everyone understand such money laundering methods. In practice, the means of money laundering through fourth-party payment platforms may be more complex and diverse, with longer and more hidden laundering chains that are harder to detect and combat.