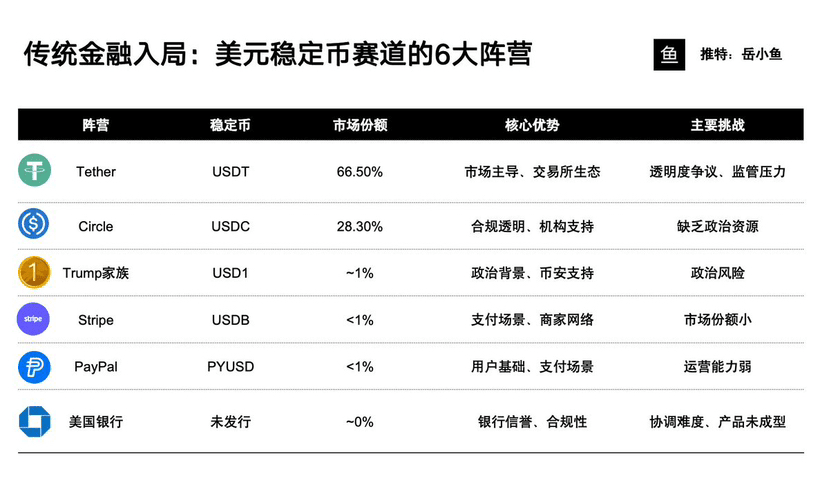

With the implementation of the US stablecoin bill (GENIUS), traditional finance has accelerated its entry, and six major forces have already formed.

The largest force is Tether, which issued USDT.

Tether has aligned with Secretary of Commerce Raimondo.

This camp also includes Bitfinex, Cantor Fitzgerald (former CEO was Secretary of Commerce), CEP (son of the Secretary of Commerce + SoftBank investment), and BitDeer (Tether holds 25.5%).

USDT has a market value of $150 billion, a market share of 66.5%, and has already occupied an absolute dominant position in the market.

The second major force is the Coinbase and Circle consortium.

They haven't relied on any political resources, but the future breakthrough point lies in scenario resources.

For example, Meta itself is not a financial company and cannot issue stablecoins, so it is negotiating cooperation with Circle, initially using Instagram as a pilot for small tips using stablecoins.

Circle's USDC has a market value of $61 billion, with a market share of 28.3%, making it the largest compliant stablecoin.

The third major force is the USD1 issued by the Trump family.

Abu Dhabi royal family MGX sovereign fund and Binance are also in this camp.

Initially, MGX invested $2 billion in Binance, all paid with the stablecoin USD1 issued by the Trump family.

Moreover, USD1 was first launched on Ethereum's Uniswap and BNB chain's Pancake.

This group's political power is the strongest, but the implied political risk is also the greatest.

The fourth major force is Stripe, which issued the USDB stablecoin after acquiring Bridge.

Stripe is the largest traditional payment solution provider in the world, thus having a strong advantage in payment scenarios.

The fifth major force is PayPal, which issued PYUSD.

PayPal has a large user base, but insufficient promotion.

It was previously popular on the Solana chain for a while, even attracting users with high dividends of 15% to 20%.

However, over the years, they have only generated $900 million, which seems to indicate they are not very good at operations.

The sixth major force consists of large American banks like JPMorgan, Citibank, Wells Fargo, as well as Zelle, similar to Alipay in the U.S., forming an alliance to issue a stablecoin together.

The advantage of the top banking alliance lies in its high credibility, while the disadvantage is the difficulty in coordination.

What will the future market landscape of the stablecoin sector look like?

In fact, the market landscape can be benchmarked against exchanges: exchanges can be divided into offshore and compliant, just as stablecoins are divided into offshore stablecoins and compliant stablecoins.

USDT is undoubtedly the leader in offshore stablecoins, while USDC is the leader in compliant stablecoins.

So, does this mean that other stablecoins have no opportunity?

In fact, in different countries and regions, as well as different business fields, many 'local leaders' similar to 'local tyrants' will emerge, such as the Hong Kong dollar stablecoin and the Stripe stablecoin in e-commerce.

These local leaders are like small tentacles, infiltrating digital dollars into various peripheral regions and niche business scenarios.

The future stablecoin market will definitely see a 'hundred coin battle'; we can look forward to the development of stablecoins.