The outlook for the crypto market in the second half of 2025 is positive, primarily driven by better-than-expected economic growth, corporate crypto adoption, and regulatory clarity.

Summary of key points:

· The trend of companies financing the purchase of crypto assets with leverage may trigger systemic risks in the medium to long term, such as forced selling or motivation-driven selling, but we believe short-term risks are still controllable.

· The regulatory environment in the U.S. is undergoing positive changes, stablecoin legislation is advancing, and discussions are ongoing regarding the crypto market structure bill.

Our constructive outlook for the crypto market in the second half of 2025 is based on several core factors: a more optimistic U.S. economic growth outlook, the Federal Reserve potentially lowering interest rates, increased corporate adoption of cryptocurrencies, and clearer U.S. regulations.

Although there are still some potential risks, such as a steepening U.S. Treasury yield curve and selling pressure triggered by listed crypto instruments, we believe these risks are manageable in the short term.

We believe there are three key themes in the crypto market for the second half of the year:

· Improved macro outlook: The risk of an economic recession in the U.S. has clearly decreased, and overall growth momentum has strengthened;

· Companies adopting crypto as an asset allocation tool: while it may lead to systemic risks in the long term, it creates strong demand in the short term;

· Regulatory pathways are becoming clearer: Especially the progress of stablecoin and crypto market structure legislation will profoundly impact the development of the crypto ecosystem.

Despite the risks, we still expect Bitcoin to maintain its upward trend. Altcoins' performance may depend more on individual factors.

For example, the SEC is reviewing multiple ETF applications involving 'in-kind purchase and redemption', staking, pooled funds, and single altcoin ETFs, and decisions are expected to be made by the end of 2025, which may reshape market structure.

Market outlook: Second half of 2025

We maintain our previous forecast—that the first half of 2025 will represent the bottom of the crypto market, while the second half may set a new historical high.

Although Bitcoin rebounded at the end of May, we still believe there may be further upside in the next 3-6 months.

In our view, the macro disturbances caused by trade tariffs are approaching an end. Looking ahead, as the government promotes more market-friendly fiscal legislative plans (expected to be completed by late summer), risk appetite is likely to warm up.

However, one risk worth noting is that this fiscal spending bill may cause the U.S. Treasury yield curve to steepen, especially in the 10-year to 30-year segment.

In fact, due to concerns about the deficit, the yield on 30-year U.S. Treasuries rose to 5.15% in May, a 20-year high. This may exacerbate financial tightening and increase financing costs for companies and consumers, thereby weakening the growth foundation and affecting market confidence.

If long-term yields rise too quickly, it could lead to volatility in the stock and credit markets, especially if investors begin to doubt whether the U.S. can sustain a high deficit without triggering systemic risks.

This development path will challenge the current mainstream narrative of 'front-loaded fiscal stimulus' or force the market to reassess risk assets in advance, especially if economic data or Federal Reserve policies do not meet expectations.

However, at the same time, we believe this may also benefit store-of-value assets like gold and Bitcoin, especially against the backdrop of a weakening dollar dominance.

Three major themes

Theme 1: The shadow of recession has significantly weakened

The trade disturbances at the beginning of the year sparked concerns that the U.S. might fall into a technical recession, especially after the annualized quarter-on-quarter decline of 0.2% in GDP in the first quarter of 2025.

At that time, mainstream media outlets, including The Economist and The Wall Street Journal, issued warnings such as 'Trump's tariff war may trigger a global recession' and 'Trump's reciprocal tariffs may ignite a U.S. recession.'

However, we remain relatively optimistic about the second half of the year. We believe the 'degree' of recession is key; a technical recession may not necessarily have a profound impact on the market unless macro momentum continues to deteriorate.

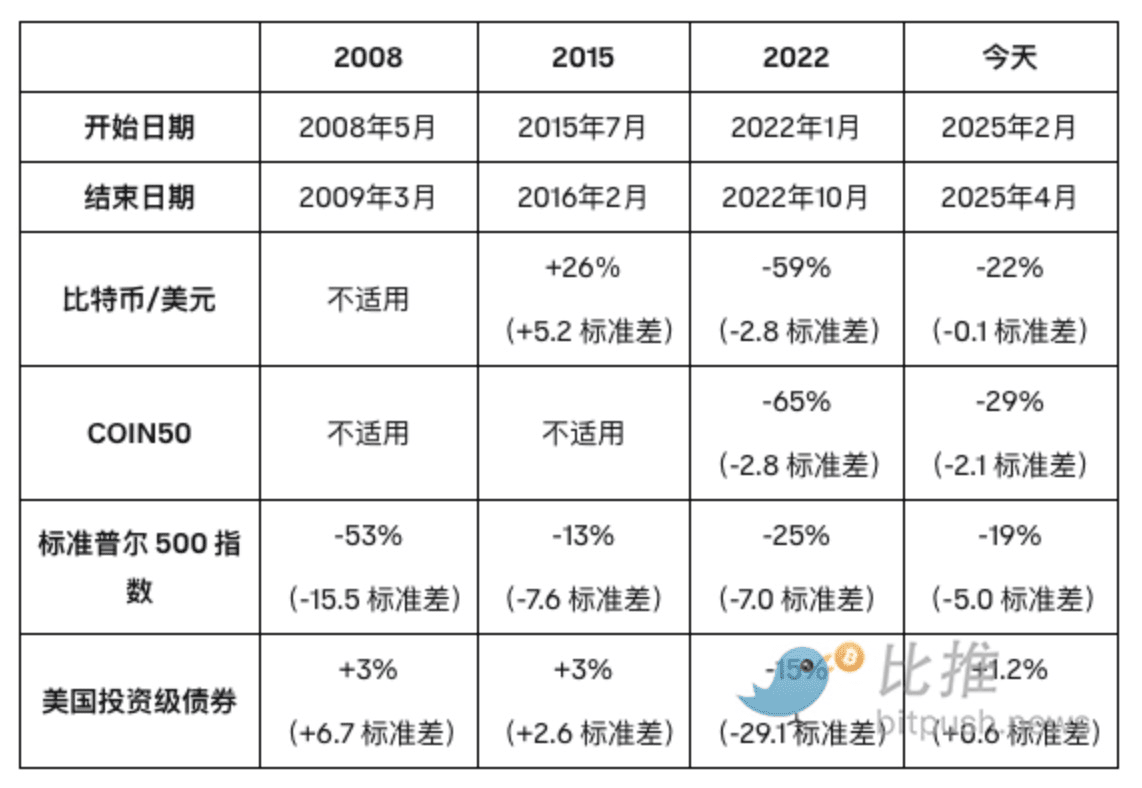

For example, during the 2008 financial crisis, the U.S. stock market fell by 53%, while the 'recessions' of 2015 and 2022 were much milder (see the table below). Additionally, the Atlanta Fed's GDPNow forecasting model has been significantly upgraded from a 1.0% quarter-on-quarter growth rate in early May to 3.8% as of June 5, reflecting an improvement in economic data.

We therefore judge that even if a slowdown occurs in 2025, it is more likely to be a mild recession or a 'soft landing', rather than a severe recession or stagnation scenario.

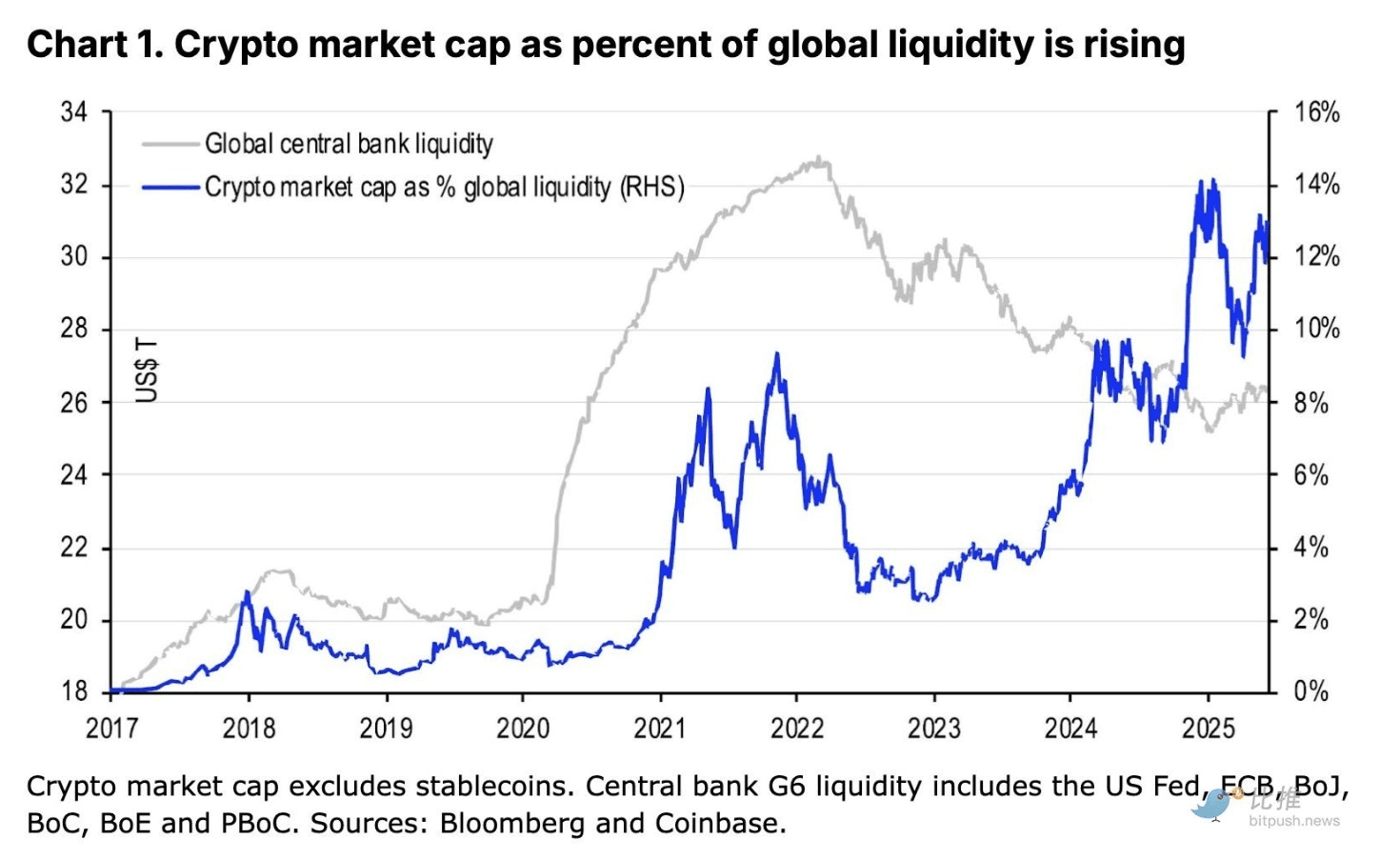

Even so, the market impact may be limited to specific sectors rather than a broad sell-off. Coupled with the expansion of the M2 money supply in the U.S. and the global central bank balance sheets, we believe the likelihood of asset prices returning to 2024 levels is low. The upward trend of Bitcoin is expected to continue. Furthermore, most 'tariff shocks' have already been absorbed by the market, although some individual policies (such as the expiration of the reciprocal tariff suspension on July 9) remain undecided, the overall marginal risk is weakening.

Comparative analysis of various asset cyclic downturns (from peak to trough):

Theme 2: The wave of corporate adoption of crypto assets is coming—Is the 'Replica Strategy' here?

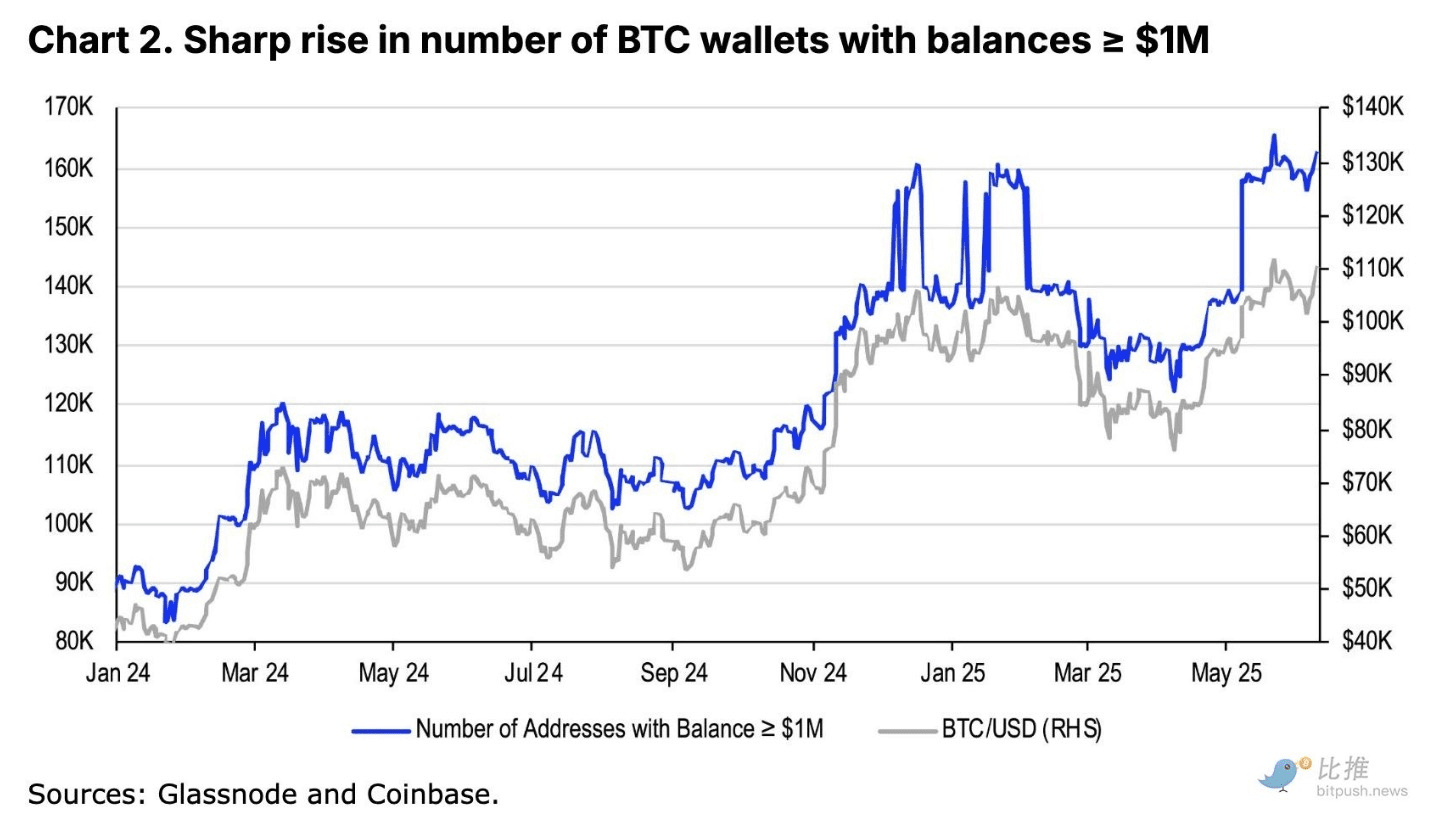

Currently, there are about 228 listed companies worldwide holding a total of 820,000 BTC. Among them, about 20 companies (and another 8 holding ETH, SOL, XRP) use a leverage financing model similar to 'Strategy (formerly MicroStrategy)'.

The new FASB accounting standards effective from December 15, 2024, will significantly promote companies to include crypto assets on their balance sheets.

Previously, U.S. Generally Accepted Accounting Principles (GAAP) only allowed companies to account for impairment of crypto assets on their balance sheets, while appreciation could only be reflected upon sale.

The new regulations allow for fair value disclosure, making financial statements more comparable and providing higher transparency for CFOs and auditors.

However, we observe that a new trend is forming—more and more listed companies are themselves 'coin-holding machines', with their core business being the purchase of crypto assets.

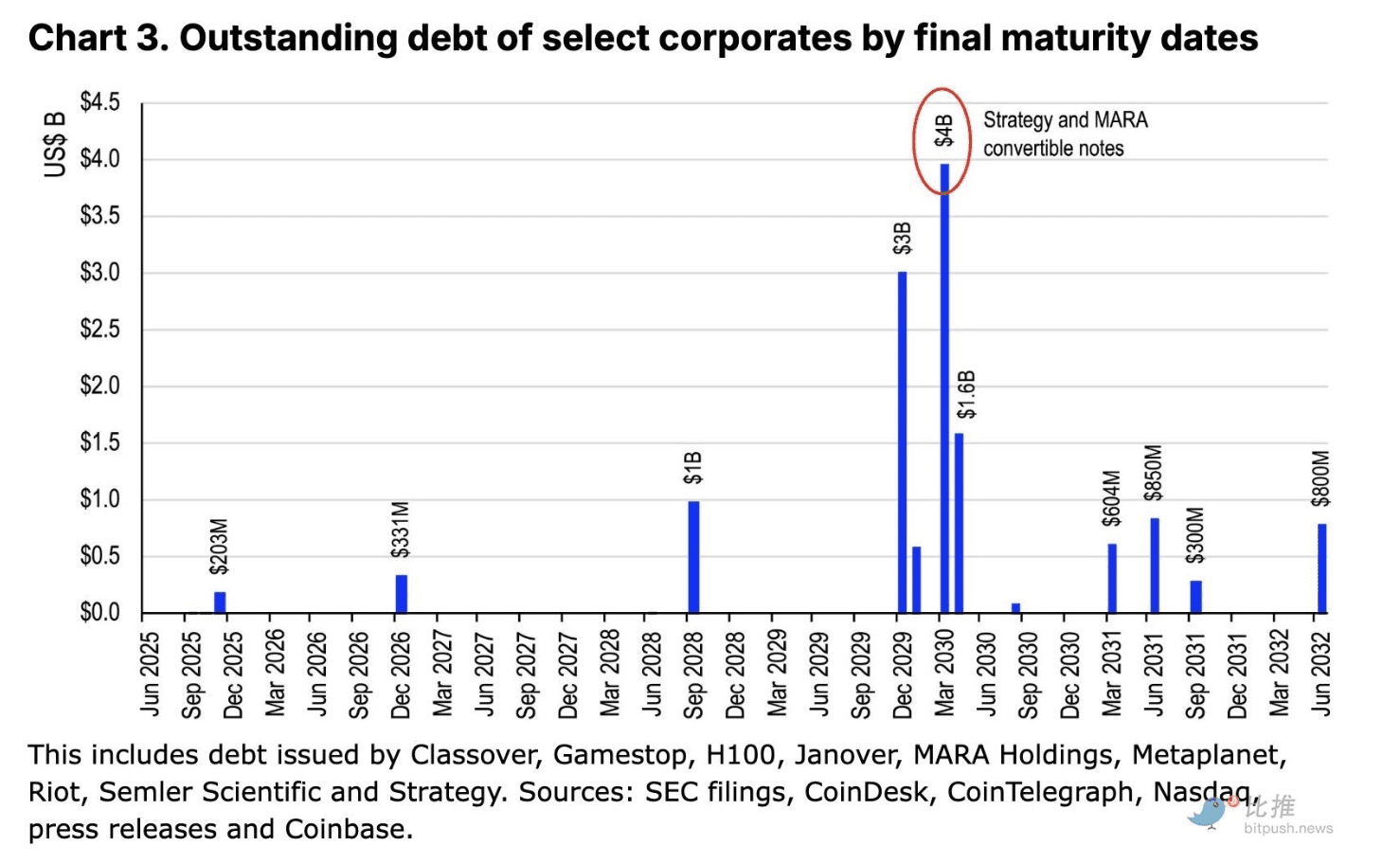

They finance their coin purchases through the issuance of stocks or convertible bonds, with market capitalizations far exceeding their net assets. Representative cases include Strategy, but now more imitators have emerged.

Two potential systemic risks:

· Forced selling:

Many PTCVs (listed crypto asset carriers) rely on convertible bonds for financing, and if the price of the underlying coins falls, or if the market environment deteriorates and refinancing fails, these companies may have to sell their crypto assets to repay debts.

· Motivated selling:

If a PTCV suddenly sells assets for operational or cash flow management needs, it may trigger a chain reaction, spreading market panic and inducing a price crash.

Nevertheless, we believe that such risks are not sufficient to pose a significant shock to the market in the short term. First, most of the debt will not mature until 2029-2030 (for instance, Strategy's $3 billion convertible bonds have their first redemption period at the end of 2026 and formally mature at the end of 2029), thus reducing short-term selling risk. Secondly, the current loan-to-value ratio (LTV) is overall still healthy, and some large companies have the ability to avoid forced sales through refinancing.

Of course, as more companies adopt this strategy and debt matures, systemic risks remain worth monitoring in the long term. The 'corporate coin-holding model' of Strategy is also attracting more 'curious' executive teams, indicating that the trend of companies hoarding coins will continue into the second half of 2025.

Theme 3: Opening a new era of regulation

In the first half of 2025, U.S. crypto policy underwent unprecedented changes. The White House abandoned the old path of 'enforcement instead of regulation' and fully turned to support the development of the crypto industry.

We believe that stablecoin legislation is most likely to be the first to be implemented. Currently, the House of Representatives is advancing the STABLE Act, while the Senate is pushing the GENIUS Act, both of which have received bipartisan support.

On June 11, the Senate passed the GENIUS Act, sending it to the House for review. Both set reserve requirements, anti-money laundering compliance, bankruptcy protection, and consumer rights provisions.

The main divergence lies in:

· How to handle non-U.S. stablecoin issuers

· How to set regulatory thresholds

The White House is expected to complete the unified version of the bill for submission to the president for signing before Congress adjourns on August 4, which may lay the groundwork for subsequent market structure legislation.

The crypto market structure bill (CLARITY Act)

On May 29, 2025, the U.S. House Financial Services Committee officially proposed a draft of the Digital Asset Market Clarity Act (CLARITY Act), which is considered the most transformative legislation of the year.

The bill aims to clarify the regulatory boundaries of the SEC and CFTC regarding crypto assets, and to delineate regulation based on asset attributes (such as 'digital commodities' or 'investment contracts'). This bill builds on the FIT21 Act passed last year and requires the SEC and CFTC to jointly define key terms and continue rule-making, indicating that there is still room for evolution in regulatory division of labor.

We believe this will become the basis for future negotiations between the two chambers, but its complexity and uncertainty will be higher than that of stablecoin legislation.

ETF Progress Timeline

The SEC is facing about 80 crypto ETF proposals in 2025, covering:

· Multi-asset crypto index funds (Bitwise, Franklin, Grayscale, etc.): Decision as early as July 2;

· In-kind purchase/redemption mechanism: Results may come in July, but the latest by October;

· Staking inclusion: Limited by the transparency of the 6c-11 clause, the SEC may make decisions in advance;

· Single altcoin ETF: Most application deadlines are in October, and the SEC is expected to use the entire review period.

Conclusion

We are optimistic about the crypto market outlook for the third quarter of 2025, thanks to a relatively optimistic U.S. economic growth outlook, potential Federal Reserve interest rate cuts, rising corporate adoption of cryptocurrencies, and increased regulatory transparency in the U.S.

Although there are risks such as a steepening U.S. Treasury yield curve and potential selling pressure from PTCVs, they remain within controllable limits in the short term. We believe the upward trend of Bitcoin will continue, although the performance of altcoins will need to be assessed based on individual projects.