The underlying logic of RWA:

The core of RWA is to map real assets as digital tokens through blockchain technology, and its implementation path includes:

Asset evaluation and certification: Professional institutions verify asset value and legality (such as real estate valuation, bond credit ratings)

Asset digitization: Converting asset ownership or income rights into tokens through smart contracts (e.g., BlackRock's BUIDL fund tokenizing U.S. Treasuries)

On-chain circulation and profit distribution: Tokens can be traded on decentralized exchanges, and profits (such as rent, interest) are automatically distributed through smart contracts.

The core of the RWA financing model is to tokenize real assets through blockchain technology, generating digital assets that can be traded on decentralized platforms. The main process is as follows:

Asset selection and evaluation: Selecting assets with clear value or stable cash flow, such as properties, receivables in supply chain finance, or intellectual property. Professional institutions evaluate the assets to ensure the reliability of the tokenization basis.

Tokenization: Using blockchain (such as Ethereum, Solana) to split asset ownership or income rights into digital tokens (such as ERC-20, NFT). Smart contracts define the rights allocation and trading rules of the tokens.

Compliance handling: Through KYC (Know Your Customer), AML (Anti-Money Laundering) verification, combined with the STO (Security Token Offering) framework, to ensure compliance with regulatory requirements.

Issuance and trading: Tokens are issued through decentralized platforms (like Uniswap) or dedicated markets, where investors purchase them using digital currencies (like USDT, ETH). Tokens can circulate in DeFi protocols or exchanges.

Profit distribution: Income generated from assets (such as rent, interest) is automatically distributed according to the proportion of token holdings through smart contracts.

RWA financing model three: RWA and digital currencies

The core role of digital currency

First, payment and settlement tools: Stablecoins (like USDC, JD-HKD) serve as a bridge between fiat currency and RWA, reducing cross-border transaction costs. For example, JD.com's Hong Kong dollar stablecoin JD-HKD connects RWA and digital yuan interactions.

Second, collateral and liquidity tools: RWA tokens can serve as collateral in DeFi protocols, for example, MakerDAO includes U.S. Treasury tokens in the DAI stablecoin collateral pool to enhance its stability.

Third, governance and incentive mechanisms: Project governance tokens (such as ONDO) enhance user participation through mechanisms like staking and fee discounts.

The development of digital currencies has gone through five periods.

First period: 1976-1982, the budding period.

Second period: 1982-2010, the growth period. In 1982, the Byzantine problem was proposed, in 1985 the elliptic curve cryptography was introduced, in 1997 the HashCash proof of work algorithm appeared, and in 2008, Satoshi Nakamoto proposed the theory of Bitcoin and created software to produce Bitcoin.

Third period: 2011-2017, the rapid development period. The development of Bitcoin has driven the issuance of more digital currencies. In 2011, Litecoin was born, in 2012, Ripple was issued, and in 2013, Ethereum was launched.

Fourth period: Rational and comprehensive development began from 2017 to 2024. Different countries have different policies, with no absolute prohibitions or permits.

Fifth period: From November 5, 2024, onwards, after Trump successfully campaigned, the strategic reserve Bitcoin policy began, opening a new era for Bitcoin, while tariff policies stimulated the circulation and global use of digital currencies.

Digital currency has gained increasing attention for its decentralization, anonymity, strong circulation, security, and traceability. The price of digital currency has also risen sharply and gradually become a reserve asset for some countries' central banks.

🌐 Understanding the inherent value logic and development path of digital currencies

Central banks begin to research and issue digital currencies, and the industry starts to build token issuance, stablecoin, and fiat currency exchange mechanisms. Tokens are issued based on stablecoins, and exchange between stablecoins and fiat currency establishes a connection between tokens and fiat. As fiat digitalization becomes widespread, fiat can directly replace stablecoins, providing a solid foundation for token issuance.

RWA financing model four: RWA and legal regulation

RWA is closely related to digital currencies. Throughout the development of digital currencies, various frauds have emerged, posing problems for financial stability and investor protection.

The strengthening of regulation is a long-term benefit for both the RWA sector and the entire cryptocurrency field. The stronger the legal regulation, the higher the safety of the industry, but with that comes fewer opportunities for ordinary people to make money.

Why is regulation necessary? How large is the group behind it?

Global cryptocurrency user count: As of 2024, the global number of cryptocurrency users reached approximately 659 million, accounting for about 8.3% of the global population.

Growth rate: From 2023 to 2024, the number of users grew by approximately 34%, indicating the rapid popularization of cryptocurrency worldwide.

Regional distribution:

Asia: User count increased from 268.2 million to 326.8 million, an increase of about 21.8%.

North America: User count is 72.2 million.

Other regions: User count has also shown significant growth, especially in developing countries.

It is precisely because of the large volume of funds and the number of users involved that regulation has emerged to better prevent and avoid capitalists manipulating the market, allowing retail investors to leave in tears. Ultimately, regulation is still a collaborative community of interests.

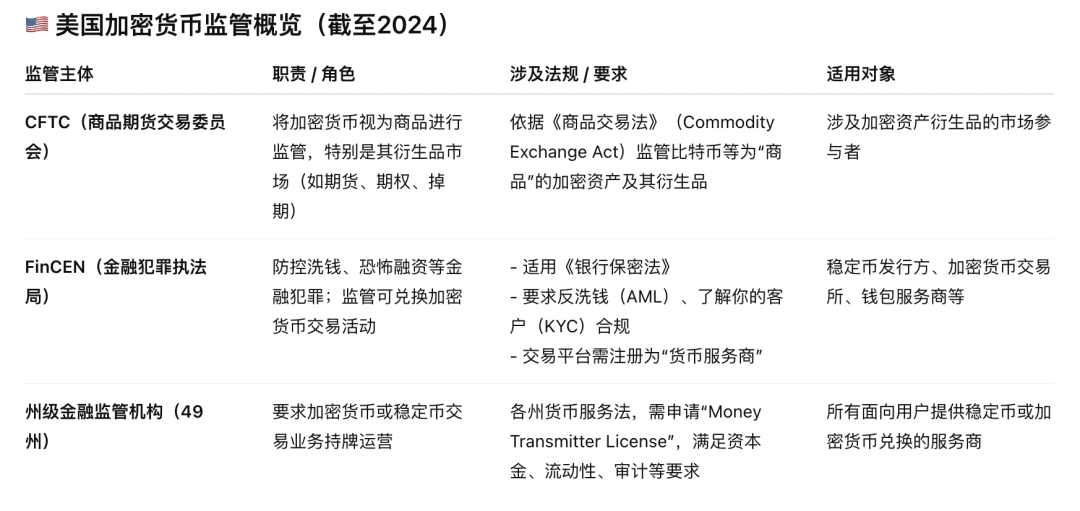

How does the U.S. Securities and Exchange Commission (SEC) regulate?

The U.S. regulation of cryptocurrency (cryptocurrency assets) is implemented under the existing financial regulatory framework by both federal and state levels, resulting in multi-faceted regulation.

The U.S. Securities and Exchange Commission (SEC) delineates the regulatory scope of whether cryptocurrency assets fall under 'securities' through regulatory enforcement, while continuously expanding its regulatory authority over cryptocurrency assets through administrative enforcement.

First: Civil lawsuits against cryptocurrency companies and their founders and executives for violating U.S. securities laws, determining jurisdiction through court rulings;

Second: Administrative penalties against cryptocurrency companies and their founders and executives for violating U.S. securities laws, determining jurisdiction through court rulings.

How does Hong Kong handle digital currency regulation?

Hong Kong is also at the forefront of digital currency regulation. As an international financial center, Hong Kong has always been a demonstration zone for the application of cutting-edge financial technology in China during the global digitalization process. The Hong Kong Monetary Authority places great importance on the formulation and management of cryptocurrency regulatory policies.

The Ensemble project builds a sandbox experiment, initially determined to focus on four areas: 'fixed income and investment funds, liquidity management, green and sustainable finance, trade and supply chain financing', with distribution handled by participating institutions in the working group.

Through the implementation of sandbox projects, the aim is to verify the interoperability between wCBDC, tokenized currencies, and tokenized assets, and to conduct end-to-end testing of tokenized asset transactions in real business scenarios to promote relevant standard formulation, supporting the development of the tokenized market in Hong Kong.

What are the standards for regulation in Hong Kong?

In terms of regulation, the Hong Kong Monetary Authority issued comprehensive regulatory standards for authorized institutions selling and distributing tokenized financial products in February 2024. These standards:

The implementation of regulatory measures in Hong Kong and the landing of sandbox projects, especially the successful issuance practices of RWA, have made Hong Kong the preferred place for mainland companies to issue RWA.

Mainland China's regulatory authorities, especially the People's Bank of China, have always attached great importance to the development of financial technology and digital currencies. Since 2020, the central bank has taken the lead in launching the digital yuan (e-CNY) and has continuously expanded its pilot applications in various scenarios such as transportation, retail, and government payments, promoting the deep integration of the digital economy with the real economy.

At the same time, due to considerations of maintaining national financial security and preventing systemic risks, the state has defined activities related to virtual currency trading, speculation, issuance, and pricing as illegal financial activities, and has comprehensively banned activities such as 'mining'. Under this regulatory framework, RWA projects involving the tokenization of real assets have no legitimate space for development in mainland China.

RWA financing can choose either tokenized financing or asset-backed lending, but regardless of the issuance model, it cannot do without digital currency.

In tokenized issuance financing, it is necessary to choose different types of stablecoins, digitize physical assets, borrow stablecoins against collateral, rely on these stablecoins to issue tokens, and obtain the required fiat funds through token sales.

Asset-backed lending also requires choosing the corresponding stablecoins, digitizing physical assets, borrowing stablecoins against collateral, and then using these stablecoins as collateral to borrow fiat funds directly from the Web3.0 currency market.

The future of RWA relies on a healthy and regulated digital currency market. How to regulate digital currency, ensuring the innovative development of Web3.0 while protecting investor interests and maintaining financial security, presents new challenges for traditional regulatory authorities.

Regarding the content on (New financing model based on Web3.0 - RWA sector), I have divided it into three parts for updates, so that readers can better understand in detail.

Next, I will update the final piece:

(New financing model based on Web3.0 - RWA sector [Part 2])

Welcome to follow: The most in-depth analysis of the cryptocurrency industry

Finally: Many of the viewpoints in the text represent my personal understanding and judgment of the market, and do not constitute advice for your investments.