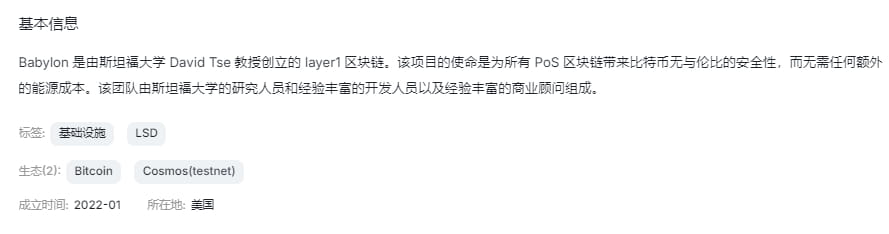

1. From Stanford Laboratory to Crypto Casino: Babylon's Crazy Fundraising Campaign

When Stanford professor David Tse wrote that paper (The Spacetime Fold Theory of Bitcoin Security) in 2023, he may not have realized that he would personally open a Pandora's box worth billions of dollars. This project, which combines Bitcoin fundamentalism with the essence of Wall Street's harvesting, completed a magical leap from academic paper to Binance exchange in two years—just like transforming Einstein's theory of relativity directly into a Las Vegas slot machine.

Babylon's core narrative is a perfect patchwork: with the left hand holding the faith flag of Bitcoin as "digital gold" and the right hand wielding the scythe of DeFi liquidity mining. They claim to turn 21 million dormant Bitcoins into the super bodyguards of the POS chain, but in reality, they're building a financial arena that allows the house to short retail investors at zero cost. The "illusion of security" created by the 57,000 staked Bitcoins is fundamentally no different from the "illusion of wealth" built by chips in a casino.

The funding history of this project is enough to make traditional VCs blush: from the $8 million seed round in 2022 to the $70 million led by Paradigm in 2024, nearly $100 million in four rounds of financing in three years perfectly illustrates the unique funding model of the crypto world, where "using a PPT to convince investors with real money suffocates dreams."

Especially remarkable is the $5.3 million investment from BingX Labs in January 2025—just three months before the token TGE, it can be called the ultimate performance art of the "pass the parcel" game.

2. The Fatal Flaw of Token Economics: The Wealth Harvesting Machine Written in Code

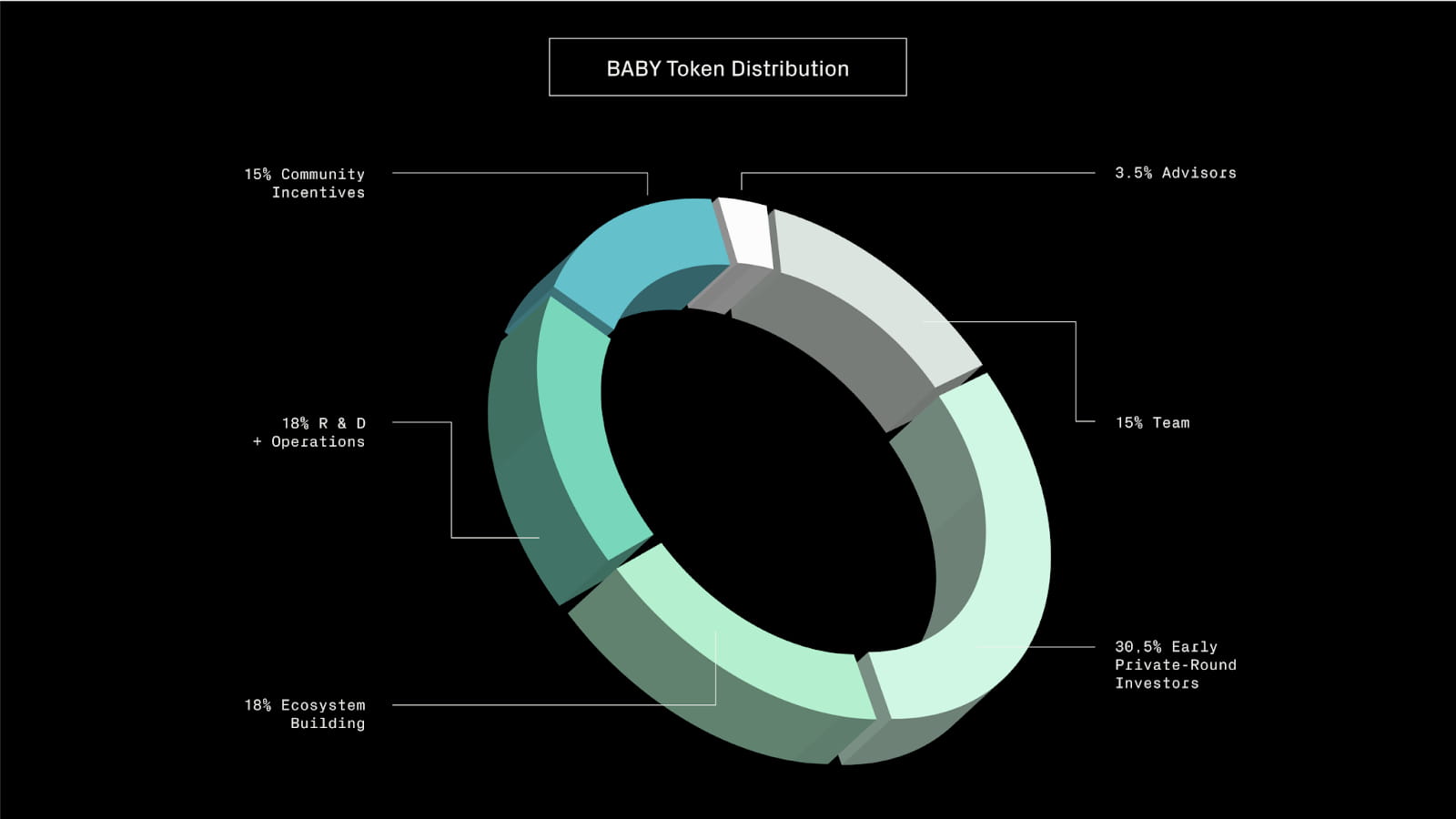

The distribution plan for the BABY token is a textbook example of "robbing the poor to enrich the rich": 30.5% to private equity firms, 15% to the team, 3.5% to consultants, while only 15% is truly left for the community.

This is equivalent to the house taking 53% of the chips before the game starts, while beautifying it as "long-term lock-up."

Even more magical is that the project team packaged this blatant wealth plunder as "preventing market abuse"—just like bank robbers claim that blowing up the vault is to protect depositors' funds.

The current price of $0.09 seems cheap, but it actually hides a mystery. Based on a total supply of 10 billion, the FDV has reached $900 million, exceeding the valuations of most second-tier public chains. However, the project's confusing "unlimited issuance" clause is the real killer: the 8% inflation rate in the first year is merely an appetizer, while the "community governance decides inflation" starting in the second year is essentially an infinite money printer tailored for the house.

While you are calculating staking returns, the project team is adjusting the nuclear button for "token dilution" in the background.

The design of the staking mechanism is filled with dark humor: the "flexibility" of a 50-hour redemption period creates a perfect arbitrage window compared to Bitcoin's 7-day lock-up period.

This design of time difference is equivalent to setting a hidden rule in the casino where "the house can change the speed of the roulette wheel at any time." The so-called "annualized APY of 200%" is merely bait to attract gamblers to increase their bets—when everyone wants to earn interest, the house is always focused on your principal.

3. Listing is the Pinnacle: A Carefully Planned Liquidity Massacre

A chain of short positions exploded on Bybit, with prices plunging to $0.159.

The Binance launch drama on April 10 is a pinnacle of contemporary financial performance art. The concentrated selling of airdrop tokens and the precise control of market makers perfectly replicated the "penny stock" manipulation techniques in (The Wolf of Wall Street). The 40% instant surge that made retail investors cheer was merely a "stress test" by the house to gauge market sentiment—just like how a butcher gently caresses the lambs before slaughter.

The pre-market pricing mechanism of $0.07 is essentially a psychological anchoring trap. When retail investors think they have found a bargain, the house has already established short positions in the futures market. The design of 22.9% initial circulation is particularly clever: it creates a false appearance of "circulation scarcity" while leaving ample ammunition for subsequent dumping.

That drop which turned a $200 million market cap to ashes was merely an appetizer for the capital predators.

Observing on-chain data reveals a more bloody truth: within 24 hours after the airdrop release, $21 million worth of Bitcoin was rapidly unstaked. This is equivalent to a gambler rushing to the payout window right after receiving their chips—smart money is always three steps ahead of retail investors. And the so-called "top exchanges all settling in" is merely hanging a five-star hotel sign over the slaughterhouse.

4. Future Trend Projection: A Chaotic Battle in the Crypto West

In the short term, $0.08-0.12 will become a battlefield for bulls and bears. The house needs to complete the turnover of chips within this range: it cannot fall below the cost price for institutions to avoid them being liquidated, while also creating enough volatility to attract leveraged gamblers. Especially after the Binance contract launch, a classic harvesting combo of "spot market decline + futures price spike" is expected.

Those retail investors who fantasize about replicating EigenLayer's trajectory will soon find themselves as "extras in someone else's script."

The biggest variable in the medium term is the collective hysteria of the Bitcoin ecosystem. If the Bitcoin L2 narrative can survive for another six months, Babylon might pull off another two waves with the story of "staking as a service."

However, given the current TVL growth rate, this castle in the air built on 57,000 staked Bitcoins is as fragile as an empire built on matchsticks. More critically, the 66% of tokens reserved by the project team hang like the sword of Damocles, potentially causing a nuclear-level sell-off at any time.

In the long run, the ultimate fate of this project has long been written in the white paper: either become the AWS of the Bitcoin ecosystem or fall into a code-based Ponzi scheme.

But given the current team's greedy design of token economics, the latter's probability exceeds 90%. When staking returns struggle to cover inflation losses, the entire system will enter a "death spiral"—just like P2P platforms that maintain themselves by borrowing new to pay old, leaving only a mess and cries in the rights protection group.

5. The Ultimate Question: What exactly are we paying for?

When we peel away Babylon's glamorous exterior, we uncover a chilling truth: this project, which claims to "activate the security value of Bitcoin," is essentially creating a new type of financial parasite. The "security services" produced by staking Bitcoin are like putting makeup on a corpse—seemingly glamorous, but already rotten inside.

In this story, the Stanford professor becomes the casino designer, Bitcoin believers turn into lambs awaiting slaughter, and the lofty ideal of "decentralization" ultimately degenerates into a marketing gimmick for harvesting retail investors. Perhaps one day, when David Tse sips wine in his Silicon Valley villa, he'll chuckle at the K-line chart: "Look, these fools really believe that code can turn stone into gold."

The final chapter of this absurd drama has long been written: when the last buyer leaves the table, and when the staking of Bitcoin recedes like a tide, what remains are only the cold numbers from the exchange and the ever-burning flames of anger in the rights protection group. Meanwhile, the wolves of Wall Street have long taken their billions in spoils to the next hunting ground.