Just released the CPI data, 2.8%, a new low since last November.

Looking at the specific sub-data, rent, food, and oil have the largest weight in inflation.

This means that eggs in supermarkets are scarce and expensive, and rent is rising.

Overall, the CPI in February was lower than expected, but several lesser-known components were not included in the Fed's preferred metrics. As a result, forecasters expect the PCE inflation reading for February to be more robust, although this may change after Thursday's PPI release. The currently tracked core PCE inflation rate is +0.32%.

From another perspective: the U.S. is in a recession, CPI data below expectations is considered good news, increasing bets on the Fed cutting rates at least twice this year. All three major U.S. stock indexes opened higher. Currently, the U.S. economy is facing a triple bind of 'high debt, low growth, and strong inflation expectations.' Although the February CPI data injected brief confidence into the market, policy uncertainty, valuation correction pressure, and structural contradictions are intertwined, making it difficult for U.S. stocks to change the downward trend in the short term.

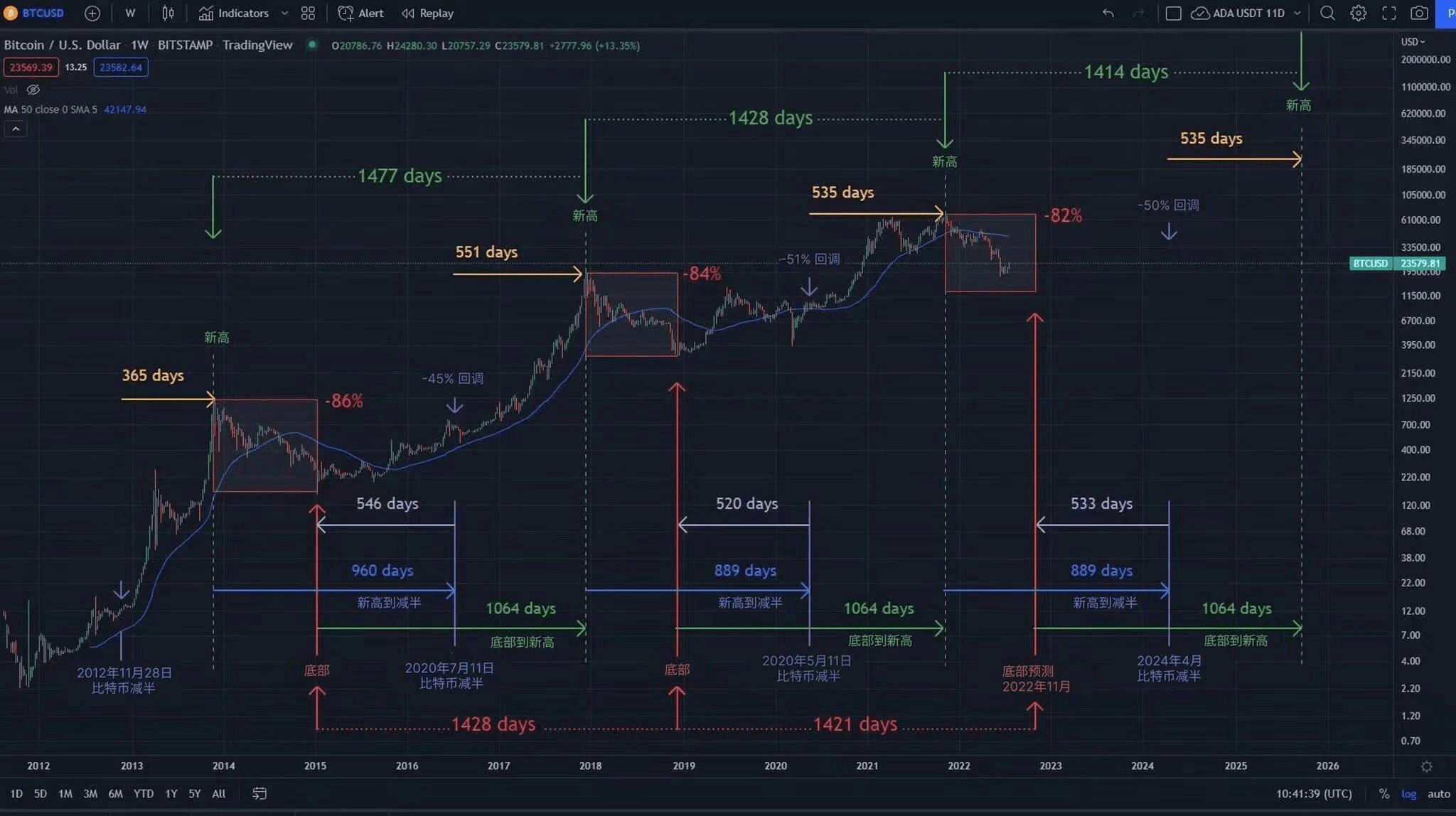

Finance is about speculating on expectations.

The market is swinging. The market will correct due to excessive optimism, leading to pessimism, while an excessively pessimistic market is rescued by the Fed, which then leads back to excessive optimism—this is the swing the market is in.

The bearish sentiment during this period marks that the washout has reached a low point, while brewing hope for the next stage.

Retail investor sentiment is low, with emotions hitting rock bottom, and the altcoin market has been declining for months—but this may be the prelude to a new round of opportunities.

Despite the market conditions seeming bad, I think this is more like a setup rather than an endpoint.