I don’t dare to sell. Many friends have this problem: [I made four transactions, and my bank card was frozen three times. I chose Alipay for the last time, but the system judged it as an abnormal transaction and Alipay was frozen again]

Purchasing cryptocurrency with legal currency is the first stop for most users to enter the Web3 world. Regardless of the type of deposit method, the user's funds and accounts should be safe, and the transaction method and platform need to be legal and compliant. The project party needs to obtain a remittance license locally and verify the user's identity before it can provide financial services such as deposits and withdrawals.

This article will discuss the types of deposit and withdrawal projects in the cryptocurrency market, regional legal regulatory requirements, and the status of major exchanges obtaining regulatory licenses.

Types of deposit and withdrawal projects

Generally, the channels for users to buy and sell cryptocurrencies are divided into over-the-counter trading and on-exchange trading.

The first difference is the distinction of venues. On-site transactions generally occur at a centralized exchange as a venue, like traditional stock exchanges. Off-site transactions do not occur at a centralized fixed location and can happen in various venues, such as through face-to-face trading or WeChat.

The second difference is the distinction of deposit and withdrawal objects. In on-exchange trading, the object of deposits and withdrawals is the exchange; users transfer fiat currency to the exchange, referred to as deposits, and withdraw fiat currency from the exchange, referred to as withdrawals. In off-exchange trading, the objects of deposits and withdrawals are other users. User A transfers fiat currency to another user B as a deposit; user A's withdrawal is another user C transferring to themselves as a withdrawal.

1. Over-the-counter trading

Over-the-counter trading (OTC) fiat deposit and withdrawal projects allow buyers and sellers to trade directly and eliminate intermediaries, but this is also a high-risk area for fraud, with two main models:

OTC counters, such as Kraken OTC. In the OTC counter model, the two parties to the transaction are clients in need of trading services and the OTC counter acting as the counterparty. This model has three major advantages in terms of deposits and withdrawals:

No trading slippage. By providing fixed quotes for large transactions, it avoids losses caused by slippage, bearing risks for customers in exchange for the possibility of profiting from better-than-quoted transactions.

More liquidity. OTC counters can execute transactions at the best prices across multiple liquidity platforms.

High privacy. Direct transactions with OTC counters allow customers to protect their privacy and avoid transaction information appearing in public order books.

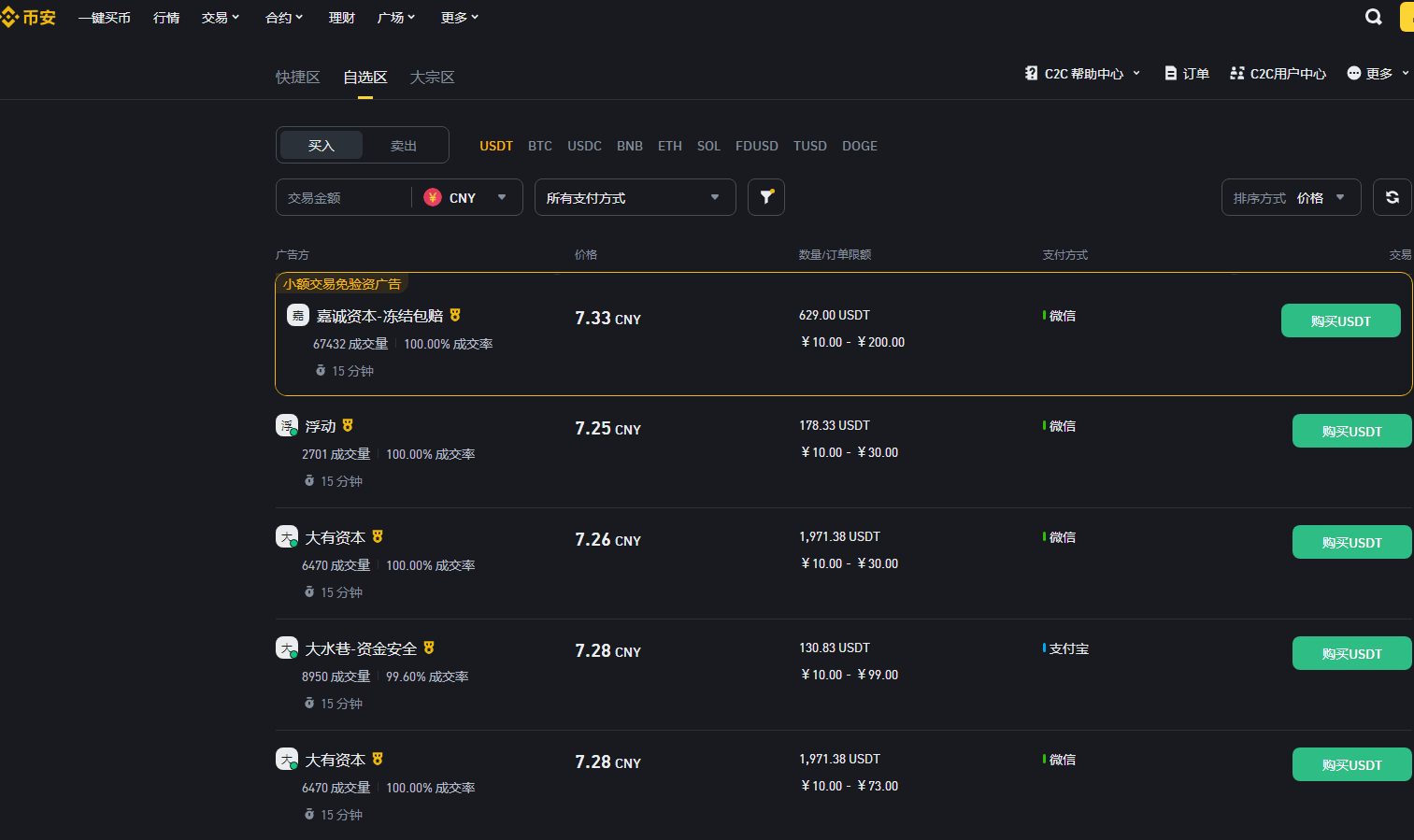

Customer-to-customer (C2C) trading platforms, such as C2C Trading. This refers to direct transactions between individuals for fiat deposit and withdrawal without intermediaries or third parties. The trading platform holds the digital currency assets of the buyer/seller until payment confirmation is received from the other party. The platform advises users to trade with certified merchants since all certified merchants have undergone careful scrutiny by the platform. The advantages of C2C are as follows:

Supports multiple payment methods. Buyers and sellers can define any payment method themselves; as long as the user confirms receipt/payment after a real transaction, the transaction can be facilitated.

Low trust costs. Both parties in a transaction must first pass the platform's identity verification and even stricter merchant certification checks. The platform will also publicly disclose users' transaction information for credit reference, but it cannot avoid the risks of some counterparties delaying or canceling orders.

2. Cryptocurrency ATMs

As physical machines, they have higher operational and maintenance costs, thus the exchange fees are also high, with some even reaching 20%. Cryptocurrency ATM merchants purchase liquidity from third-party suppliers and transfer it to users' self-custody wallets, requiring remittance licenses.

The biggest advantage of cryptocurrency ATMs is anonymity and privacy, as users can purchase cryptocurrencies with cash, and most do not require KYC procedures. Sometimes identification documents may be required, but proof of residence and facial recognition are not necessary.

However, the types of cryptocurrencies supported are limited, mainly only supporting BTC and ETH. Most ATMs do not provide withdrawal services and are often referred to as the dumbest way to buy cryptocurrency due to high fees.

3. Centralized Exchange (CEX)

Centralized exchanges are the most commonly used platforms for fiat deposits and withdrawals. Exchanges naturally have licensing advantages, lower fees, and support a variety of cryptocurrencies. They are also the largest liquidity providers in the ecosystem, where retail investors can freely deposit and withdraw through custodial wallets, while merchants usually implement transactions and transfers via API and SDK. As liquidity intermediaries, centralized exchanges profit from the spread of buying and selling liquidity and user fees.

When merchants and their customers use the same exchange's custodial wallet, transactions incur no fees, as funds are only transferred between different accounts within the same custodial wallet. However, transferring using a self-custody wallet will incur corresponding blockchain network fees.

4. Independent Deposit and Withdrawal Projects

Independent deposit and withdrawal projects, such as Moonpay, operate like small exchanges but mostly only provide fiat deposit and withdrawal services, and need to register for remittance licenses in each operational region. However, due to their relatively small scale and limited legal and technical resources, these types of projects are more vertical, mostly only providing fiat deposit and withdrawal services and focusing on a single area of use.

However, due to differences in sources of liquidity and the fact that most customers need to provide self-custody wallet addresses, the fees for this type of project are higher than those of centralized exchanges, as they include intermediary and network fees. Although independent deposit and withdrawal projects are generally smaller and have higher fees than centralized exchanges, they also have their advantages:

A simple and user-friendly interactive interface. The minimalist interactive page directly displays the fiat amount and the corresponding cryptocurrency amount. Users only need identity verification for large transactions, making it friendly for small deposit and withdrawal users.

High privacy. Most projects only support self-custody wallets, thus eliminating the step of transferring cryptocurrency assets from custodial wallets, allowing users to use as little other wallet information as possible.

Most projects allow cooperative distributors to set distribution bonuses using SDKs, so distributors can freely control profits, while the profit-sharing in centralized exchanges is not as clear.

5. Deposit and Withdrawal Aggregators

Deposit and withdrawal aggregators, such as MetaMask's fiat deposit service, guide users to purchase through multiple independent deposit and withdrawal projects and centralized exchange quotes to earn commissions. This category essentially serves as an information intermediary, achieving liquidity sharing by aggregating multiple exchanges and independent deposit and withdrawal projects.

Acts only as an intermediary providing quotes, with all transactions conducted through third-party suppliers.

No remittance license is required, as users undergo identity verification through third-party suppliers.

In addition to fiat deposits and withdrawals, it can also provide DEX aggregation, liquidity staking, and NFT market functionalities. Deposit and withdrawal aggregators primarily target retail investors and do not provide payment solutions to merchants.

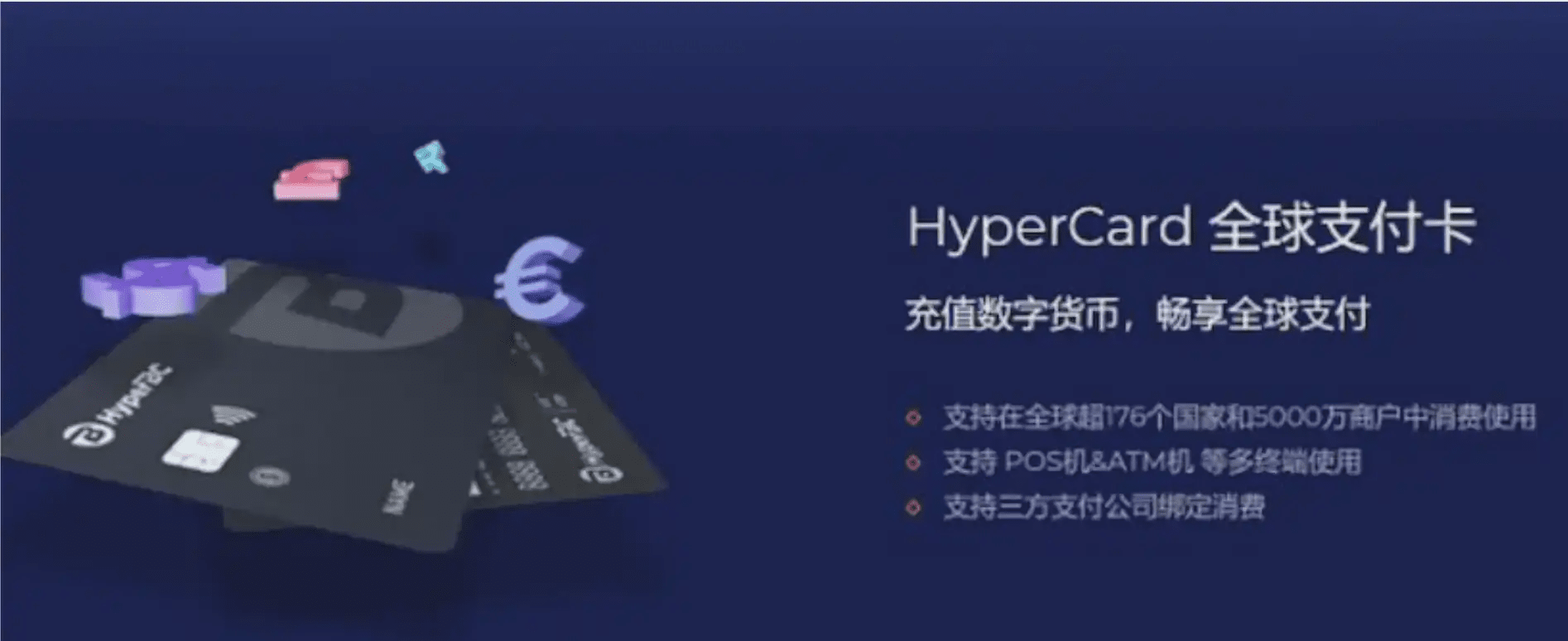

6. Cryptocurrency Debit Cards

The main advantage of cryptocurrency debit cards is that they allow the use of cryptocurrency for everyday consumption. In traditional consumption scenarios, it is difficult to do this unless merchants directly accept cryptocurrencies. Cryptocurrency debit cards are increasingly accepted by users in the crypto community, allowing direct consumption of cryptocurrencies or conveniently converting cryptocurrencies into fiat within the card for global payments and consumption.

Cryptocurrency debit cards are equivalent to secondary accounts delegated by centralized exchanges. As one of the customer services of centralized exchanges, the encrypted part of the deposit and withdrawal process is managed by the centralized exchange (no additional remittance license is required), while the processing of fiat payments is managed by payment network providers. The fees for cryptocurrency debit cards are often higher than those of centralized exchanges because users need to pay additional exchange fees to the payment network providers. Users pay merchants for goods and services priced in fiat currency with cryptocurrency through the debit card, so cryptocurrency debit cards can only serve as channels for fiat withdrawals. It is important to note that using a cryptocurrency debit card for payments will incur capital gains tax, and the card must be preloaded with cryptocurrency before use.

Using cryptocurrency debit cards also has the following advantages:

Fund security: Funds deposited into cards are operated by banks, so there is no need to worry about the source of funds or frozen cards. Physical cards support ATM withdrawals. In actual consumption, users directly spend fiat currency, not cryptocurrency assets.

Cross-border payments: Most cryptocurrency debit cards are Visa or Mastercard, supporting cross-border payments and usable at tens of millions of online and offline locations globally.

Cashback: Most cryptocurrency debit cards support cashback, which is returned to users in the form of cryptocurrency.

Security and compliance issues

Having understood the common methods of deposit and withdrawal, which one do you use most often? Different types of deposit and withdrawal methods each have their advantages, but we are more concerned about the legal safety of funds and transactions. Due to the differentiated regulations among major countries, there is still room for non-compliant deposit and withdrawal transactions in the market. Money laundering, tax evasion, fraud, and various means are frequently seen. Users' assets can be stolen, funds frozen, or they may be visited directly by relevant authorities, which makes ordinary users very distressed and anxious.

In Hong Kong, cryptocurrencies are classified as security tokens and non-security tokens, so operating virtual currency legally in Hong Kong requires applying for dual licenses. According to different regulatory authorizations, the Hong Kong Securities and Futures Commission regulates the trading of security tokens on virtual asset exchanges under the Securities and Futures Ordinance (License 1 + License 7); simultaneously, it also regulates the trading of non-security tokens on virtual asset exchanges under the Anti-Money Laundering Ordinance (VASP license). On August 3, HashKey and OSL received permission from the Hong Kong Securities and Futures Commission to upgrade License 1 (Securities Trading) and License 7 (Providing Automated Trading Services), being allowed to engage in retail cryptocurrency business in Hong Kong, becoming the first batch of licensed institutions since the new regulatory requirements for retail digital asset trading took effect on June 1, 2023.