Share a funding rate arbitrage method

Let’s first talk about the basic logic of realizing arbitrage

If the funding rate is > 0, long positions pay the funding fee and short positions receive the funding fee.

When the funding rate is less than 0, short positions pay funding and long positions receive funding.

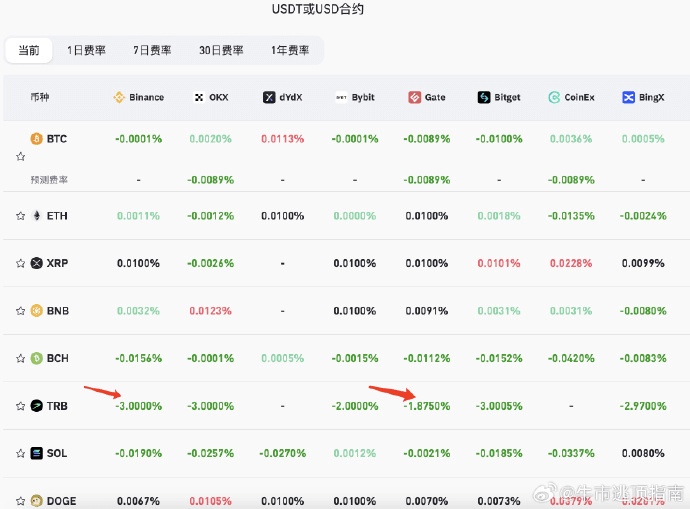

Let’s take TRB as an example.

Among them, the funding rate of Mouan is currently -3% and the funding rate of GATE is -1.87%

If a certain An opens long and GATE opens short, the opening price is 1x, which can offset the loss caused by the rise and fall.

However, those who open long positions can enjoy a 3% commission, while those who open short positions will lose a 1.87% commission.

So there is a spread in the middle, about 1.13%

If we use 500,000 yuan for arbitrage, after deducting all the handling fees, there is about a 1% interest rate difference.

The funding rate is settled every 8 hours, and you can earn 5,000 yuan every 8 hours.

The funding rate is about this level from yesterday to today, so in 24 hours, it is about 15,000 yuan

Finally, let’s talk about the risks

The biggest risk is that the sharp price fluctuations may lead to the risk of liquidation.

The second risk is the risk of small exchanges running away.

If you have enough margin and choose a large exchange, there is still a certain profit margin.

If you think it helps you, please remember to forward, comment and like it.