1) Executive summary

Raydium $RAY launched in 2021 and is the largest decentralized exchange on Solana, operating automated market maker (AMM) liquidity pools that enable permissionless token swaps, liquidity provision, and token launches. Token Terminal tracks Raydium across five products: OpenBook (legacy AMM), CLMM (concentrated liquidity), CPMM (constant product), Stable Swap, and LaunchLab (token launchpad). Raydium's architecture allows it to serve both passive liquidity providers through its legacy pools and active traders seeking capital-efficient execution through concentrated liquidity, while LaunchLab extends the project's reach into asset issuance.

Q1 2026 extended the downward trend that began after Q1 2025's memecoin-driven peak. All headline metrics declined on both a quarterly and annual basis, with year-over-year comparisons reflecting the extreme baseline set by Q1 2025. Beneath the headline declines, a compositional shift is emerging: tokenized asset volume on Raydium nearly tripled QoQ to $224.86m, representing one of the few volume categories that grew while overall activity contracted. Raydium's take rate has also risen structurally, from 5.59% in Q1 2025 to 13.27% in Q1 2026, as the product mix shifted toward higher-margin products

🔑 Key metrics (Q4 2025)

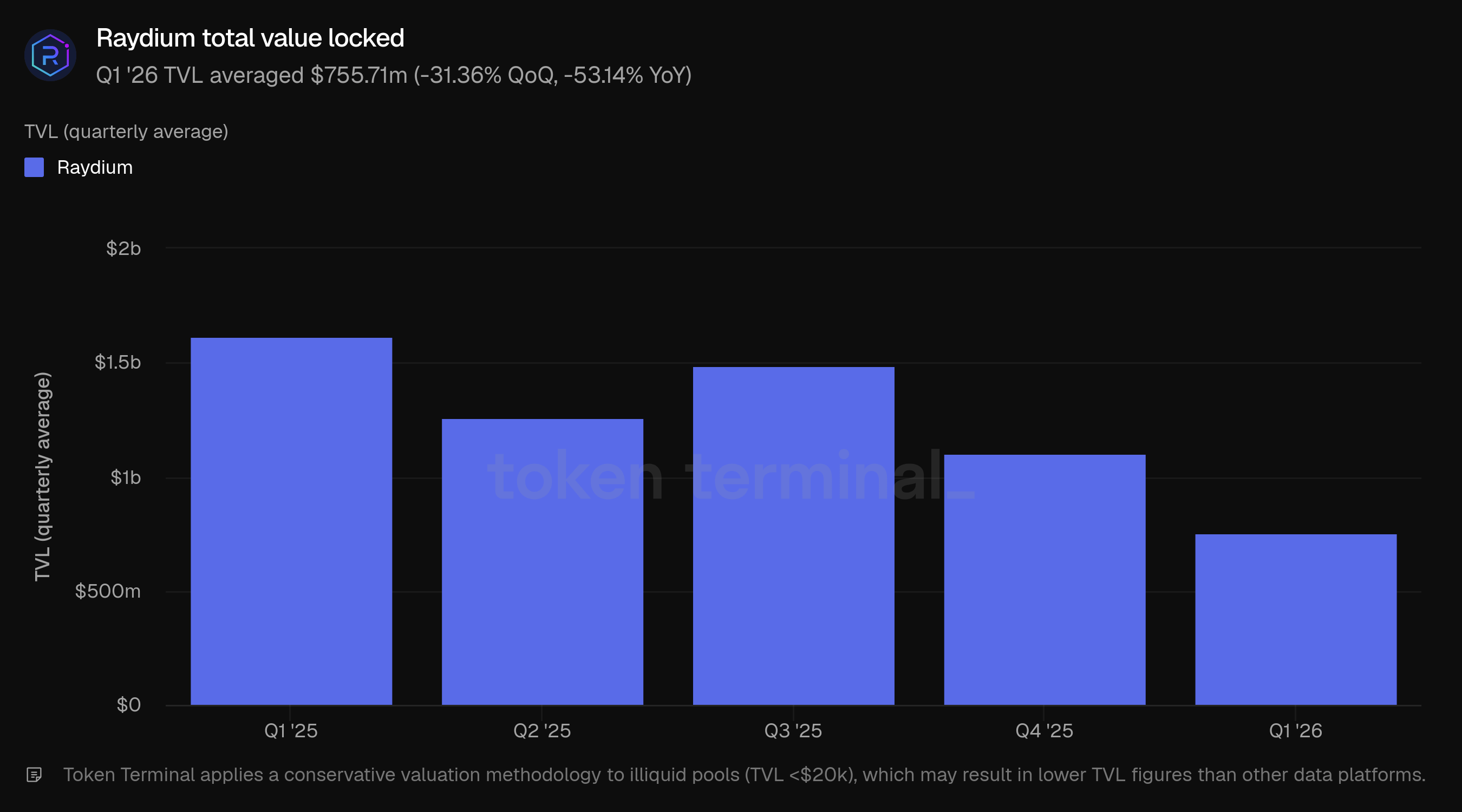

Total value locked: $755.71m (-31.36% QoQ, -53.14% YoY)

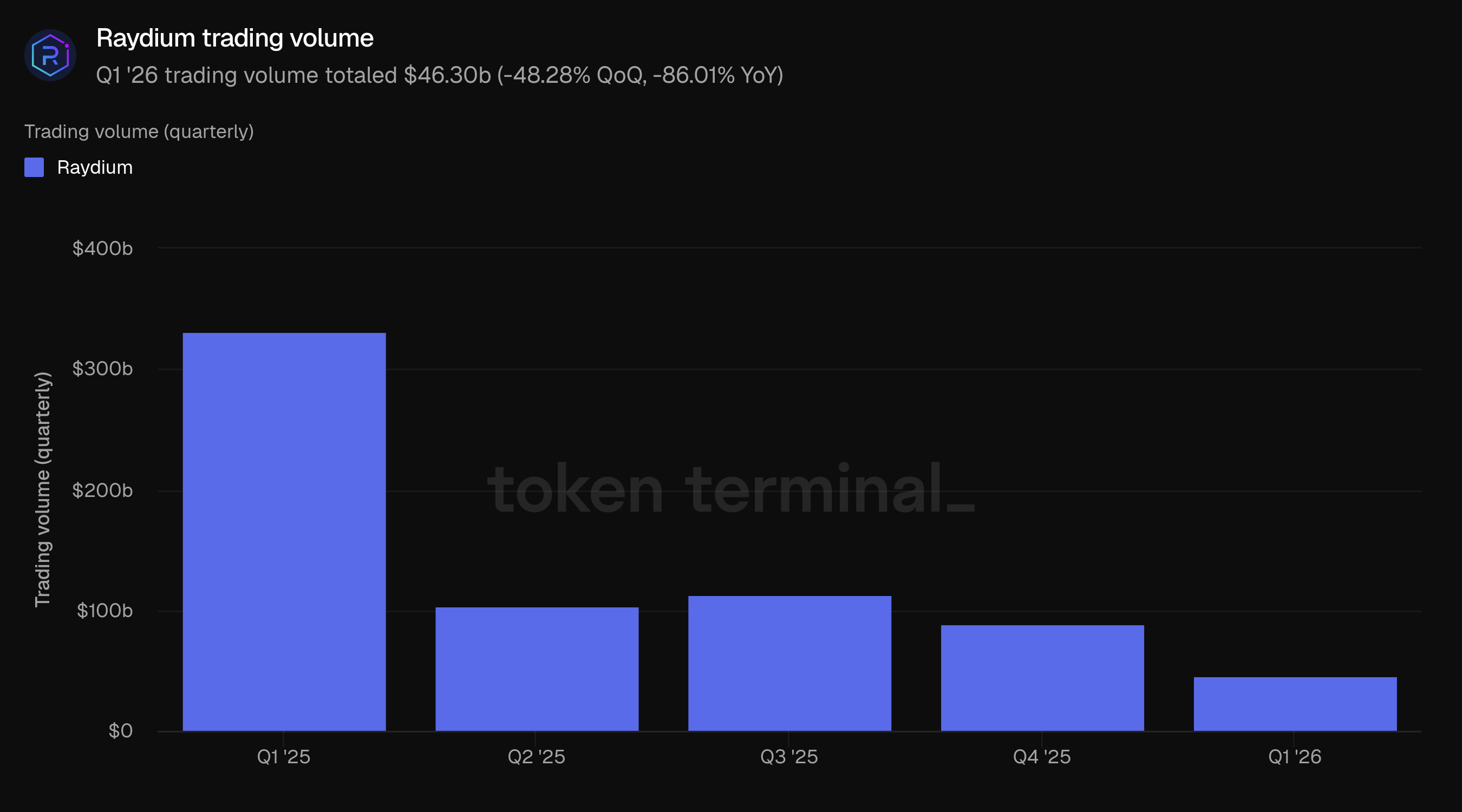

Trading volume: $46.30b (-48.28% QoQ, -86.01% YoY)

Fees: $24.61m (-26.12% QoQ, -96.86% YoY)

Revenue: $3.32m (-31.67% QoQ, -92.88% YoY)

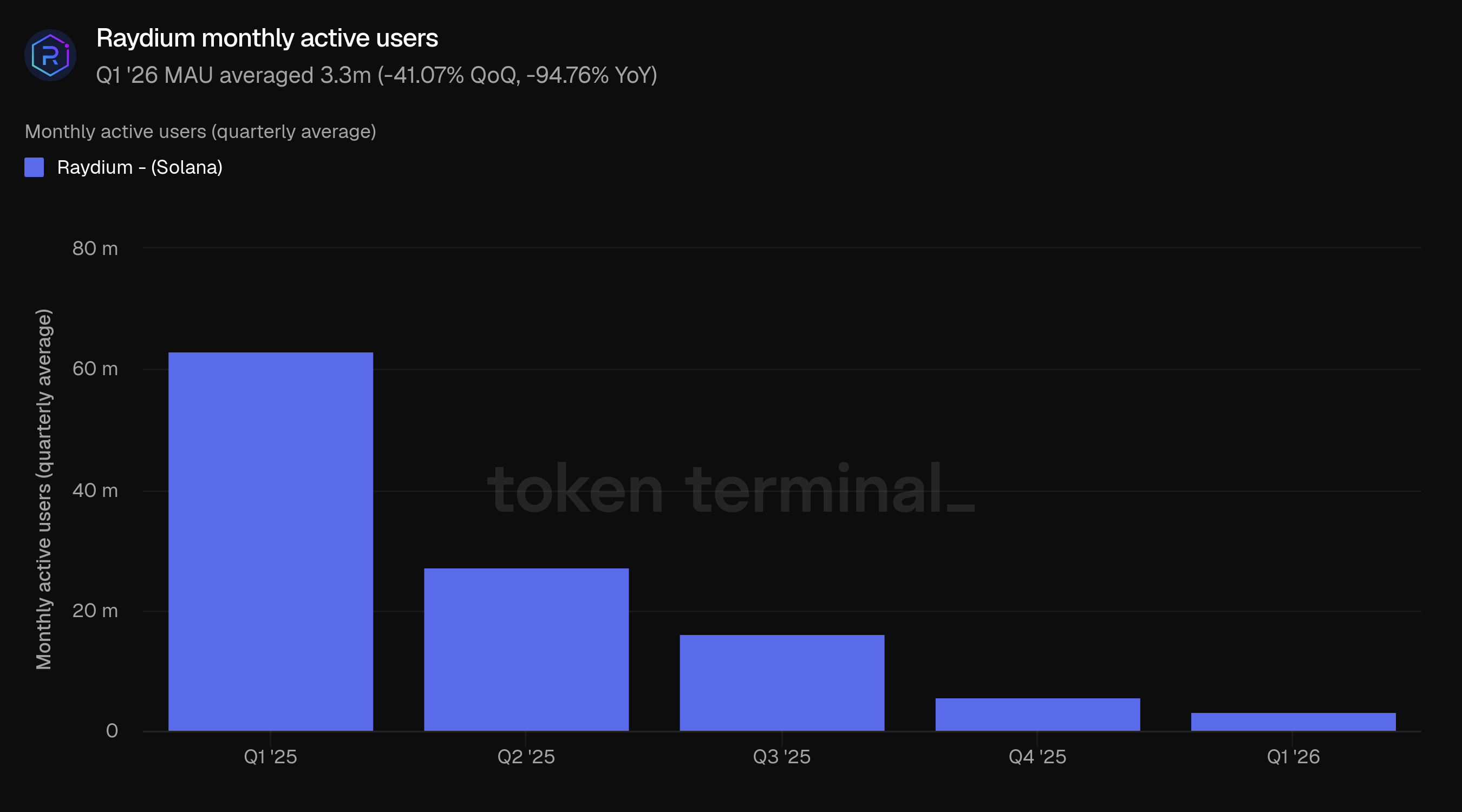

Monthly active users: 3.3m (-41.07% QoQ, -94.76% YoY)

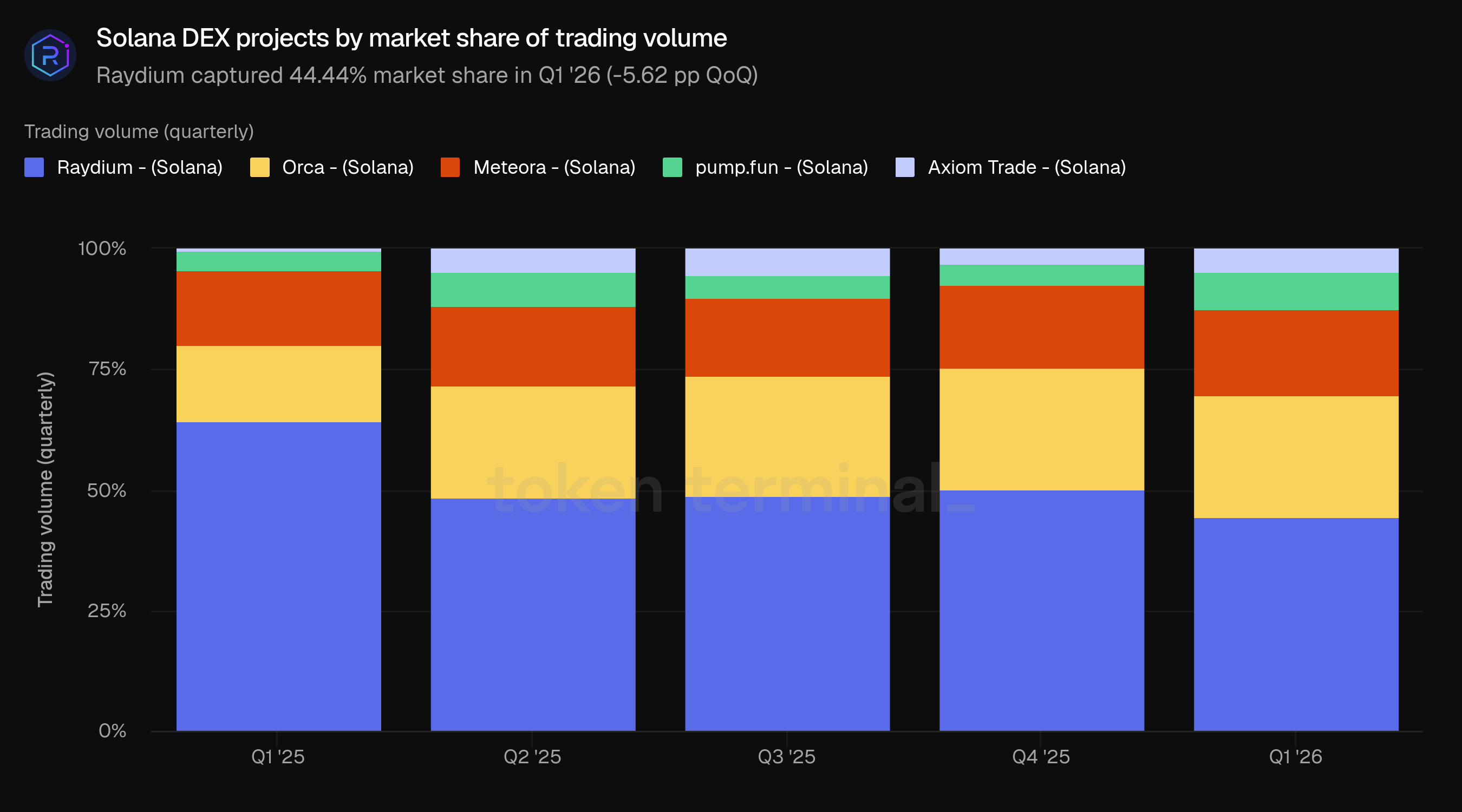

Market share: 44.44% (-5.62 pp QoQ, -19.75 pp YoY)

Year-over-year comparisons reflect Q1 2025, the highest-activity quarter in Raydium's history due to the memecoin trading peak.

👥 Raydium team commentary

"Q1 2026 extended the normalization trend that began in Q4 2025, with Solana application revenue and spot DEX volume continuing to compress. Raydium generated $3.32m in Token Terminal-measured revenue against a backdrop of declining ecosystem activity, though the quarter was characterized by internal mix rotation rather than broad deterioration: LaunchLab revenue increased significantly while swap revenue declined. This divergence reflects improving launchpad-specific conditions even as secondary trading activity remained soft.

Raydium's non-RAY balance sheet closed Q1 at $49.47m, comprising $21.1m in stablecoins and $28.3m in SOL, offering a substantial operational runway independent of token price volatility. On an adjusted basis, removing bought-back RAY from circulating supply, Raydium ended Q1 with an adjusted circulating supply of 187.9m RAY and an adjusted market cap of $118m.

Raydium is making progress on tokenomics updates pertaining to non-circulating supply, including mechanisms to smooth reflexivity in buyback execution and incorporate new staking dynamics. These updates aim to provide greater clarity on token supply projections and improve the alignment between protocol economics and long-term holder outcomes. The focus for Q2 shifts from resilience to conversion: broadening LaunchLab distribution beyond concentrated partner channels, sustaining CLMM-led liquidity depth, and translating tokenized-asset share gains into repeatable monetization."

2) Total value locked

Total value locked (TVL) measures the total USD value of tokens deposited into Raydium's liquidity pools on Solana. Q1 TVL averaged $755.71m, down 31.36% from Q4's $1.10b and down 53.14% from Q1 2025's $1.61b.

The decline reflects both continued liquidity withdrawal and the impact of lower SOL prices, which fell approximately 30% over Q1 2026. SOL-denominated pools represent the majority of Raydium's TVL, meaning asset price declines directly reduce the dollar value of deposits even when token-denominated liquidity remains stable.

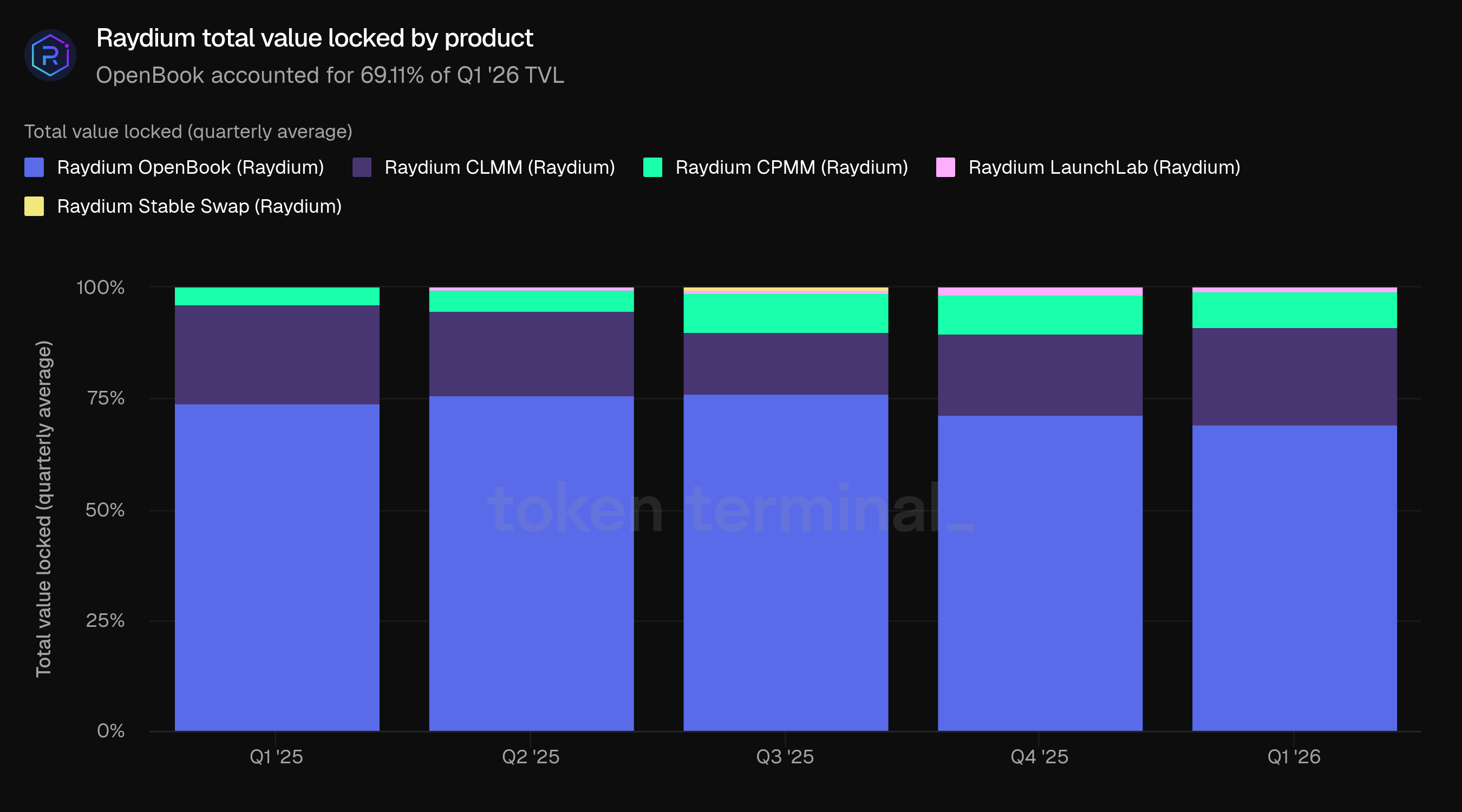

OpenBook held the largest share at 69.11% of Q1 TVL, down from 71.26% in Q4. CLMM pools accounted for 22.06%, up from 18.39%, followed by CPMM at 7.98%, LaunchLab at 0.69%, and Stable Swap at 0.15%. The increase in CLMM's TVL share (from 18.39% to 22.06%) is notable.

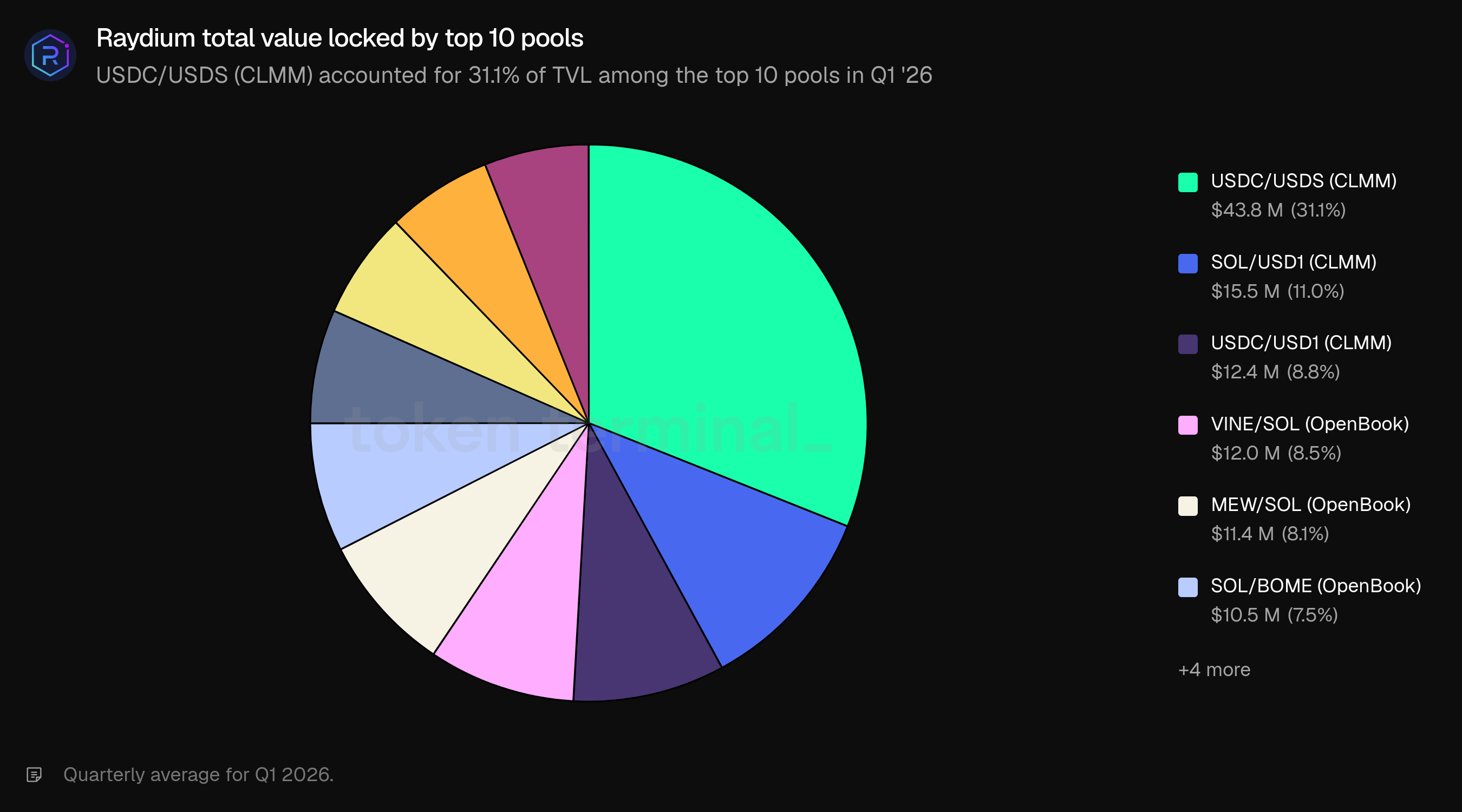

Among the top ten pools by average TVL, the largest was USDC/USDS (CLMM) at $43.8m (31.1%). Two other CLMM stablecoin pairs ranked among the top ten: SOL/USD1 ($15.5m, 11.0%) and USDC/USD1 ($12.4m, 8.8%). The emergence of USD1 pairs among the largest pools reflects the impact of the World Liberty Financial partnership, which incentivized USD1 liquidity provision on Raydium through Project Wings. The remaining seven of the top ten pools were OpenBook legacy pairs, predominantly memecoin/SOL pairs: VINE/SOL ($12.0m, 8.5%), MEW/SOL ($11.4m, 8.1%), SOL/BOME ($10.5m, 7.5%), USDC/SOL ($9.3m, 6.6%), FARTCOIN/SOL ($8.7m, 6.2%), SLERF/SOL ($8.6m, 6.1%), and SMOLE/SOL ($8.6m, 6.1%).

👥 Raydium team commentary

"The 31% QoQ decline in USD-denominated TVL reflects the combined impact of SOL price depreciation (approximately 30% over Q1), following Q4's contraction. In SOL terms, the decline was more modest, suggesting that a meaningful portion of the drawdown is attributable to asset price movement rather than fundamental shifts in liquidity provider confidence.

The rise in CLMM's TVL share (from 18.39% to 22.06%) is driven in part by stablecoin pair growth, including the emergence of USD1 pools following the World Liberty Financial partnership through Project Wings. This stablecoin TVL growth reflects both external partnership activity and Raydium's continued positioning as the primary venue for permissioned and institutional-grade liquidity on Solana. The legacy OpenBook and CPMM pools remain important for passive liquidity providers and new token launches, while CLMM pools serve active traders and shorter-tail assets. Raydium’s dual architecture continues to serve distinct user segments effectively."

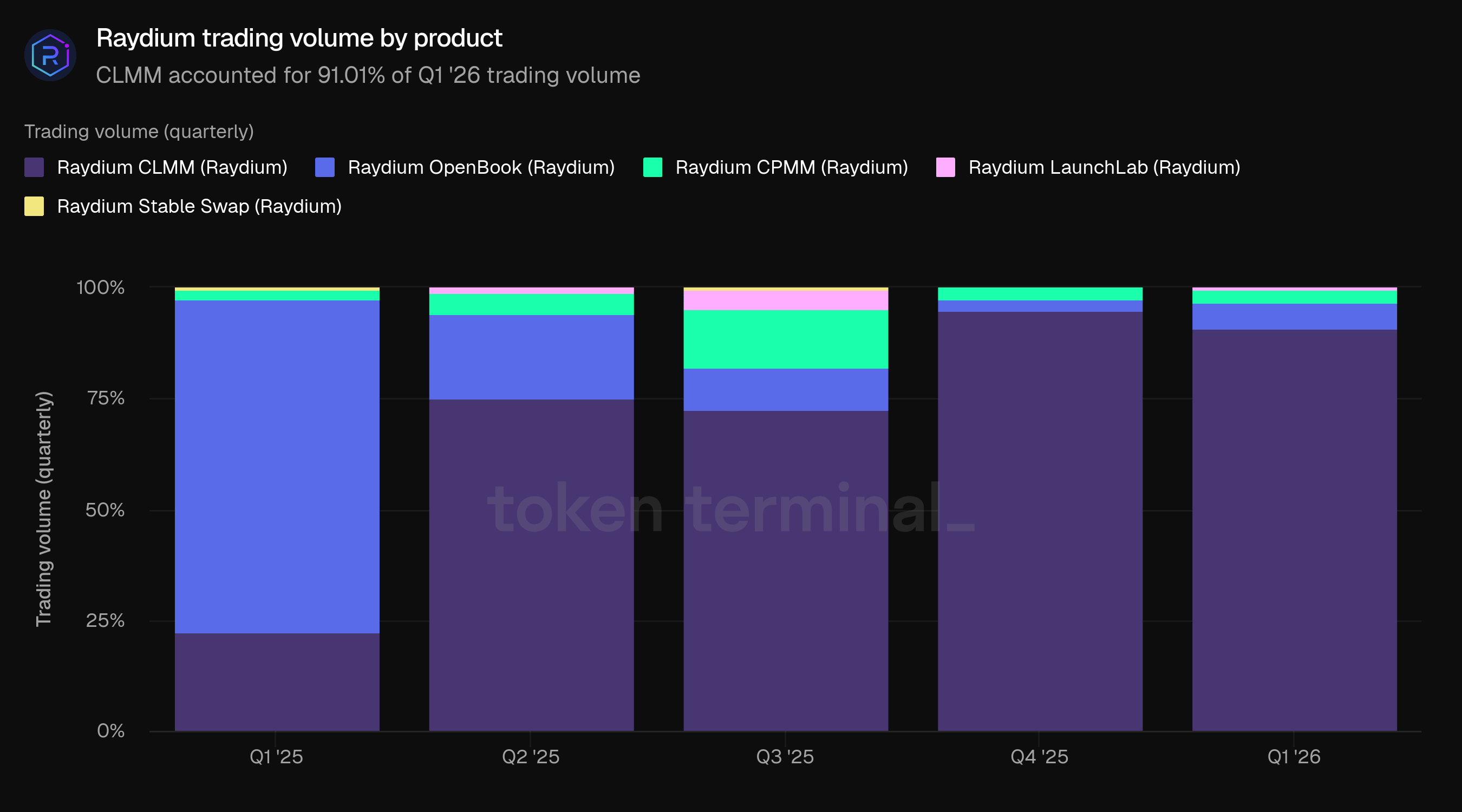

3) Trading volume

Trading volume measures the total USD value of tokens traded on Raydium across its various products. Q1 trading volume totaled $46.30b, down 48.28% from Q4's $89.54b and down 86.01% from Q1 2025's $330.82b.

The decline was broad-based, consistent with a continued reduction in Solana ecosystem activity. Q1 2025 represented the peak of the memecoin trading cycle, making the year-over-year comparison (-86.01%) particularly stark.

CLMM pools captured 91.01% of Q1 volume, down slightly from 94.78% in Q4. OpenBook's share rose to 5.73% from 2.76%, while CPMM accounted for 2.92%, LaunchLab for 0.33%, and Stable Swap for a negligible share.

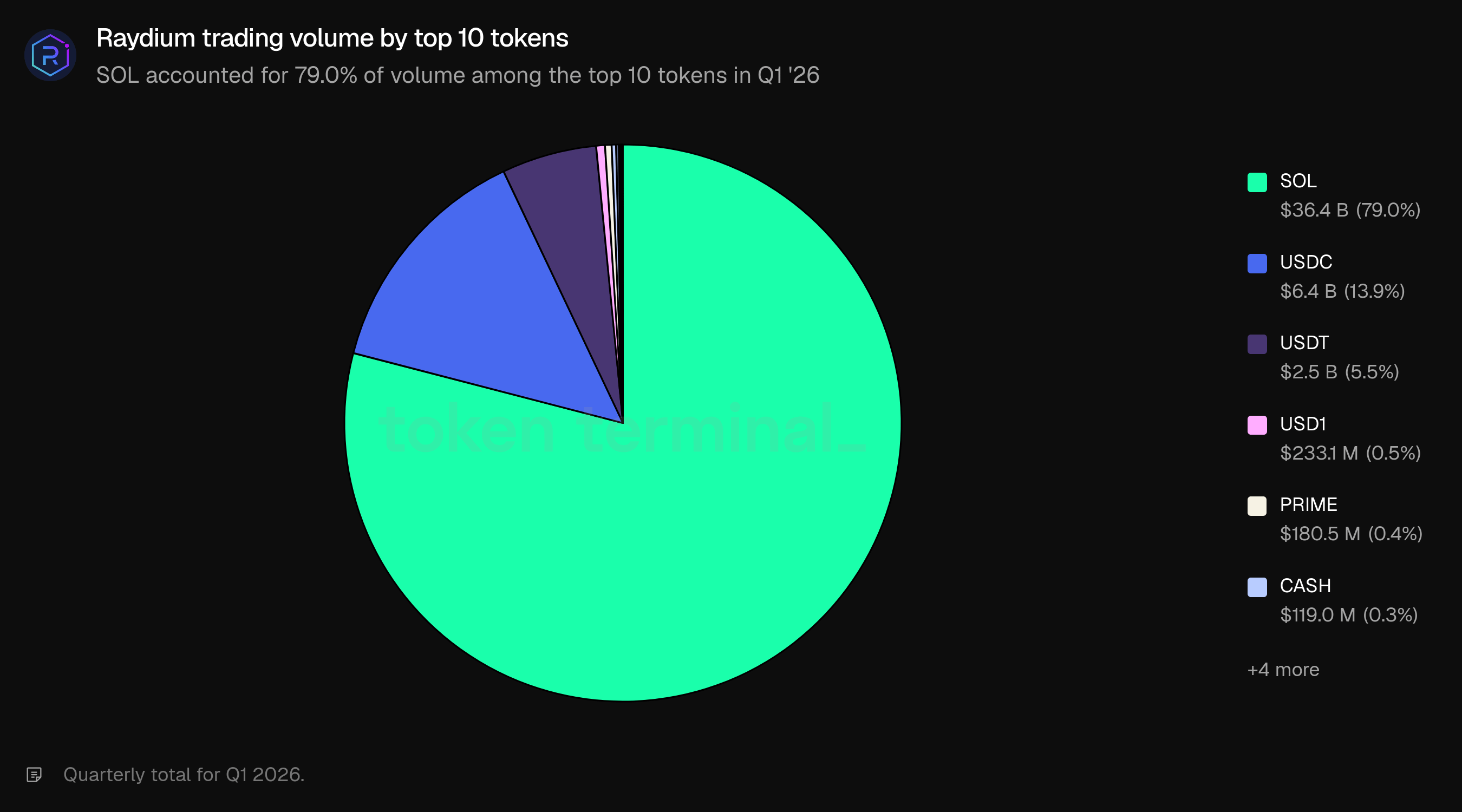

Among the top ten tokens by volume, SOL dominated at $36.4b (79.0%), followed by USDC at $6.4b (13.9%), USDT at $2.5b (5.5%), USD1 at $233.1m (0.5%), and PRIME at $180.5m (0.4%). USD1's presence among the top tokens reflects the impact of the World Liberty Financial partnership, while PRIME, a tokenized yield product from Figure's onchain RWA infrastructure, highlights the continued growth of tokenized asset trading on Raydium. The remaining tail included CASH ($119.0m, 0.3%), USDG ($67.5m, 0.1%), WAR ($39.7m, 0.1%), 1COIN ($35.5m, 0.1%), and WBTC ($32.4m, 0.1%).

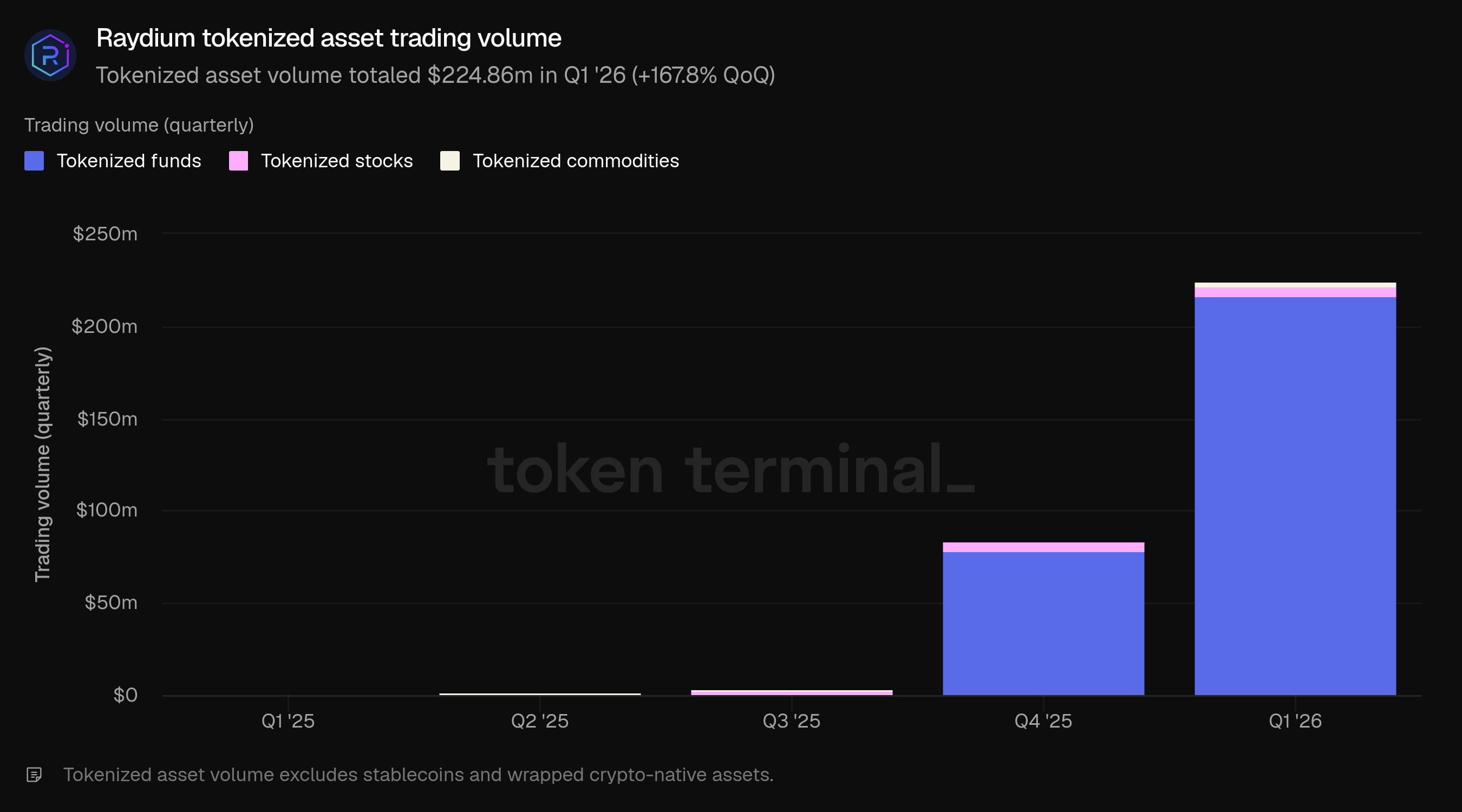

Tokenized asset trading volume on Raydium totaled $224.86m in Q1, up 167.8% from Q4's $83.93m. While memecoin-driven activity, which powered Raydium's record volumes in early 2025, has contracted sharply over the past four quarters, tokenized asset volume has moved in the opposite direction. Tokenized funds dominated at $216.99m (96.5% of the total), driven primarily by PRIME and related onchain yield products. Tokenized stocks contributed $5.03m and tokenized commodities $2.84m. The growth trajectory has been steep: tokenized asset volume was effectively zero in Q1 2025 ($1.22m), rose to $83.93m in Q4 2025, and nearly tripled again in Q1 2026.

👥 Raydium team commentary

"The volume decline reflects the natural cyclicality of crypto markets following Q1 2025's memecoin-driven peak, combined with continued compression in Solana ecosystem activity more broadly. Raydium's 48% QoQ volume decline was consistent with ecosystem-wide trends.

OpenBook's volume share increase (from 2.76% to 5.73%) likely reflects concentrated activity in specific legacy pairs during periods of volatility, where the established pool architecture and deeper liquidity for certain tokens provide execution advantages. The shift toward tokenized asset volume, which nearly tripled QoQ to $224.86m, represents an intentional strategic direction. Raydium's CLMM allowList framework and partnerships with tokenized asset issuers position the protocol to capture institutional and RWA-adjacent flow as the market matures beyond speculative cycles. This diversification provides a more durable revenue baseline independent of memecoin activity."

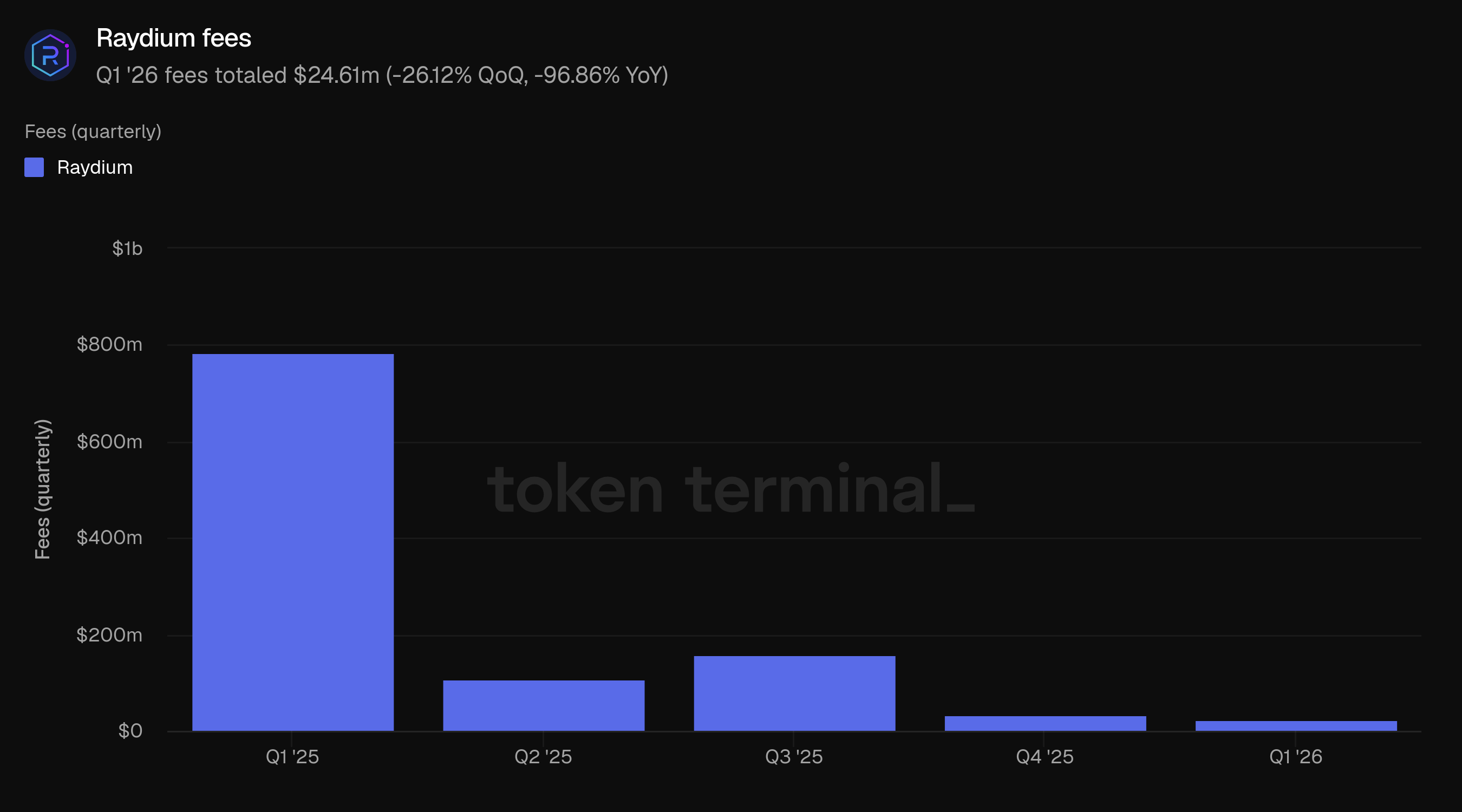

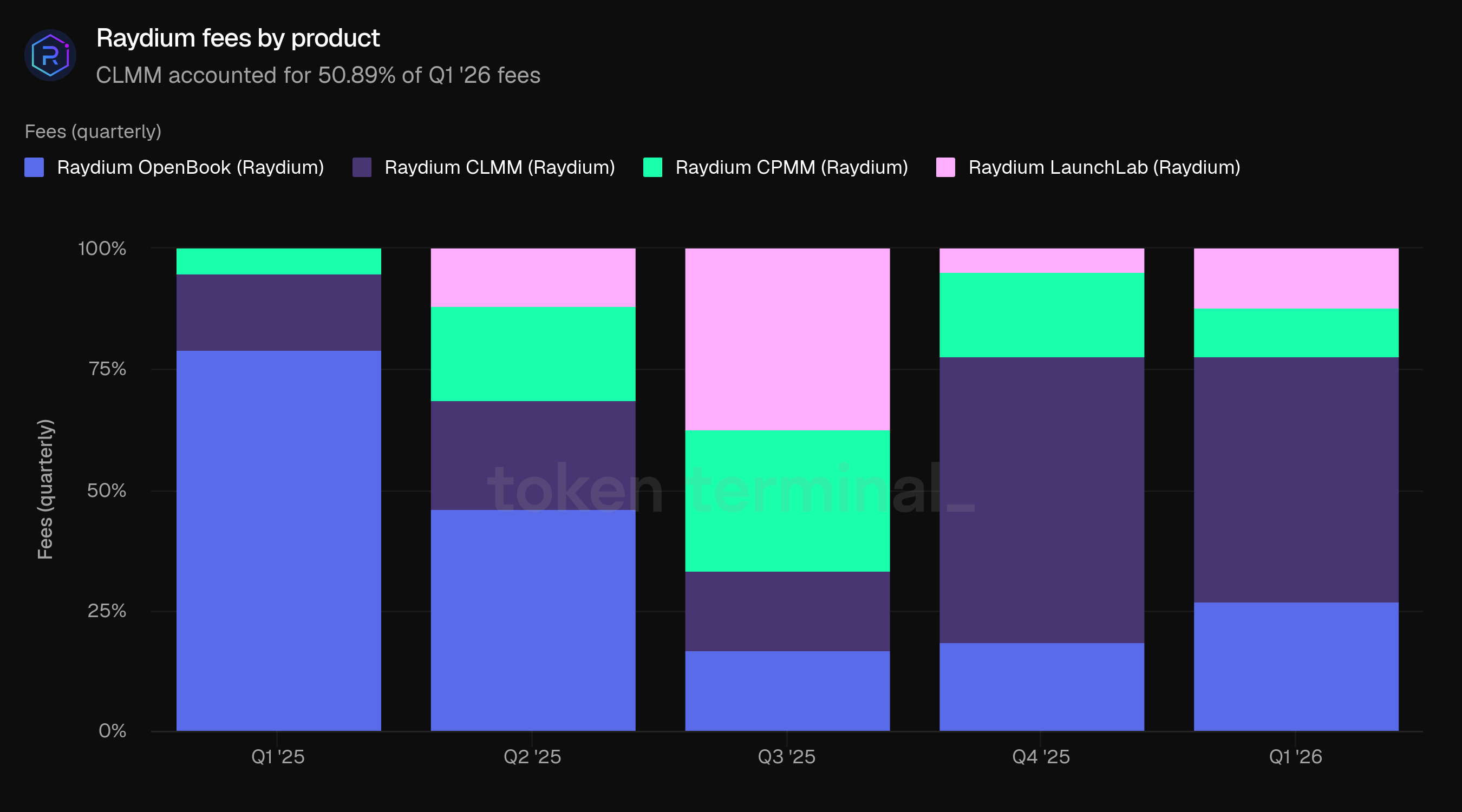

4) Fees

Fees measure the total USD value of trading fees paid by users across Raydium's products, calculated by applying pool-specific fee rates to trading volume. Q1 fees totaled $24.61m, down 26.12% from Q4's $33.31m and down 96.86% from Q1 2025's $784.50m.

The fee decline (-26.12%) was notably smaller than the volume decline (-48.28%), indicating a shift in activity toward higher-fee-rate products and pools. This is the most significant compositional dynamic in Q1.

By product, CLMM represented 50.89% of Q1 fees, down from 59.20% in Q4. OpenBook's fee share rose significantly from 18.56% to 26.96%, LaunchLab from 4.81% to 12.24%, and CPMM fell from 17.43% to 9.92%.

The LaunchLab resurgence is striking: LaunchLab generated 12.24% of fees despite accounting for just 0.33% of volume, reflecting the product's high fee rates on token launches. This dynamic mirrors Q3 2025, when LaunchLab peaked at 37.45% of fees. OpenBook's fee share increase (18.56% to 26.96%) alongside its volume share increase (2.76% to 5.73%) is consistent with the product's fixed 25bps fee rate, which is higher than the typical CLMM fee tier used for major pairs.

The effective fee rate (fees as a percentage of volume) was approximately 5.3bps in Q1, up from 3.7bps in Q4. This increase reflects the shift in fee composition toward higher-rate products (LaunchLab, OpenBook) and away from the lowest-tier CLMM pools that dominated Q4 volume.

👥 Raydium team commentary

"LaunchLab's fee resurgence (from $1.6m in Q4 to $3.0m in Q1) reflects improved launchpad-specific conditions and continued partner activity through the integrated token-lifecycle model. Platform volume increased 64.5% QoQ to $0.97b in Raydium's internal accounting, outpacing broader Solana bonding-curve launchpad growth. The product's high fee rates on token launches, generating 12.24% of fees despite just 0.33% of volume, demonstrate the value capture potential of the issuance-to-secondary-trading integration.

Fee diversification remains a priority as the product mix evolves. The effective fee rate increase (from 3.7bps to 5.3bps) reflects the shift toward higher-rate products and validates the multi-product strategy."

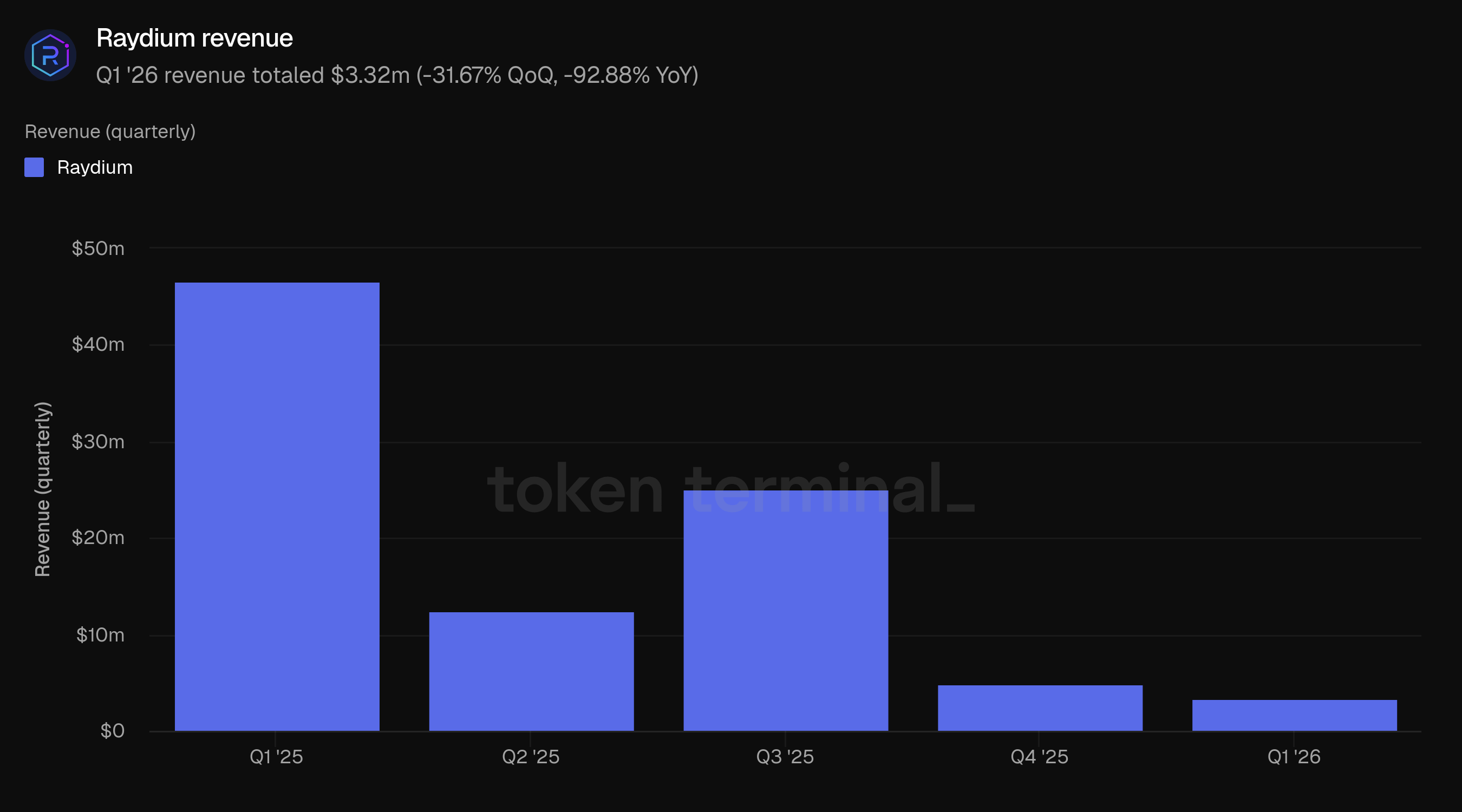

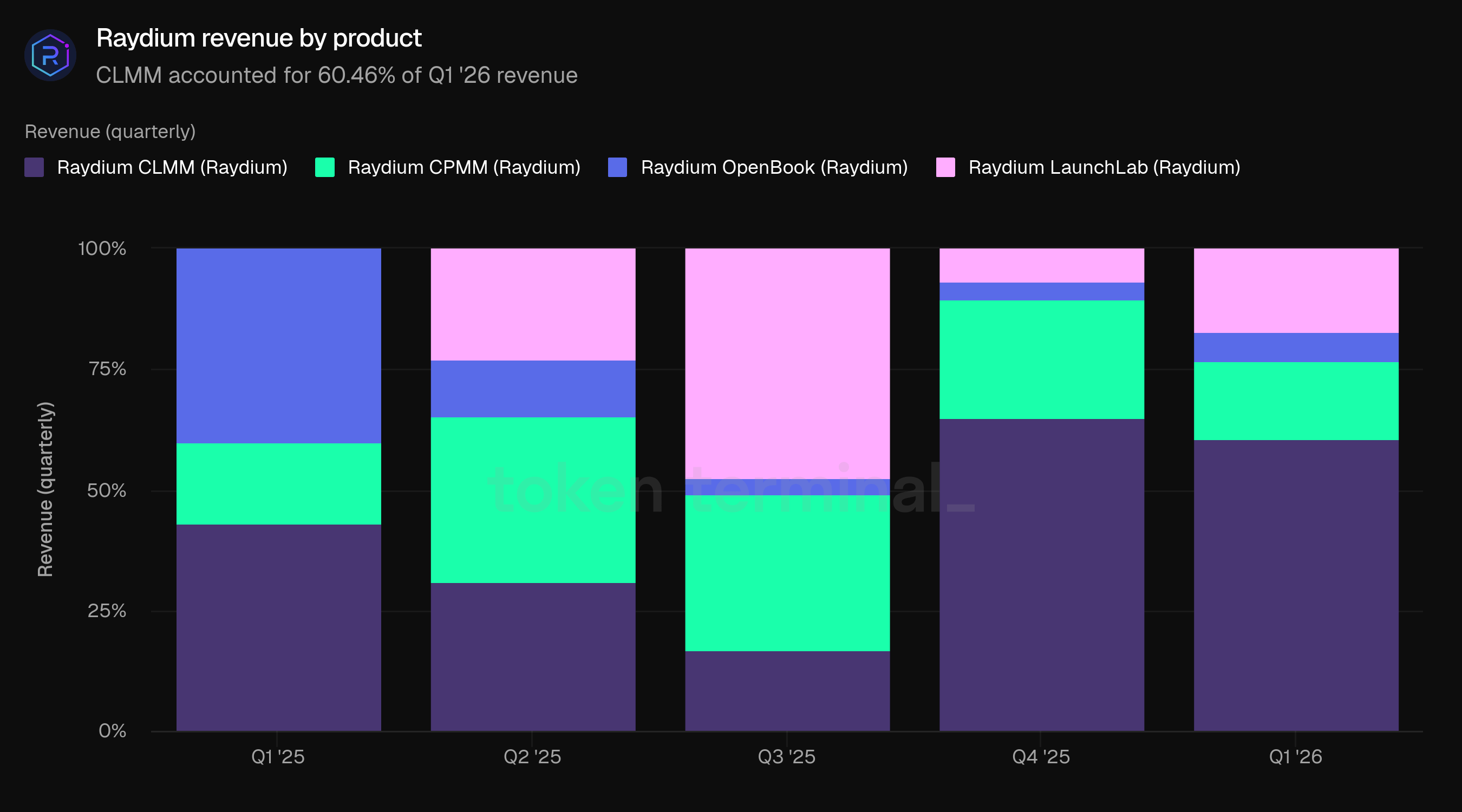

5) Revenue

Revenue measures the total USD value of trading fees retained by Raydium after compensating liquidity providers. Q1 revenue totaled $3.32m, down 31.67% from Q4's $4.85m and down 92.88% from Q1 2025's $46.57m.

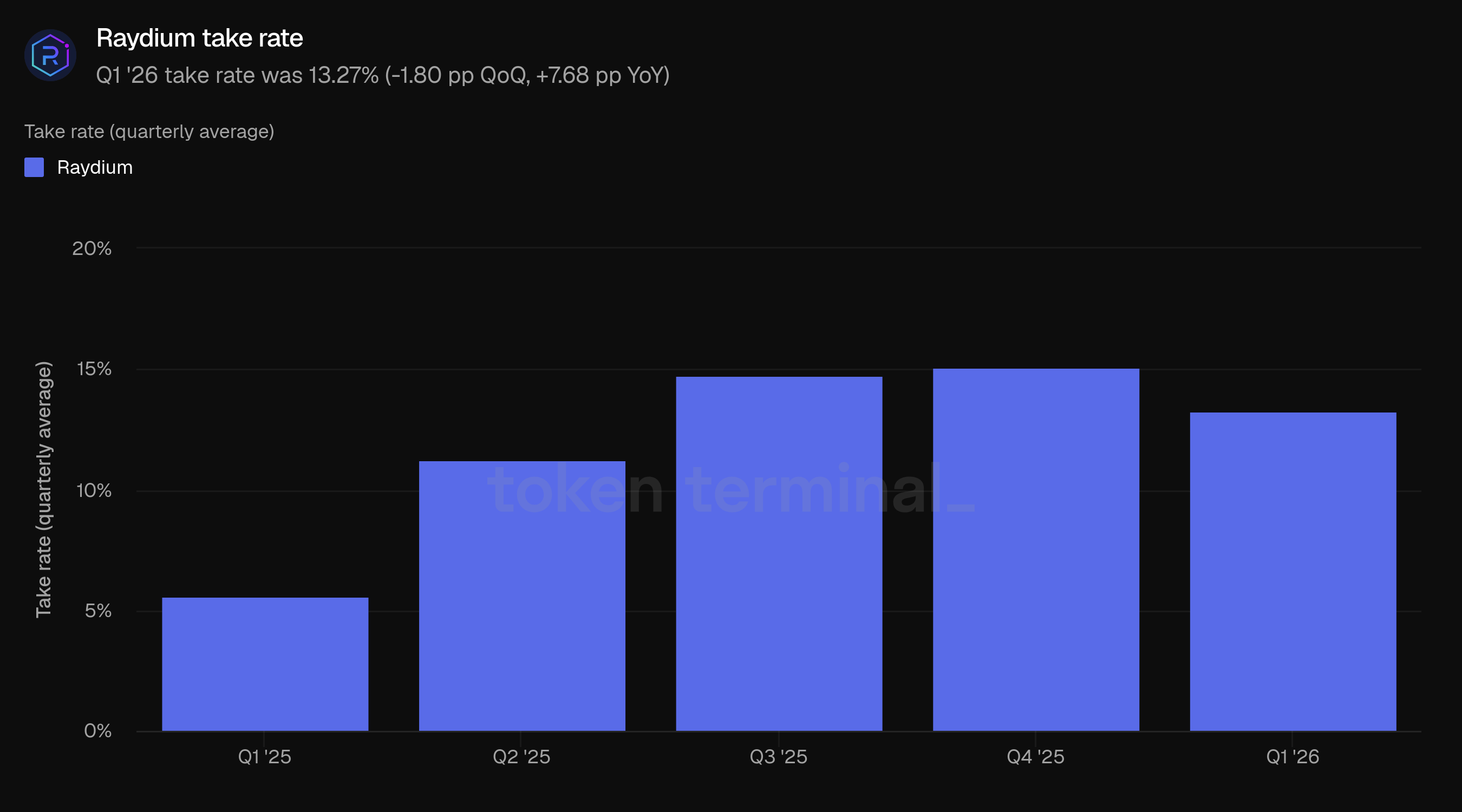

The revenue decline (-31.67%) was steeper than the fee decline (-26.12%), reflecting a slight compression in take rate from 15.07% to 13.27% as the product mix shifted (see below).

By product, CLMM was the largest contributor at 60.46% of Q1 revenue, followed by LaunchLab at 17.06%, CPMM at 16.48%, and OpenBook at 6.00%.

LaunchLab's share of revenue (17.06%) is notable given that the product accounted for just 0.33% of trading volume and 12.24% of fees. LaunchLab charges a 1% platform fee on token launches, of which 0.25% is burned and 0.75% flows to the protocol, resulting in a higher revenue conversion rate than spot trading products.

Take rate measures the percentage of total fees that Raydium retains as revenue. Q1 take rate was 13.27%, down from 15.07% in Q4 but up from 5.59% in Q1 2025. The five-quarter trajectory (5.59% → 11.25% → 14.77% → 15.07% → 13.27%) reflects the structural shift in Raydium's product mix: in Q1 2025, OpenBook dominated fee generation, while the subsequent rise of CLMM and LaunchLab lifted the overall rate. The Q1 2026 dip from Q4 is consistent with LaunchLab's fee share moderating from its Q3 peak and OpenBook's fee share rising.

👥 Raydium team commentary

"Raydium's non-RAY balance sheet closed Q1 at approximately $49m, comprising $21m in stablecoins and $28m in SOL. This reserve base offers a substantial operational runway independent of token price volatility. Capital discipline remained strict through the quarter, with buybacks continuing despite the revenue contraction, and net profit margins remaining above 87%.

LaunchLab value capture remains a 2026 priority. The integrated token-lifecycle model, capturing value from issuance through secondary trading, continues to provide revenue optionality distinct from core swap dependency. Partnerships including the Winner's Arc collaboration with World Liberty Financial, Bonk Fun, and Axiom expanded LaunchLab distribution. On Raydium Perps, the product continues scaling with 100+ perpetual markets available; while not captured in Token Terminal's revenue data, Perps represents the protocol's first structural expansion away from spot swap dependency and remains a near-term growth focus."

6) Monthly active users & market share

Monthly active users (MAU) measures the number of unique addresses that executed at least one trade on Raydium within a rolling 30-day period. Q1 MAU averaged 3.3m, down 41.07% from Q4's 5.6m and down 94.76% from Q1 2025's 63.0m.

The MAU decline has been the steepest and most sustained metric across all quarters, reflecting the continued normalization of Solana wallet activity after the memecoin peak. As the team noted in Q4, MAU measured by active addresses can be a misleading metric in low-fee ecosystems like Solana, where the cost of account creation is low and periods of speculative activity inflate address counts through spam and bot activity. Q1 2025's 63.0m MAU baseline included significant bot-driven activity.

Raydium's Solana DEX market share of trading volume averaged 44.44% in Q1, down 5.62 pp from Q4's 50.06% and down 19.75 pp from Q1 2025's 64.19%. This was the first quarter below 50% since Q2 2025 and the largest single-quarter decline in the dataset.

The share loss was distributed across competitors. Orca held roughly steady at 25.28% (from 25.38%), while Meteora gained modestly to 17.86% (from 17.12%). pump.fun's share rose sharply from 4.46% to 7.64%, and Axiom Trade increased from 2.98% to 4.79%. The growth of pump.fun, which operates its own AMM rather than routing volume through Raydium, represents a structural competitive dynamic rather than a cyclical one.

👥 Raydium team commentary

"Monthly active user declines mirror patterns seen across the broader Solana ecosystem and reflect the normalization of trading activity for long-tail assets following 2025's speculative peaks. As noted in prior quarters, MAU measured by active addresses can be a misleading metric in low-fee ecosystems like Solana, where the cost of account creation is minimal and can lead to heightened address activity during periods of market fervor. The focus remains on diversifying revenue streams to flatten reflexivity while maintaining leadership in core trading infrastructure."

7) Outlook

Raydium's 2026 roadmap is oriented around reducing the project's dependence on memecoin-driven trading cycles, which have produced sharp revenue swings over the past year. Q1 data suggests this transition is underway: tokenized asset volume grew from effectively zero in Q1 2025 to $224.86m in Q1 2026, the effective fee rate rose even as headline volume halved, and the take rate has more than doubled year-over-year.

The team has framed Q2 as a shift from resilience to conversion, with three near-term priorities: broadening LaunchLab distribution beyond concentrated partner channels, sustaining CLMM-led liquidity depth, and translating tokenized-asset share gains into repeatable monetization. Raydium Perps continues scaling across 100+ perpetual markets as the project's first structural revenue line outside spot swaps. On the tokenomics side, the team has indicated progress on updates to non-circulating supply mechanics, including measures to smooth reflexivity in buyback execution and incorporate new staking dynamics.

8) Definitions

Products:

OpenBook (Legacy AMM): Raydium’s legacy AMM that originally bridged onchain liquidity pools with a Central Limit Order Book (CLOB). It now functions solely as a traditional AMM but remains the project's foundational layer.

Stable Swap: Raydium’s optimized AMM pools designed for low-slippage swaps between assets with closely correlated prices, such as stablecoins.

CLMM: Raydium’s concentrated-liquidity automated market maker, which allows liquidity providers to allocate liquidity within specific price ranges to improve capital efficiency.

CPMM: Raydium's latest iteration of constant product pools. CPMM pools are anchor-compatible, support Token-2022, and offer several fee configs.

LaunchLab: Raydium’s token launchpad, introduced in April 2025, that enables permissionless token creation and supports liquidity bootstrapping for newly launched assets.

Metrics:

Total value locked: measures the total USD value of assets deposited into Raydium’s liquidity pools on Solana.

Trading volume: measures the total USD value of token swaps executed across Raydium’s CLMM, CPMM, OpenBook, LaunchLab, and Stable Swap products.

Fees: measures the total USD value of trading fees paid by users across Raydium’s products, calculated by applying pool-specific fee rates to trading volume.

Revenue: measures the total USD value of trading fees retained by Raydium after compensating liquidity providers.

Take rate: measures the percentage of total fees that Raydium retains as revenue.

Monthly active users: measures unique addresses that executed trades on Raydium within a 30-day rolling window.

9) About this report

This report is published quarterly and produced leveraging Token Terminal's end-to-end onchain data infrastructure. All metrics are sourced directly from blockchain data. Charts and datasets referenced in this report can be viewed on the corresponding Raydium Q1 2026 Report dashboard on Token Terminal.