I did not notice it immediately, but every on-chain transaction carries a small moment that most of us rarely stop to examine.

We usually talk about settlement because settlement is easy to understand. Value moves. A wallet balance changes. The transaction becomes final. It is visible, clean, and measurable.

But before that final moment, there is another stage.

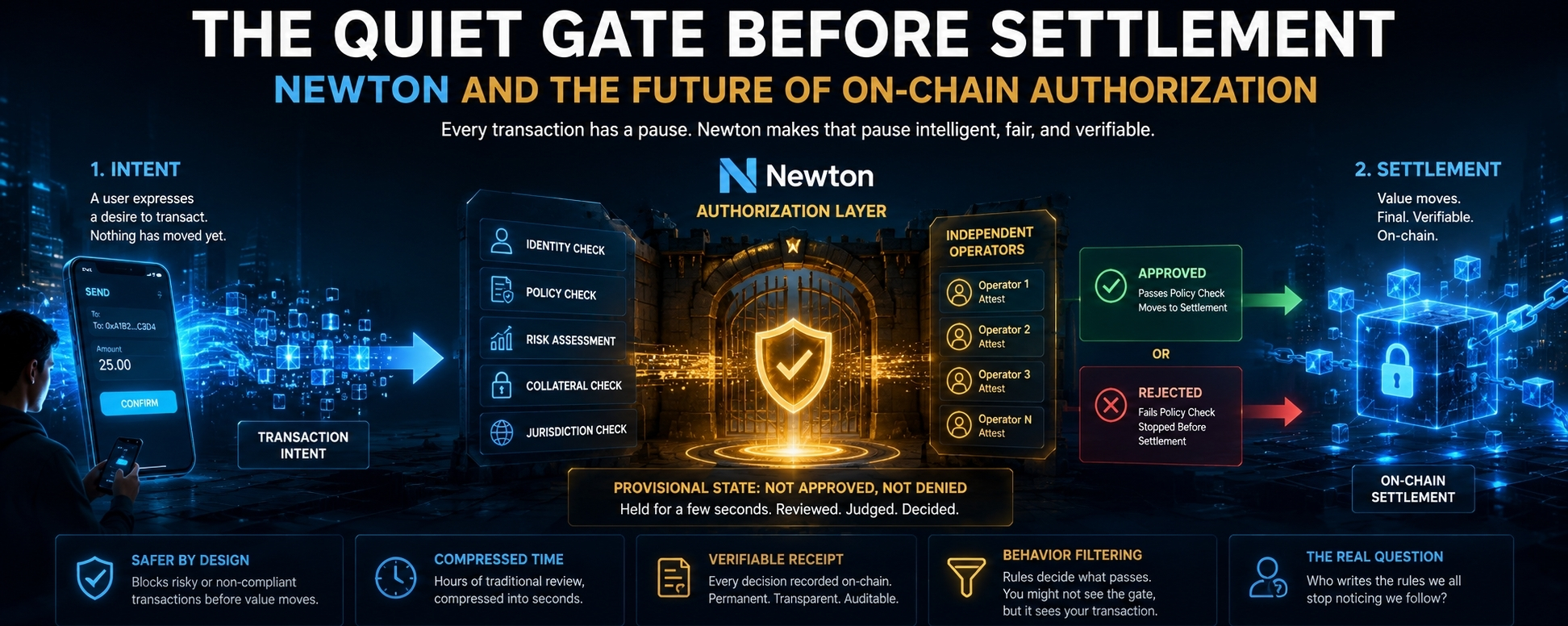

A transaction exists first as intent.

Nothing has moved yet. Nothing has been settled. The user has only expressed a desire for something to happen. And the more I think about it, the more I realize that this thin space between intention and execution may become one of the most important layers in on-chain finance.

That is where Newton’s position becomes interesting.

Newton is not simply trying to make settlement faster. It is working on something quieter and more structural: an authorization layer that sits just before value is allowed to move. Before a transaction reaches final execution, it can pass through a policy check. For a brief moment, the transaction is held in a provisional state. It is not approved yet. It is not rejected either. It is waiting.

During that pause, independent operators review the same request and decide whether it should be allowed to continue. Each operator makes that judgment separately, based on the rules and conditions set around the transaction. If the request passes, it moves forward. If not, it stops before settlement ever happens.

That small pause changes the behavior of the entire system.

It brings back a kind of friction that crypto originally tried to remove. In traditional finance, there was always someone or something standing between intent and clearance. A compliance officer looking at a wire transfer. A risk team flagging an unusual counterparty. A second layer of review when a transaction looked unfamiliar.

Crypto removed much of that human friction, and in many ways that was the point. But removing friction also removed the layer that asked whether a transaction should happen at all.

Newton’s bet is that this missing layer can return in a different form. Not through paperwork, not through manual review, and not through slow institutional processes, but through rules written in code and enforced by operators who have something at stake.

That is what makes the idea more serious than a simple compliance tool.

There is a strange compression of time happening here. What once took hours inside traditional financial systems can now happen in seconds. Review, risk assessment, identity checks, policy enforcement, collateral behavior, jurisdictional logic — all of it can be compressed into a short authorization window before execution.

From the user’s perspective, it may feel almost instant.

But that does not mean the work disappeared.

It only means the work moved underneath the surface.

Every approval becomes the result of many small judgments folded into one simple outcome: pass or fail. The transaction either fits the approved pattern, or it does not. It either matches the conditions written into policy, or it stops before value moves.

This is where the idea becomes more complicated.

A policy engine does not read a transaction like a person would. It does not understand intention in a human sense. It checks whether the transaction matches a structure it has been told to recognize. And those structures are not neutral. They are designed by whoever writes the rules.

That means authorization is not just protection. It is also behavior filtering.

The system decides which actions are acceptable before the user may even notice that a decision has been made. The transaction either enters the allowed path or gets blocked at the edge.

The on-chain receipt that follows can be permanent and verifiable. That part is genuinely powerful. It creates a record of what was allowed, what was checked, and how the system responded. Unlike traditional finance, where internal decisions, exceptions, and memos can disappear into private archives, these judgments can become part of a visible and lasting history.

But that permanence also raises a deeper question.

If the authorization layer becomes reliable, fast, and invisible, will users still notice it?

The most powerful systems often become the ones people stop seeing. Nobody thinks about the rules when everything works smoothly. Nobody questions the gate when it opens every time. But once that gate becomes part of the financial infrastructure, it quietly shapes what can be built, what can be automated, and what kinds of behavior are allowed to pass through.

That is why Newton’s position matters.

It is not only building around transactions. It is building around the moment before transactions become final. The moment where intent is judged. The moment where policy becomes execution. The moment where invisible rules begin to shape visible finance.

And the real question is not only whether this makes on-chain finance safer.

The bigger question is who writes the rules that everyone else may eventually move through without noticing.