When Paul Faecks sat in a London office on February afternoon 2025 watching a billion dollars flood into Plasma’s deposit contract in ninety seconds, he experienced what he later called the most stressful moment of his life. Not because something went wrong. Because with that much capital moving that fast, absolutely anything could go wrong. One exploit, one bug, one vulnerability, and Plasma’s entire future would evaporate before the mainnet even launched.

The deposit window closed. The contracts held. No hacks, no exploits, no disasters. In those ninety seconds, Plasma proved something important. People were desperate for better stablecoin infrastructure. They just needed someone to build it properly.

**The Founders Who Saw The Gap**

Paul Faecks didn’t take the obvious path. After working at Deribit Insights analyzing crypto derivatives, most people in his position would have joined a hedge fund or high-frequency trading firm. The money was good. The career trajectory was clear. But Paul resisted what he called the allure of predictability. He wanted independence more than security.

In 2021, he co-founded Alloy, a platform for institutional digital asset operations. The company served clients like the German Stock Exchange and Franklin Templeton. Working at the intersection of traditional finance and crypto gave Paul a front-row seat to the endless compliance procedures, procurement delays, and corporate politics that slowed everything down. Alloy eventually got acquired. Paul described the outcome as fine but not incredible.

The experience pushed him back toward crypto’s core where experimentation and speed still ruled. He’d seen the problems institutions faced trying to use blockchain infrastructure built for other purposes. He understood why stablecoins struggled with efficiency on general-purpose chains. The market needed specialized infrastructure, not another Ethereum clone promising slightly better performance.

Christian Angermayer brought a completely different background to the partnership. As founder of Apeiron Investment Group with over three and a half billion dollars under management, Christian made his name investing in life sciences, fintech, and future technologies. He co-founded companies like atai Life Sciences working on psychedelic treatments for mental health. He produced films including critically acclaimed movies and Netflix hits. He advised political leaders and spoke at global forums.

But Christian had become increasingly involved in crypto, particularly helping Tether build its investment portfolio. Through Apeiron, he introduced Tether to companies like Northern Data and Blackrock Neurotech where Tether became majority shareholder. He understood the stablecoin issuer’s strategic thinking better than almost anyone outside the core team. He saw where Tether’s interests aligned with broader market needs.

When Paul and Christian came together to found Plasma in 2024, they combined technical expertise with strategic connections that few projects could match. Paul understood the infrastructure requirements from building institutional-grade systems. Christian understood the capital and partnership landscape from managing billions across multiple sectors. Together, they identified the opportunity others missed.

**The Tether Connection Nobody Talks About**

Plasma’s relationship with Tether runs deeper than typical blockchain investments. This is functional vertical integration through carefully structured corporate relationships. Paolo Ardoino, CEO of both Tether and Bitfinex, invested as an angel investor and became a vocal champion. Christian manages Tether’s profit reinvestment through Apeiron Investment Group. Bitfinex led Plasma’s Series A funding round. The entire go-to-market strategy centers on USDT with zero-fee transfers.

Paul Faecks publicly pushed back against characterizing Plasma as Tether’s designated blockchain. But the connections are undeniable and strategic. Tether currently profits from reserve yield, approximately thirteen billion dollars in 2024 from Treasury holdings backing USDT’s one hundred sixty-four billion dollar circulation. But the transactional value of billions of daily USDT movements accrues to host blockchains. TRON alone generated over two billion dollars in fee revenue in 2024, primarily from USDT transactions.

From Tether’s perspective, Plasma represents a strategic move to recapture billions in transaction value currently flowing to competitor networks. If significant USDT volume migrates to Plasma, the fees and ecosystem value remain within Tether’s sphere of influence rather than enriching TRON or other chains. The relationship benefits both sides. Plasma gets institutional credibility and guaranteed liquidity. Tether gets infrastructure optimized specifically for their product.

The fundraising trajectory showed this strategic alignment. Bitfinex led an initial three and a half million dollar round in October 2024. Framework Ventures and Bitfinex co-led a twenty-four million dollar Series A in February 2025, with Paolo Ardoino participating alongside major institutions like Mirana Ventures, Cumberland DRW, Flow Traders, Bybit, IMC Trading, Nomura Holdings, and others. Peter Thiel’s Founders Fund announced a strategic investment in May 2025 specifically to accelerate stablecoin adoption in Latin America and the Middle East.

The public token sale in July 2025 attracted massive attention. Users deposited over one billion dollars in stablecoins to earn allocation rights for XPL tokens. The sale targeted fifty million dollars at a five hundred million dollar valuation. Demand reached three hundred seventy-three million dollars, making it seven point four times oversubscribed. One participant reportedly spent one hundred thousand dollars in Ethereum gas fees just to secure their allocation. That level of demand created enormous pressure to deliver on launch.

**The Technical Architecture That Makes It Work**

The zero-fee USDT transfer promise requires sophisticated technical architecture. At the heart sits PlasmaBFT, a consensus mechanism inspired by Fast HotStuff and optimized specifically for high-frequency stablecoin transactions. Understanding how it works reveals why Plasma can compete with established chains.

Traditional Byzantine Fault Tolerant consensus protocols like PBFT face scalability issues because of message complexity. In each phase, nodes must send messages to every other node. This creates quadratic growth in communication overhead as the network expands. HotStuff improved this by reducing communication complexity, enabling linear scaling even as validator counts increase.

PlasmaBFT takes HotStuff’s design further by using only two stages for consensus instead of three. In the Prepare stage, the leader proposes a block and backup validators verify and sign it, forming the first Quorum Certificate. In the Pre-Commit stage, a second QC forms by collecting responses based on the first QC. The Fast Commit happens when the QCs of consecutive blocks connect, confirming the earlier block.

The clever optimization is pipelining that allows parallel processing of multiple rounds. While round v plus two commits block v, it simultaneously pre-commits for block v plus one and prepares for block v plus two. This parallelism increases maximum throughput without sacrificing safety guarantees. The protocol operates under classic BFT security assumptions where the network can tolerate up to one-third of validators being malicious or faulty.

Plasma aims for sub-second block finality with throughput exceeding one thousand transactions per second. These specifications target payment use cases where users expect near-instant confirmation. Waiting fifteen or thirty seconds breaks the experience when someone’s paying at a store or sending money to family across borders.

The execution layer uses Reth, a high-performance Ethereum Virtual Machine implementation written in Rust. Unlike Geth or other clients written in Go, Reth provides both memory safety and performance advantages. The modular architecture splits the full node into independent components including P2P networking, database, EVM execution engine, transaction pool, and RPC server, each implemented as separate libraries.

This modularity enables optimization of individual components without affecting others. Developers can swap out the database layer for better performance without touching the consensus code. The separation creates flexibility as requirements evolve. Full EVM compatibility means any smart contract deployable on Ethereum runs on Plasma without code modifications, removing typical migration friction.

**The Protocol-Level Paymaster Magic**

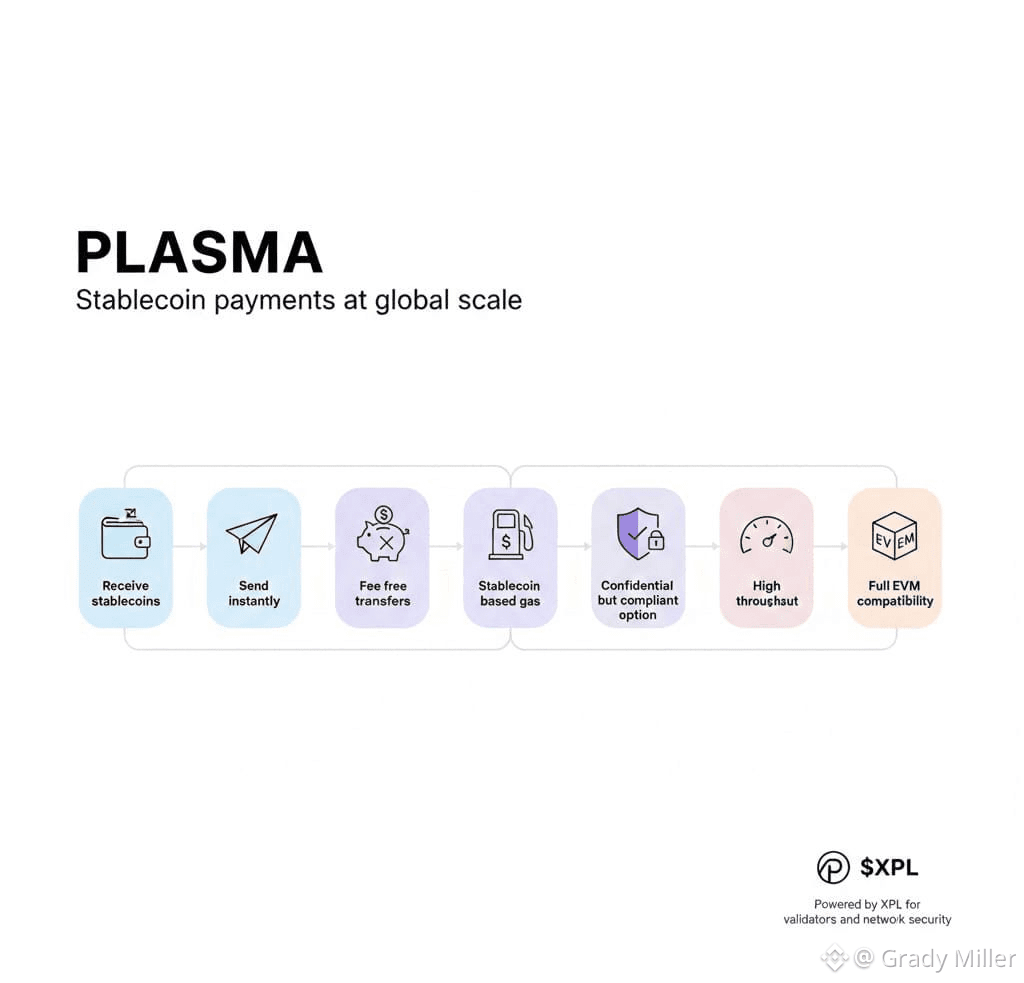

The zero-fee USDT transfers work through a protocol-level paymaster system. On most blockchains, every transaction requires the native token for gas fees. If you want to send USDT on Ethereum, you need ETH for gas. Want to transfer on Polygon, you need MATIC. This creates friction where users must hold multiple tokens just to transact.

Plasma’s paymaster allows the protocol itself to sponsor gas fees for USDT transfers. Users only need USDT in their wallet. The protocol handles gas payment behind the scenes. This abstraction removes a major barrier especially for non-technical users who don’t understand why sending one token requires holding a different token for fees.

The system extends beyond just USDT. Users can pay transaction fees in any whitelisted stablecoin or even Bitcoin through the native bridge. For complex operations like deploying smart contracts, fees get paid in XPL or automatically converted from user-provided stablecoins. The flexibility adapts to different use cases without forcing everyone to acquire and manage the native token.

The economic sustainability question looms. Zero-fee transfers mean the protocol generates no revenue from its primary use case. Plasma must either transition to fee-based transfers once user habits form, cross-subsidize from DeFi ecosystem fees, or receive permanent backing from the three hundred seventy-three million dollars raised. At estimated daily incentive distribution of several million dollars, burn rates are significant. Long-term viability requires converting subsidized growth into sustainable economics.

**Building The Team That Could Execute**

Beyond the founders, Plasma assembled a team with relevant experience across crypto and traditional finance. The hiring strategy focused on people who had built similar systems before rather than just general blockchain developers.

They brought in Firat, who previously founded Turkish crypto exchange and lira-pegged stablecoin issuer BiLira. His experience building payment rails in a market with currency instability and capital controls directly applied to Plasma’s target markets. Jacob Wittman joined as general counsel bringing legal expertise crucial for navigating regulatory requirements across different jurisdictions.

The payments infrastructure needed someone who understood traditional finance integration. They hired someone who had been global head of payments at FTX before spending time at Canadian fintech firm Nuvei. Despite FTX’s eventual collapse, the payments infrastructure team there had built sophisticated systems that processed billions in volume. That expertise transferred to Plasma’s payment architecture.

Security expertise came through hiring someone ranked sixth on the ImmuneFi leaderboard for crypto bug bounties. When you’re building infrastructure to move billions in stablecoins, security cannot be an afterthought. Having someone who professionally finds vulnerabilities reviewing your code before launch reduces risk significantly.

Anonymous contributors river0x and murf joined as DeFi lead and senior product designer respectively. The willingness to hire pseudonymous talent showed Plasma’s crypto-native approach. Many traditional companies would never hire someone they couldn’t identify, but crypto culture recognizes that some of the best builders prefer privacy. Excluding them means losing top talent.

The team grew to around fifty people by mainnet launch, pulling experience from Goldman Sachs, Los Alamos National Laboratory, Blur, and leading blockchains. The diversity of backgrounds mattered. Someone who worked on scientific computing at a national lab brings different problem-solving approaches than someone who built DeFi protocols. Combining those perspectives creates more robust solutions.

**The Bitcoin Security Anchor**

Plasma operates as a Bitcoin sidechain, meaning it’s an independent blockchain cryptographically linked to the Bitcoin network. The connection provides security guarantees that attract institutional adoption. Periodically, Plasma anchors its state roots to Bitcoin’s blockchain by embedding data into Bitcoin transactions using OP_RETURN outputs.

Once confirmed on Bitcoin, Plasma’s corresponding state becomes anchored to Bitcoin’s highly secure and censorship-resistant ledger. This provides strong guarantees against Plasma chain reorganizations extending beyond the checkpoint. Bitcoin’s proof-of-work consensus secures over one hundred billion dollars in market value. Inheriting that security profile gives institutions confidence without requiring Plasma to match Bitcoin’s decentralization directly.

The Bitcoin bridge enables users to move actual BTC into Plasma’s EVM environment through a trust-minimized architecture. Rather than wrapped tokens controlled by custodians, a decentralized network of independent verifiers monitors deposits. When users deposit Bitcoin, validators composed of entities like stablecoin issuers and infrastructure providers verify the transaction meets requirements before minting corresponding assets on Plasma.

The bridge remains under development as one of Plasma’s key roadmap items. Getting it right requires careful security design since bridges represent major attack vectors in crypto. But once operational, direct BTC transfers into an EVM-compatible environment with stablecoin-optimized infrastructure opens new use cases. DeFi protocols can offer Bitcoin collateralized lending for stablecoins. Payment applications can accept Bitcoin and settle in USDT. The flexibility increases utility for both assets.

**The Launch That Shook The Industry**

September 25, 2025 marked Plasma’s mainnet beta launch and the most intense period of Paul Faecks’ career. Within twenty-four hours, two point three billion dollars in total value locked flowed into the ecosystem. Within one week, that figure reached five point six billion dollars, briefly approaching TRON’s DeFi TVL which stood at six point one billion.

The XPL token launched at one dollar and twenty-five cents, peaked at one dollar and fifty-four cents, then settled around one dollar and thirty cents after the launch weekend. The token’s market cap exceeded two point four billion dollars at peak, giving Plasma a fully diluted valuation of ten billion dollars. For comparison, TRON took years to reach similar scale. Plasma achieved it in days.

The rapid growth immediately put pressure on the infrastructure. Teams scrambled to handle user onboarding volumes that exceeded projections. Customer support requests flooded in from users across different time zones and languages. Every component from RPC nodes to database indexing to frontend servers faced loads they hadn’t been tested against. The team worked around the clock addressing issues as they emerged.

TRON’s response came swiftly. On August 29, 2025, even before Plasma’s mainnet, TRON cut energy unit prices by sixty percent from two hundred ten sun to one hundred sun. This reduced USDT transfer costs from over four dollars to under two dollars. Daily network fee revenue dropped from nearly fourteen million dollars to approximately five million. The move acknowledged Plasma as a genuine competitive threat worth sacrificing revenue to counter.

The subsequent months proved more challenging. TVL declined from the peak five point six billion to around one point eight billion by November 2025. The XPL token fell eighty-five percent from its all-time high to around twenty cents. The brutal correction exposed the fundamental challenge of converting incentivized deposits into organic usage. Yield farmers who came for launch rewards left when better opportunities emerged elsewhere.

**What The Numbers Actually Show**

Strip away the hype and examine what Plasma accomplished versus what it promised. The project raised three hundred seventy-three million dollars and launched with two billion in immediate liquidity. Those numbers are real. Major DeFi protocols including Aave, Ethena, Fluid, and Euler deployed on day one. The infrastructure worked without major exploits or downtime. From a technical execution standpoint, the launch succeeded.

The token performance tells a different story. Falling eighty-five percent from peak suggests either the initial valuation was inflated, the market lost confidence in the model, or both. Token price doesn’t always reflect fundamental value especially in crypto where speculation dominates. But sustained decline indicates problems retaining users and capital.

Transaction volume provides clearer signals. Plasma reports USDT volumes already exceeding one trillion dollars annualized. If accurate, that’s substantial activity suggesting real usage beyond just depositing and withdrawing. However, volume can be misleading. Wash trading, arbitrage bots, and incentivized activity inflate numbers without representing genuine payment adoption.

The key metric becomes retention. Are users who tried Plasma staying, or did they extract launch incentives and leave? Are new applications launching on the platform, or has development activity stagnated? Is DeFi usage growing organically or remaining flat? These indicators determine whether Plasma built sustainable infrastructure or just another over-hyped launch.

**Comparing To TRON’s Playbook**

TRON built its stablecoin dominance gradually over years. They optimized fees low enough to attract users without going to zero. They focused relentlessly on emerging markets where stablecoin utility was highest. They worked with exchanges and wallets to make USDT on TRON the default option. They built developer tools and documentation making integration straightforward. Most importantly, they sustained their approach long enough for network effects to compound.

Plasma chose a different strategy. Launch with massive liquidity and name recognition. Offer zero fees to undercut competition immediately. Secure institutional backing that provides credibility and capital. Build consumer products like Plasma One that deliver complete experiences rather than just infrastructure. Target the same emerging markets but with localized teams and partnerships.

The aggressive approach creates faster initial growth but requires solving sustainability quickly. TRON’s fee revenue funds ongoing development and operations. Plasma’s zero fees mean burning through venture capital while figuring out alternative revenue sources. The DeFi ecosystem could provide fees if volumes grow large enough. The XPL token could accrue value if the network achieves sufficient adoption. But both require converting current users into long-term participants.

TRON had the advantage of emerging when stablecoin infrastructure was primitive. They competed against Ethereum with fifty dollar gas fees during peaks. Offering few-dollar transfers was transformative. Plasma launches into a market where TRON already optimized costs after seeing the competitive threat. The incumbent adapted faster than new entrants typically expect.

**What Comes Next For Specialized Chains**

Plasma represents a broader trend of specialized blockchain infrastructure. Rather than general-purp