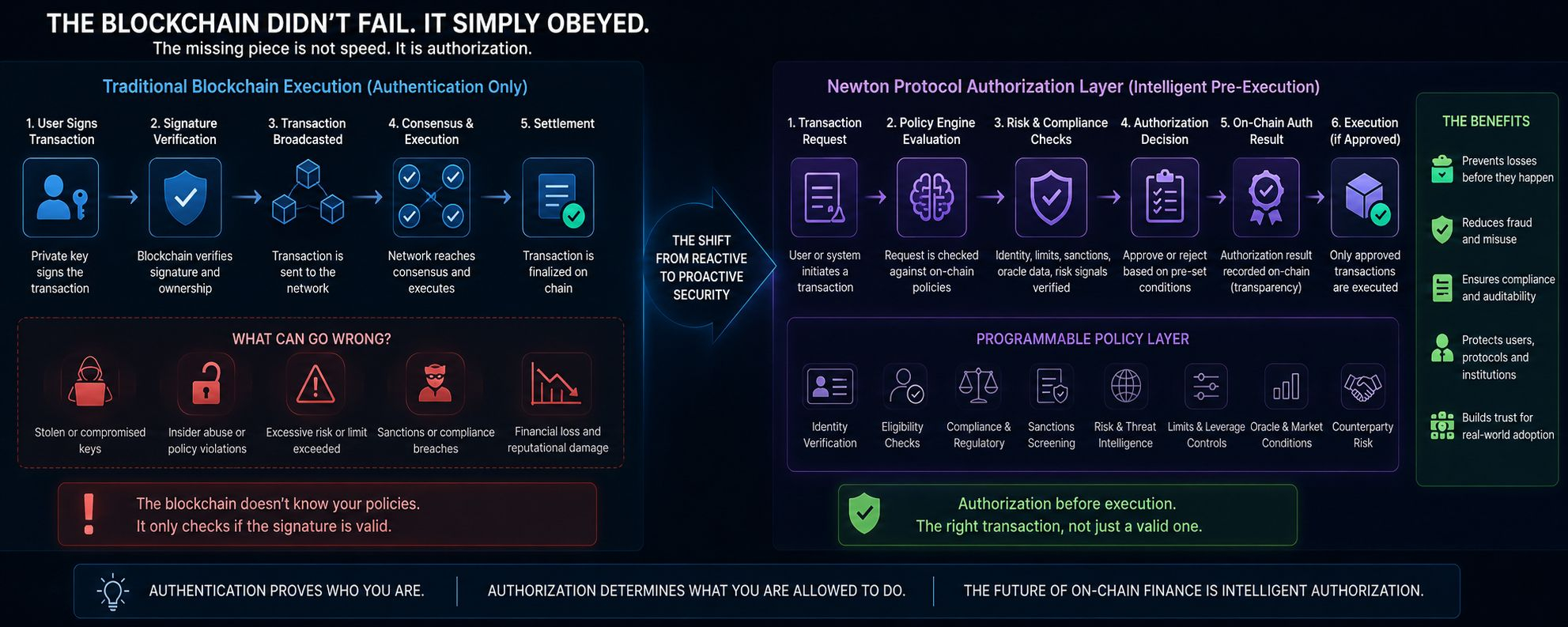

@NewtonProtocol Every time a major crypto exploit makes headlines, I notice the discussion usually follows the same pattern. People immediately want to know who controlled the wallet, whose private key was used, or how the attacker managed to sign the transaction. Those questions are understandable, but I think they focus on only part of the bigger picture. Whether the incident involves a bridge, an exchange, or a DeFi protocol, the blockchain normally behaves exactly as it was designed to. It checks the signature, verifies that the transaction is valid, reaches consensus, and processes the request. From the network's perspective, nothing has gone wrong. It simply follows the rules it was given.

The more I think about it, the more I believe this is where many people misunderstand blockchain security. A digital signature is excellent at proving ownership and confirming that the correct key authorized an action. What it cannot do is determine whether that action is actually appropriate. It doesn't know if the transfer breaks an organization's internal policy, exceeds a risk threshold, violates compliance requirements, or creates unnecessary financial exposure. The blockchain isn't built to make those decisions. Its job is to execute valid instructions, not to question their purpose.

That distinction becomes increasingly important as blockchain technology moves beyond retail trading. Today, decentralized finance is handling far more than token swaps. Stablecoins, tokenized real-world assets, institutional portfolios, treasury operations, and autonomous software agents are becoming part of the same ecosystem. As the value secured on-chain continues to grow, relying only on authentication becomes less practical. Confirming who initiated a transaction is useful, but protecting billions of dollars requires another layer that determines whether the transaction should be allowed before any assets actually move.

Traditional financial systems recognized this challenge many years ago. When someone pays with a bank card, approval is not based solely on whether the card is genuine. Behind every successful payment, multiple systems quietly evaluate the transaction. They consider fraud indicators, spending patterns, merchant reputation, transaction limits, compliance obligations, and several other risk signals before approval is granted. Identity alone is never the final decision. Authorization is what ultimately determines whether the payment proceeds.

This is why I find the approach behind Newton Protocol particularly interesting. Rather than concentrating only on monitoring activity after settlement, it introduces an authorization layer that evaluates transactions before execution. Every request can be checked against programmable policies that include identity verification, eligibility requirements, regulatory compliance, sanctions screening, security intelligence, leverage limits, oracle conditions, and counterparty risk. Instead of simply reporting suspicious behavior after assets have already changed hands, the protocol provides an on-chain authorization result that indicates whether predefined conditions have been satisfied before settlement begins.

I think this represents a meaningful change in how blockchain infrastructure can evolve. Monitoring systems are valuable because they explain what has already happened, but they usually operate after the damage is done. Authorization serves a different purpose. It influences outcomes before execution takes place. One creates a historical record, while the other actively reduces the possibility of preventable mistakes or unauthorized activity.

Blockchain technology has already proven that it can execute financial transactions without relying on centralized intermediaries. The next stage of innovation may not be about making transactions faster or cheaper. It may be about making them more intelligent through programmable policies that balance decentralization with practical risk management. If that direction continues, the most important question in on-chain finance may no longer be who signed the transaction. Instead, it may become whether that transaction met every condition required to deserve execution in the first place.