MicroStrategy, is it really the next bomb?—An in-depth analysis of the hidden risks of the 'largest listed cryptocurrency holding company'

A storm is approaching, if we say that the cryptocurrency market from 2020 to 2024 has a 'super bull market engine',

There is no doubt that it is called MicroStrategy.

This company used to make money by selling software, and now it has become the world's largest 'corporate treasury' by continuously borrowing money to buy Bitcoin.

However—when Bitcoin pulls back, financing costs rise, and index companies want to kick it out, the mNAV premium disappears...

MicroStrategy is facing real systemic pressure for the first time.

Is it the next bomb? Today, Yongqi will clarify it completely.

One, what is MicroStrategy? A software company? Or a Bitcoin fund?

On the surface, MicroStrategy is a traditional business intelligence software company.

But since Michael Saylor personally led the 'ALL IN Bitcoin' effort in 2020, its positioning has completely changed: software sales account for a small part, the company's cash flow cannot support hundreds of billions of dollars in BTC holdings, stock price fluctuations completely follow BTC, business profitability has almost no impact on valuation, and its balance sheet is highly tied to Bitcoin.

In summary: MicroStrategy is no longer a software company but a 'semi-official fund' that uses stocks + debt to leverage Bitcoin.

The problem is: this model is glamorous but dangerous.

Two, holding logic: why does it 'buy more as prices rise, become dangerous as prices drop'?

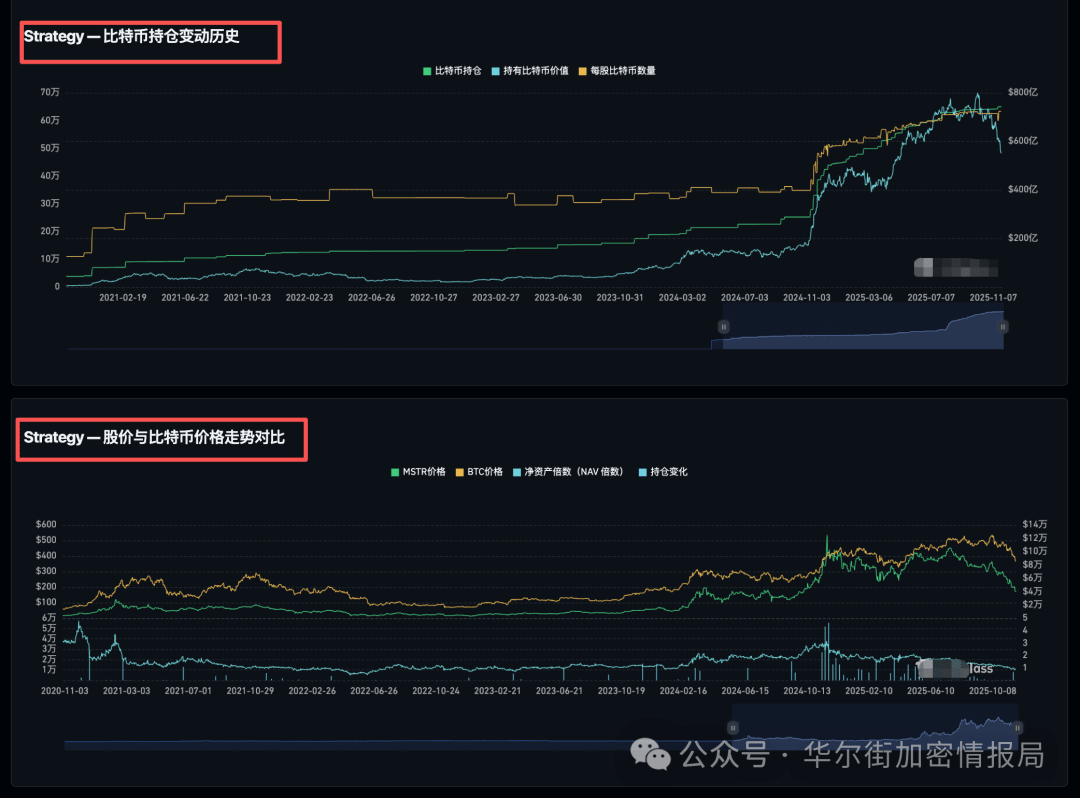

1) Huge position size.

As of November 2025: MicroStrategy holds approximately 649,870 BTC; the book value exceeds $66 billion; the company's market value is only about $50.9 billion.

This means: its 'Bitcoin value' is greater than the overall market value of the company—the market is unwilling to pay a premium for it.

2) Average cost $74,433.

When Bitcoin drops to $80,000: only 8% remains of the cost; the market no longer trusts its 'buy logic'; stock prices fall faster than BTC.

Because: it is an amplifier for BTC: it doubles when it rises and doubles when it falls.

3) The critical point for the 'positive cycle' turning into a 'negative cycle' is appearing.

MicroStrategy's model is:

Financing → buying BTC → stock price rises → refinancing → buying BTC again.

This requires two prerequisites: stock prices have a premium (mNAV > 1); the market continues to believe it can finance.

But the current issue is: has the premium disappeared? Is the stock price discounted? Is the cost of debt rising? Is BTC volatile? Is the difficulty of financing increasing?

This is the signal that the 'positive cycle' may reverse into a 'negative cycle'.

Three, financing logic: why its leverage.

Much bigger than you think?

1) It does not use profits to buy BTC, but rather 'borrows money to buy'.

MicroStrategy's funds for buying BTC come from: stock issuance, convertible bonds, perpetual preferred shares, and bonds. I have detailed MicroStrategy's financing in previous articles: MicroStrategy leveraged $42 billion off-market to buy BTC, will it become a bomb targeted by Wall Street capital?

Latest example: issuing $710 million perpetual preferred shares, followed by six convertible bonds maturing from 2027 to 2032, while its 'cash and equivalents' are only $54.3 million.

In other words: it buys BTC relying on financing, its life is tied to financing.

2) The debt snowball is growing larger.

As BTC weakens and stock prices drop: refinancing becomes difficult; debt costs rise; lifeline tools become expensive.

It will form: unable to repay old debts → hard to issue new debts → the chain may break; this is what the market fears the most.

3) Once the financing chain breaks, it is no longer a 'leverage BTC amplifier' but becomes a 'source of forced selling pressure for Bitcoin'.

Of course, there is still a long way to go before forced selling of cryptocurrencies occurs. But risks are accumulating.

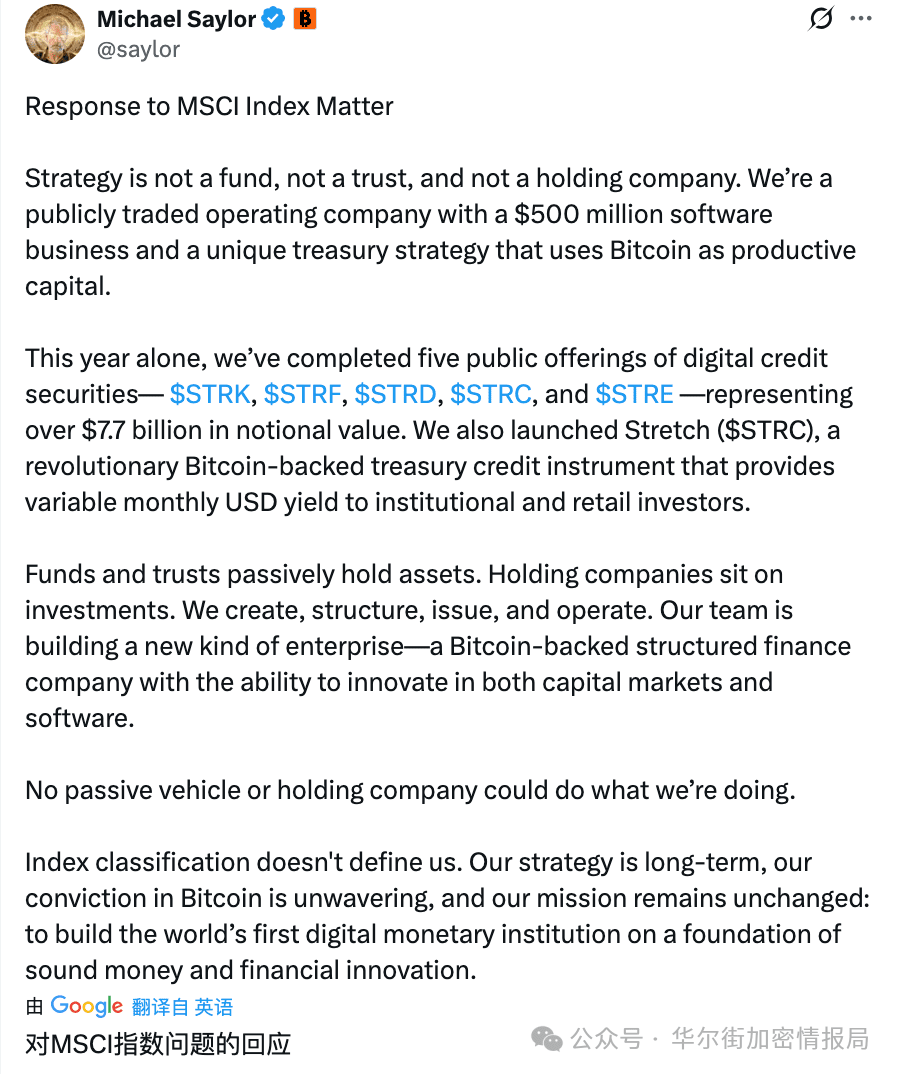

Four, being excluded from the MSCI index: this could be.

The key straw that broke the camel's back.

MSCI (Morgan Stanley Capital International), as a global leader in index provision, has its indices (such as MSCI USA, MSCI World, etc.) widely used in ETFs, mutual funds, and benchmark investments, affecting trillions of dollars in capital flow. Why is MSCI doing this?

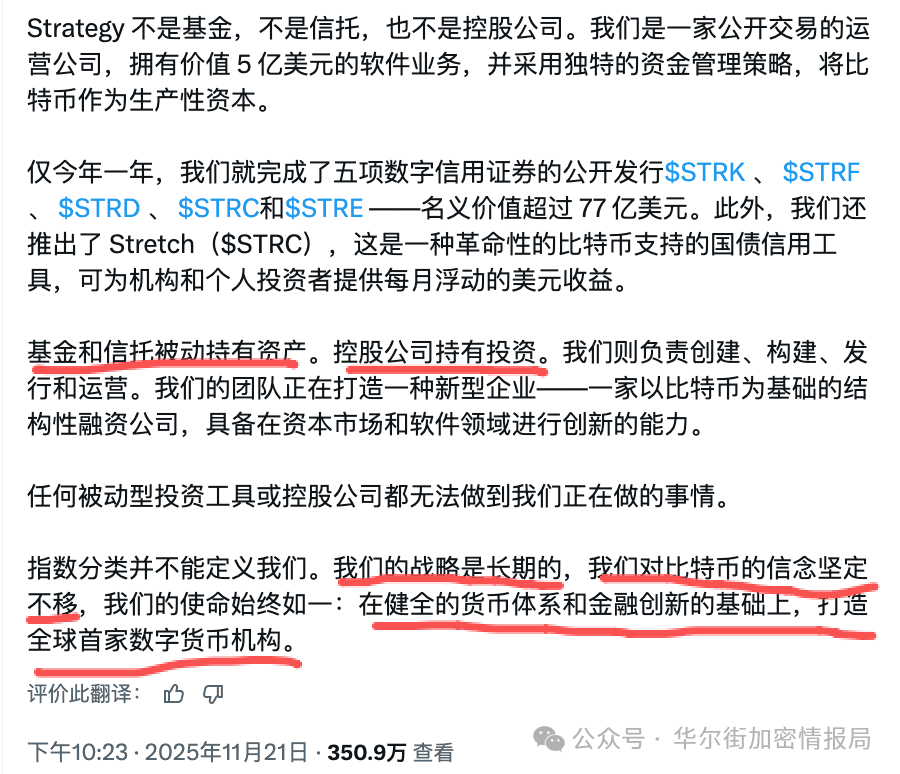

Core reason: MSCI believes such companies (like MicroStrategy, Riot Platforms, etc.) are no longer traditional 'operating companies' but are more like 'investment vehicles'.

The value of these companies mainly relies on their holdings of crypto assets, rather than core business operations, which does not align with the original intent of the MSCI index—to focus on real economic activities and equity benchmarks. If the exclusion takes effect, passive funds tracking the MSCI index (such as ETFs) will be forced to sell these stocks.

This is the biggest structural risk facing MicroStrategy.

1) What happened?

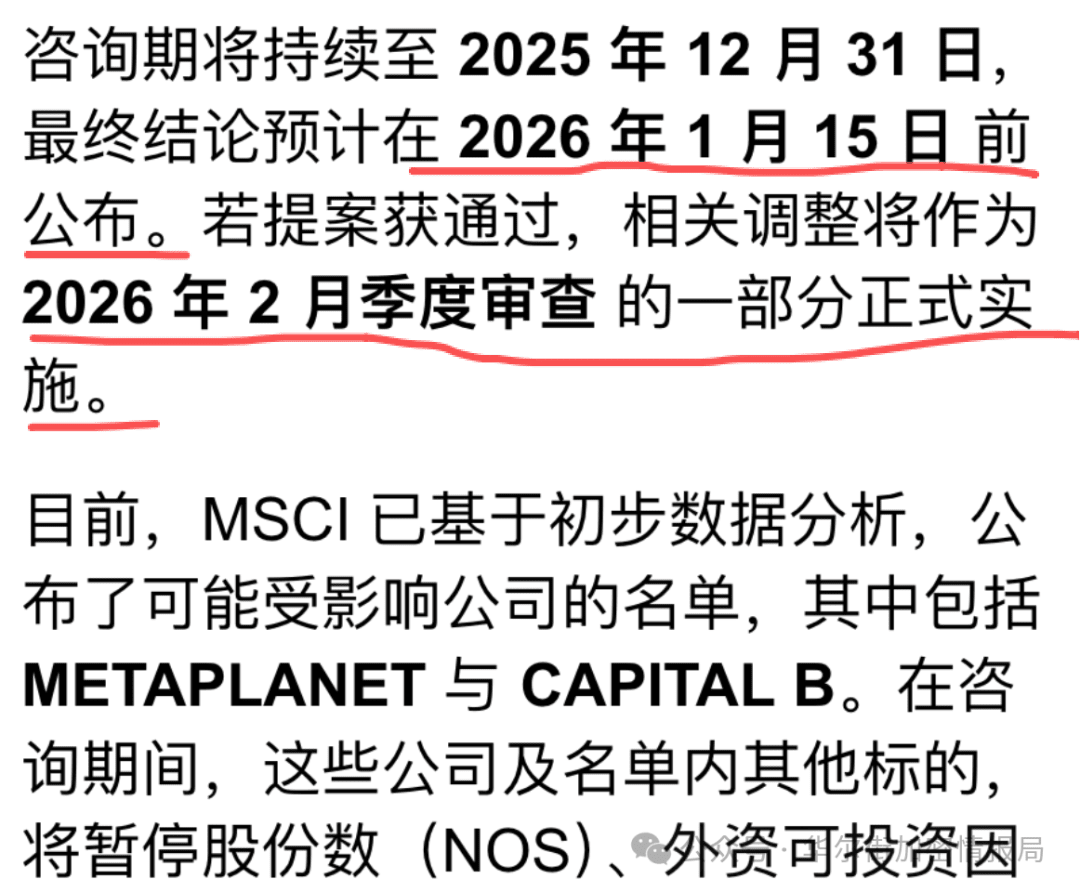

MSCI announced it is seeking opinions on whether to exclude companies with 'digital asset holdings exceeding 50%' from the MSCI index system. MicroStrategy's Bitcoin holdings have long exceeded 50%.

If the announcement lands in January 2026:

2) Possible selling pressure: up to $9 billion.

JP Morgan analysis: MSCI alone will trigger approximately $2.8 billion in passive selling pressure;

If the Nasdaq, Russell, and other indices follow → total outflow could reach $9 billion.

Passive funds can only sell mechanically. This means: MicroStrategy does not choose to fall; instead, it is forced to fall by the system.

3) Why is index exclusion a 'structural negative'?

Because: active funds may reduce their positions in advance, passive funds automatically sell: stock prices drop → mNAV lower → financing harder → can't continue to buy BTC: the positive cycle completely stops.

More critically, this is the first time the traditional financial system has 'officially' questioned the legality and investability of corporate cryptocurrency holding models.

Five, all risks are accumulating: this is not a single-point problem.

But it is a chain reaction.

Will MicroStrategy's encounter with MSCI brakes really collapse the Bitcoin market?

MicroStrategy is essentially: a company that leverages debt issuance and market faith to buy $BTC. As long as the financing channel is fine, it can continue to leverage; and now MSCI is coming to suppress this leverage, which will obviously affect the company's liquidity, financing ability, and market pricing.

MicroStrategy's story is: a publicly traded company leveraging Bitcoin faith, when you buy it, you are actually buying Bitcoin + company leverage + financing structure.

The MSCI proposal will indeed limit MicroStrategy's financing ability, but in the short term, it will not trigger forced liquidation and does not constitute substantial selling pressure. Because the probability of forced selling is very low, once forced selling occurs, it proves that MicroStrategy itself does not believe the story it tells anymore, and they can announce GG.

MicroStrategy's logic is not about blowing up, but about growth being 'policy-limited'. Whales will not die; they just can't run fast anymore.

The market's panic far exceeds the real risks, but this is a 'structural noise' that will repeatedly ferment before 2026.

By stringing this content together, a complete chain will be revealed.

① BTC volatility → leads to MicroStrategy stock price falling more than BTC.

② Stock price drops → mNAV premium disappears → leads to the market unwilling to provide cheap financing for it.

③ Expensive / insufficient financing → leads to reduced ability to purchase BTC.

④ Reduced purchasing power → means its 'core story: buy more as prices rise' is no longer valid.

⑤ MSCI index exclusion → triggers structural forced selling pressure.

⑥ Structural selling pressure → further lowers stock prices and premiums, entering a negative feedback loop.

If the accumulation continues: global interest rates remain high, risk assets are generally under pressure, Bitcoin is in mid-term volatility.

The MicroStrategy model has indeed reached a phase of systemic risk that cannot be ignored for the first time.

Six, will MicroStrategy explode? When will it explode?

What does it mean to explode?

First, the most critical point: it will not explode in the short term. But it has shown a 'possible explosion' path for the first time.

Possible trigger points include:

(1) Index exclusion takes effect (January 2026), this is the maximum structural selling pressure.

(2) BTC continues to fall towards the $75,000–68,000 range: close to its financing safety line for a large number of chips.

(3) The market gives no premium at all, the financing chain is blocked: the 'negative cycle' is officially initiated.

(4) Debt concentration maturity, liquidity depletion: unable to replenish through preferred shares / convertible bonds.

Seven, if it really explodes, what does it mean for the cryptocurrency world?

1) Bitcoin will face 'non-economic selling pressure'.

If it is forced to sell cryptocurrencies, it is not because of a bearish outlook but because of financing being locked. This type of selling pressure often causes significant damage.

2) The corporate cryptocurrency holding model will face regulatory reflection.

This could directly impact companies such as Riot, Marathon, Hut 8, CleanSpark, and other future companies that want to go public by 'holding cryptocurrencies'.

3) The 'tolerance' of US stocks to BTC assets will be repriced.

Retail investors love to watch Saylor's passionate speeches, but Wall Street only looks at: risks, liquidity, index weight, debt structure.

The 'institutional risk' of the MicroStrategy model is being reassessed.

Eight, conclusion: MicroStrategy is not a scam.

But it indeed increasingly resembles a bomb.

It must be emphasized: MicroStrategy is not a Ponzi scheme, nor is it a scam. It is just an extremely aggressive corporate strategy.

But now: the market no longer gives it a premium, index providers are starting to take action, debt costs are rising, BTC is entering a mid-cycle volatility, and financing logic shows cracks.

These factors have combined to turn it from a 'super bull market engine' into a systemic risk point that must be seriously evaluated.

The next six months (especially January 2026) will be its critical testing period.

Deep observation · Independent thinking · Value goes beyond price.

Star #Wall Street Crypto Intelligence Bureau, don't miss good content⭐

Finally, many of the viewpoints in this article represent my personal understanding and judgment of the market and do not constitute investment advice for you.