Written by: Oluwapelumi Adejumo

Translated by: Saoirse, Foresight News

On November 10, when Uniswap's administrators submitted the 'UNIfication' proposal, the document read more like a corporate restructuring than a protocol update.

The proposal plans to activate previously unused protocol fees, circulating funds through a new on-chain treasury engine, and using the proceeds to purchase and destroy UNI tokens. This model is akin to stock buyback programs in traditional finance.

One day later, Lido also launched a similar mechanism. Its decentralized autonomous organization (DAO) proposed to establish an automatic buyback system: when the price of Ethereum exceeds $3000 and the annual income exceeds $40 million, the excess staking rewards will be used to repurchase its governance token LDO.

This mechanism deliberately adopts a 'counter-cyclical' strategy—stronger in bull markets and more conservative when the market environment tightens.

These initiatives collectively mark a significant transformation in the DeFi space.

In recent years, the DeFi space has been dominated by 'meme tokens' and incentive-driven liquidity activities; now, leading DeFi protocols are repositioning around core market fundamentals like 'revenue, fee capture, and capital efficiency.'

However, this shift also forces the industry to confront a series of thorny issues: ownership of control, how to ensure sustainability, and whether 'decentralization' is gradually yielding to corporate logic.

The new financial logic of DeFi

For most of 2024, DeFi's growth mainly relied on cultural fervor, incentive programs, and liquidity mining. Recent moves such as 're-enabling fees' and 'implementing buyback frameworks' indicate that the industry is attempting to bind token value more directly to business performance.

Taking Uniswap as an example, its initiative to 'plan to destroy up to 100 million UNI tokens' redefines UNI from a purely 'governance asset' to an asset more akin to a 'protocol economic equity certificate'—even though it lacks the legal protections or cash flow distribution rights of equity.

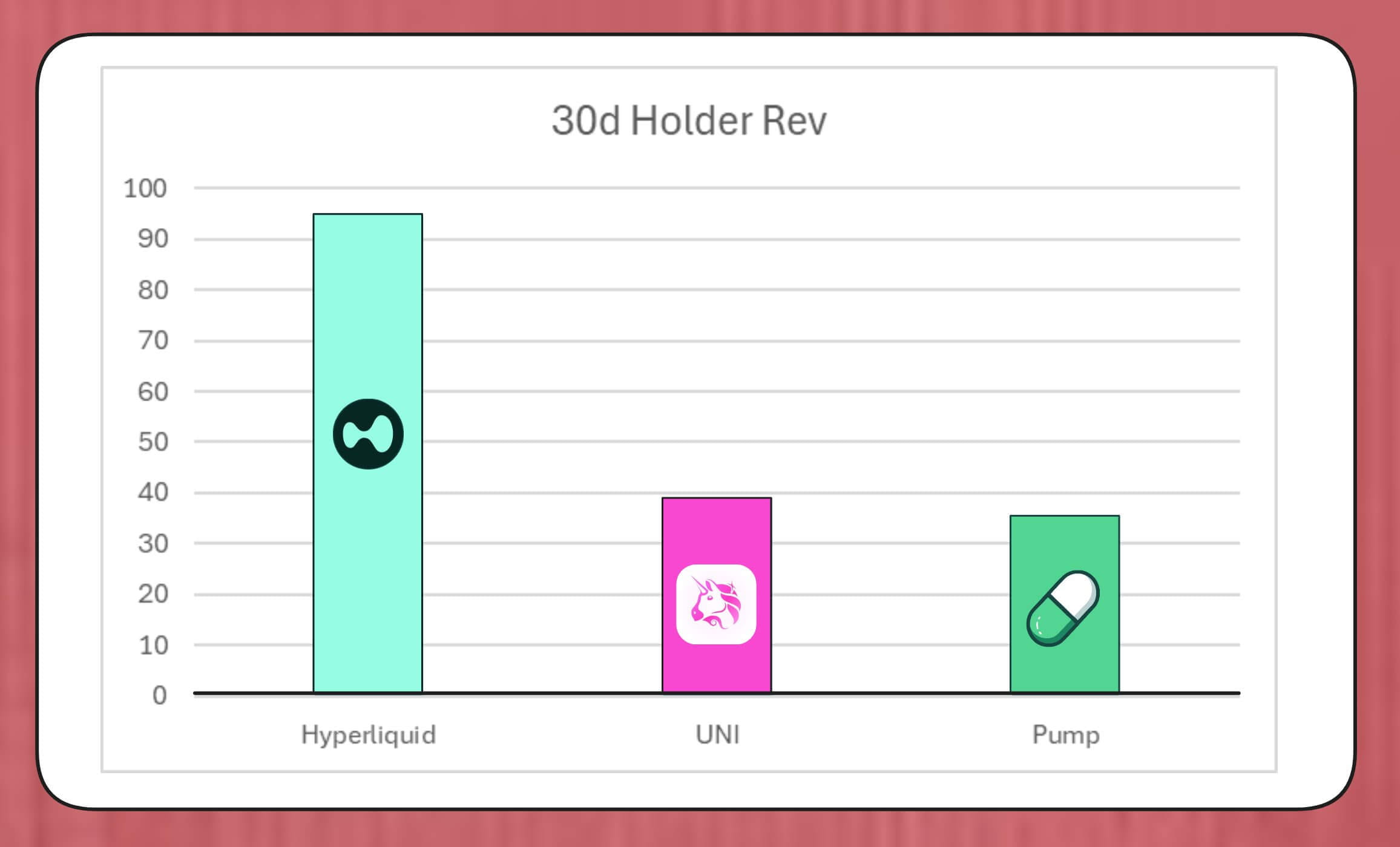

The scale of such buyback plans should not be underestimated. MegaETH lab researcher BREAD estimates that, based on current fee levels, Uniswap could generate about 38 million dollars in buyback capacity each month.

This amount will exceed the buyback speed of Pump.fun, but is lower than Hyperliquid's monthly buyback scale of about 95 million dollars.

Comparison of token buybacks of Hyperliquid, Uniswap, and Pump.fun (Source: Bread)

Lido's simulation mechanism structure shows that it can support a buyback scale of about 10 million dollars annually; the repurchased LDO tokens will be paired with wstETH and placed into liquidity pools to enhance trading depth.

Other protocols are also accelerating similar initiatives: Jupiter will use 50% of its operating income for JUP token buybacks; dYdX will allocate a quarter of network fees to buybacks and validator incentives; Aave is also formulating specific plans, intending to invest up to 50 million dollars annually to promote buybacks through treasury funds.

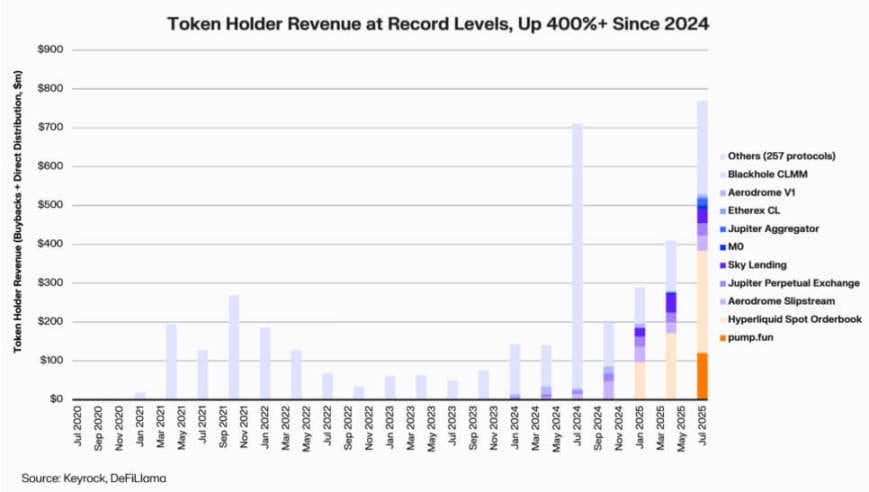

Keyrock data shows that since 2024, dividends for token holders linked to income have increased more than fivefold. In just July 2025, the total spending or allocation by various protocols on buybacks and incentives reached about 800 million dollars.

DeFi protocol holders' income (Source: Keyrock)

As a result, about 64% of the income from leading protocols now flows back to token holders—this contrasts sharply with the previous cycle of 'prioritizing reinvestment, then distribution.'

Behind this trend is a new consensus forming in the industry: 'scarcity' and 'recurring income' are becoming the core of the DeFi value narrative.

Institutionalization of token economics

The wave of buybacks reflects the deepening integration of DeFi with institutional finance.

DeFi protocols have begun to adopt traditional financial metrics such as 'price-to-earnings ratio', 'yield threshold', and 'net distribution rate' to convey value to investors—who are also viewing DeFi projects in the way they assess growth-oriented companies.

This integration provides fund managers with a universal analytical language but also brings new challenges: the original design intent of DeFi did not include institutional requirements such as 'discipline' and 'information disclosure', yet the industry now needs to meet these expectations.

It is worth noting that Keyrock's analysis has pointed out that many buyback plans are heavily reliant on existing treasury reserves rather than sustainable recurring cash flows.

This model may support token prices in the short term, but its long-term sustainability is in doubt—especially in a market environment where 'transaction fee income is cyclical and often linked to token price increases.'

In addition, Blockworks analyst Marc Ajoon believes that 'autonomously decided buybacks' usually have limited market impact and may lead protocols to face unrealized losses when token prices fall.

In light of this, Ajoon advocates establishing a 'data-driven automated adjustment system': allocate funds when valuations are low, reinvest when growth indicators are weak, and ensure that buybacks reflect true operational performance rather than speculative pressure.

He stated:

'As it stands, buybacks are not a panacea... Due to the existence of the 'buyback narrative', the industry blindly places it above other paths that may bring higher returns.'

Jeff Dorman, Chief Investment Officer of Arca, holds a more comprehensive view.

He believes that corporate buybacks will reduce the number of circulating shares, but tokens exist in a special network—its supply cannot be offset by traditional restructuring or merger activities.

Therefore, burning tokens can drive the protocol towards a 'fully distributed system'; however, holding tokens also allows for future flexibility—if demand or growth strategies require, new tokens can be issued at any time. This duality makes the capital allocation decisions in DeFi more influential than decisions in the stock market.

New risks emerge

The financial logic of buybacks is simple and direct, but its impact on governance is complex and far-reaching.

Taking Uniswap as an example, its 'UNIfication' proposal aims to transfer operational control from the community foundation to the private entity Uniswap Labs. This trend towards centralization has raised alarms among analysts who believe it may replicate the hierarchical structure that decentralized governance should avoid.

In response, DeFi researcher Ignas pointed out:

'The original vision of cryptocurrency 'decentralization' is struggling.'

Ignas emphasized that over the past few years, this 'centralization tendency' has gradually emerged—the most typical example being that DeFi protocols often rely on 'emergency shutdowns' or 'core team accelerated decision-making' when addressing security issues.

In his view, the core of the problem is: even if 'concentrating power' has economic rationality, it will damage transparency and user participation.

However, supporters counter that this concentration of power may be a 'functional necessity' rather than an 'ideological choice.'

Eddy Lazzarin, Chief Technology Officer of venture capital firm a16z, described Uniswap's 'UNIfication' model as a 'closed-loop model'—in this model, the income generated by decentralized infrastructure flows directly to token holders.

He added that the DAO will still retain the power to 'issue tokens for future development', thereby achieving a balance between flexibility and financial discipline.

'The tension between 'distributed governance' and 'executive decision-making' is not a new issue, but its financial impact has now expanded significantly.

Currently, the treasury size managed by leading protocols reaches hundreds of millions of dollars, and their strategic decisions can significantly impact the entire liquidity ecosystem. Therefore, as the DeFi economy gradually matures, the focus of governance discussions is shifting from 'decentralized ideals' to 'actual impact on the balance sheet.'

The maturity test of DeFi

The wave of token buybacks indicates that decentralized finance is evolving from a 'free experimental phase' to a 'structured, metric-driven industry.' The 'free exploration' that once defined the field is gradually being replaced by 'cash flow transparency', 'performance accountability', and 'alignment of investor interests.'

However, maturity also brings new risks:

Governance may lean towards 'central control';

Regulatory agencies may view buybacks as 'real dividends', leading to compliance controversies;

Teams may shift their focus from 'technological innovation' to 'financial engineering', neglecting core business development.

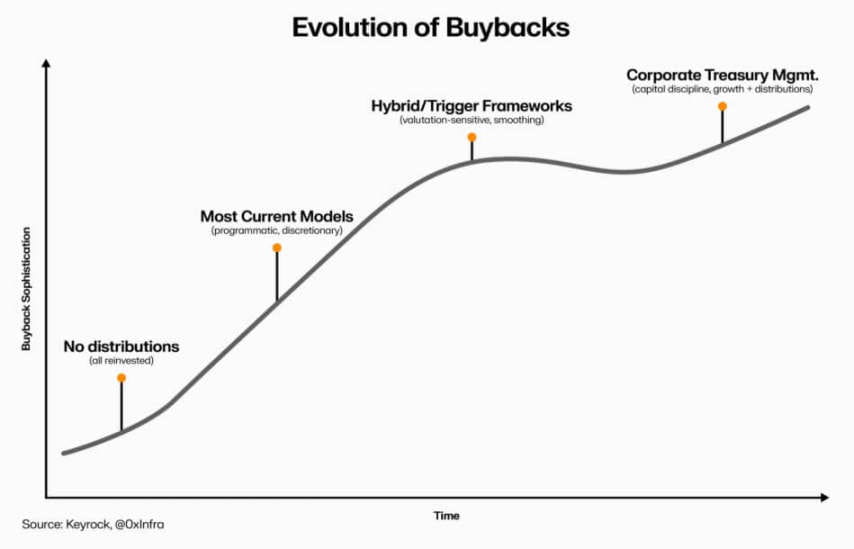

The durability of this transformation depends on choices at the executive level:

'Programmatic buyback models' can implant transparency through on-chain automation while retaining decentralization characteristics;

'Autonomous buyback frameworks' may be implemented more quickly but could undermine credibility and legal clarity;

'Hybrid systems' (linking buybacks with measurable and verifiable network metrics) may be a compromise, but there are currently few cases in the actual market that prove to be 'resilient.'

The evolution of DeFi token buybacks (Source: Keyrock)

But one thing is clear: the interaction between DeFi and traditional finance has surpassed 'simple imitation.' Now, the field is integrating corporate management principles such as 'treasury management', 'capital allocation', and 'balance sheet prudence' while retaining its 'open-source foundation.'

Token buybacks are a concentrated manifestation of this integration—they combine market behavior with economic logic, driving DeFi protocols to transform into 'self-funded, income-oriented organizations': accountable to the community and measuring success by 'execution results' rather than 'ideology.'