The article reposts a piece from Wu that claims last year's article is not original. The content revealed in the article is identical to that of MYX's malicious fund that harvested 67,000 U a couple of days ago. The article gives examples of harvesting every 8 hours, but in reality, MYX harvests funding fees every hour. The article concludes by stating that being a fund manager is not charity; the coins bought are neither gold nor BTC. Ultimately, profits must come from selling, but the final sell-off is not something retail investors can detect. It may suddenly drop by -80% in the middle of the night while you’re sleeping, leaving those who want to follow the trend with no time to react. Currently, the malicious fund harvests funding fees every hour, comfortably waiting for shorts to hand over money. When everyone follows the trend and eats the funding fees with the fund manager, they suddenly sell off, harvesting the longs. The best operation for retail investors is to avoid these manipulated coins by malicious funds. Both longs and shorts will ultimately be harvested. Treasure your capital and stay away from malicious funds!#MYX

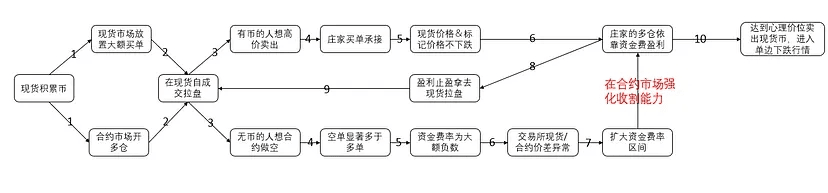

The author has worked in relevant overseas institutions, mainly focusing on risk management at the trading level, and has had more direct or indirect contact with large market makers, project parties, and institutional users. Recently, there have been many instances of small-cap contracts being pulled up, and I will share my experience to decode and discuss how project parties, market makers, and institutional investors passively conduct market making in the spot and contract limits, as well as why it constitutes unfair competition against retail investors.

This article is not aimed at R***, I just randomly picked a project with obviously abnormal data related to the secondary market, which makes it easier to argue.

This article discusses a common strategy for manipulating the prices of spot and contract coins, which may involve the project party's own market value management team, professional market makers, or large retail investors. Therefore, the following text will use the term 'speculator' that everyone likes to refer to them uniformly.

1. Simple process first written out.

2. Phenomenon

Do you often see the following unreasonable situations at exchanges?

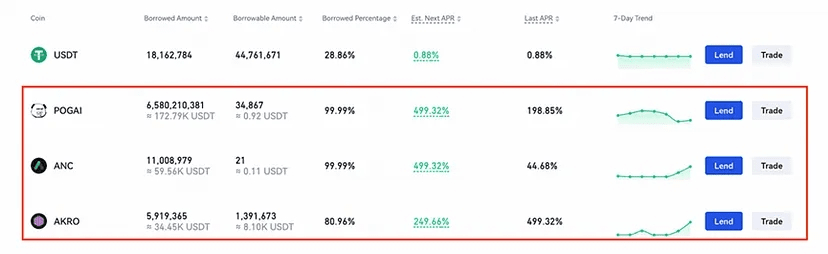

Phenomenon 1: Low transaction volume on-chain and in the spot market, but high transaction volume in contracts.

Taking Gate as an example, the trading volume of contracts is about 60 times that of the spot market.

Phenomenon 2: Prices are soaring but trading volume is gradually declining?

Prices keep rising, but trading volume is decreasing, and MACD is obviously showing a top divergence.

Phenomenon 3: The ratio of buy and sell orders in the spot and contract markets is completely opposite, resulting in a negative funding rate.

Soaring prices lead users to collectively short, but without coins in hand, they can only open short positions in contracts. Therefore, there is a completely opposite market sentiment between the spot and contract markets.

The completely opposite market sentiment has caused the funding rate to reach -0.66%, which is settled every 8 hours, so over 24 hours it is -1.98%.

For example, trading derivatives (contracts) is like buying and selling houses. I am a real estate developer, and my houses mainly serve wealthy person A, who buys all the buildings in my development at once. The pricing power only exists between me and A; we are the supply and demand sides that influence house prices.

Although B is not the homeowner, he believes that the housing prices of this property will fall. Therefore, B takes out 1 million to bet against A, believing that A's investment will definitely lose money. B is unlikely to succeed because the circulating price of the house is controlled by me and A, and only the transactions between me and A will truly affect the circulating price; as long as I and A agree on the transaction price, B is sure to lose. The bet between B and A is similar to derivatives trading and will not affect the circulating price of the spot.

Even if B thinks the house price is overvalued and is actually worth 1 yuan per square meter, it is impossible to realize this because his transaction is not a spot transaction but a derivatives transaction. And derivatives trading bets on the spot price, so those who control the spot price (me and A) can largely determine the derivatives trading.

In the above example, the real estate developer is the project party, 'A' is the speculator who controls the circulating supply of the spot (who may control the spot price), and B is the contract user.

This is also why it is often said that naked short selling in the derivatives market is a very dangerous behavior.

3. Some essential knowledge about contracts that must be known.

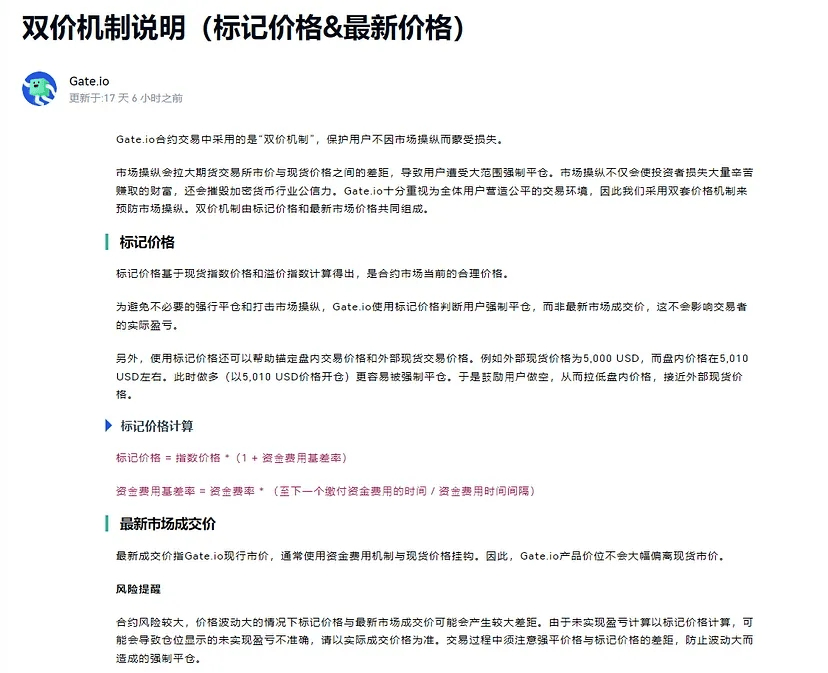

Knowledge Point 1: What are the marked price and latest transaction price of the contract?

A contract has two prices: the latest transaction price and the marked price. Users generally default to using the latest transaction price when closing positions. Liquidations use the marked price, which is calculated using the latest transaction price of the external spot market to objectively reflect the price situation.

In other words, as long as the spot price is controlled, the marked price can be controlled, and thus it can control whether the contract market gets liquidated.

Knowledge Point 2: What is the funding rate of the contract?

To ensure that the latest transaction price of the contract does not decouple from the latest transaction price of the spot, every 8 hours, funding fees are paid from long position users to short position users, or from short position users to long position users, and the gap between the latest transaction price of the spot and the latest transaction price of the contract is narrowed.

Knowledge Point 3: What is the circulating market value of a project?

The economic mechanism of a project specifically needs to look at the white paper. Generally, it will be divided into project parties, early investors, community airdrops, project treasury, etc. If a project's white paper is not transparent enough, it is more likely to be manipulated. For example, while the white paper gives the community enough freedom, it also gives market makers/institutional investors enough freedom—they can acquire low-priced chips at low levels without being diluted because there is no issuance or linear unlock mechanism.

4. Small-cap contract control process.

Step 1: Find a project with a relatively low circulating market value that has opened a contract on a centralized exchange.

Generally, small projects with a circulating market value of 1 - 10 million USD are chosen, with contract leverage typically between 20 - 30 times.

Step 2: Prepare funds, with funds > external circulating market value.

Million-level retail investors prefer to control small-cap contracts. Taking S*** as an example, with a circulating market value of 5 million. During a long decline, if the speculator acquires 60% of the circulating quantity at a low price, he only needs to prepare 2 million USDT and hold 3 million coins without moving them to fully control the spot and contract prices of this coin.

Step 3: Control the spot market price.

As long as 3 million of the coins are not sold, the spot market can have at most 2 million sell orders. Therefore, as a 'speculator' who wants to manipulate the price well, one needs to prepare 2 million USDT as the funds to maintain the spot price.

It is obvious that even if all the S*** outside the 'speculator' sells at the same time, the price will not drop.

Step 4: Control the marked price of the contract.

It has been mentioned earlier that the marked price of the contract is the spot price of each exchange, which means that the marked price of the contract remains unchanged.

Step 5: Open a long position in the contract.

After ensuring that the marked price is controlled, one can use their own funds to open any levered position in the contract. It can be conservative by opening a lower position or aggressive by opening a higher position—either way, it does not matter as long as the marked price is controlled; the 'speculator's' long position will never be liquidated.

Step 6: Use funding to pull up prices or trade against small accounts.

For coins with shallow depth and small market values, pulling up the spot price by 10% requires very little capital. If the price cannot be raised, one can create a small account and place a high sell order at the price after the 10% increase, and once the transaction is completed, it will naturally show as a +10% change in the coin's price over the last 24 hours.

After seeing this news, retail investors will rush in, creating a large demand for short selling.

Step 7: Use the funding rate to earn steadily.

At this moment, there are very few sell orders in the spot order book, while there are many short positions in the contracts, causing the spot price to be higher than the contract price, resulting in a negative funding rate. The larger the difference, the more negative the funding rate, which means that even if the marked price remains unchanged, the short position holders have to pay a high negative rate to the long position holders every 8 hours just to maintain their positions.

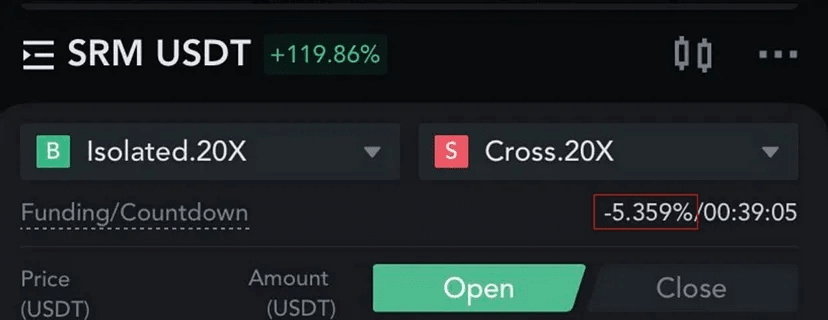

Under this game mechanism, the speculator continuously generates wealth through funding rates. For example, by holding SRM for 24 hours without any position, one can earn a profit of 16%.

Coincidentally, recently exchanges have frequently adjusted the funding rate to help narrow the price difference between the spot market and the contract market.

However, they did not find the root cause of the abnormal funding rate, and expanding the funding rate range can still allow for market making; this issue may instead help project parties/market makers/institutional investors harvest retail investors using the funding rate.

You may also notice that LINA and MT were the coins that were recently pulled up, and the funding rates for contracts showed significant negative values.

5. How do speculators profit?

First profit point: Buy low and sell high in the spot market.

Remember, speculators do not do charity; the coins bought are neither real gold nor BTC, and they will definitely profit by selling in the end. The so-called pump is all for the subsequent dump.

Second profit point: Contract funding rate.

Third profit point: Directly lend coins that are held and not sold to the leveraged lending market. For example, Gate can achieve an annualized return of 4.9% through its Yubi Bao, which is a similar concept.

After going through the process, everyone can see that the premise is to control the circulating supply of the spot coins. If there are a large number of linear unlocks of circulating coins, they cannot be manipulated long-term. Each unlock will change the circulating volume.

6. Where is the problem?

Question 1: Can contract Open Interest exceed the circulating market value?

Contracts only require USDT to open positions, while spots must have coins to sell. Obtaining coins to form sell pressure in the spot market and shorting in the contract market are not the same in difficulty.

Returning to the third part, step three, the speculator has already locked the coins in his hands. Even if users believe this coin is severely overvalued, they cannot form sell pressure in the spot market. At this point, they will turn to the contract market to short. In other words, shorting is easier to lean towards coins with lower circulating volumes, which cannot be released in the spot market and can only go to the contract market to short.

Returning to the first point of the marked price in the fourth section, the marked price of the contract is the latest transaction price of the spot, and the marked price of the contract has already been controlled by the project party/market makers/institutional investors. Therefore, how the contract may get liquidated is already clear.

Therefore, when contract Open Interest > circulating market value, it means that due to the scarcity of coins, the trading demand from market makers cannot be reflected in the market price. The excess contracts will exacerbate the divergence of the spot price.

Question 2: When the funding rate is abnormal, how can large investors in the limits of spot and contract collaborate on the funding rate to promote fairness?

Currently, the exchange's solution is to expand the funding rate, which superficially addresses the price difference issue between the spot and contract markets, but in reality, it expands the ability of project parties/market makers/institutional investors to harvest retail investors.

Thus, the existing funding rate mechanism, while helping the derivatives market anchor the spot market price, does not help make the trading market fairer, and may instead exacerbate unfairness in the trading market.

7. How can retail investors hedge?

Note 1: Beware of projects with small market values that have opened high-leverage contracts. They give large investors a very unequal competitive advantage compared to retail investors.

When users choose to buy in the spot market and open long positions in contracts, they accumulate enough buyers for the project parties/market makers/institutional investors, allowing them to gradually sell off and harvest retail investors again.

Note 2: Projects with a relatively high absolute value of funding rates.

Note 3: Speculators do not do charity; the final cost of pulling the price up must be realized through dumping for profit.

Flee in advance, be careful not to become a scapegoat for the speculators. When the idea of 'this coin is a valuable coin, I want to hold it long-term until the next bull market' arises, the time until the speculator dumps the coin is not far away. His goal in pulling up the price is to cultivate this kind of user psychology for himself to take over.

In the small-cap contract market, trading against speculators is like playing poker with them; they are both players and dealers.