Author: Jack Inabinet, Bankless

Compiled by: Saoirse, Foresight News

Stablecoin issuer Circle has drawn significant attention this summer. On June 5, Circle's stock opened at a price as high as $69 in the public market, allowing early investors who participated in its already expanded IPO to directly double their funds.

Throughout June, CRCL's stock price continued to soar, and as the price approached $300, the stock had firmly established itself as a 'high-performing cryptocurrency concept stock.' Unfortunately, the good times were short-lived, as the stock ultimately could not escape the effects of seasonal downturns as summer progressed...

Despite a 7% rise in the stock following Powell's comments on rate cuts last Friday, it has been in a downward trend for most of the past month, currently down nearly 60% from its historical peak.

Today, we will explore the rate cut dilemma facing stablecoins and analyze the impact of changing monetary policy on CRCL's future.

The tricky issue related to 'interest'

Circle operates a bank-like business model: earning profits from interest.

Bank deposits exceeding $60 billion, overnight loan agreements, and short-term U.S. Treasury bonds provide support for USDC. In Q2 2025, Circle earned $634 million in interest from these stablecoin reserves.

When interest rates rise, each $1 of USDC reserves in the portfolio generates more interest; conversely, when interest rates fall, returns decrease. Although interest rates are driven by market forces, the cost of dollars is also influenced by Federal Reserve policies, especially regarding short-term instruments used by Circle to manage reserves.

Last Friday, Federal Reserve Chairman Jerome Powell strongly hinted at the possibility of a rate cut in his speech at Jackson Hole. We have previously encountered 'false rate cuts,' but this is the first time Chairman Powell has clearly leaned towards supporting a rate cut.

Powell attributed the residual inflation to one-time tariff spikes, emphasized that the labor market is slowing, and defended possible rate cuts. The market currently expects the Federal Reserve to announce a rate cut at its policy meeting on September 17.

According to CME FedWatch and Polymarket data, the likelihood of a rate cut has significantly increased after Powell's speech, with substantial probability changes actually starting on August 1. On that day, employment data showed that only 73,000 jobs were added in July, and the previous two months' data were also significantly revised down.

Since August 1, both CME FedWatch and Polymarket have consistently predicted a high likelihood of a 25 basis point (0.25%) rate cut. If the Federal Reserve does implement a rate cut as expected, Circle's income will decrease overnight.

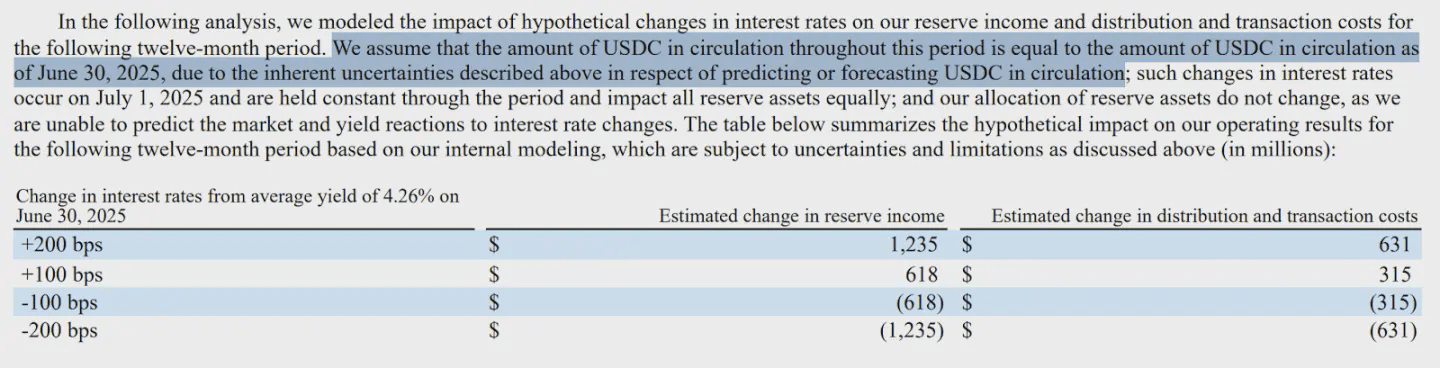

According to Circle's own financial projections, for every 100 basis points (1%) drop in the federal funds rate, the company will lose $618 million in interest income annually, meaning a 'standard' 25 basis point rate cut would result in a $155 million loss in income.

Fortunately, half of the income loss will be offset by the decrease in distribution costs. This aligns with Circle's agreement with Coinbase, which stipulates that about 50% of the USDC reserve interest income is distributed to Coinbase. However, the reality is that Circle's operations will become increasingly difficult in an environment of continuously declining interest rates.

Modeling analysis of the impact of rate changes on reserve income as well as distribution and transaction costs over the next 12 months

Source: Circle

Despite Circle reporting a net loss of $482 million in Q2, which was far below analyst expectations, this unexpected difference largely stemmed from a $424 million accounting write-off related to employee stock compensation during the IPO.

Even so, Circle's financial situation still highlights the vulnerability of this company that is on the brink of break-even. At the current USDC supply level, it cannot withstand the impact of a significant drop in interest rates.

Solution

On the surface, a rate cut may reduce Circle's interest income per dollar of reserves, harming profitability. However, for CRCL holders, fortunately, a simple variable change can completely reverse the situation...

Powell and many financial commentators believe that current interest rates are at 'restrictive' levels, and minor adjustments to the Federal Reserve's policy rate can address a weak labor market while controlling inflation.

If these experts' judgments are correct, a rate cut could trigger an economic rebound, where employment rates remain high, credit costs decrease, and the cryptocurrency market surges. If this optimistic scenario comes to fruition, demand for crypto-native stablecoins may increase, especially when they offer decentralized financial native yield opportunities above market levels.

To offset the negative impact of a 100 basis point rate cut (the minimum level considered in Circle's aforementioned rate cut sensitivity analysis), the circulation of USDC needs to increase by about 25%, which requires injecting $15.3 billion into the crypto economy.

Based on projected net profits for 2024, Circle's current price-to-earnings ratio is 192 times, making it a high-growth opportunity. However, despite the stock market's optimistic view on CRCL's expansion prospects, this stablecoin issuer needs to achieve growth to survive if the Federal Reserve implements rate cuts in the coming weeks.

Assuming the Federal Reserve cuts rates by at least 25 basis points, Circle needs to increase the supply of USDC by about $3.8 billion to maintain its current profit levels.

In Circle's words, 'Any relationship between interest rates and USDC circulation is complex, highly uncertain, and unproven.' Currently, there is no model that can predict how USDC user behavior will respond to low interest rates, but history shows that once a rate cut cycle begins, it often accelerates quickly.

Although in a booming economy, Circle might compensate for losses due to falling interest rates through growth, data shows that the company has an inherent conflict with a low interest rate environment.

The majority of the company's income comes from reserve earnings, and interest rate fluctuations can affect reserve yields, potentially changing reserve income. However, due to the uncertainty of user behavior impacting the circulating USDC, while the impact of interest rates on reserve yields can be predicted, the ultimate effect on reserve income cannot be accurately anticipated.

Source: Circle