Hyperliquid's token $HYPE set a new high again on August 27, and before that, on August 26, a meticulously planned 'flash short squeeze' storm swept through the $XPL pre-market contract market on Hyperliquid. In less than an hour, the price K-line chart was violently drawn into nearly vertical lines, and countless short trader accounts were instantly wiped out, while the manipulators left with over $46 million (about 14.6 billion New Taiwan dollars) in huge profits.

This incident quickly sparked a huge uproar in the crypto community, with cries of despair, anger, and conspiracy theories intertwined. People couldn't help but ask: Was this an accidental extreme market fluctuation, or a precise 'massacre' exploiting protocol vulnerabilities? And at the center of the storm—Hyperliquid—why does it repeatedly become the perfect hunting ground for whales?

A long-planned 'hunt'.

This seemingly sudden market crash was, in fact, a meticulously planned encirclement.

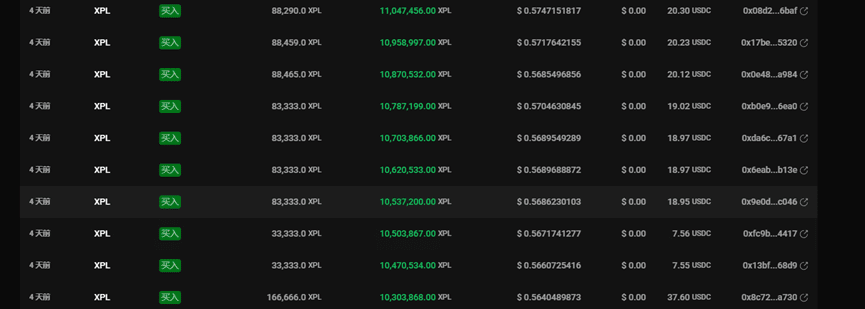

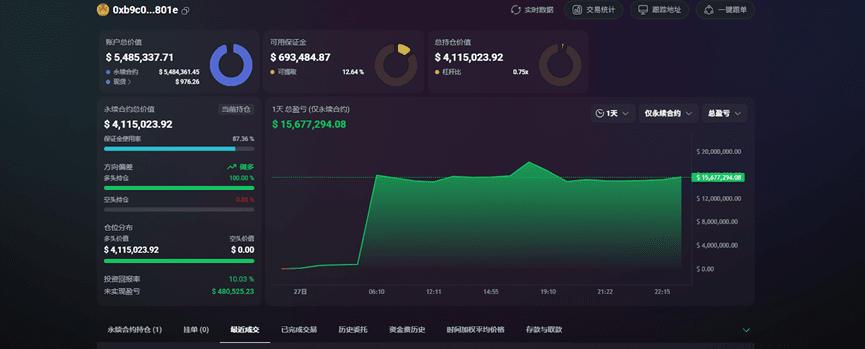

According to Ai Yi's on-chain data tracking, this collaborative attack was executed by at least four core wallet addresses. Among them, the roles and fund deployments of the two main attacking addresses are particularly clear: one is the address starting with 0xb9c0, and the other belongs to the DeBank user named 'silentraven'. The other two addresses played auxiliary roles. These wallets showed similar operational behaviors, with three addresses transferring large amounts of funds to start accumulating long positions in XPL between the 23rd and 25th. Among them, as the main attacking address, the address 0xb9c0 even preemptively used $11 million of $USDC to open long positions in XPL on Hyperliquid at an average price of around $0.56.

Source: (PANews)

Source: (PANews)

The DeBank user named 'silentraven' used $9.5 million in USDT to establish a long position of 21.1 million XPL at an average price of $0.56 over the past three days.

These several addresses collectively invested over $20 million, acquiring huge long positions in batches and at different times within almost the same price range. Several of these addresses clearly only set up long positions for the XPL token after their creation.

Around 5:30 AM on August 26, as most traders in the Asian region were still asleep, the hunting moment quietly arrived.

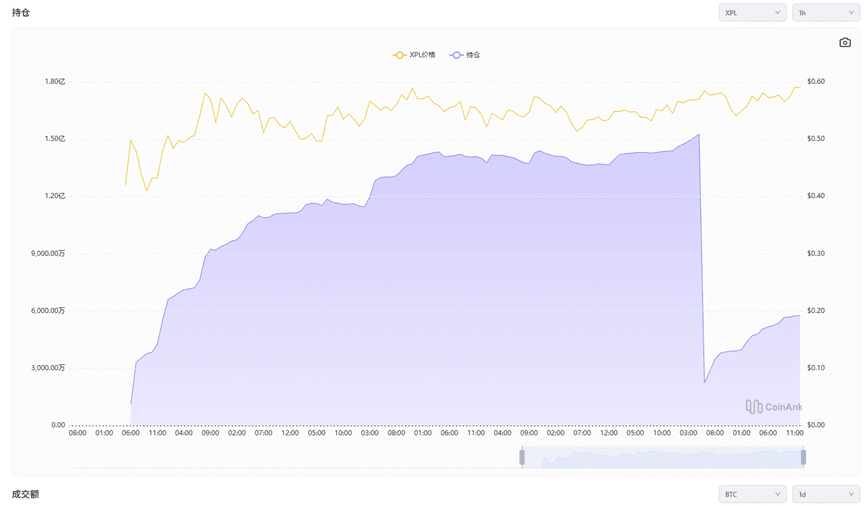

Address 0xb9c0 transferred an additional $5 million to the Hyperliquid platform. Then, indiscriminately raised the price of the token. In the pre-market of XPL, where liquidity is already extremely thin, this fund was like a spark thrown into a powder keg, instantly igniting the entire order book. Within minutes, the price of XPL surged from around $0.6 to $1.8, an increase of over 200%.

In such a short-term surge, several obvious outcomes occur. First, most traders do not have time to increase margin to elevate the liquidation price. Second, the minimum 1x leverage hedging orders can also be blown up. Third, as many short positions are liquidated one by one, the forced buy orders will further push the price up, creating the most terrifying 'short squeeze' phenomenon in the financial market.

Eventually, at the peak of the price, manipulators began to close positions at prices between $1.1 and $1.2. According to Ai Yi's statistics, this operation brought the manipulators over $46 million in profits.

Source: (PANews)

Source: (PANews)

The wails of $60 million and the platform's 'indifference'.

A feast for capital inevitably accompanies the wails of another group of people. When manipulators return with full hands, all that is left for other market participants are bloody loss accounts and endless questions.

Crypto KOL @Cbb0fe stated that he allocated 10% of his funds on Hyperliquid for hedging, resulting in a loss of $2.5 million, and he will no longer touch isolated markets.

Source: (PANews)

Source: (PANews)

Other media reported that the maximum loss for a single address was about $7 million. However, specific address information was not disclosed, leading to doubts.

However, from the perspective of the manipulators' profits, the maximum profit amount at that time indeed exceeded $46 million, and it remains uncertain whether there were other undiscovered partners involved in this process.

From the changes in contract positions, before the attack began, the contract position of XPL on Hyperliquid reached a peak of $153 million, then quickly plummeted to $22.44 million, with a reduction of over $130 million, and the overall loss for short users may reach $60 million.

Source: (PANews)

Source: (PANews)

This loss even exceeded the maximum floating loss of $11 million caused by the JELLY token against Hyperliquid in March. Moreover, this time it may be because the official was not directly harmed, so the victims could only silently swallow their losses.

In community discussions, a familiar name was repeatedly mentioned, Tron founder Justin Sun. Some users pointed out that during this attack, one address had transferred ETH to Justin Sun's associated address years ago, but this action does not directly prove any actual connection between the address and Justin Sun.

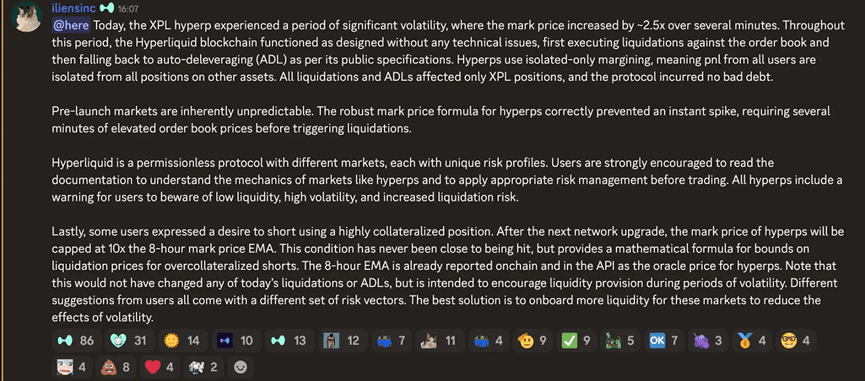

After the incident, many users also turned their hopes to Hyperliquid, expecting the platform to provide an explanation or remedial actions. However, this time, Hyperliquid did not handle the profit orders as brutally as when the JELLY token was manipulated in March, closing them and directly shutting down related accounts. Instead, they responded in the official Discord community, stating that the XPL market experienced severe volatility, but Hyperliquid's blockchain functioned normally during this period without any technical issues. The liquidation and automatic deleveraging (ADL) mechanisms were executed according to public agreements, and due to the platform's use of a fully isolated margin system, this incident only affected XPL positions, and the protocol did not incur any bad debts.

Source: (PANews)

Source: (PANews)

For many onlookers, not making adjustments is quite reasonable. After all, when XPL was launched, Hyperliquid had already warned about high volatility and risks, and such manipulation was completed under the rules of the market.

Source: (PANews)

Source: (PANews)

However, for those severely affected users, such a response seems a bit cold.

Causes of the tragedy: a deadly conspiracy of platform, subject, and timing.

Looking back at the whole process of the incident, this is not the first time Hyperliquid has experienced similar market manipulation. In this process, it is evident that the manipulators had premeditated and meticulously planned. On the other hand, this is also closely related to Hyperliquid's platform design itself.

First of all, such short squeeze operations are not uncommon in financial markets, often occurring in markets with poor liquidity and isolated prices. This operation on Hyperliquid is based on several characteristics of Hyperliquid: first, the extreme transparency on-chain, where manipulators can calculate the funds needed to manipulate the market and the effects achieved through publicly available data such as positions, liquidation prices, and funding rates. Second, Hyperliquid's isolated oracle system, as XPL uses an independent pricing system on Hyperliquid that does not rely on external oracles. This allows manipulators to freely manipulate prices within this enclosed space without worrying about the difficulties brought by price balancing from other exchanges.

Additionally, there are many nuances in the selection of operating targets. The manipulated XPL (and another token WLFI that experienced a similar situation but was not as exaggerated) are both unlisted tokens, which also means that they are a type of 'paper contract', with no issues of spot delivery and spot dumping suppression, making them easier to manipulate.

Finally, regarding the timing of the attack. Before the attack, the trading volume of XPL was only around $50,000 every 5 minutes. Just at the weakest period after the launch when trading enthusiasm had waned, this thin liquidity provided a favorable opportunity for attackers, allowing manipulators to achieve market manipulation with minimal funds.

The XPL incident exposed deep structural risks, reminding us of the need for reflection on both the platform and user levels.

From the platform's perspective, first, there is a mechanism vulnerability. Since 2025, Hyperliquid has experienced three market manipulation incidents. Each time, some vulnerabilities of Hyperliquid as a decentralized derivatives trading platform were almost exposed. The result of these vulnerabilities has repeatedly harmed ordinary users' funds while weakening Hyperliquid's credibility. In this case, on the one hand, there is the enclosure caused by the isolated oracle mechanism, and on the other hand, there is a lack of active price intervention from the platform's liquidity when abnormal positions occur.

Secondly, is it more important to treat evildoers equally or to maintain a decentralized shell? In the JELLY incident, Hyperliquid unhesitatingly initiated an on-chain vote, ultimately preserving the losses and expelling the evildoers. The rationale at that time was to protect the funds in the user treasury from losses, which forced actions detrimental to decentralization. Now, facing amounts far exceeding the previous losses, is it because the platform treasury was not harmed or to avoid letting the banner of decentralization fall again that it chose to ignore? This may leave a significant doubt in users' minds.

Finally, for users, the XPL manipulation incident once again reminds us to be vigilant about scarce liquidity and isolated markets. In the market, those pre-market contracts with extremely low liquidity and lacking spot market anchoring are often favored 'hunting grounds' for whales. Additionally, reducing leverage and setting stop-loss orders—these age-old trading principles—are always relevant.

This article is reprinted with permission from: (PANews)

Original title: (Another tragic incident on Hyperliquid: XPL flash short squeeze, users lose over $60 million, when will the whale hunting stop?)

Original author: Frank, PANews

'Another tragedy on Hyperliquid! The XPL short squeeze caused a loss of $60 million, is there a premeditated hunt behind it?' This article was first published on 'Crypto City'.