Written by: Lacie Zhang, Bitget Wallet Researcher

Introduction: On August 20, 2025, a rumor about 'China may consider issuing RMB stablecoins' reported by Reuters quickly sparked widespread speculation in the global cryptocurrency and financial markets. Although this seems more like a 'wild rumor', the fact that this long-regarded 'forbidden zone' topic can stir such waves is itself an important policy indicator. This trend is not unfounded; it is the inevitable result of years of grassroots exploration and cautious observation by officials. The Bitget Wallet Research Institute will take you through the historical evolution of RMB stablecoins.

I. Tentative Explorations on the Edge of the 'Red Line': The Exploration Process of RMB Stablecoins

Before discussing official intentions, we must first understand a basic background: RMB stablecoins are not a new phenomenon; their exploration has been ongoing in the 'gray area' of the market for several years. To understand all this, the key lies in distinguishing between two core concepts - onshore RMB (CNY) and offshore RMB (CNH). In simple terms, CNY is the legal currency of mainland China, subject to strict capital controls; while CNH is the RMB circulating outside of China, with a more market-oriented exchange rate, providing a natural soil for the early exploration of stablecoins.

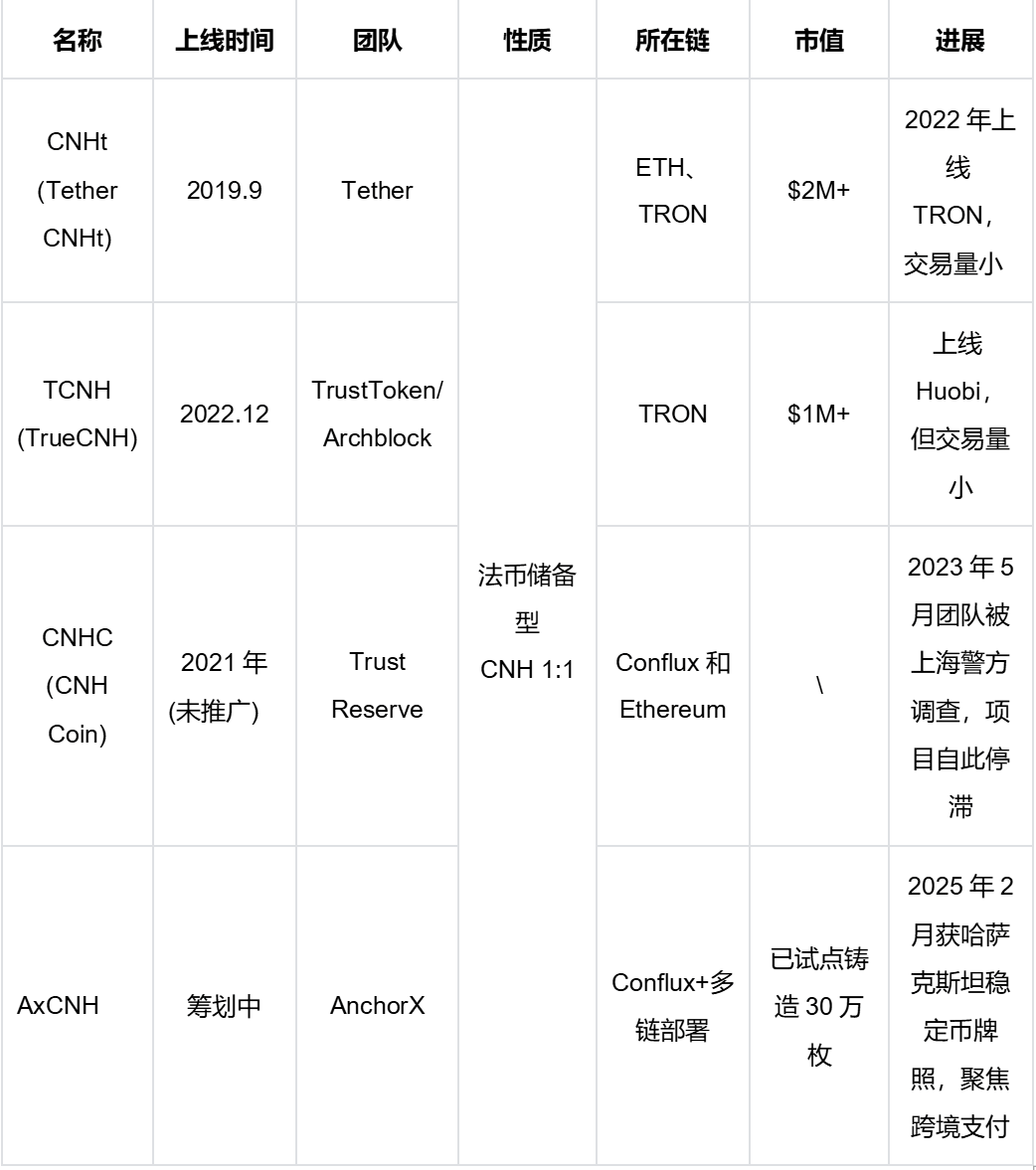

Based on this, the stablecoins that have truly formed circulation in the market are basically those pegged 1:1 to offshore RMB (CNH) - the statistics on RMB stablecoins on Coingecko only cover offshore RMB (CNH). Looking at its development history, three groups of players with different backgrounds can be seen, each representing three different paths of attempts.

International giants' half-hearted attempts: Stablecoin giants Tether and the American team TrustToken (now renamed Archblock) launched CNHt and TCNH in 2019 and 2022, respectively. They seem more like strategic probes into a potential market, intending to leverage small-scale cross-border payments, but constrained by the regulatory high walls of mainland China, they did not invest heavily in promotion, resulting in a lukewarm response and gradually fading from mainstream view, with a combined market cap of only a few million dollars.

The setbacks of the mainland team: The CNHC, founded by a Chinese team, was once regarded as the most promising competitor in this field and received investments from prominent capitals such as KuCoin Ventures, members of the Circle founding team, and IDG. However, just as the project was about to take off, its Shanghai office was raided by police in May 2023, and core members were taken away, abruptly halting the project. This has become a significant event marking the strict regulation of crypto businesses in mainland China.

The circumstantial breakout under the background of the 'Belt and Road': After the CNHC incident, the Hong Kong fintech company AnchorX was jointly incubated by Conflux and Hongyi Capital. Its core team is said to have deep ties to CNHC. They chose a more roundabout path - in February 2025, they were the first to obtain a 'fiat stablecoin issuance' license in Kazakhstan, focusing on cross-border trade settlement along the Belt and Road in Central Asia and currently have initiated sandbox testing.

Offshore RMB (CNH) Stablecoin Case Overview

Data Sources: Coingecko, CoinMarketCap, Token Radar

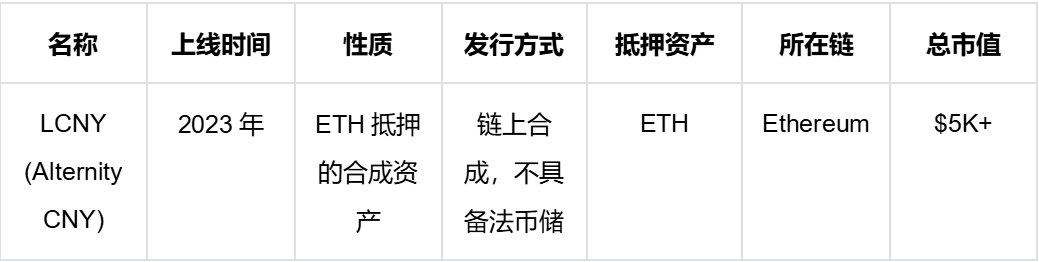

The exploration of the offshore market has experienced ups and downs, but attempts at onshore RMB (CNY) stablecoins are nearly a desert. A few projects like LCNY and bitCNY essentially rely on collateralized crypto assets to generate synthetic assets, rather than being supported by real fiat reserves. The logic behind this is very clear: under China's strict foreign exchange control system, any stablecoin directly pegged to onshore RMB with fiat reserves would be tantamount to openly challenging the country's core financial defenses.

Onshore RMB (CNY) Stablecoin Case Overview

Data Source: Defilama

These varied attempts, with differing degrees of success, collectively outline the realistic picture of RMB stablecoin development and reveal several clear internal rules behind them:

1. 'Offshore' is the only path, while 'onshore' remains a red line. All effective attempts are concentrated in the CNH sector, clearly indicating that in the foreseeable future, any official or semi-official projects will be strictly limited to the offshore market to ensure risk isolation from the domestic financial system.

2. Feasibility has been validated, but scaling up is a huge challenge. The technical implementation and small-scale pilots have proven that issuing RMB stablecoins is not difficult. However, the current total market cap of several million dollars, compared to the hundreds of billions of dollars of US dollar stablecoins, is merely a drop in the bucket. Finding real, large-scale application scenarios is the key to whether it can rise.

3. The strategic focus is shifting from 'globalization' to 'geopolitization'. If earlier projects still held a vague vision of serving globally, then AnchorX's establishment in Kazakhstan marks a significant shift in strategic direction: serving specific geopolitical and economic goals such as the 'Belt and Road' is becoming the most realistic application scenario for RMB stablecoins.

II. Opportunities and Challenges: The Three Critical Questions Beneath the Grand Narrative:

In such a context, the concept of RMB stablecoins undoubtedly carries enormous strategic opportunities. It not only hopes to create an independent 'Digital Silk Road' for trade along the 'Belt and Road' that is independent of SWIFT, reconstructing the regional settlement system; it can also contend with US dollar stablecoins in the global crypto economy, vying for the 'minting rights' in the digital age - this is the core driving force behind the government's willingness to reassess its possibilities.

However, beneath the grand narrative, three core practical issues loom large, which are both the three critical questions that must be answered and the key obstacles that must be cleared before the issuance of stablecoins.

First critical question: How to balance monetary innovation with financial stability?

Even for offshore RMB stablecoins, their capital flows will ultimately have intricate connections with the onshore system. How to encourage innovation and expand the international influence of the RMB while ensuring that it does not become a 'Trojan horse' for capital outflow, and how to construct effective risk isolation and regulatory penetration mechanisms is the 'Sword of Damocles' hanging over all practitioners.

First critical question: How to overcome the bottleneck of insufficient reserve assets?

A core contradiction is laid bare: the potential demand for RMB stablecoins is enormous, but qualified reserve assets are extremely scarce. A recent article by Professor Fang Xiang from the University of Hong Kong quantifies this issue: based on a cross-border RMB settlement amount of 16 trillion yuan in 2024, assuming only 20% of it turns to stablecoin settlement, and referring to the currency circulation rate of US dollar stablecoins at 6.8, the required stablecoin scale would exceed 400 billion yuan. However, the problem is that by the end of 2024, the total amount of available high-quality short-term bonds in offshore RMB is only a few hundred billion yuan. This gap of more than ten times is an unavoidable practical bottleneck on the road to the development of RMB stablecoins. Data Source: People's Bank of China (Financial Statistical Data Report), image created by the author.

Second critical question: How to break the monopoly position of US dollar stablecoins?

After years of development, US dollar stablecoins have established a large user base, deep liquidity, and a mature ecosystem globally. The emerging offshore RMB stablecoin not only needs to build user trust from scratch but also faces strong network effect barriers. Convincing global users and developers to 'abandon the dollar and use the RMB' will be an exceptionally difficult battle.

III. 'Tacit Approval' and 'Expedition': The Future Roadmap of RMB Stablecoins

Regardless of the truth behind the rumors, facing such a complex situation, it can be anticipated that the official strategy will never be a simple and crude 'full liberalization', but rather a prudent and sophisticated 'combination punch', which can generally be understood from the following three dimensions.

Firstly, in terms of official attitude, a shift from 'strict prohibition' to 'tacit approval + timely guidance' must be achieved. From the current widespread use of USDT among Yiwu merchants, which is an 'open secret' in the industry, to the AnchorX team traveling to Central Asia to obtain compliance licenses, these seemingly isolated events point to a subtle change in regulatory attitude: the exploration that serves national strategies is transitioning from strict obstruction to observation and even tacit approval. The recent rumors of review may signal a high-level intention to formally incorporate these 'gray explorations' into a more macro and controllable top-level design.

Secondly, in terms of issuance strategy, the concept of 'openly building a path while secretly taking a shortcut' may emerge. Hong Kong will be the 'path' that attracts global attention - as an officially recognized pilot, it will conduct limited sandbox testing. The true chess piece of the policy, however, lies in the 'shortcut' along the 'Belt and Road' - encouraging compliant teams to apply for licenses in friendly countries, using a model of 'one license serves the globe' to lay a compliant landing point for the globalization 'expedition' of the RMB.

Finally, in terms of long-term goals, it is to build a set of 'new cross-border infrastructure for digital finance'. Issuing stablecoins is just the first step; in fact, the long-term goal of the Chinese government has always remained unchanged, which is to create a global cross-border payment network independent of SWIFT - only the current technological foundation is shifting from traditional architecture to blockchain. It can be anticipated that in the future, not only will more publicly-backed public chains emerge, but they will also be deeply embedded in the trade networks of the 'Belt and Road', interfacing with the central banks and commercial banking systems of the countries along the route, ultimately settling into a regional trade settlement ecosystem that is RMB-centered, multi-currency coordinated, and highly efficient.

IV. Conclusion

As the issuance of Hong Kong dollar stablecoins has been put on the agenda and the offshore RMB stablecoin is quietly piloted in trade scenarios in Central Asia, the re-examination of this field by mainland China is both logical and urgent. Whether the Reuters report is a wild rumor or an intentional 'leak' by officials remains unknown. However, it is certain that discussions about RMB stablecoins have moved from behind the scenes to the forefront. How the final policy will be implemented, especially regarding a clear distinction between 'onshore' and 'offshore', will not only determine the future form of the digital RMB but also serve as an important window for observing China's strategic ambitions in a new round of global financial reforms.