The bad debts in the real world often come from 'mismatches': either the money is given too quickly or the verification is too slow. Huma's approach is the opposite: to preemptively put risk control on 'behavior and notes', breaking down the recoverable cash flow into verifiable fragments. For example, a merchant's card settlement flow, refusal records, average transaction value, and fluctuations; the repayment cycle of a cross-border channel, and the refusal rate of intermediary banks; these can form interpretable fingerprints on the chain, which are then discounted based on the pool's strategy. Coupled with the closed loop of Circle/USDC for payments, it becomes easier to account for the direction of funds, reducing repeated readings between 'on-chain ↔ off-chain'.

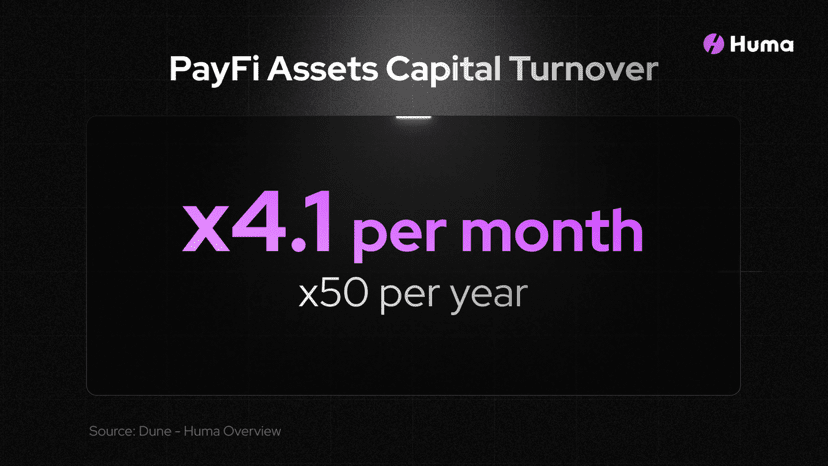

The statement from Binance Research that says 'zero historical defaults' is not a guarantee of 'never having issues', but rather a side effect of 'drawing the risk control boundaries narrow enough': preferring to move slowly rather than including high-risk notes in the pool; preferring a lower yield center rather than relying on high interest rates to gamble on liquidation. In terms of data, a cumulative scale of 4.5 billion dollars + an annualized income of 9 million looks more like 'transforming the old logic of the payment industry into a new interface on the chain.'

I suggest you add a 'complaint/review' mechanism when writing HUMA: when a merchant/user is tagged as high-risk by the system, can they provide triggering factors (e.g., 'abnormal repayment cycle/refusal/amount fluctuation') and allow supplemental evidence for a second evaluation. For PayFi to continue to grow, explainability and the ability to appeal are key to traversing cycles.

Finally, leave three 'observation lines' for the readers:

Is the overdue rate and refusal rate consistently low over the long term;

Duration and exit waiting improvements with 2.0 mechanism;

An increase in the proportion of institutional LPs indicates that the quality of the notes can withstand scaling up.

Interaction: If you are an LP or a merchant, do you prefer the platform to be 'strict but slow' (low default, stable returns) or 'lenient but fast' (quick loans, high returns)?

@Huma Finance 🟣 #HumaFinance $HUMA