Last week, the discussion on inflation in the Polkadot community saw new changes. The Growth Pressure proposal originally put forward by Alice_und_bob was replaced by a relatively mild Medium Pressure proposal after further communication.

After comparing these two versions, we found that Medium Pressure is essentially no different from Growth Pressure in terms of market value pressure; the main difference is that it extends the timeline to reach the hard cap, making the overall path appear smoother.

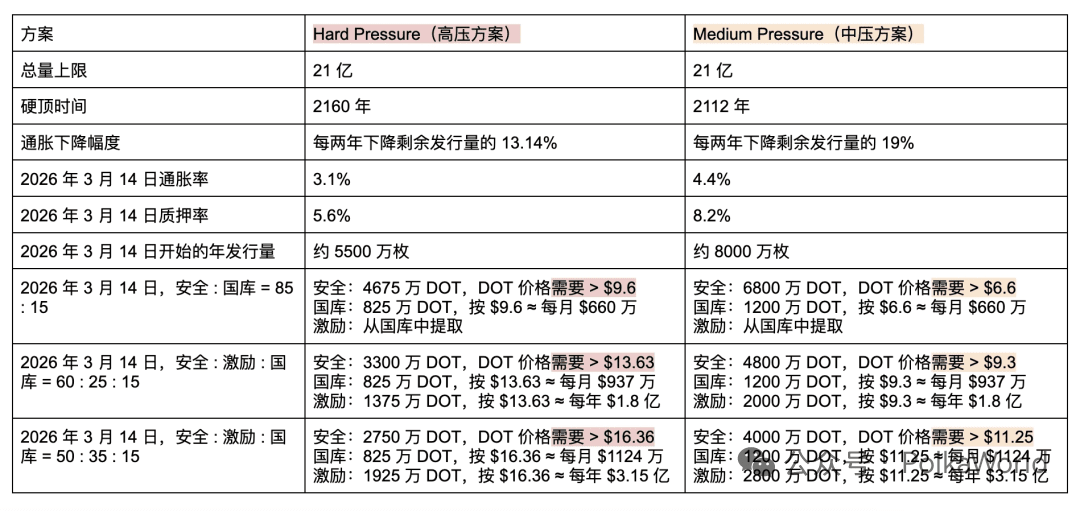

In the horizontal comparison between Hard Pressure and Medium Pressure, it can be seen:

Hard Pressure: Annual issuance sharply decreases at first (blue line), and after 2052 (about 27 years later), the annual increase will be below 1 million DOT.

Medium Pressure: The decline curve is smoother (blue line), and similarly, after 2052, the annual increase will be below 1 million DOT.

Under the same distribution ratio, the market value pressure of Hard Pressure is significantly greater than that of Medium Pressure.

Regardless of which plan is chosen, the community can still adjust the distribution ratio parameters to change the market value pressure and economic incentives faced by DOT.

In summary, we can adjust DOT's market value pressure through two types of 'pressure':

Inflation Reduction

Adjusting Staking Reward Ratio

This means that the future inflation model is not a single choice but a combination and trade-off of two pressures.

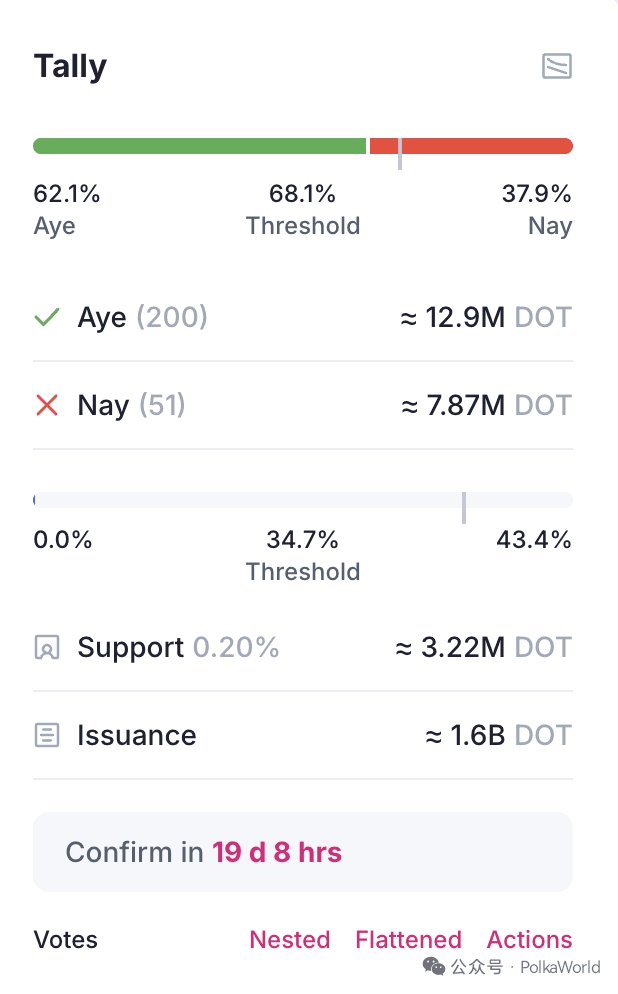

Currently, among the three plans, Hard Pressure has the highest support rate, with 62.1% support, and will enter the confirmation period in 19 days.

However, behind the discussion of the inflation curve, Jonas Gehrlein, a research scientist at the Web3 Foundation, reminds everyone that a more critical issue has been overlooked, which is economic security—reducing inflation not only affects market value pressure but also directly determines Polkadot's ability to resist attacks.

Jonas believes that in a PoS system, security is not free. It relies on the DOT staked by validators and nominators. If the cost to attack the network is lower than the potential gains, security no longer exists. Therefore, when designing the inflation curve, we cannot only look at 'how much is issued,' but also at 'how much security is worth.' If inflation is significantly reduced, Polkadot's economic resilience will almost proportionally decline, and the network will be more susceptible to economic attacks.

In the worst-case scenario (bribing existing validators), the cost to attack Polkadot is only 14.71 million DOT, while inflation drops by half in Hard Pressure, this safety lower limit will directly drop to 8.18 million DOT, thus greatly lowering the difficulty of the system to resist attacks, increasing risk. If the chain publicly offers a reward amount slightly above the lower limit, validators may collectively betray → consensus collapses in an instant.

Therefore, simply 'cutting inflation' is likely to drag down Polkadot's security.

Can we maintain low inflation while ensuring security?

How can we find a balance between 'reducing inflation' and 'maintaining security'? Jonas proposed four types of policy measures:

Policy 1: Minimum Commission and Minimum Self-Staking

At the protocol level, there are two mechanisms that can directly affect the economic resilience of the network.

First, enforce a minimum commission for validators. This will ensure that validators can maintain stable long-term income even in a competitive and compressed profit situation, thus enhancing the sustainability of node operations.

Second, require validators to have a minimum self-staking amount. This means that validators need to genuinely invest their own funds into the network, taking on more 'skin in the game' responsibility. In other words, validators do not just rely on the support of nominators but demonstrate their commitment to the future development of Polkadot through their own capital binding.

These two measures complement each other: minimum commissions ensure validators can have reasonable profit expectations, while minimum self-staking requires them to be more closely tied to the network’s security and development. This enhances overall economic resilience and strengthens network security.

Policy Two: Reduce Issuance

The most direct way to reduce inflation is to decrease the number of newly minted DOT.

Currently, the new issuance of Polkadot is mainly divided into two parts:

Staking rewards: approximately 279,439 DOT per day

Treasury income: approximately 49,313 DOT per day

Therefore, achieving inflation reduction does not necessarily require a 'one-size-fits-all' approach, but can be completed by adjusting the ratios of these two parts. For example: moderately reducing the proportion of staking rewards or cutting the share going into the treasury, or even adjusting both at the same time. This approach makes inflation control more flexible and avoids overly intense impacts on the incentive mechanisms of any one party.

In fact, this viewpoint has been advocated by PolkaWorld all along— we can adjust DOT's market value pressure through two types of 'pressure': reducing inflation and adjusting the staking reward ratio, where the future inflation model is not a single choice, but a combination and trade-off of two pressures.

Policy Three: Remove Nominee Reduction and Unbonding Period

Under the current mechanism, nominators take most of the staking rewards. However, from the perspective of economic security, the network's safety lower limit does not directly depend on nominators' staking, which also means that the rewards for nominators are the most likely to be compressed.

If the earnings of nominators are reduced in the future, compensation must be made in terms of experience and risk. A feasible approach is:

Remove the penalty for nominators, making participation nearly risk-free for nominators;

Cancel the unbonding period to allow nominators to exit at any time, improving fund liquidity.

It is important to note that under the NPoS mechanism, the system will take 'snapshots' at specific points in time to record which validators nominators voted for, and then decide which validators enter the active set based on this snapshot. If nominators suddenly withdraw funds during this very short time window, it may lead to inconsistencies between the snapshot data and the actual funding situation, affecting the fairness or stability of the validator election.

Therefore, even if the unbonding period is canceled and nominators are allowed to exit at any time, at the moment of the snapshot (for example, in a few minutes or hours), withdrawal operations may need to be temporarily restricted to avoid chaos in the election process.

Therefore, if we remove frictions like penalty reductions and unbonding periods, the process of participating in staking will become simpler and smoother. Reducing risk and thresholds means that even if nominators earn less, they still have the motivation to participate and continue to play a role in ensuring network security. Meanwhile, even if earnings decrease, nominators are still not 'dispensable'; they play an important role in the network—responsible for selecting, supervising validators, and submitting choices to the system's election algorithm.

Policy Four: Decreasing Issuance Curve

The so-called 'decreasing issuance curve' means that the new issuance of DOT gradually decreases over time, ultimately approaching a set upper limit, rather than growing indefinitely.

If no additional design is made, the system will naturally converge to a certain 'endogenous upper limit' (such as several billion DOT), but the exact amount is uncertain. If we want the total amount of DOT to converge to a clear value—such as π × 10⁹ DOT or e × 10⁹ DOT—we need to introduce a dynamic issuance mechanism.

Why go dynamic? Because DOT will continue to be destroyed (for example, when purchasing coretime or paying transaction fees), and the amount destroyed is unpredictable. Ignoring destruction may lead to discrepancies between the total supply and the expected curve.

In the dynamic model, the issuance amount for each cycle depends on 'how far from the limit':

The farther away, the more issuance;

The closer to the limit, the less issuance.

This design has an additional benefit: when DOT is destroyed, the total supply decreases, and the gap between it and the cap widens, allowing the system to slightly relax the issuance limit in subsequent cycles, thus maintaining the balance and flexibility of the model.

In summary, decreasing curve + dynamic adjustment = it can allow the total amount of DOT to gradually converge to the limit while flexibly absorbing unpredictable destruction factors in the ecosystem, making the inflation mechanism more stable and sustainable. As for how to set the specific dynamic function, it requires deeper modeling and design, which should be further improved by new proposers.

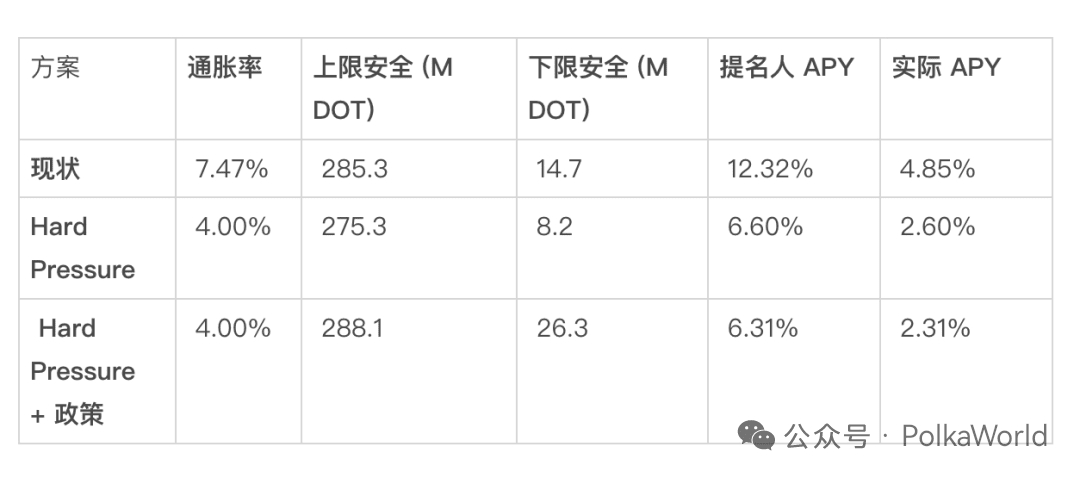

Data Comparison

From the comparison of the tables, we can draw the following conclusions:

Conclusion One: Simply cutting inflation will reduce security.

In the Hard Pressure scenario, inflation drops from 7.47% to 4%, resulting in the lower safety limit dropping directly from 14.7M DOT to 8.2M DOT. This means that the cost of attacking the network decreases, making Polkadot more susceptible to economic attacks.

Conclusion Two: Supporting policies can turn the situation around.

If the suggested policies mentioned above are introduced based on Hard Pressure, the lower safety limit not only does not decrease but instead rises to 26.3M DOT, higher than the current state. At the same time, it also ensures the same low inflation rate.

Conclusion Three: Yield will inevitably decline

Nominator APY drops from 12.32% to ~6%, actual APY drops from 4.85% to ~2.3%. The reduction in earnings is an inevitable cost of declining inflation, but by simplifying the nominator experience (removing penalty reductions and unbonding periods), participation enthusiasm can still be maintained.

Conclusion Four: Policy design is more critical than pure parameters

Cutting inflation can only change the issuance amount but can harm security. Institutional design (commissions, self-staking, mechanism optimization) can restore security while reducing inflation. 'Low inflation + high security' is not contradictory, as long as appropriate institutional support is in place.

Inflation is not the only variable; economic resilience is the core.

From this discussion about inflation, it can be seen that the Polkadot community is not simply pursuing a binary answer of 'high or low inflation,' but is exploring a path to maintain or even enhance security while reducing inflation.

Hard Pressure seems to be the most radical solution, but without accompanying policies, the safety lower limit will drop significantly, bringing risks to the network; however, once mechanisms like minimum commission and minimum self-staking are introduced, safety can not only be preserved but enhanced. Meanwhile, the earnings of nominators and validators will indeed be reduced, but through optimizing the staking mechanism and reducing participation friction, this negative impact can be partly offset.

This discussion also reveals a key point: economic models cannot rely solely on parameter adjustments; institutional innovation is also needed.

Reducing inflation is the direction, but it must be combined with supporting measures like commission mechanisms, self-staking requirements, optimizing the nominator experience, and decreasing issuance curves to form truly sustainable economic resilience.

Therefore, this is not just a discussion about 'how much DOT to issue,' but also a deep reflection on Polkadot's long-term governance and economic security. The future path may not simply be Hard or Medium but a new combination of parameters and systems.

Between 'low inflation' and 'high security,' the Polkadot community is searching for that balance.