Core Viewpoint (Thesis): WalletConnect protocol, as a key infrastructure of Web3, is the governance token, with its core value lying in whether it can successfully convert the massive technology adoption rate (penetration rate over 90%) into commercial revenue. In the short term, due to defects in the token economic model (high inflation staking, low liquidity) and macro market sentiment under pressure, if the planned 'charging per MAU' model is implemented, its current valuation (FDV $288 million) is significantly underestimated, with potential for several times return. However, this is a high-risk investment, and success fully depends on commercialization execution capability and ecosystem expansion capability.

I. Project Fundamentals: Absolute Industry Monopoly Position and Lagging Value Capture

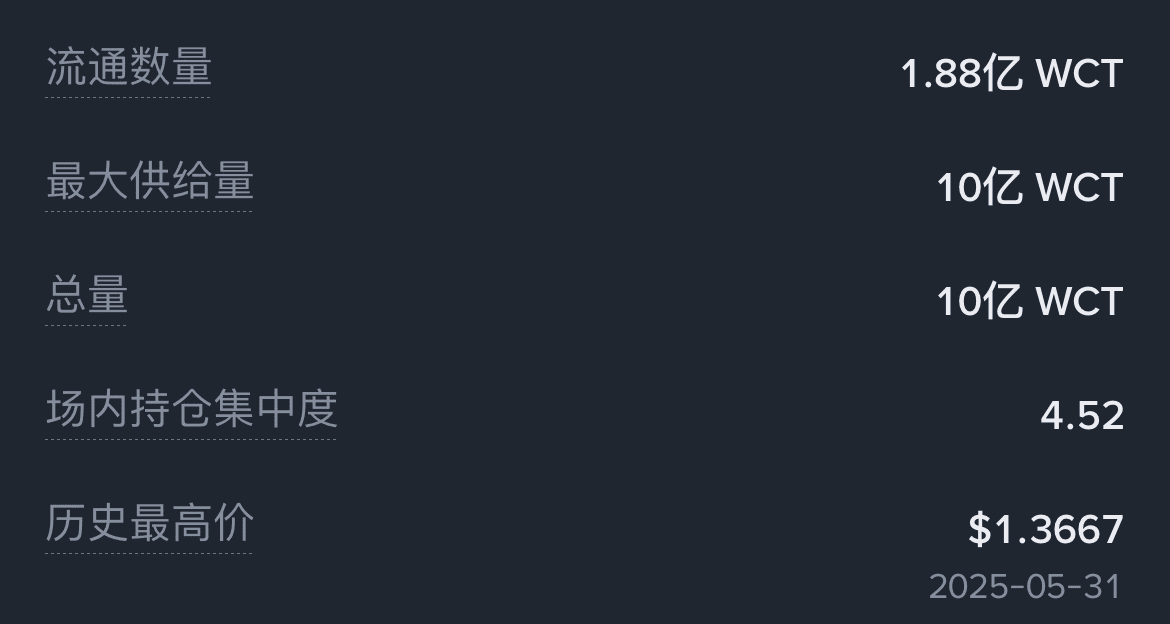

The value foundation of WCT is built upon the undisputed market leadership of the WalletConnect protocol.

• Market Share Data: The protocol has connected over 600 wallets and 67,000+ decentralized applications (DApp), completing a total of 300 million connections, with a penetration rate exceeding 90% in the Web3 field, becoming a 'necessary entry point' connecting users with blockchain applications.

• Network Effect Barrier: Protocol layer attributes bring a strong Metcalfe effect; the integration of each new wallet or new DApp exponentially expands the potential connection combinations of the network (600 wallets × 67,000 applications, approximately 400 million potential connections), making it difficult for competitors to surpass.

• Core Dilemma: Despite massive usage, 90% of the services are currently free, and the annual revenue of the protocol is only about $2 million, resulting in a price-to-sales ratio (PS) of up to a hundred times, leading to a severe disconnection between valuation and actual revenue.

II. Investment Theme: Paradigm Shift from 'Free Tool' to 'Value Gateway'

The essence of investing in WCT is betting that its team can successfully execute a commercial transformation to turn 'connections' into 'revenue'.

1. Clear Commercialization Path (The Road to Revenue):

◦ The team plans to launch a 'Connection Fee Tiered Model' to charge fees based on monthly active users (MAU) for high-frequency applications (e.g., exchanges, chain games), with a fee standard of about 0.1-0.3 WCT per instance.

◦ If this model is implemented, the expected annual revenue could reach $30 million. Based on this calculation, the fully diluted valuation (FDV) to revenue ratio (FDV/Revenue) will drop from the current hundred times to a reasonable range of ten times, leading to a reconstruction of the valuation system.

2. Massive Scalability (Total Addressable Market - TAM):

◦ Cross-Chain Integration: It has supported the Solana ecosystem and plans to expand to Bitcoin, Cosmos, etc., capturing the growth dividends of a multi-chain ecosystem.

◦ Web2 User Entry: Deep integration with wallets like MetaMask is expected to become a bridge for hundreds of millions of Web2 users to enter the Web3 world, bringing new user increments.