If traditional lending is like 'checking a savings passbook', then Huma is more like 'checking a cash flow statement'. It does not require you to pledge existing crypto assets but instead turns future incoming money (salary, invoices, remittances, receivables, etc.) into immediately usable liquidity through on-chain certificates, stablecoin settlements, and smart contract risk control—this is what Huma focuses on with PayFi (Payment + Finance): transforming 'accounts receivable' in real payment scenarios into 'financeable receivables'. The official positioning is as the 'world's first PayFi network', aiming to allow instant access to funds anytime, anywhere.

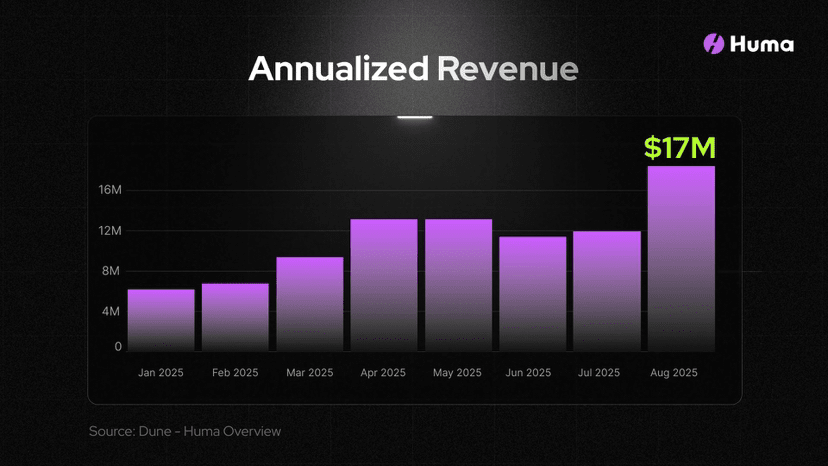

The core idea is straightforward: entrust the 'heavy risk control and computation' to on-chain contracts and data flows, while handing over 'fast settlement and disbursement' to stablecoins and high-performance chains. In November 2024, Huma announced its entry into Solana for practical reasons: lower transaction costs, higher throughput, and shorter finality time, suitable for high-frequency small amount funding flows like 'payment + financing'. Huma also disclosed in the announcement that its historical transaction volume exceeded $2 billion; by May 2025, the team stated in the airdrop article that the cumulative amount over two years had surpassed $4.4 billion, indicating real business growth (note this is the official statement).

Huma 2.0 has turned the product into a 'ready-to-use yield platform':

Classic mode: a stable double-digit USDC annualized return (the example at the time of article publication was 10.5% APY, updated dynamically monthly), suitable for LPs seeking stable cash flow;

Maxi mode: gives up interest, focuses on caps for Feathers (points), suitable for heavy users who want to 'accumulate points for benefits';

Depositing into Classic will earn you $PST (PayFi Strategy Token), a composable LP certificate that can be exchanged, collateralized, and cycled within the Solana ecosystem (integrating Jupiter, Kamino, etc.). This 'mode switching + composable' design blends 'real returns' with 'DeFi gameplay'.

From a business perspective, what Huma does is essentially rework traditional factoring, accounts receivable financing, and salary advances through an on-chain programmable and auditable method:

Funding side: LPs deposit USDC into the pool and earn returns generated from real payment activities;

Demand side: merchants/individuals convert 'future receivables' into on-chain certificates and discount them according to rules;

Intermediate layer: smart contracts set limits, fee rates, and repayment processes based on historical cash flows and risk control rules. In the official explanation, it is emphasized that PayFi can timely convert 'accounts receivable and other real cash flows' into cash, improving cash turnover for businesses and individuals.

Many people are concerned about how much they can borrow? A common saying in the community is that 'you can get 70%-90% of your expected future income', understood as 'salary/invoice advances'. However, this is not an official blanket commitment; the specific ratio depends on the funding pool strategy and risk control factors, subject to official and actual contract terms; you can regard '70%-90%' as a community's intuitive description of 'considerable limits'.

On tokens and incentives

HUMA launched airdrop Season 0 (5% of total supply) around the TGE in 2025, focusing on real liquidity providers, ecological partners, and community contributors; governance tools will be gradually opened thereafter. For LPs, HUMA can be staked to earn reward bonuses and enhance the 'multiplier factor' of LP positions; this design, which is 'strongly tied to usage', aims to treat tokens as usage-driven fuel rather than mere market sentiment.

A vivid metaphor:

Assuming you are a cross-border e-commerce merchant, you sell goods, but it takes 30 days for the payment to arrive; what Huma does is 'flatten' this 30 days—based on historical cash return performance and risk control parameters, they provide you with a portion of the money upfront, and settle the difference when the buyer's payment arrives. You wait 30 days less, gaining 30 more days for inventory turnover and advertising time—in business, this often makes the difference between living and not living.

How is risk controlled?

The authenticity of the asset side and the rhythm of cash returns are the lifeline of PayFi; Huma claims that contracts have undergone multiple audits (Halborn, Spearbit, Certora, etc.), but application parties still need to manage credit limits, black and white lists, and anomaly monitoring; stablecoins and payment networks (such as Mastercard and MoonPay's layout) are accelerating clearly in 2025, which is beneficial for the settlement and circulation of PayFi, but this part is public infrastructure of the industry, still affected by compliance and integration progress.

Huma does not 'create credit out of thin air'; it transforms 'future receivables' into present productivity. When real cash flows can be programmatically processed, audited, and settled, PayFi may become the most pragmatic track in Web3.

@Huma Finance 🟣 #HumaFinance $HUMA