This research provides a comprehensive analysis of the dynamics of cryptocurrency token listings among major centralized exchanges and Binance's related issuance plans during the period from January 2024 to June 2025. The study subjects include several mainstream trading platforms, including Binance, Binance's perpetual contract market, Coinbase, OKX, Upbit, Bithumb, and Bybit. The research scope covers issuance channels for spot, perpetual contracts, and decentralized exchanges (DEX), focusing on two types of listing activities: first listings (new assets directly allocated through mechanisms such as airdrops, i.e., token generation events (TGE) or initial exchange offerings) and secondary listings (tokens that have trading history on other platforms listed on a new exchange).

This study systematically reviews the listing trends of different exchanges, the distribution of fully diluted valuation (FDV), the performance of tokens after listing, and cross-platform listing paths, with the core goal of gaining in-depth insights into Binance's dominant role as a core listing channel, while conducting comparative analysis of strategies and performance differences among other platforms such as Coinbase, OKX, Upbit, Bithumb, and Bybit. Ultimately, the aim is to reveal the diverse models and intrinsic mechanisms of token issuance, price performance, and market expansion in different liquidity environments.

Listing activities of exchanges

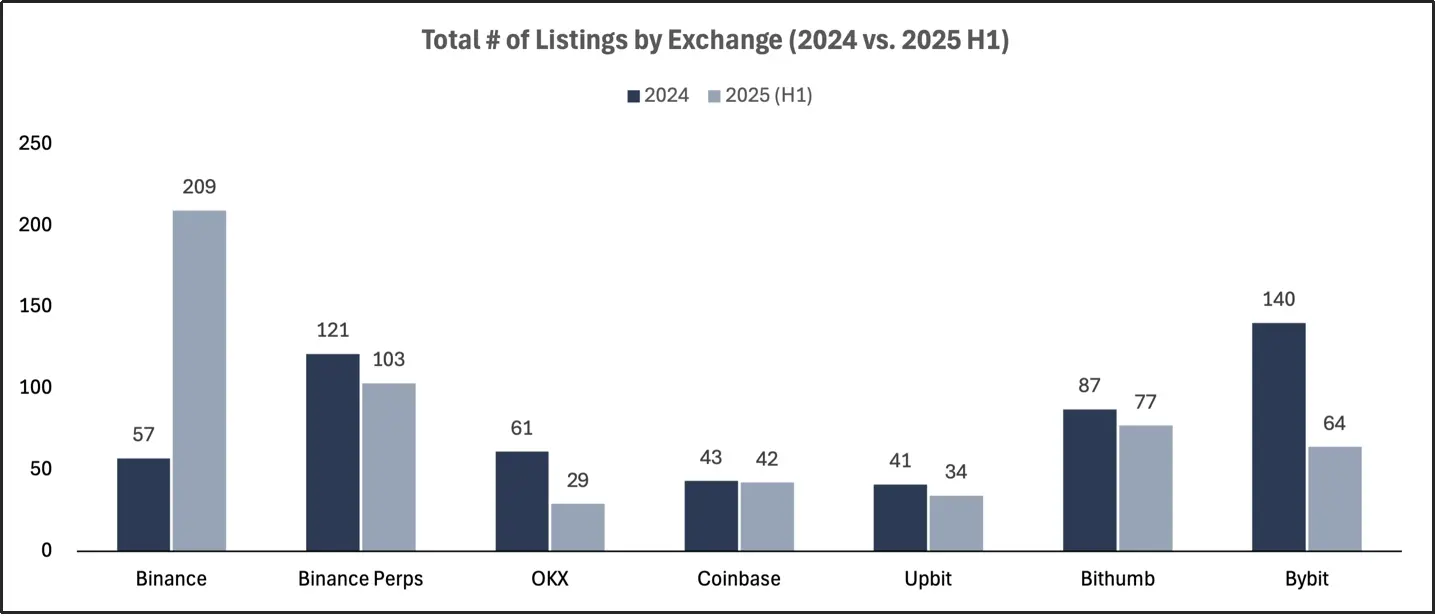

The total number of listings across exchanges for the entire year of 2024 and the first half of 2025

In the first half of 2025, listing activities in cryptocurrency exchanges saw significant growth, but first listings and secondary listings exhibited distinct development paths. Binance significantly expanded its token listing ecosystem, driven by its DEX issuance business and the ongoing expansion of the perpetual contract market; in contrast, other mainstream exchanges showed a slowdown or stabilization in their listing rhythm, resulting in a trend towards centralization.

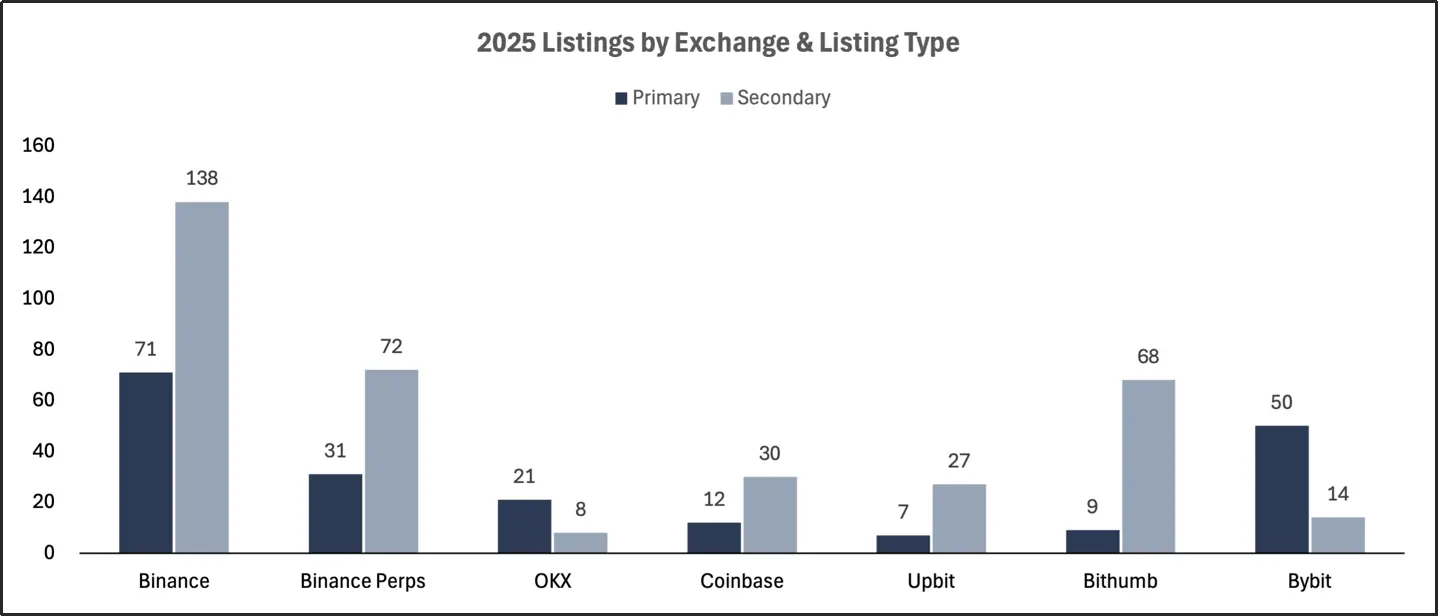

The number of first and second listings across exchanges in 2025

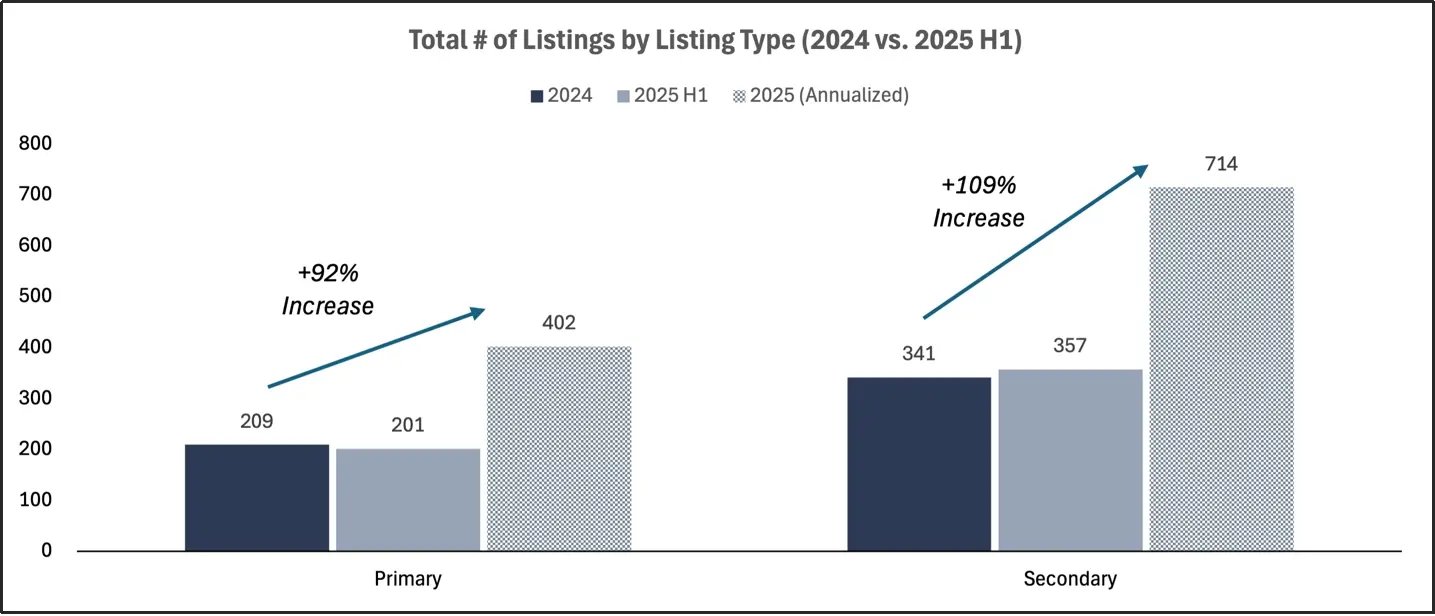

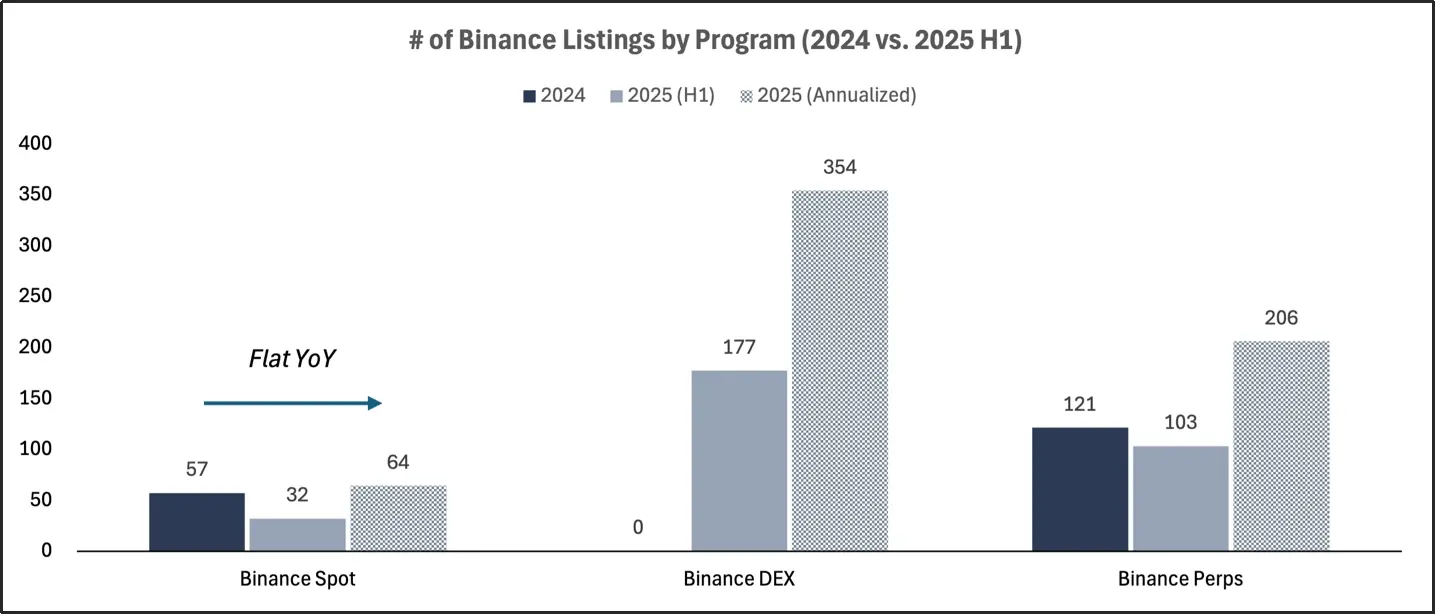

Total number of listings across exchanges for the entire year of 2024, the first half of 2025, and the projected total for 2025

In the first half of 2025, Binance remained the most active exchange for first listings globally, launching 71 first listing projects, all driven by DEX issuance channels, specifically including token discovery platform Binance Alpha's airdrops and initial decentralized issuance (IDO). Upbit and Coinbase maintained relatively stable first listing rhythms, with approximately 12 projects launched in the first half, primarily consisting of mainstream cryptocurrencies with larger market capitalizations. In contrast, Bybit and OKX have significantly reduced their first listing scales, dropping from double digits in 2024 to single digits in the first half of 2025. Overall, the total number of first listings across the industry is expected to increase significantly, from 209 in 2024 to 402 in 2025, representing a year-on-year increase of 92%; this growth is primarily driven by decentralized issuance methods such as Binance Alpha and IDO.

In terms of secondary listings, Binance launched a total of 138 secondary listing projects during the same period, the vast majority of which were promoted through the Binance Alpha platform to relist existing tokens. Coinbase, Upbit, and Bithumb also placed more emphasis on secondary listings, which accounted for about 80% of their total listing volume in 2025. Binance's perpetual contract market is also significantly biased towards secondary listings, with their number nearly doubling that of first listings. The number of secondary listings for the year is expected to achieve a 109% year-on-year increase, rising from 341 in 2024 to 714 in 2025. Under the leadership of Binance and its Alpha program, secondary listings are rapidly becoming the dominant form of listing activity on exchanges in 2025.

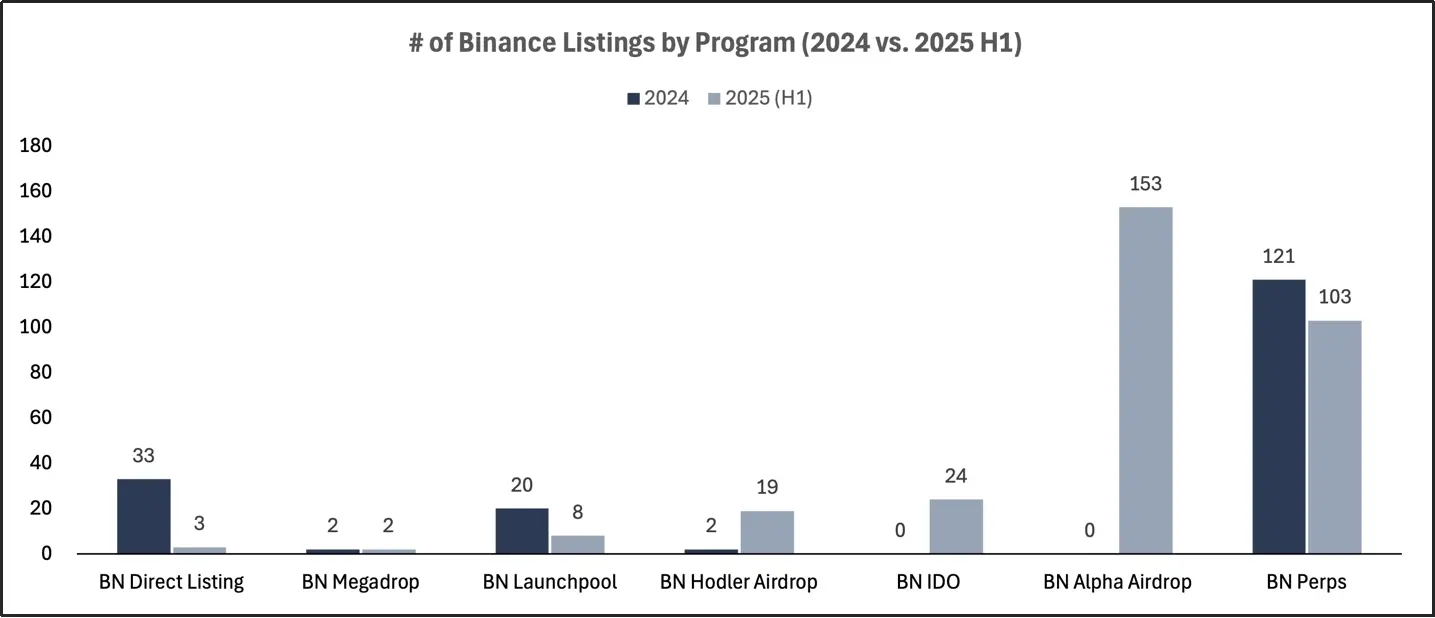

The number of tokens listed on Binance by project for the entire year of 2024 and the first half of 2025

In Binance's token generation events (TGE), Alpha airdrops and IDOs dominate, collectively contributing to 84% of new asset issuance. Year-on-year comparison indicates that the overall spot listing plan remains stable, with 64 expected for 2025, almost on par with 57 in 2024. This statistic covers various issuance methods, including direct listings, Launchpool, Megadrop, and holder airdrops.

The total number of listings for Binance's spot, decentralized exchanges, and perpetual contracts for the entire year of 2024, the first half of 2025, and projected for the full year of 2025

In Binance's futures listing projects, secondary listings dominate. Among the 103 projects launched in the first half of 2025, 72 were secondary listings, consistently generating strong trading volumes, but their role in driving new token generation events (TGE) is relatively limited. Currently, Binance's listing strategy has clearly shifted towards DEX-based issuance as the core, while traditional spot listing mechanisms maintain strict auditing and control.

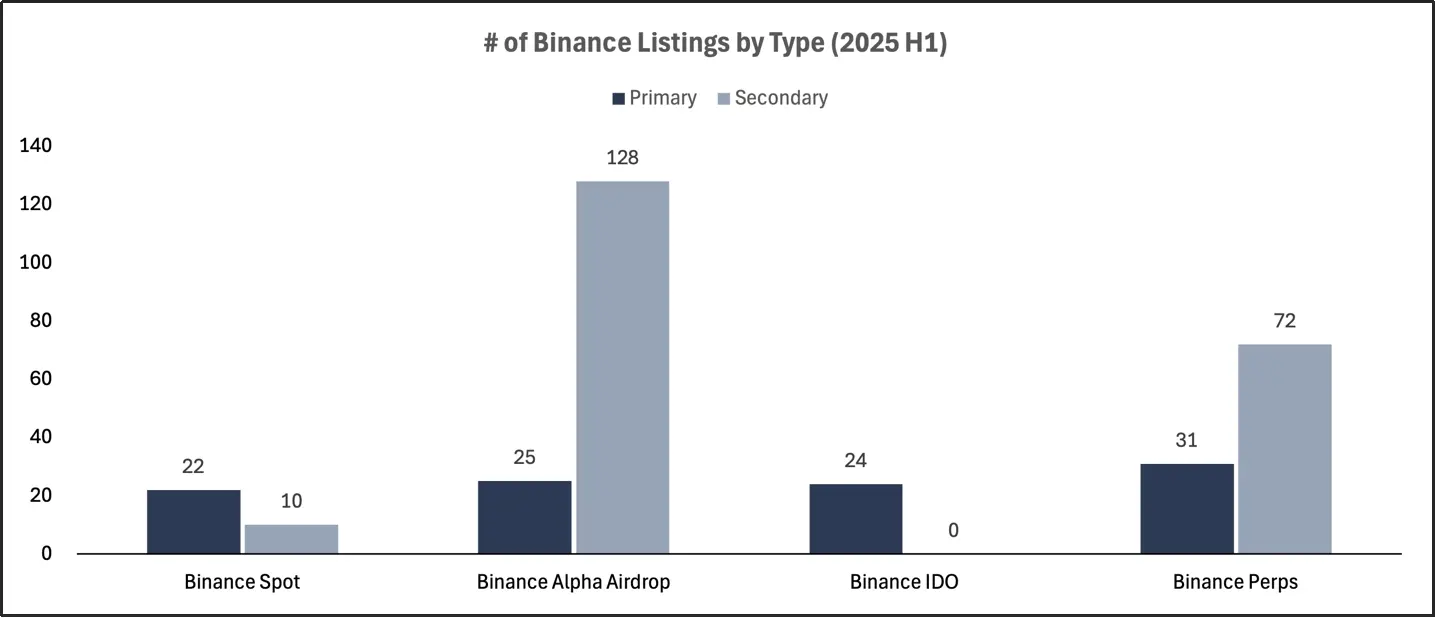

The number of first and second listings of various types on Binance in the first half of 2025

The listing performance of various exchanges

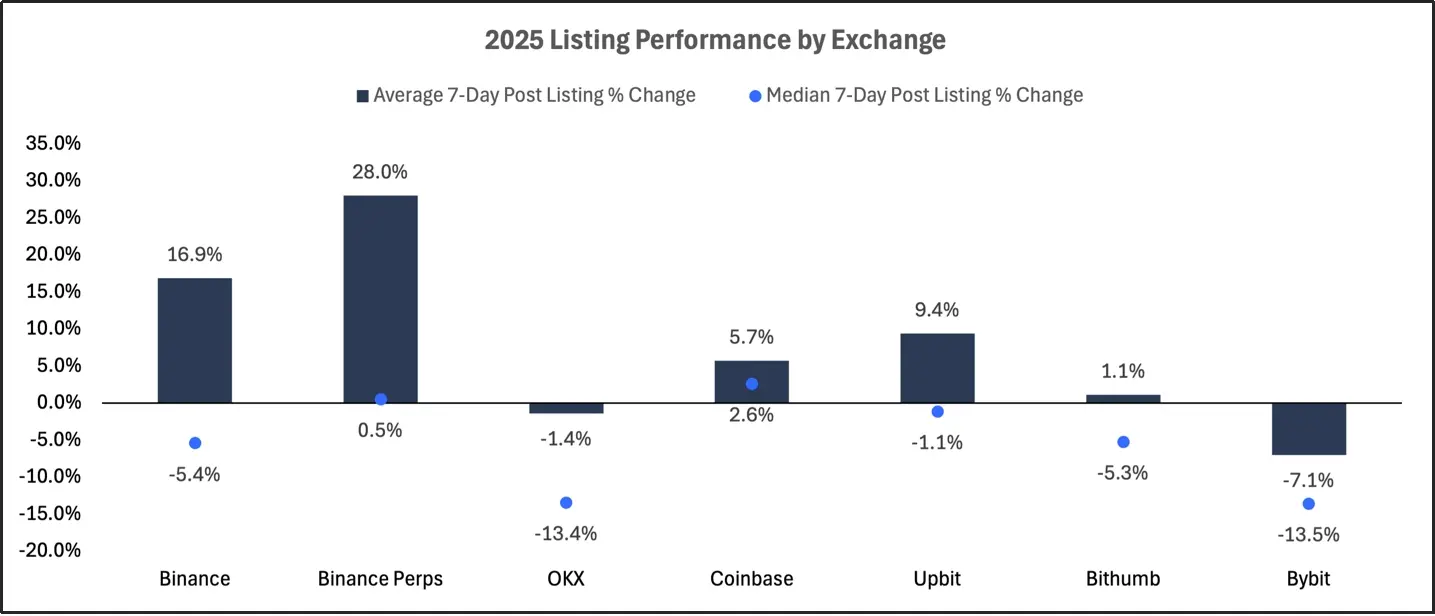

Token performance within 7 days of listing on various exchanges in 2025

The seven-day performance data of listing projects across exchanges indicates a significant differentiation between first listings and secondary listings. For nearly all platforms, tokens from first listings performed weakly, with both average and median returns falling into negative territory after the token generation event (TGE). In contrast, secondary listings generally exhibit stronger and more stable positive returns, largely due to their existing market consensus and liquidity foundation.

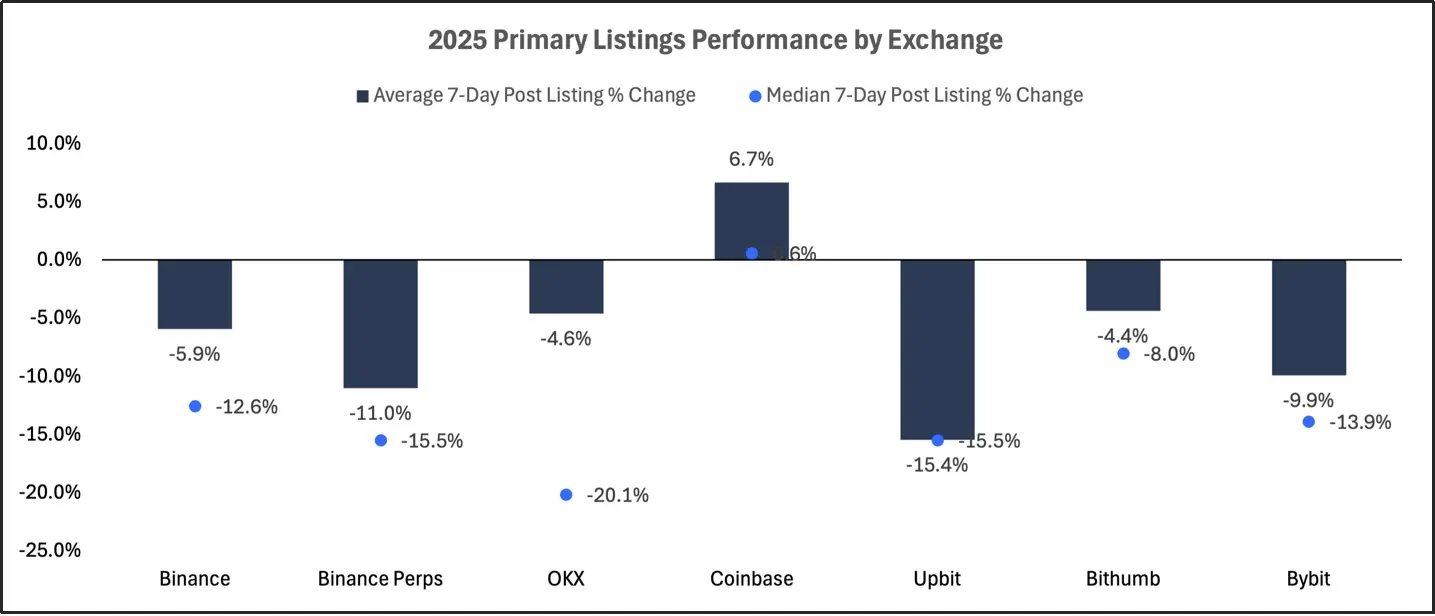

Token performance within 7 days of first listings for each exchange in 2025

New coin projects listed on the main board of various exchanges generally performed poorly, recording negative returns across the board over the past week. Although Coinbase showed a slight average positive return (+6.7%), its median return remained flat, indicating a lack of upward momentum. The performance of new coins listed through Binance's spot, Alpha airdrop, and IDO channels fell short of expectations, with median returns ranging from -5% to -19%. Exchanges such as OKX, Bithumb, and Upbit also displayed continuous losses, with average returns between -4% and -15%. Overall, regardless of the exchange or project channel used for listing, new coins seem to face widespread selling pressure immediately after listing.

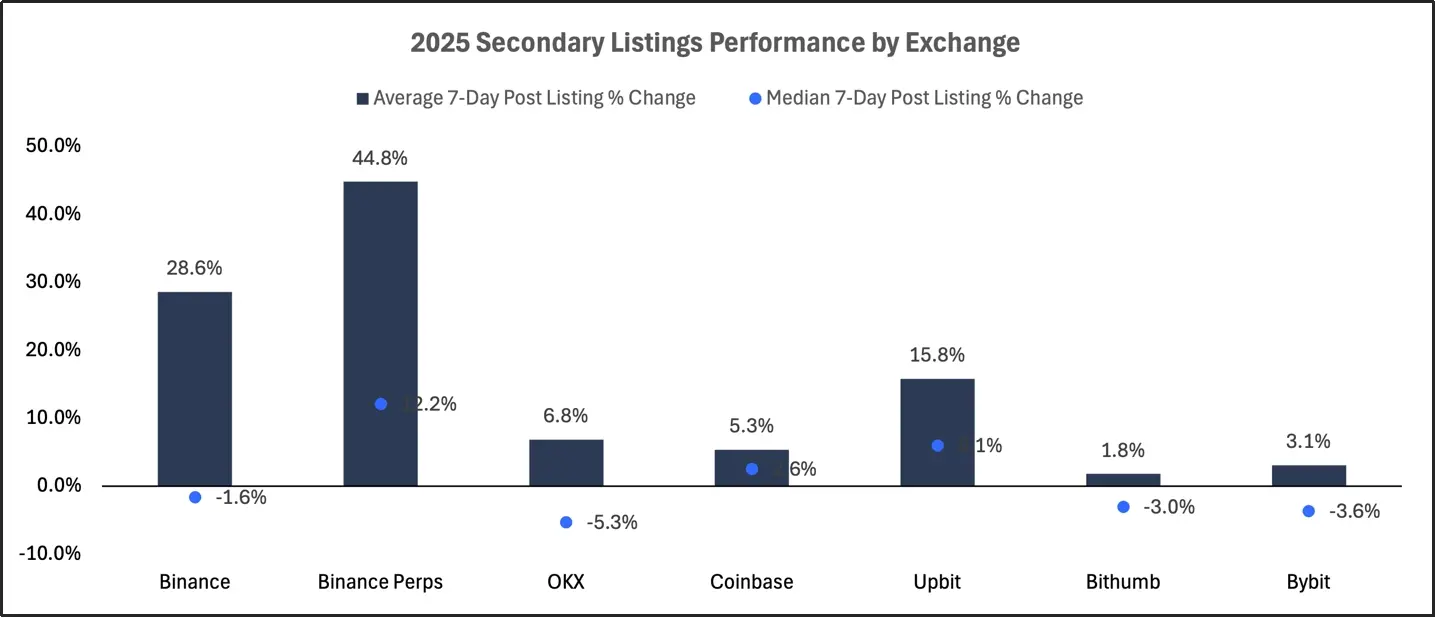

Token performance within 7 days of secondary listings across exchanges in 2025

Token performance within 7 days of listing across exchanges shows a significant difference between first listings and secondary listings. In almost all exchanges, first listings performed poorly, with both average and median returns post-token generation event (TGE) being negative. In contrast, secondary listings often yield stronger and more stable returns, thanks to their existing market recognition and liquidity.

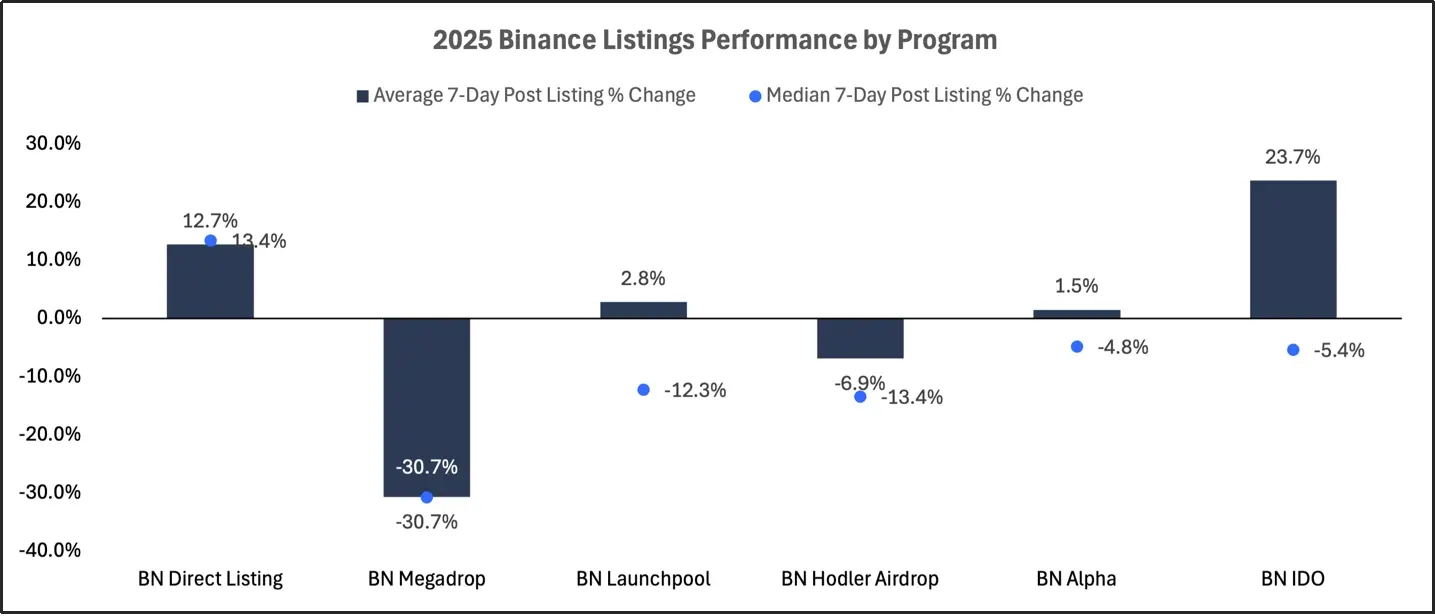

Token performance within 7 days of listing for Binance's projects in 2025

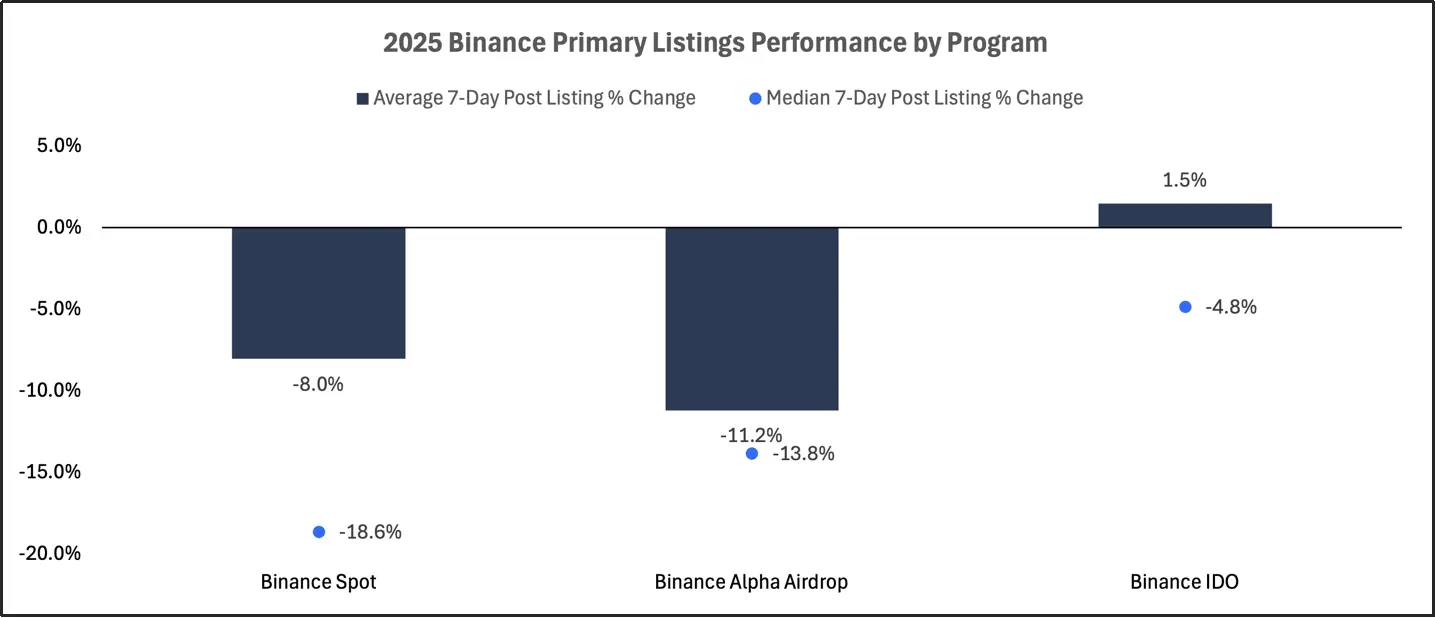

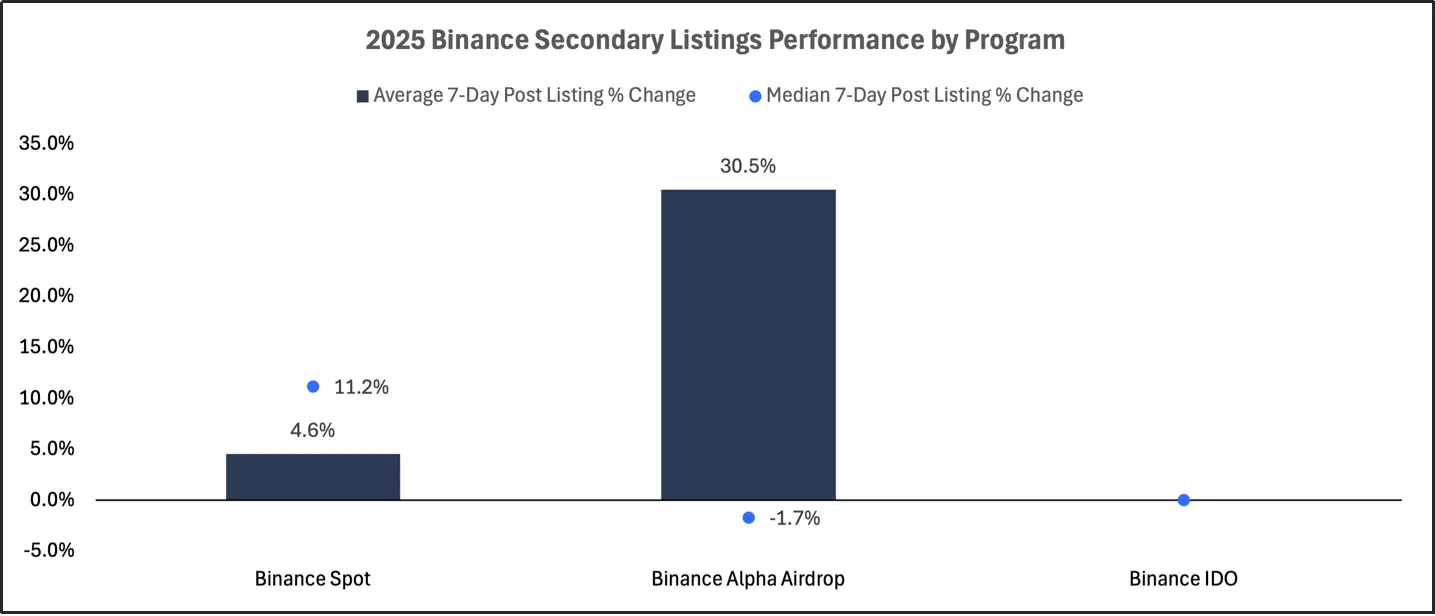

The average return rate for first listings via initial decentralized exchange offerings (IDO) is +1.5%, but a median of -4.8% highlights the limited coverage of successful cases. The performance of first listings via Alpha airdrop ranks at the bottom, with an average return rate of -11.2% and a median of -13.8%. First listings via spot have an average return rate of -8.0% and a median of -19%, ranking the lowest among all projects. The performance of secondary listings in both spot and futures outperforms their respective first listings, further confirming a notion: that existing tokens tend to perform better when listed on new exchanges than during their token generation event (TGE). The strongest performance after listing on Binance has always been secondary listings, while first issuances, especially those through Alpha and spot channels, generally perform poorly.

Token performance within 7 days of first listings for Binance's projects in 2025

The token performance of Binance's projects in secondary listings within 7 days in 2025

Peak fully diluted valuation (FDV) ratio and time analysis

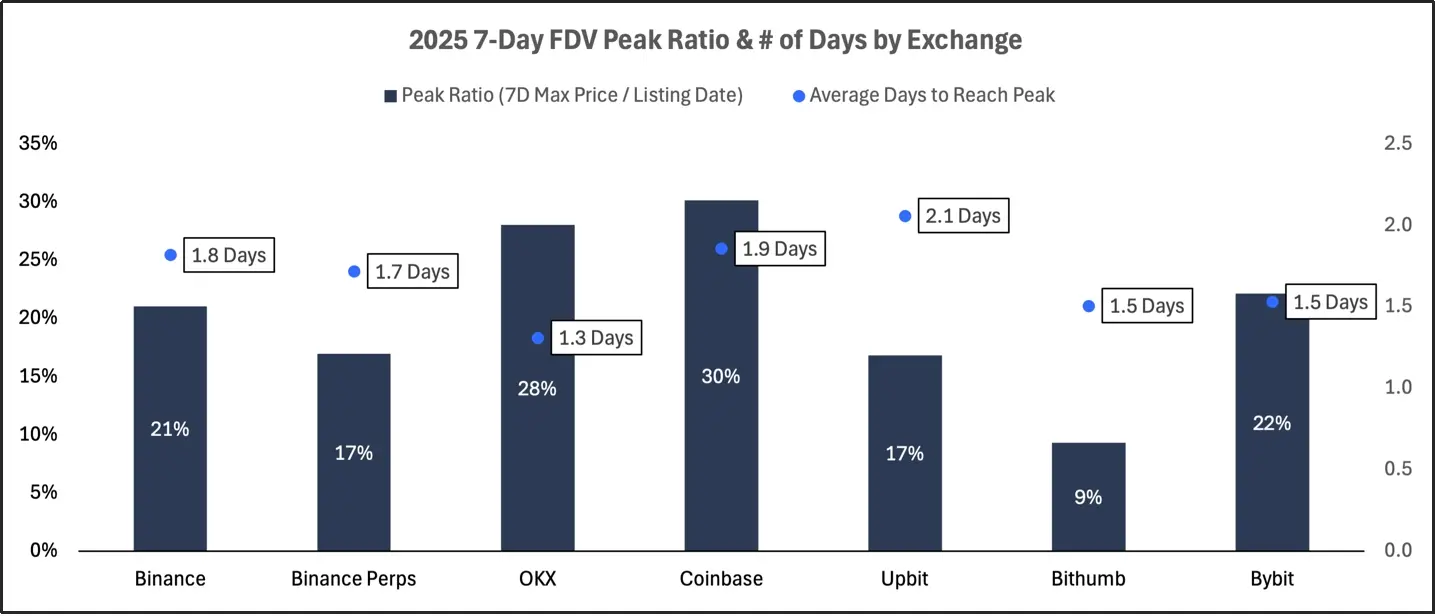

The FDV peak ratio and average number of days to reach peak for each exchange within 7 days in 2025

This section analyzes the peak fully diluted valuation (FDV) ratios and the average number of days required to reach these peaks. These indicators reveal the dynamics of price discovery: a higher FDV peak ratio reflects stronger early demand and upward momentum, while a longer time to peak indicates sustained buying interest rather than initial speculation.

The calculation method for the peak FDV ratio in this article is: the highest price within 7 days after listing divided by the closing price on the listing day.

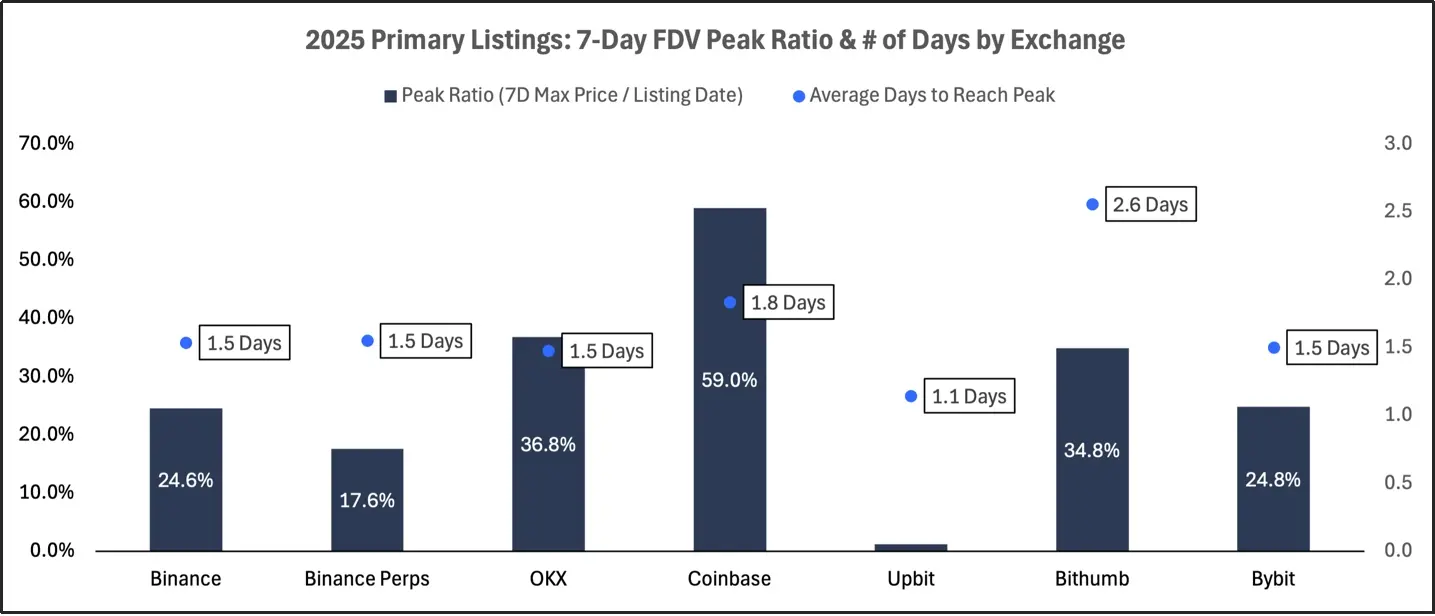

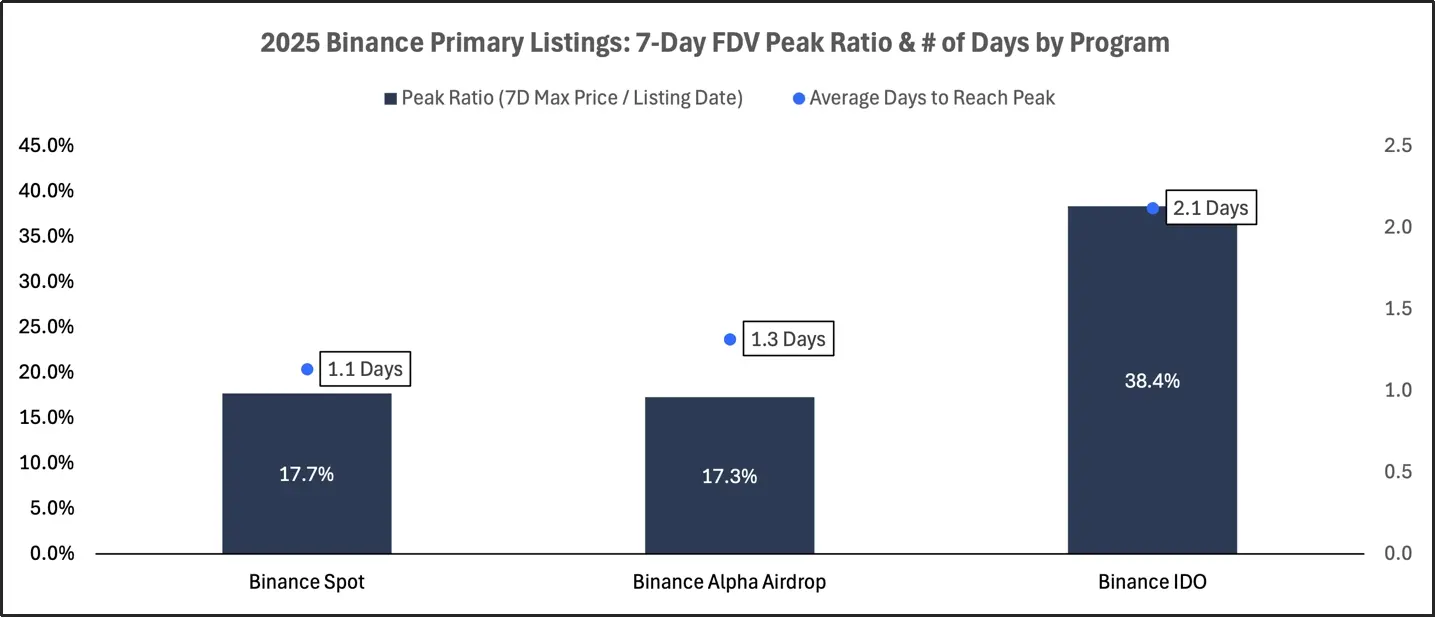

The FDV peak ratio and the average number of days to reach peak for the first listings in each exchange within 7 days in 2025

Among first listing projects, Coinbase and OKX stand out with peak FDV ratios of 59% and 37%, respectively, both achieved within approximately 1.5 to 1.8 days. The first listings through Binance IDO channels also performed strongly, with an average peak FDV ratio of 38%, achieved within 2.1 days, reflecting sustained and stable market demand. In contrast, the peaks for projects via Alpha airdrop and direct spot listings arrived earlier and at lower levels, with FDV ratios only between 17% and 18%, typically reaching their summit within 1.1 to 1.3 days. Upbit and Bithumb's listing projects also surged quickly but showed a clear lack of follow-up momentum, indicating limited support from secondary market buying. Overall, most first listing projects reach their peaks quickly in the early stages, with relatively limited upward potential.

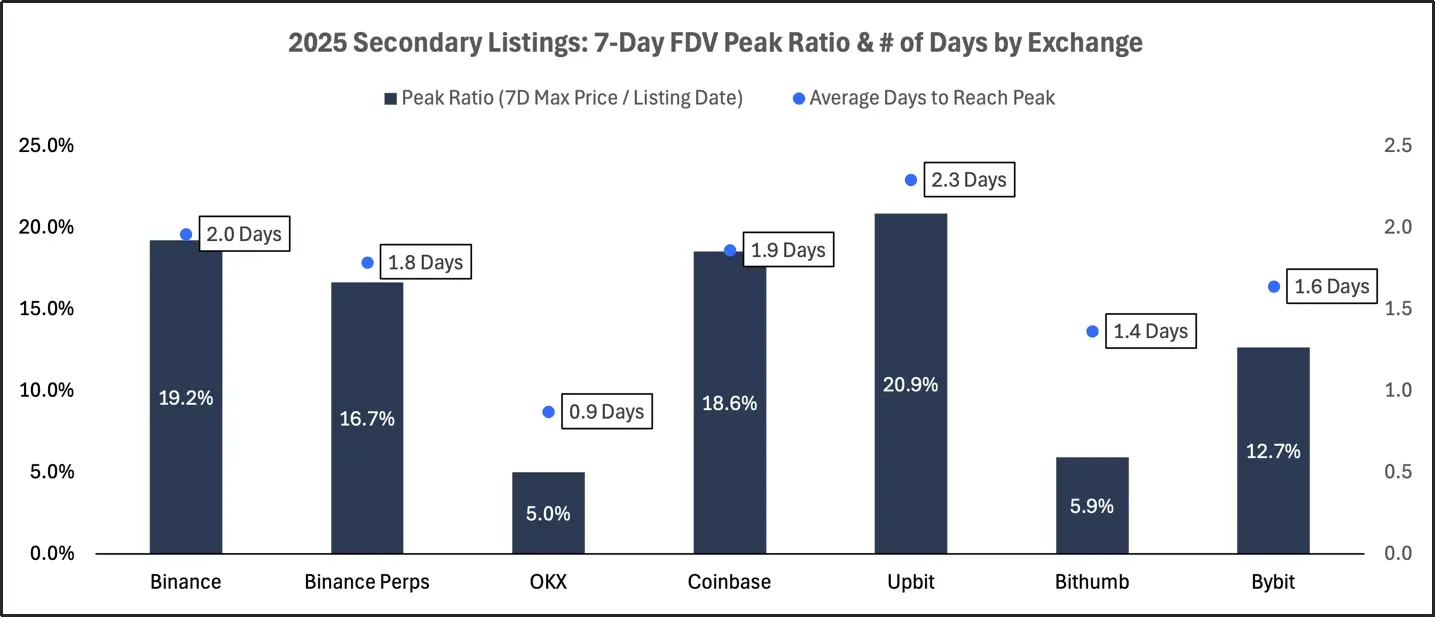

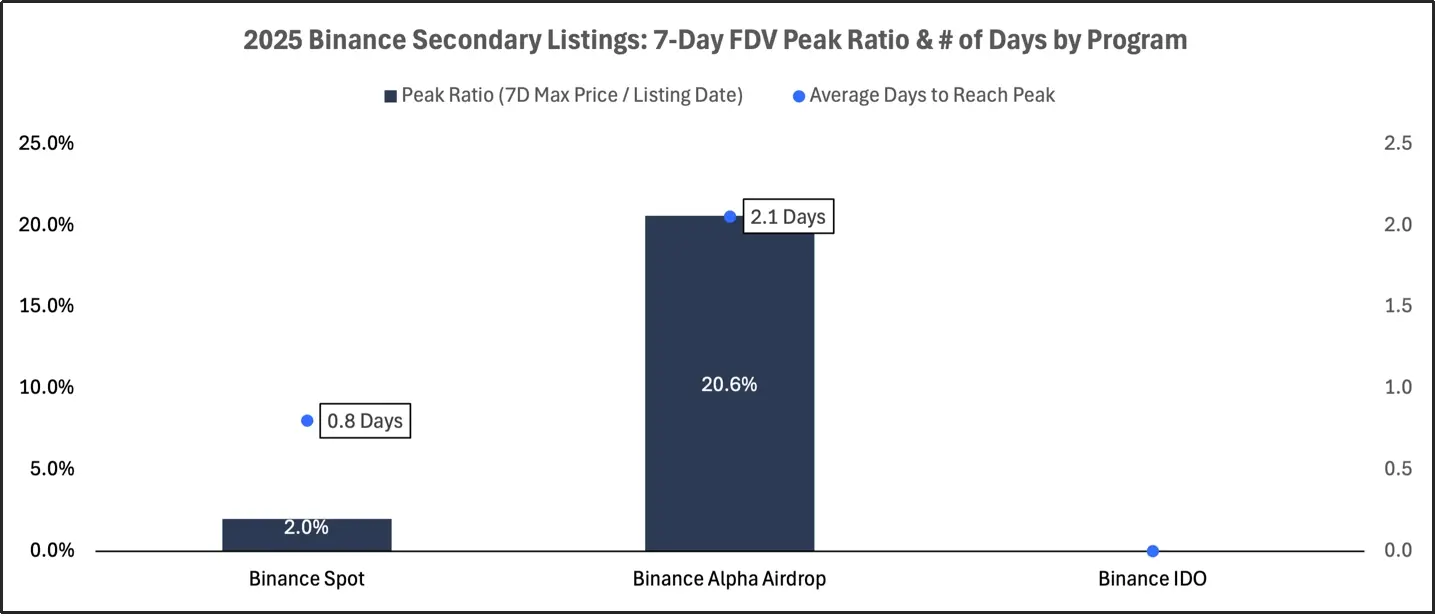

The FDV peak ratio and the average number of days to reach peak for secondary listings within 7 days in each exchange in 2025

The peak performance of Binance's spot and Alpha second listings is robust (about 20%-30%), but the time to peak for Alpha second listings is longer (2.1 days), and they are more affected by extreme values. Upbit and Coinbase's second listings exhibit a similar trend, with peak FDV ratios of 18%-21%, taking about 2 days to reach peak. OKX and Bybit's second listings have peaks that appear quickly but perform poorly, with an upward potential of less than 10%, reaching peaks in less than 1.5 days. Overall, the price discovery curve for second listings is healthier and more stable.

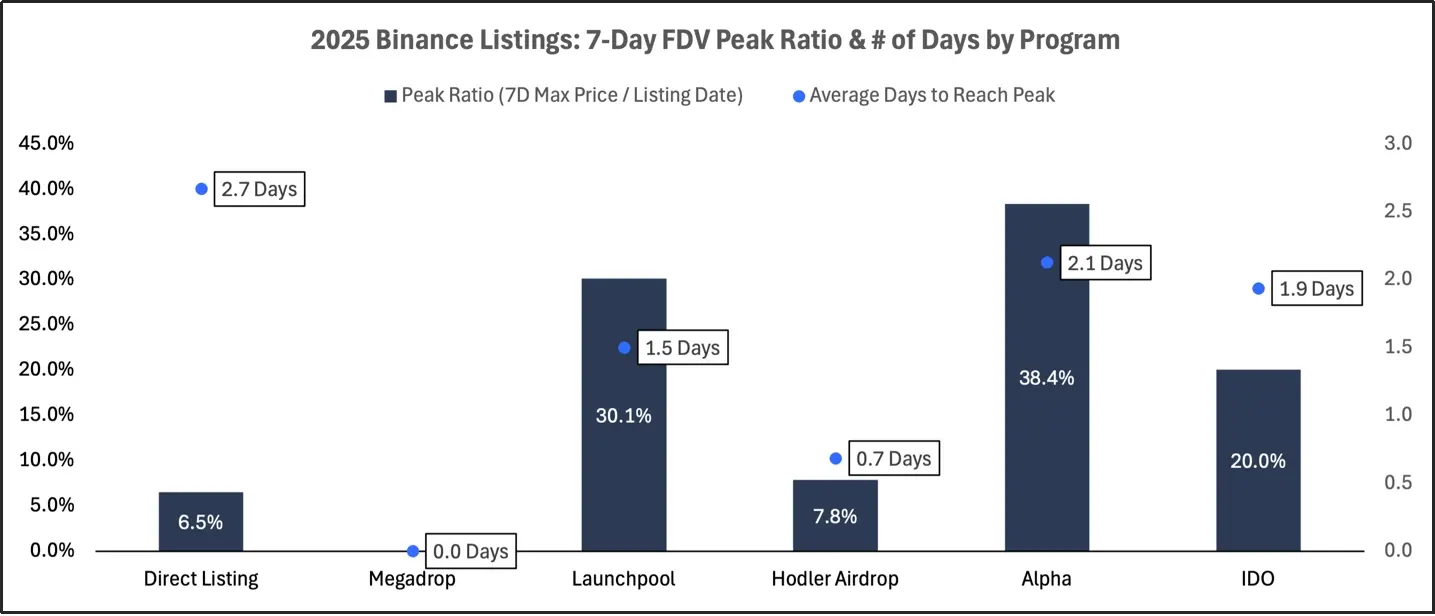

The FDV peak ratio and average number of days to reach peak for Binance's projects within 7 days of listing in 2025

The first listing via Binance IDO achieved the highest peak ratio among all projects (38%), and it took the longest to reach peak (2.1 days), indicating strong and sustained demand at the time of project listing. The peak for first listings via Alpha airdrop occurred earlier and at a lower level, with an FDV ratio of 17% within 1.3 days, suggesting that early momentum was dominant. The performance of first listings via spot is similar to Alpha, with an average peak of 18%, and peaks typically occurring on the first day of listing. The peak for Binance's second listing via spot appeared quickly but was only 2%, with many projects reaching their peak on the listing day. Overall, the peak potential of Binance's spot listings is limited, and prices tend to decline quickly after reaching peaks.

The FDV peak ratio and the average number of days required to reach peak for Binance's projects within 7 days of first listing in 2025

The FDV peak ratio and average number of days to reach peak for Binance's projects within 7 days of secondary listings in 2025

The listing situation based on fully diluted valuation (FDV) distribution

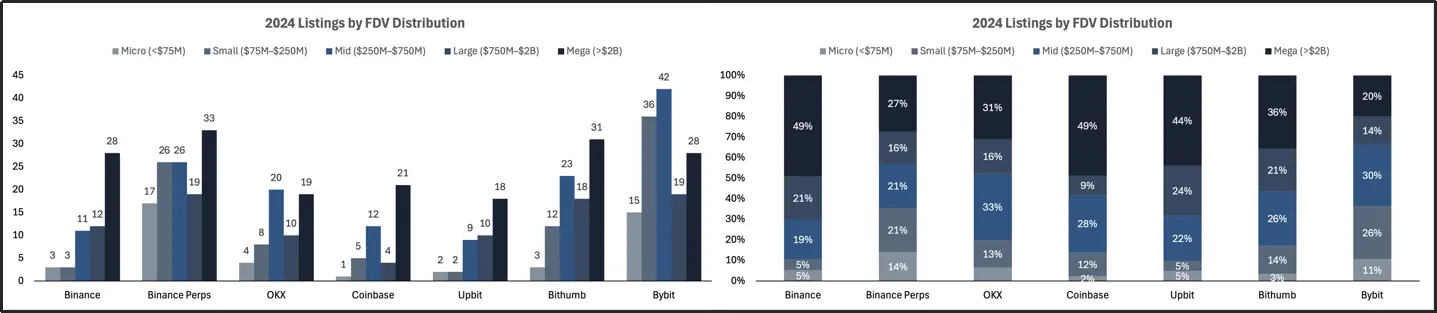

Project valuation levels distributed by fully diluted valuation (FDV) for each exchange in 2024

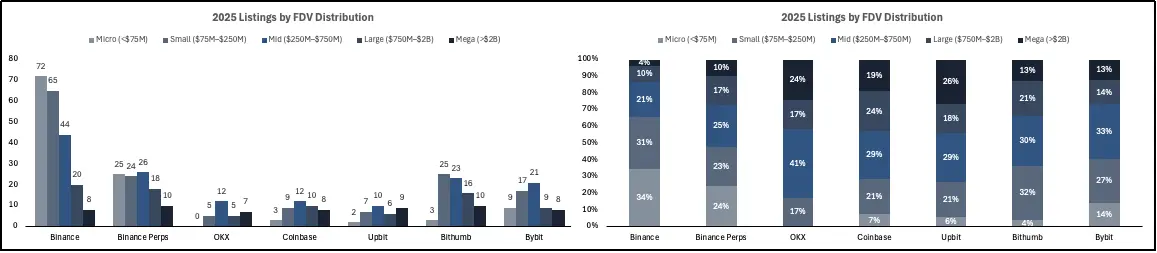

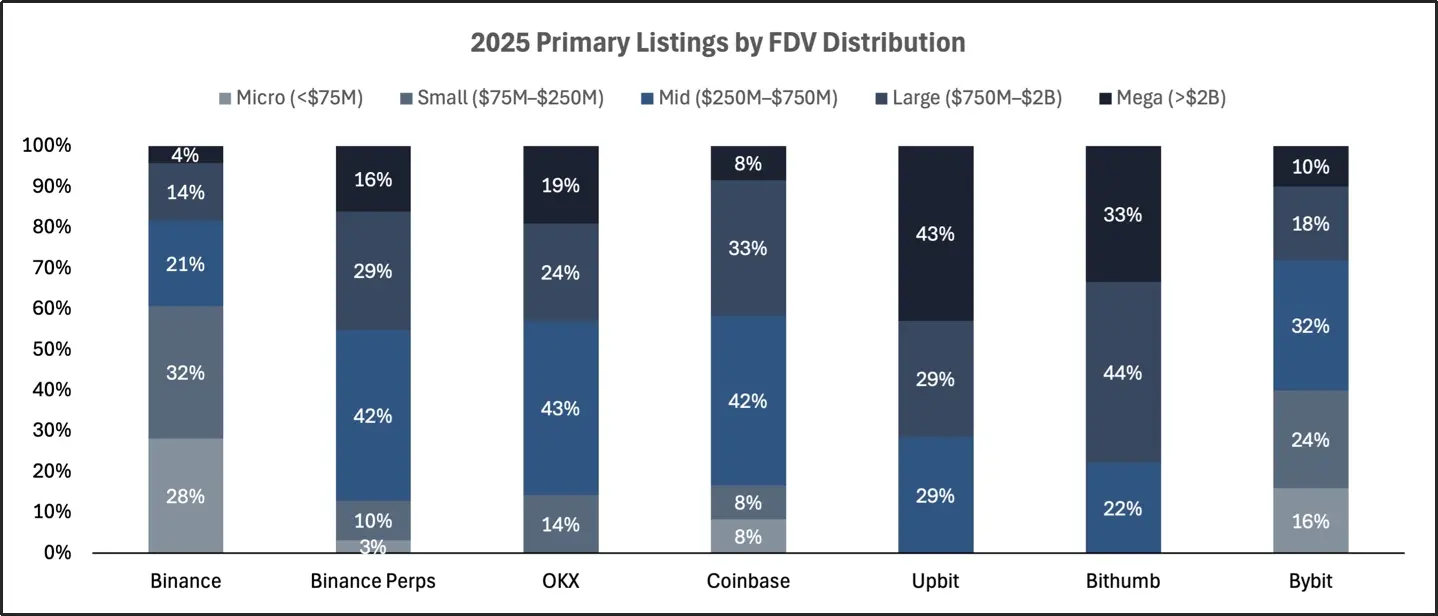

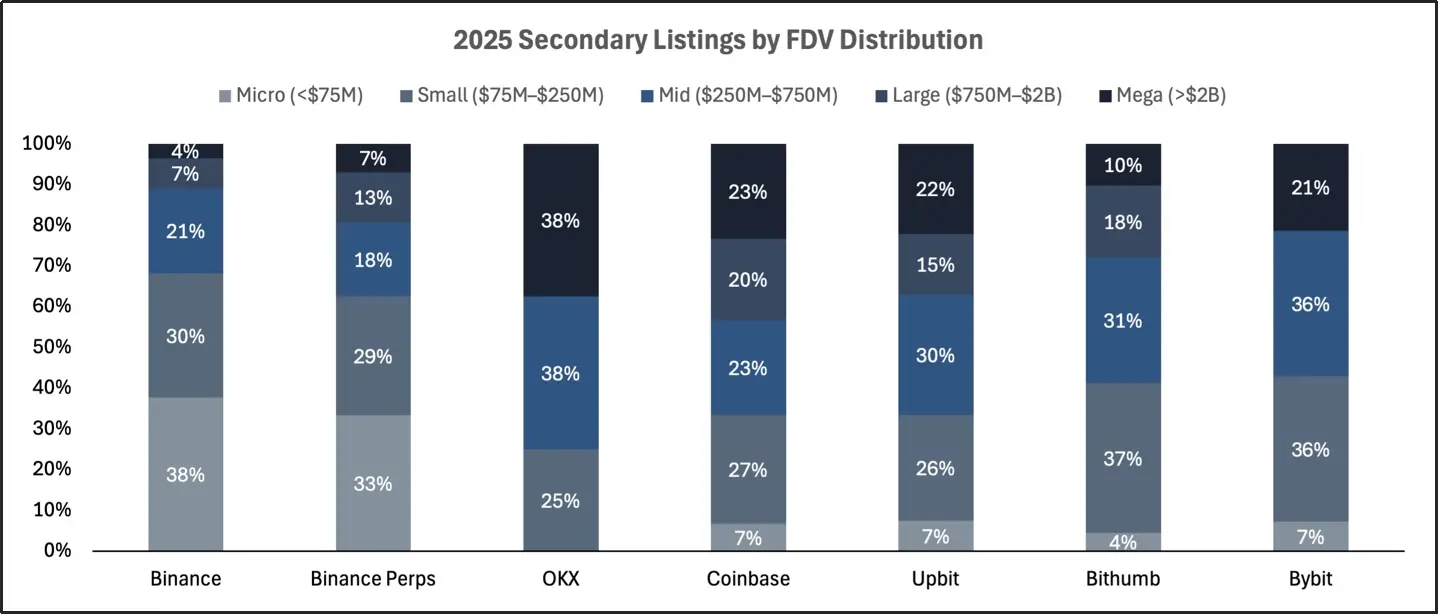

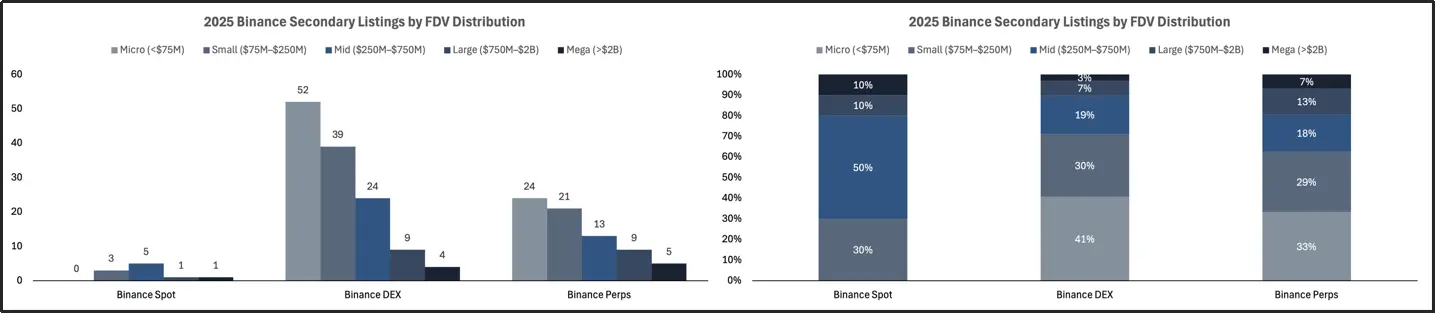

Project valuation levels distributed by fully diluted valuation (FDV) for each exchange in 2025

This section will analyze the fully diluted valuation (FDV) of listed projects to assess how different exchanges and listing plans allocate trading volume by project size. For first listing projects, FDV is calculated based on the closing price on the listing day; for secondary listing projects, FDV reflects the valuation prior to listing. By comparing various exchanges and Binance's related plans, we can identify the patterns of how listing platforms filter tokens and execute segmented issuance across different valuation levels. The valuation levels are specifically divided into: micro-cap (≤ $75 million), small-cap ($75 million–$250 million), mid-cap ($250 million–$750 million), large-cap ($750 million–$2 billion), giant-cap (> $2 billion).

The ratio of project valuation levels distributed by fully diluted valuation (FDV) for each exchange in 2024

The first listing projects of Upbit and Bithumb are heavily skewed towards large-cap and giant-cap tokens, with projects having a fully diluted valuation (FDV) of over $750 million accounting for 72% and 77%, respectively, of their listings, among which 43% of Upbit's projects belong to the giant-cap category. Coinbase and OKX's first listing projects are concentrated in the mid-to-large cap range, with 75% of projects having an FDV exceeding $250 million, mostly within the range of $250 million to $750 million. Binance's futures first listing projects also tend towards high FDV types, with 87% of projects having an FDV over $250 million. Bybit's distribution is the most balanced, with micro-cap accounting for 16%, small-cap for 24%, mid-cap for 32%, and large-cap and giant-cap combined accounting for 28%. Overall, first listing projects are usually dominated by high FDV projects, but in 2025, influenced by the Binance DEX issuance plan, this trend has shifted towards low FDV projects.

The ratio of project valuation levels distributed by fully diluted valuation (FDV) for each exchange in 2025

Driven by Binance Alpha, the secondary listing projects on Binance tend to be small-scale, with fully diluted valuations (FDV) below $250 million. Bybit and Coinbase's secondary listing projects have a broader FDV distribution. The secondary listing projects of Korean exchanges, namely Upbit and Bithumb, are heavily skewed towards large projects. These patterns indicate that secondary listings provide a more flexible and accessible channel for projects of varying maturity.

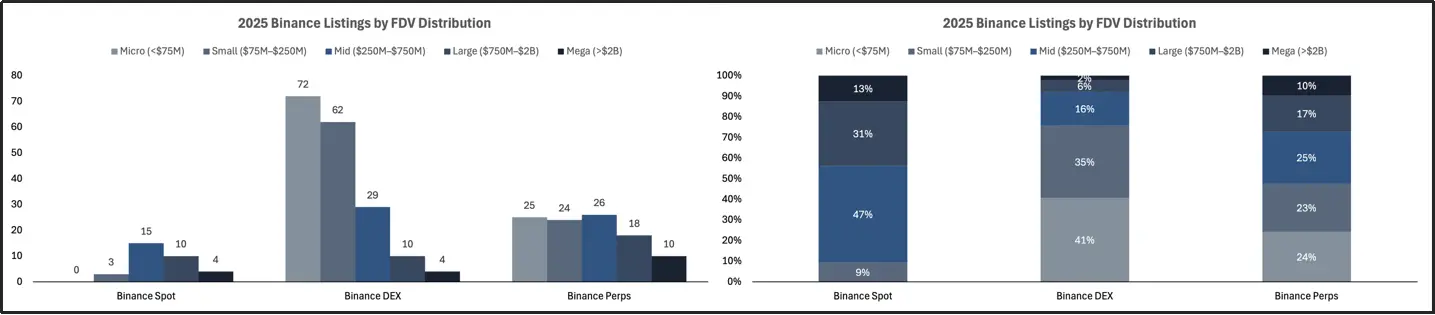

Project valuation levels distributed by fully diluted valuation (FDV) for Binance in 2025

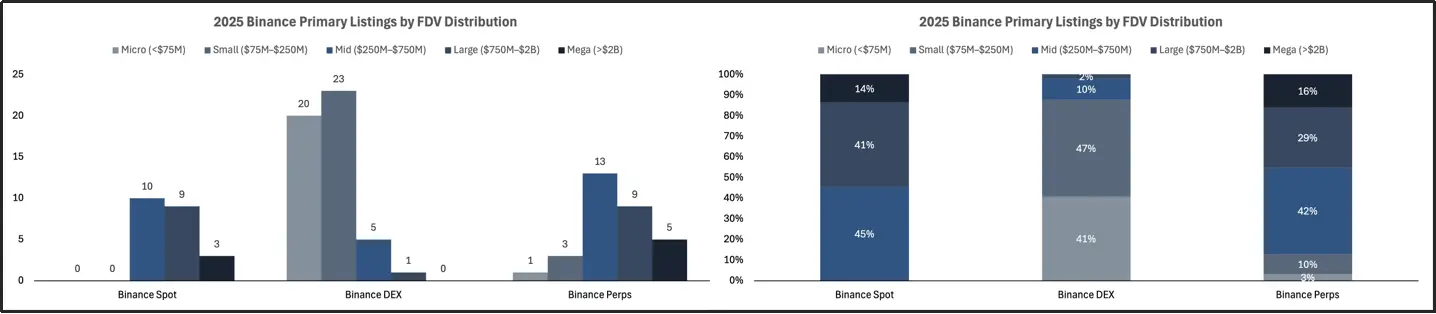

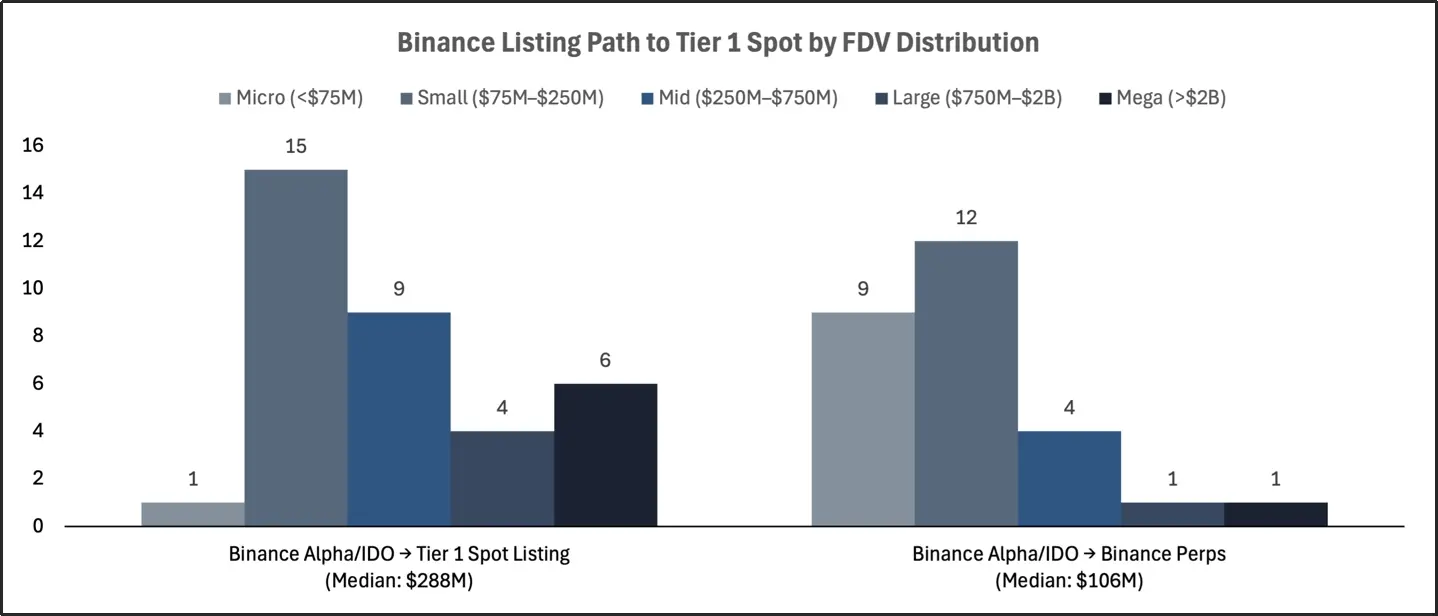

Binance's spot listing projects lean towards large caps, with no micro-cap projects; most projects have a fully diluted valuation (FDV) above $250 million, concentrated above $750 million. Alpha airdrops target small-cap projects, with about 80% of listing projects having an FDV below $250 million, and a high proportion of micro-cap projects. The range of projects for Binance IDO is concentrated, with nearly all projects having an FDV between $75 million and $250 million, none exceeding $750 million. Each of Binance's listing plans targets different market segments, with almost no overlap across FDV levels. Clearly, Binance's strategy is distinctly targeted: the spot segment focuses on scaled tokens, Alpha on early-stage projects, and IDO on carefully selected growth-stage project issuances.

The project valuation levels distributed by fully diluted valuation (FDV) for Binance's first issuance in 2025

The project valuation levels distributed by fully diluted valuation (FDV) for Binance's secondary issuances in 2025

The listing path of Binance

The listing path of Binance's first-tier spot tokens based on fully diluted valuation (FDV) distribution

This section will analyze the downstream listing paths of Binance Alpha airdrops and Binance IDOs, tracking how these tokens subsequently land on Binance perpetual contracts, Binance spot, and other first-tier centralized exchanges (CEX) such as OKX, Coinbase, Upbit, and Bithumb.

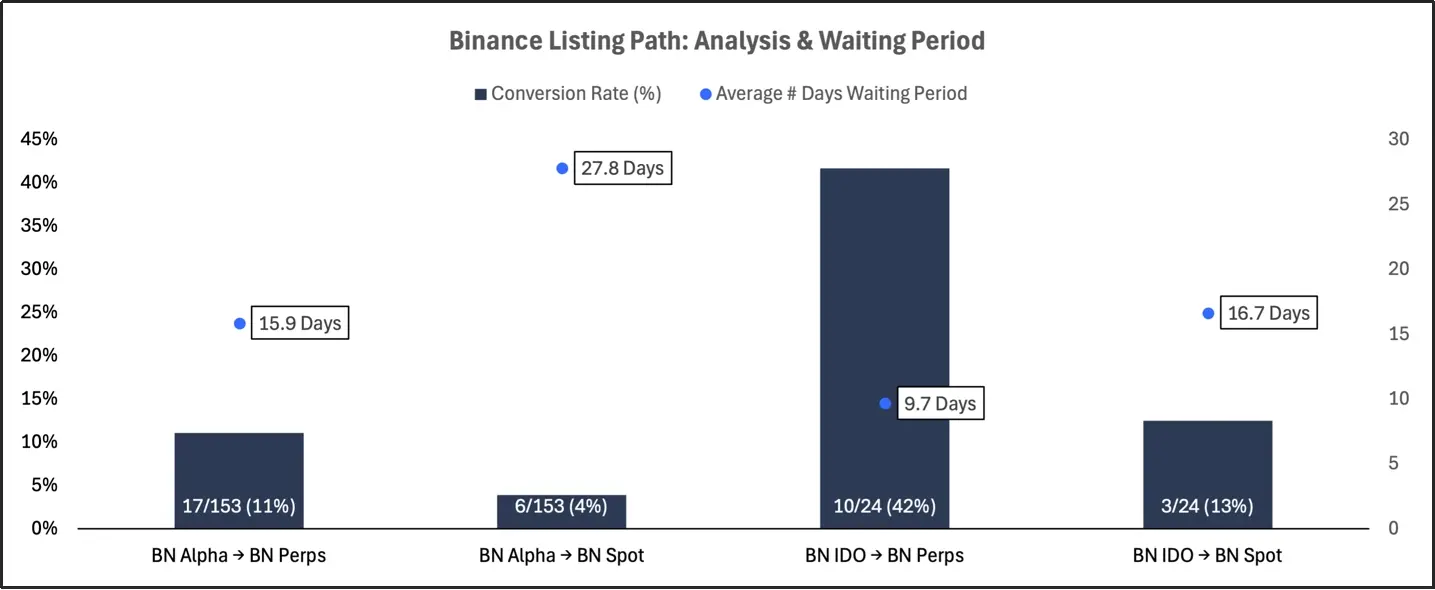

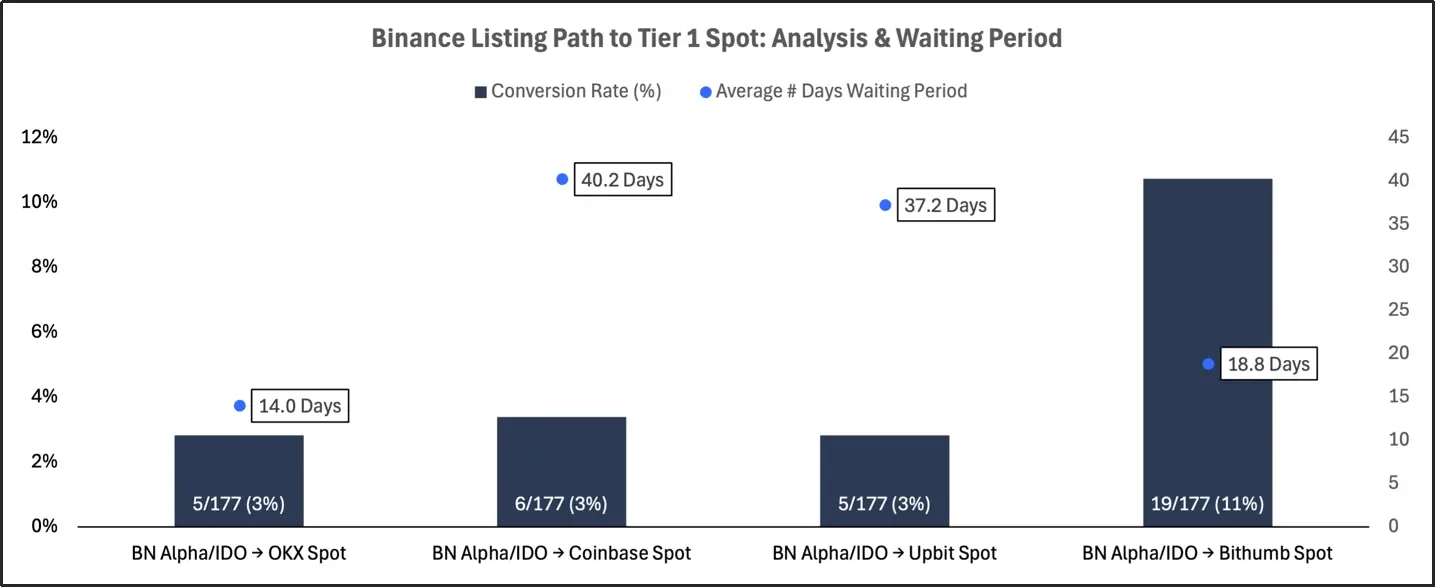

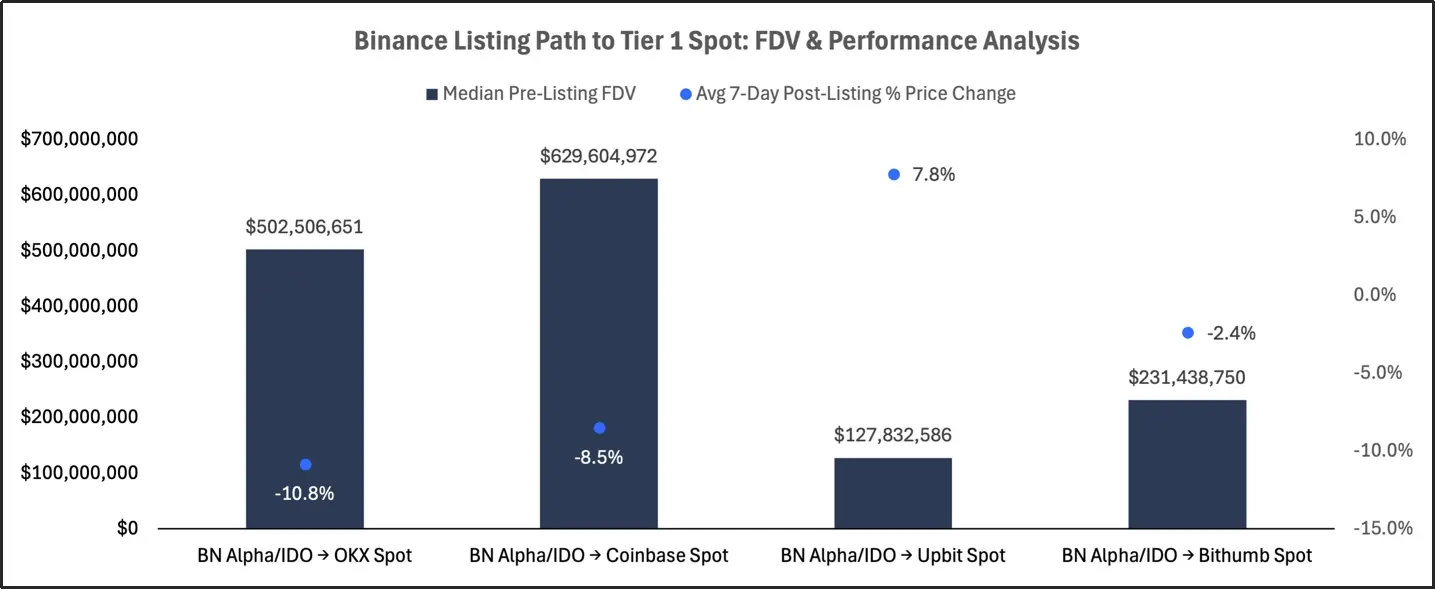

Binance's listing path: conversion rate and average waiting days

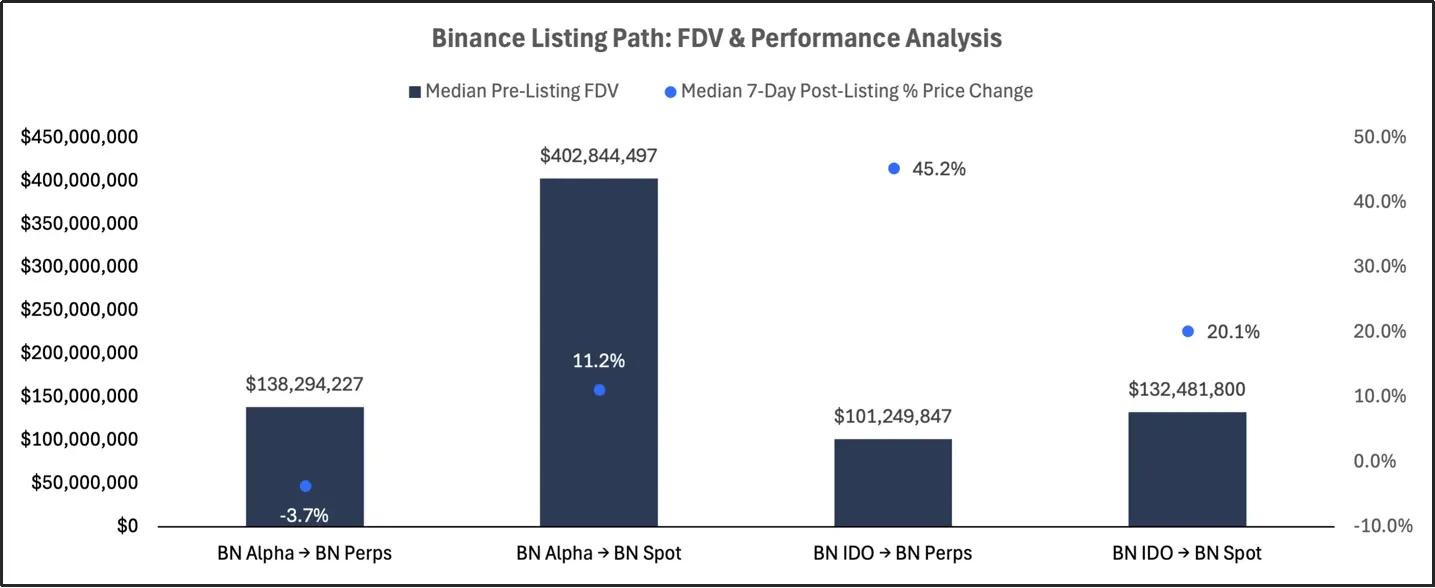

Binance's listing path: Analysis of fully diluted valuation (FDV) and performance

Binance Alpha airdrops rarely advance to quality listing stages, with a low conversion rate to perpetual contracts and spot listings; the performance after listing is generally weak; those tokens that enter the spot market via Alpha are mostly high fully diluted valuation (FDV) projects, which have some follow-up performance. In contrast, Binance IDO has significantly stronger attractiveness downstream, particularly in perpetual contract listings, with fast promotion speed and impressive 7-day returns; although transitions from IDO to spot are not common, they still outperform Alpha. Overall, Binance Alpha has low downstream conversion and performance differentiation, while IDO is a stronger path to downstream listings (especially perpetual contracts).

The listing path of Binance's first-tier spot tokens: Conversion rate and average waiting days

The listing path of Binance's first-tier spot tokens: Analysis of fully diluted valuation (FDV) and performance

Among tokens issued from Binance Alpha or IDO, those that manage to land on the spot segments of first-tier exchanges remain rare, with low conversion rates, and these tokens often experience long delays before listing on other mainstream exchanges. The performance of these tokens after landing on other exchanges is generally poor, with most return rates being negative, with only minor increases observed on Upbit. Such listings tend to favor large-cap tokens, further reinforcing the view that projects with higher fully diluted valuations (FDV) are more likely to secure more opportunities for listing on first-tier exchanges. Although listing on external exchanges can bring broader exposure, such conversions are not only rare but also often underperform, especially for high FDV projects, where liquidity events are more likely used for token distribution rather than project growth.

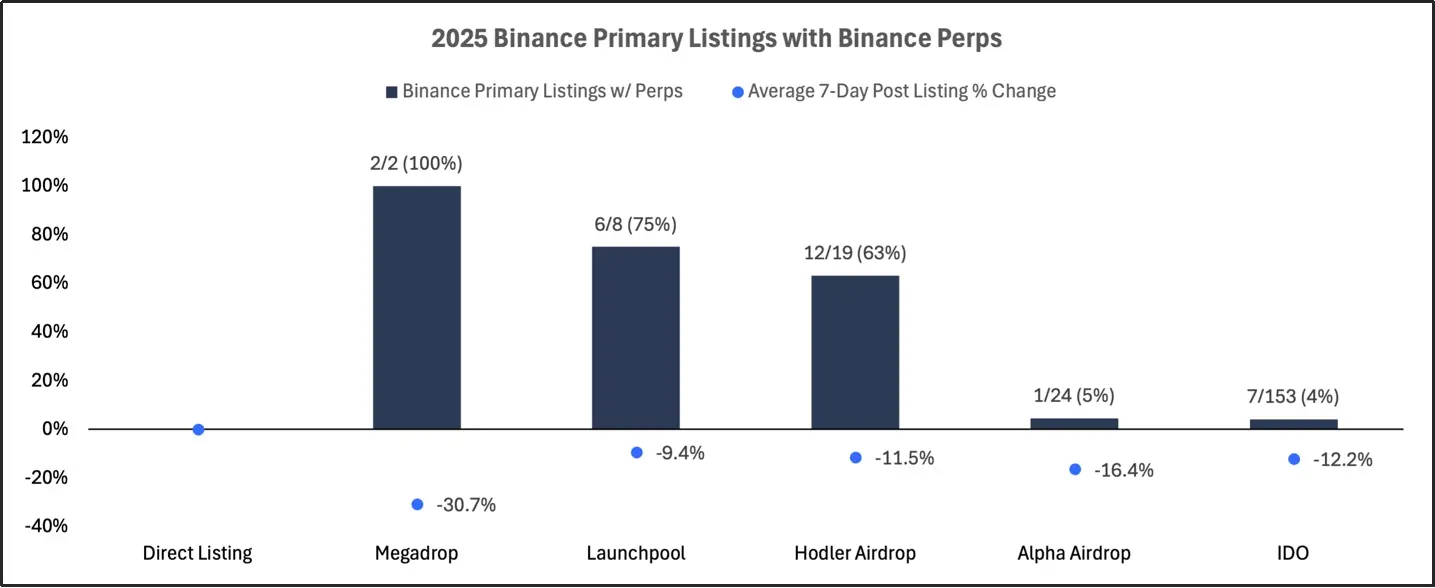

Projects that simultaneously had first listings and perpetual contract listings on Binance in 2025

The above analysis examined the projects that had both first listings on Binance and perpetual contract listings in 2025. The data shows that Binance has a clear preference for pairing perpetual contract listings with token generation events (TGE) through first-day spot projects rather than Alpha airdrops or IDOs.

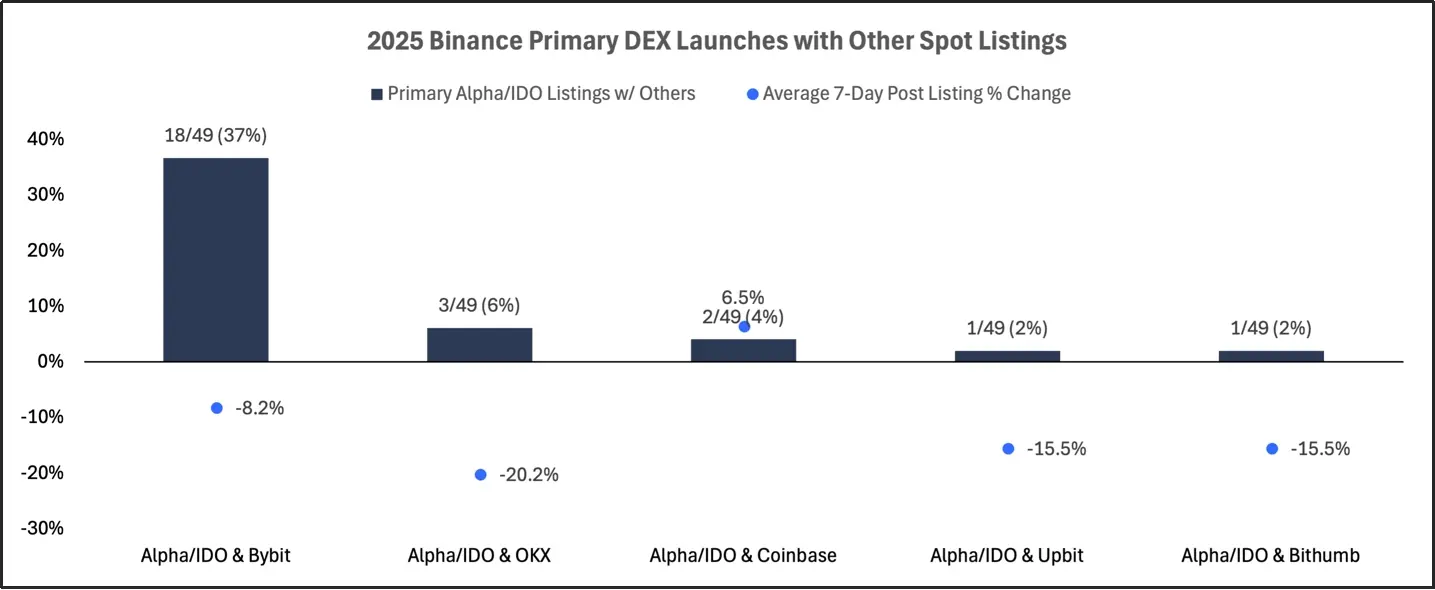

The frequency and performance of Binance's first DEX issuance projects coinciding with other exchanges' spot listings in 2025

The above chart analyzes the frequency and performance of Binance's first DEX issuance projects (including Alpha airdrops and IDOs) occurring simultaneously with spot listings on other mainstream exchanges (such as Bybit, OKX, Coinbase, Upbit, and Bithumb). The performance after these joint listings is generally poor, with the average 7-day return rate across all exchanges being negative, particularly pronounced declines seen in OKX, Upbit, and Bithumb.

Summary

In the first half of 2025, the listing landscape in cryptocurrency exchanges underwent significant changes, driven by the rise of on-chain issuance projects, the enhanced dominance of secondary listings, and clearer segmentation of different valuation levels and platforms in listing paths.

Binance continues to maintain a clear lead in total listing numbers, but its strategy has decisively shifted towards 'on-chain priority' projects—particularly Alpha airdrops and IDOs, which currently dominate new token issuance. However, the effectiveness of these projects varies greatly: while Alpha airdrops can achieve large-scale issuance, their subsequent performance and conversion are weak; in contrast, IDOs have become a more stringent but higher-performing path, especially notable in entering Binance's perpetual contracts. Among all exchanges, secondary listings consistently outperform first issuances in both 7-day return rates and peak FDV ratios, reflecting the advantages of tokens being listed after having prior liquidity and market presence. Notably, the subsequent performance of secondary listings is strongest for Binance, Coinbase, and Upbit, while OKX and Bybit lag behind.

Valuation segmentation has now deeply integrated into the project systems of various exchanges: Binance's spot listings favor large caps and high FDV tokens, while Alpha and IDO channels precisely focus on early projects and growth-stage projects, respectively. This reflects a more targeted filtering method in the token listing process and clear hierarchical differences in access to quality trading channels. Cross-exchange liquidity remains rare and slow, with only a few projects originating from Binance successfully landing on the spot segments of other leading exchanges. Even when such conversions occur, they tend to concentrate on high FDV projects, and their performance after listing often remains mediocre.

In summary, these trends highlight that the listing ecosystem is maturing, with the unprecedented importance of project types, token development stages, and listing orders. For project parties, investors, and exchanges, understanding these structural dynamics is key to navigating the increasingly tiered path from token generation to long-term exchange liquidity.